Author: Culper Research(@CulperResearch)

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: Culper Research is a well-known short-selling institution on Wall Street, having accurately targeted several prominent companies. This report directly addresses the core issues of Ethereum: the Fusaka upgrade in December 2025 brought a large amount of cheap block space, but real organic demand has not kept up—the "prosperous" on-chain data is actually fabricated by address poisoning attacks. Vitalik himself has been selling a significant amount of ETH, while Tom Lee, Ethereum's most staunch bull advocate, continues to defend it with incorrect data. This article is not a prediction; it is a well-researched short thesis with data and verification, worth reading carefully for every ETH holder.

We are shorting Ethereum and ETH-linked securities, including BMNR.

We believe that the Fusaka upgrade in December 2025 has severely damaged Ethereum's token economic model. Vitalik himself knows this and is continuously selling; meanwhile, Tom Lee, ETH's most steadfast bull, is pouring good money into a bad bet.

$ETH will continue to decline.

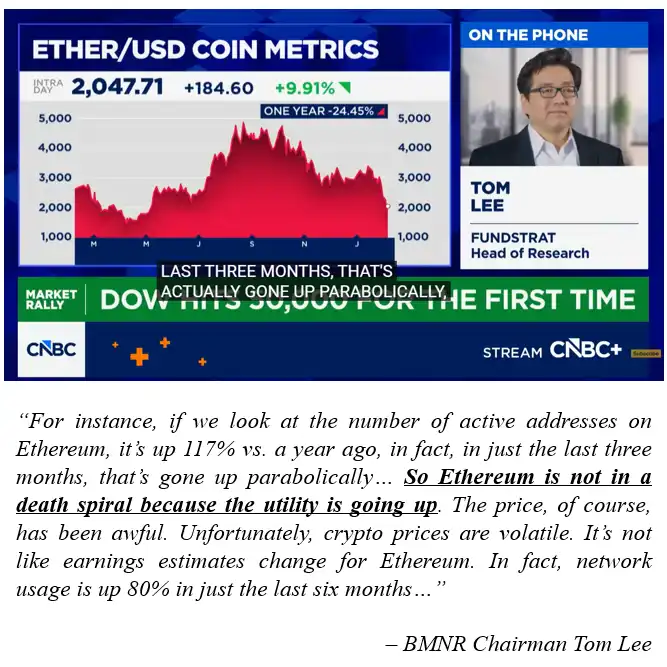

Tom Lee's Defense: Active Addresses and Transaction Volume Are Rising

Tom Lee's $BMNR defends ETH, claiming that "ETH is not entering a death spiral because utility is increasing." He cites the surge in ETH active addresses and transaction volume after Fusaka as evidence of "strengthening fundamentals" and institutional adoption.

Lee's logic is wrong.

By his own logic, if ETH's on-chain activity does not reflect real utility growth, then ETH is heading toward a death spiral.

Our research shows that this is exactly what is happening.

The full report and disclosure information are now available at culperresearch.com.

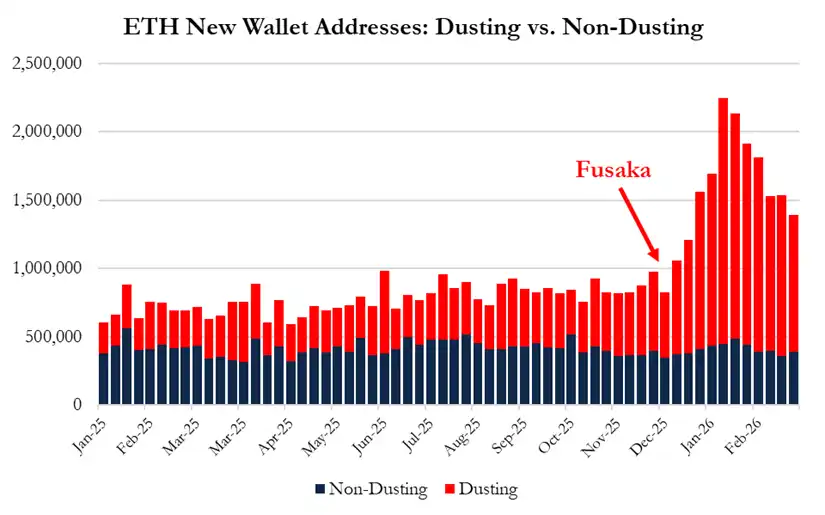

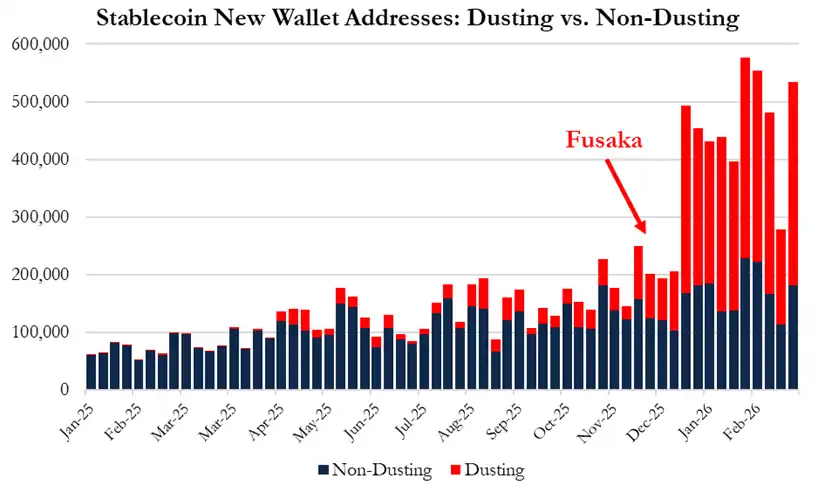

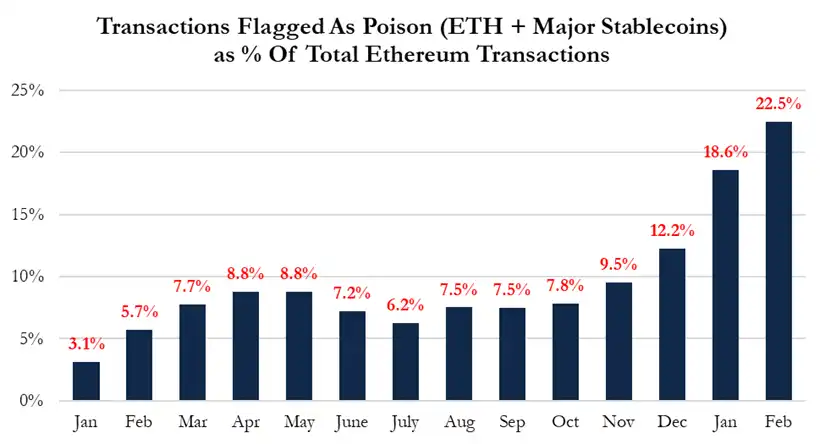

The Truth About On-Chain Data: 95% of New Wallets Are Poisoning Attacks

Our comprehensive analysis of on-chain data from January 2025 to February 2026 shows: the "institutional adoption" data cited by Tom Lee is actually explained by large-scale low-value address poisoning/wallet dusting attacks triggered by the block space surplus brought by Fusaka.

Specific data after Fusaka:

- 95% of new wallet growth is explained by newly created "poisoned" wallets

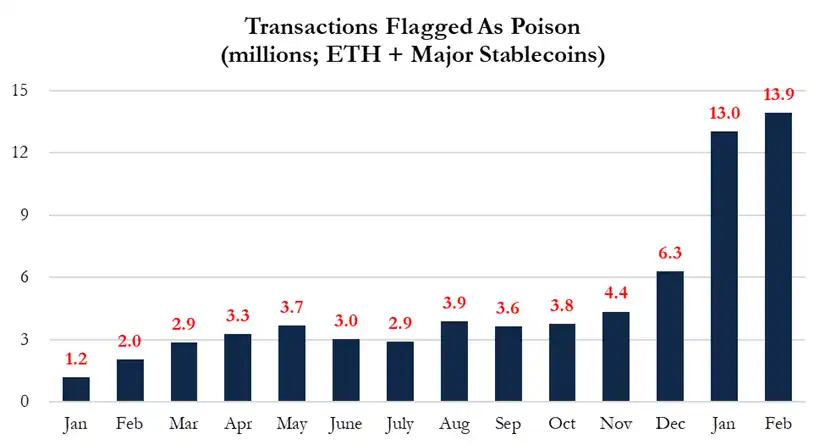

- Address poisoning attacks have increased more than 3 times

- Poisoning attacks explain over 50% of ETH transaction volume growth

- Poisoning attacks now account for 22.5% of all ETH transactions

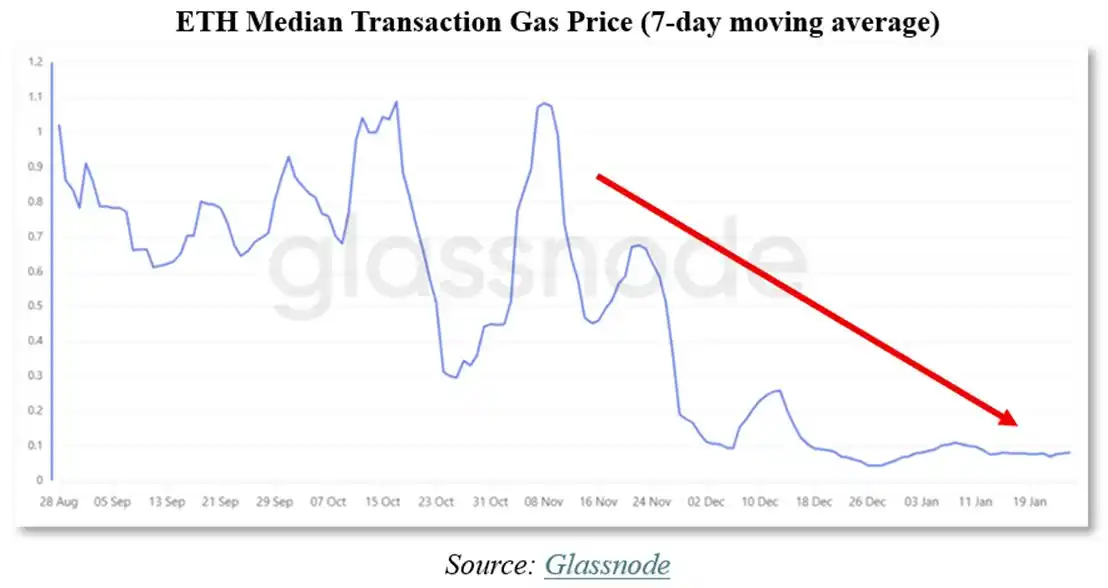

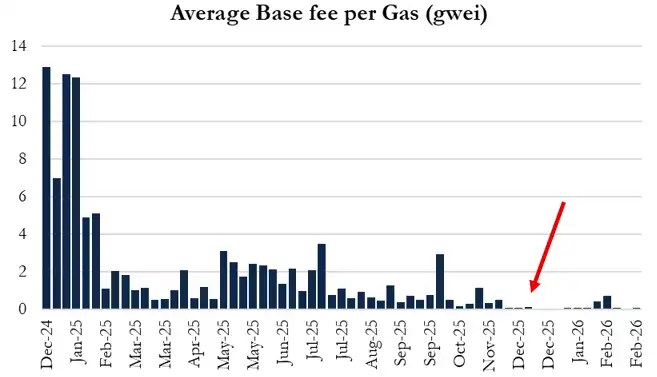

Fusaka Upgrade: Gas Fees Collapsed by 90%, 3-9 Times Worse Than Expected

Fusaka increased the gas limit from 45 million to 60 million, aiming to scale Ethereum L1. Vitalik and PTG estimated that gas fees would drop by 10-30%.

The reality is: gas fees dropped by approximately 90%.

Vitalik and the validators severely underestimated L1 demand elasticity, with an error of 3-9 times—using outdated mathematical models from before EIP-1559 and before L2s emerged.

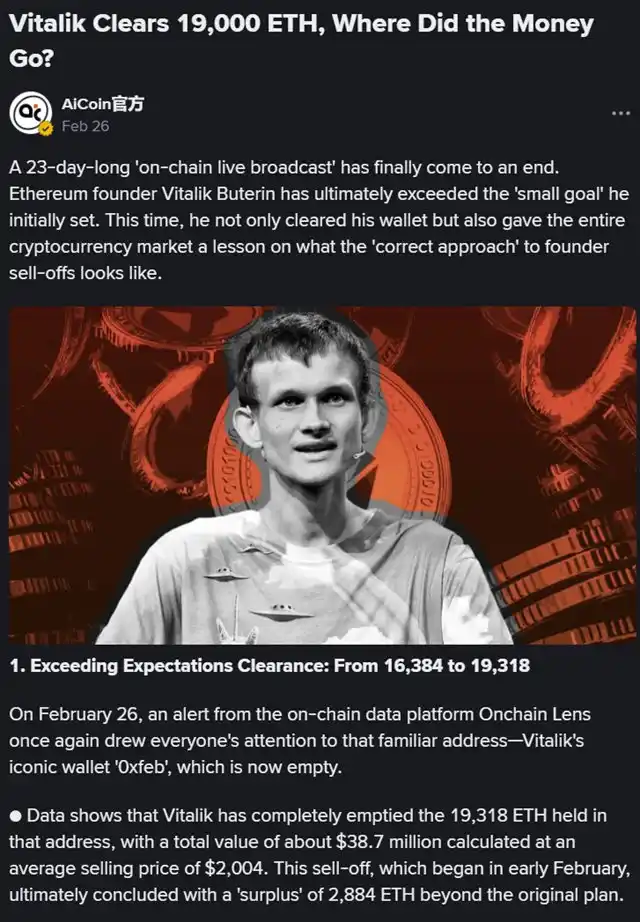

Vitalik Is Selling Like Crazy

This is why we believe Vitalik is selling ETH heavily. On January 30, he announced he would sell 16,384 ETH to fund the Ethereum Foundation's "austerity period." Since then, he has sold over 19,300 ETH and is still continuing.

He knows what Tom Lee does not: ETH's token economic model has broken.

We Personally Verified the Address Poisoning Attack

We documented the ETH address poisoning process firsthand: we created two new wallets, initiated a transfer between them, and were targeted by a poisoning attack within 5 minutes.

We encourage readers to verify this themselves.

Losses from poisoning attacks have grown at a rate more than 8 times faster than before Fusaka.

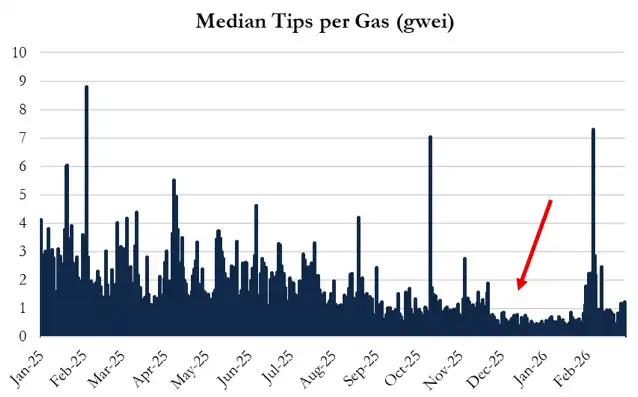

The Validator Flywheel Is Reversing

Additionally, the gas limit increase has severely impacted ETH validators, who now see a 40-50% drop in tips per unit of gas. Lower returns reduce staking demand and high-value activity, thereby weakening the foundation for institutional adoption.

The flywheel is now reversing.

Ethereum Is Losing to Solana and Its Own L2s

Meanwhile, ETH continues to lose market share:

- Solana developers grew by 29% in 2025, while Ethereum only grew by 6%; talent is draining away

- Visa and Citigroup chose Solana to build DeFi applications

- Solana DEX trading volume is now more than double that of Ethereum

Conclusion: The Next Nokia

During the internet bubble era, Netscape and Nokia dominated the market for over a decade, but ultimately, Google and Apple reaped the rewards.

We view ETH in the same light.

We believe the token economic model has broken, Tom Lee is in over his head, and $ETH will continue to decline.