Author: Deep Tide TechFlow

The long-sluggish Crypto market has welcomed another $1 billion valuation project, but this time the biggest highlight isn't the valuation itself.

On March 14, 2026, Pharos, an institutional-grade high-performance parallel Layer 1 public chain built for real finance, announced a comprehensive upgrade in capital cooperation with the Hong Kong Stock Exchange-listed company GCL New Energy (0451.HK), quickly becoming a market focus.

The market was initially drawn by the valuation: According to the latest agreement signed by both parties, GCL New Energy will complete the investment subscription in Pharos at a valuation of nearly $1 billion. The figure $1 billion was enough to ignite community discussion.

But soon, everyone discovered something even more interesting than the valuation:

According to the disclosure documents, this investment subscription is not a simple "sign and it's effective" one-time investment but is attached with multiple preconditions and tranched closing clauses. If any key condition fails, the cooperation instantly becomes a worthless piece of paper.

Simply put, signing the cooperation ≠ money actually received; everything depends on the listing price performance of the Pharos Token.

All this makes this investment subscription look less like a typical Crypto deal and more like a capital game with distinct gamble characteristics between the traditional market and Crypto: both parties aim for win-win cooperation, but with safeguards in the form of前置条件 (preconditions).

As Crypto financing, accustomed to "unconditional funding," is pulled onto the negotiating table by traditional capital, what should we expect for the subsequent market?

New Crypto Financing Play: Token-Equity Binding, Tranched Unlocking

Many compare this investment subscription to a Crypto version of a "gamble agreement" (对赌 - duì dǔ, valuation adjustment mechanism - VAM) because it captures the risk control logic of such plays well.

In traditional capital markets, VAMs are investors' favorite risk control tool: investors offer a high valuation, and entrepreneurs make a pledge (军令状 - jūn lìng zhuàng). If future KPIs are met, everyone is happy; but if things go wrong, the founder needs to buy back the shares out of their own pocket.

Traditional investment banks often focus on future revenue and profit, while Crypto focuses on a highly Web3-specific metric: token listing performance.

But if you only focus on the VAM concept, you might easily overlook the model innovation led by this transaction.

How can equity, representing traditional capital, and tokens, symbolizing Crypto capital, better integrate? Pharos and GCL New Energy have jointly provided a demonstration first: a sophisticated new capital model of mutual investment, simultaneous effectiveness, and tranched unlocking through isomorphic binding.

The first step in this structural innovation is Pharos's upfront subscription to GCL New Energy shares.

Pharos will act as a pre-investor, subscribing to new shares of GCL New Energy at HK$1.05 per share, with a maximum subscription quota of 183,480,000 shares (equivalent to about 10% of GCL New Energy's shares). Compared to GCL New Energy's stock price of about HK$1.23, this subscription gives Pharos a discount of about 15%.

But at the capital table, there are no free chips.

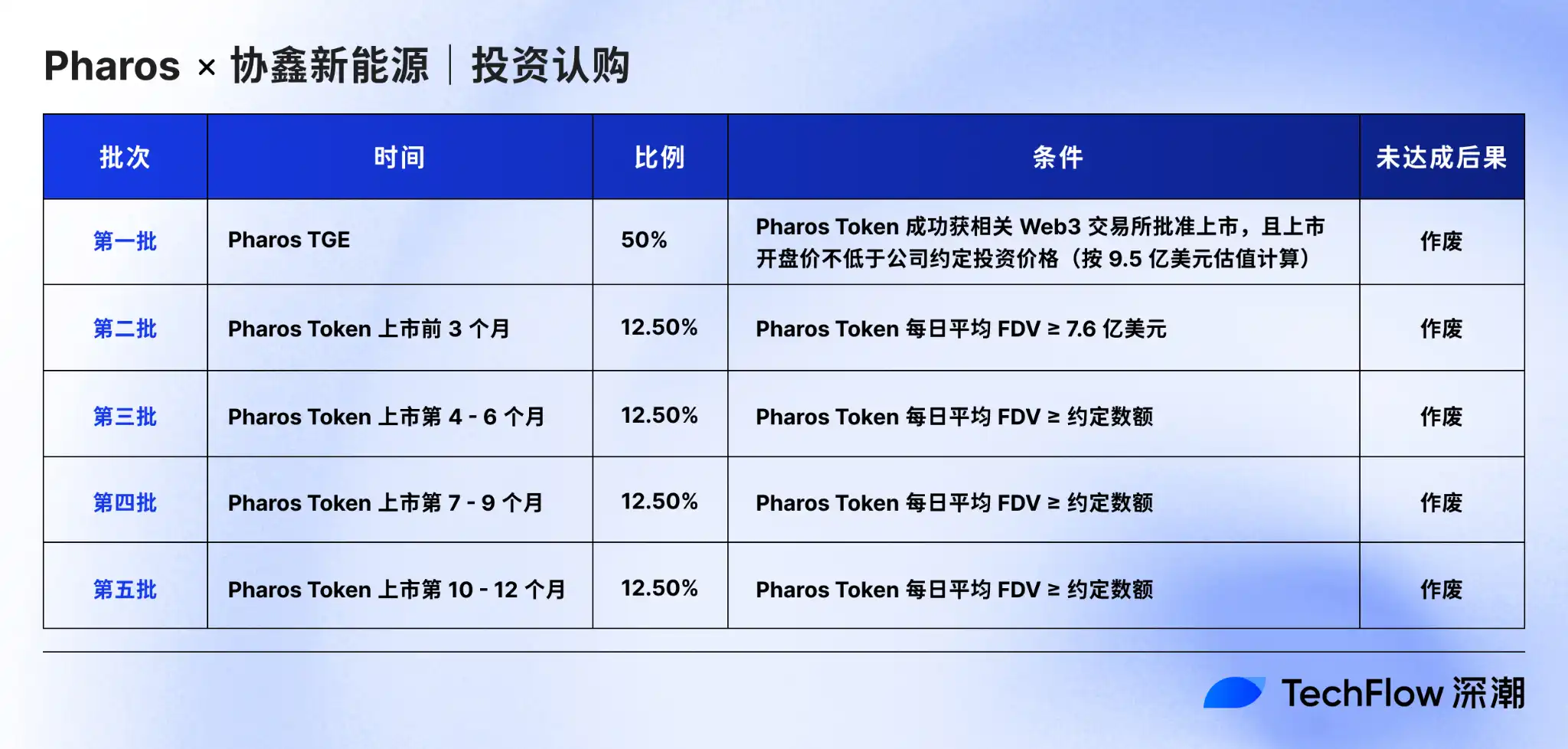

To truly pocket these discounted shares, Pharos must, within an 18-month validity period, meet the "five-step" closing conditions proposed by GCL New Energy, each step closely watching the future market performance of the Pharos Token.

And once the Pharos Token meets the closing conditions, Pharos's share subscription in GCL New Energy will take effect accordingly, and simultaneously, GCL New Energy's subscription for Pharos Token will also take effect, with the same unlocking ratio.

Under this two-way binding:

- If the Pharos Token performance meets the standard, both equity and tokens are delivered together;

- If the Pharos Token performance falls short of expectations, both equity and tokens stall together.

Taking the most critical first tranche as an example, after the successful listing of the Pharos Token and its opening price meeting the target, Pharos will immediately deliver 50% of the share subscription to GCL New Energy, while GCL New Energy will acquire Pharos Tokens worth approximately HK$96.73 million at a valuation of $950 million.

Under such an investment subscription agreement, coupled with Pharos's previous announcement that Anchorage Digital will provide regulated minting, distribution, and custody services for the Pharos TGE, Pharos may now be in the countdown phase, infinitely close to its TGE.

Mutual Benefit: One Agreement, Two Ways to Win

This special investment subscription transaction happens at a微妙 (subtle/delicate) point in time.

Past experience has taught us that the old financing logic of Crypto using whitepapers to tell stories and liquidity imagination to support valuations has失效 (become ineffective). The market has seen too many bubbles and too many crashes. What we need now is a vivid demonstration that simultaneously possesses real assets, a compliance framework, and on-chain imagination.

And the deal between Pharos and GCL New Energy is恰好 (exactly) that demonstration.

Behind the complex terms lies the interest game where both parties try to lock what they care about most into the contract:

For GCL New Energy, this is an excellent model that allows them to attack and defend effectively (进可攻、退可守).

Investing in Pharos is an active bet on the on-chain narrative, while introducing the VAM form effectively controls risk. If Pharos underperforms, GCL can withdraw in time. But if Pharos performs excellently, GCL can not only receive real capital injection but also acquire tokens with high appreciation potential at the initial valuation.

For Pharos, the value of this transaction is far more than just adding a partner.

The first gain is trust endorsement. A Hong Kong-listed company is willing to bind its shares with Tokens, which in itself is the most significant public recognition for Pharos.

The second gain is a confidence proof. Pharos's agreement to this series of strict closing conditions largely signals to the market the project's confidence in its future development. This posture is more convincing than any technical whitepaper.

The third gain is the historical position as an "industry first." Over the past year, we have seen too many DAT model cases where traditional listed companies purchase crypto assets. This time, the direction is reversed: Through this subscription, Pharos directly enters the shareholder ranks of GCL New Energy, becoming the first Crypto project to strategically hold shares in a traditional Hong Kong-listed company in reverse.

In a significant sense, this represents the first time a quality Crypto project from the加密世界 (crypto world) has obtained a real negotiating seat and pricing power in the traditional capital market. Meanwhile, this transaction has also received support through an HKEX announcement, demonstrating Hong Kong's foresight in embracing compliant Crypto innovation and injecting a strong compliance background into this deal.

One contract, two ways to win.

In striving for a win-win and avoiding a lose-lose situation, it also makes more people curious about the two leading protagonists behind this model innovation.

After all, Hong Kong-listed companies are known for strict risk control and conservative作风 (style). Why did Pharos dare to write future price performance into the contract, and why did GCL New Energy dare to bind the listed company's shares with a token that hasn't yet completed market validation?

A closer look reveals that behind this seemingly bold attempt at a cross-border联姻 (alliance/marriage), lies the inevitability of a双向奔赴 (two-way rush / mutual attraction).

Mirror Complementarity: The Inevitable Rendezvous of Pharos and GCL

On one end of the table in this model innovation is GCL New Energy.

As a leading Asian photovoltaic company, its core business focuses on the development, construction, operation, and management of solar power stations (photovoltaic power stations),同时涉及 (also involving) electricity sales and solar-related services. Although it holds the highest quality green assets, it also suffers from the common problems of traditional assets: long construction cycles, slow return realization, and increasingly fierce financing competition.

What GCL needs more is not another power station, but a financial tool that can reorganize, recirculate, and revalue these off-chain assets.

On the other end of the table is Pharos.

As a parallel L1 focused on institutional-grade scenarios, Pharos was clear from its birth: not to build another higher-performance public chain, but to致力于 (dedicate itself to)承接 (undertaking/ hosting) more real things, including stablecoin settlement, institutional-grade DeFi, regulation-friendly payment networks, and the on-chain circulation of RWA, especially energy, commodity, and infrastructure assets. Simply put, Pharos aims to become the infrastructure that can truly support the real finance narrative.

Performance is the premise supporting the "RealFi infrastructure" vision. Pharos, based on a modular + deep parallel execution engine design, boasts advantages like sub-second finality, high throughput, and low fees,能够更好的支撑 (can better support) the on-chaining, circulation, and real-time settlement of assets.

Facing the compliance issues that institutions care deeply about when going on-chain, the Pharos protocol layer has built-in ZK-KYC/AML, digital identity, supports regulation-friendly features, while remaining open.

Even before the cooperation with GCL New Energy, Pharos had already won the favor of capital and institutions:

According to public information, Pharos completed two rounds of financing in November 2024 and September 2025, receiving support from知名 VC (well-known VCs) like Hack VC and Lightspeed Faction.

Regarding institutional cooperation, Pharos previously announced a partnership with the decentralized financial platform Centrifuge. By combining Centrifuge's institutional-grade tokenization infrastructure and asset standards with Pharos's "inclusive and execution-first" Layer 1, they aim to further achieve the规模化分发与运营 (large-scale distribution and operation) of a series of institutional-grade assets on-chain, including tokenized U.S. Treasury bonds (JTRSY) and AAA-rated structured credit products (JAAA).

Putting the two counterparties together, one finds an镜像般的互补 (almost mirror-like complementarity) between GCL New Energy and Pharos.

For GCL New Energy, it wants to find a Crypto vehicle that can open up Web3, RWA, and market revaluation space, transforming offline heavy assets into new capital forms on-chain;

For Pharos, it needs a traditional capital entry point that can承接 (accommodate) high valuation, compliance narrative, and real asset imagination, grounding the on-chain story in real assets.

Therefore, from this perspective, this investment subscription is less of a cooperation and more of an inevitable rendezvous.有趣的是, (Interestingly,) Ant Group, with whom both parties have交集 (intersections/connections), is jokingly called by many netizens the隐形桥梁 (invisible bridge) for this rendezvous.

As early as December 2024, GCL Energy Technology (affiliate) cooperated with Ant Digital Technologies to complete China's first RWA cooperation for photovoltaic green assets exceeding RMB 200 million. In June 2025, the two even established a joint venture, "Ant Xin Neng," to further explore scenarios like Energy AI + RWA.

Meanwhile, we know that Pharos's co-founder and several members come from Ant Group. Ant Group's AntChain has extensive ToB landing experience in the enterprise blockchain field. This might further bring Pharos more solid technical implementation capabilities and richer institutional resource integration capabilities when solving institutional RWA needs, also indirectly foreshadowing the cooperation between Pharos and GCL.

But if this transaction is only understood as a capital binding, its potential might be underestimated. As the cooperation is signed, the subsequent cooperation structure, asset on-chain path, and more innovative cooperation directions are the bigger story.

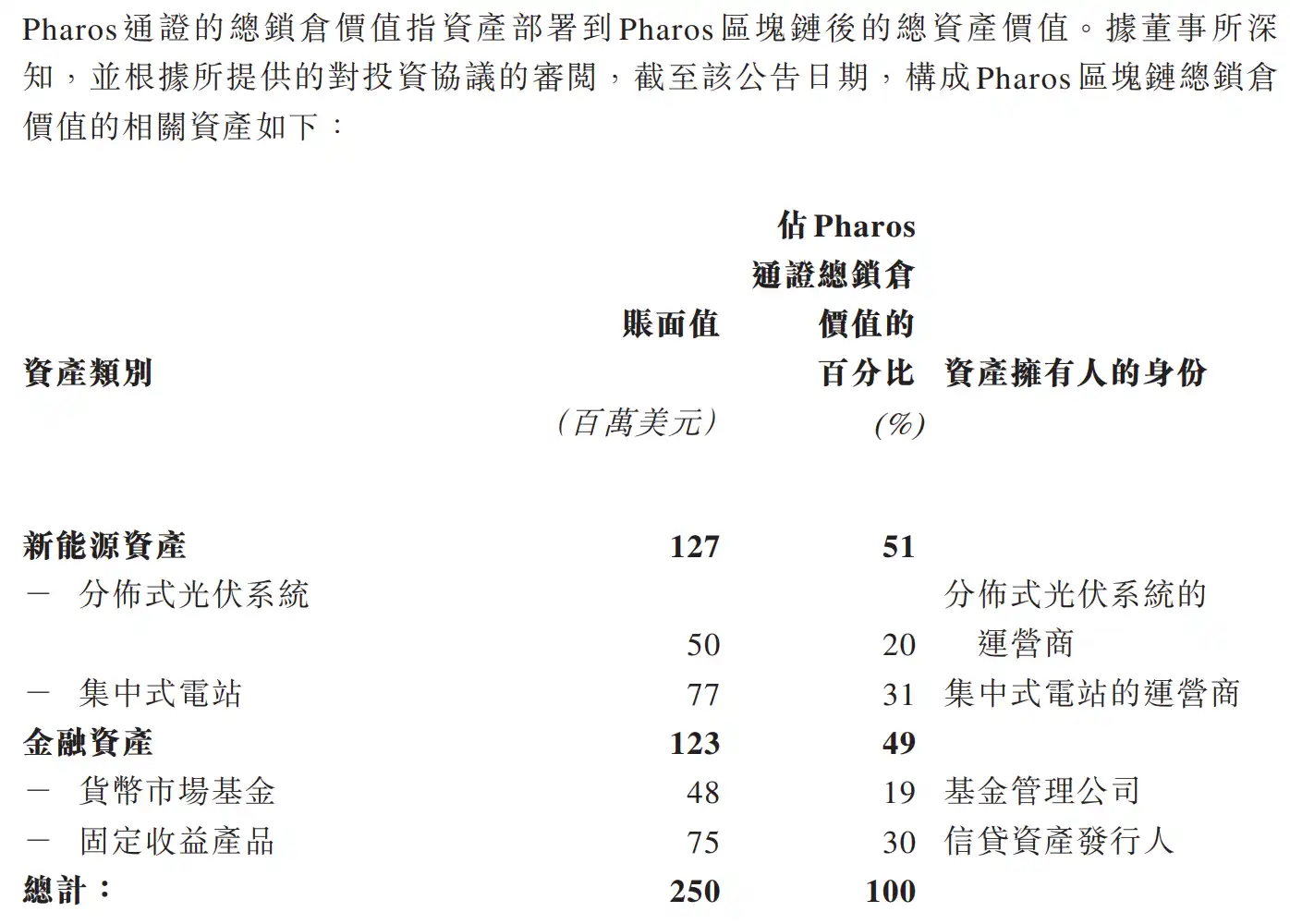

According to the types of on-chain locked assets announced by Pharos, we can see that currently, among all Pharos's locked assets: 51% come from new energy assets of distributed photovoltaic operators and centralized power station operators; 49% come from financial assets of fund management companies and credit asset issuers.

This largely indicates that the assets owned by GCL, such as photovoltaics and new energy power stations, will almost certainly be put on-chain through Pharos in the future.

This means that in the future, high-quality green energy assets in Asia, represented by GCL New Energy, will be able to break through geographical restrictions and connect with the global market more efficiently on-chain. Simultaneously, Pharos will also strive to introduce high-quality RWA assets from Europe and America to Asia, enhancing the global asset allocation capabilities of Asian investors.

Whether pushing out or bringing in, this binding model built on equity, Token, and asset synergy may release growth momentum far exceeding that of a mere subscription itself.

Conclusion

Of course, everything is at a very early stage.

In the present,高度不确定 (highly uncertain) about the future, it is perfectly normal to have voices of concern and doubt.

Some community members believe that, according to the document disclosure, Pharos's nearly $1 billion valuation is calculated based on the current total value of locked assets of $250 million disclosed unilaterally by the project party, lacking real market endorsement.

Others worry that the conditional tranched delivery model will create excessive pressure on the secondary market for the Pharos Token. While the mainnet is not yet launched and the token is not released, we can regard this as a confidence bet, but it is also uncertain whether this will become a提前透支 (pre-overdraft) of confidence in the future.

But different voices恰好证明 (precisely prove) the community's attention to the subsequent development of the event itself. At the same time, none of this prevents us from seeing the model innovation through this token-equity cooperation:

In the past, Crypto financing was more accustomed to first getting money with a good story, then using that money to prove itself;

Now, the cooperation between Pharos and GCL New Energy, by leading innovation, sends a strong signal: the next phase of Crypto might compete on who dares to write the story into a contract, hand the narrative to the market, and turn promises into reality that must be fulfilled.

In the bubble era, the most expensive thing was imagination; in the revaluation era, the most expensive thing is the ability to deliver (兑现力 - duì xiàn lì).

And this, perhaps, is the real value this investment subscription leaves for the industry.