Written by: Cointelegraph

Compiled by: AididiaoJP, Foresight News

Key Summary

- A brief 2.85% pricing deviation in wstETH collateral triggered approximately $27 million in liquidations on Aave. This event demonstrates that even minor technical issues in automated DeFi lending systems can lead to significant financial impacts.

- This wave of liquidations occurred because the Aave system briefly valued wstETH at approximately 1.19 ETH, while its market value was near 1.23 ETH, causing some borrowing positions to be mistakenly judged as undercollateralized.

- Price oracles are critical DeFi infrastructure, responsible for transmitting external market data to smart contracts to determine collateral value, assess loan health, and trigger automatic liquidations.

- The root cause was not a failure of the price data source, but a misconfiguration of Aave's CAPO risk oracle module. Outdated smart contract parameters within this module set a temporary cap on the token's exchange rate.

DeFi protocols rely on automated logic to handle everything from collateral management to risk assessment. While this mechanism builds a truly open, permissionless financial system, it also means that minor technical problems can quickly escalate, causing severe financial turmoil.

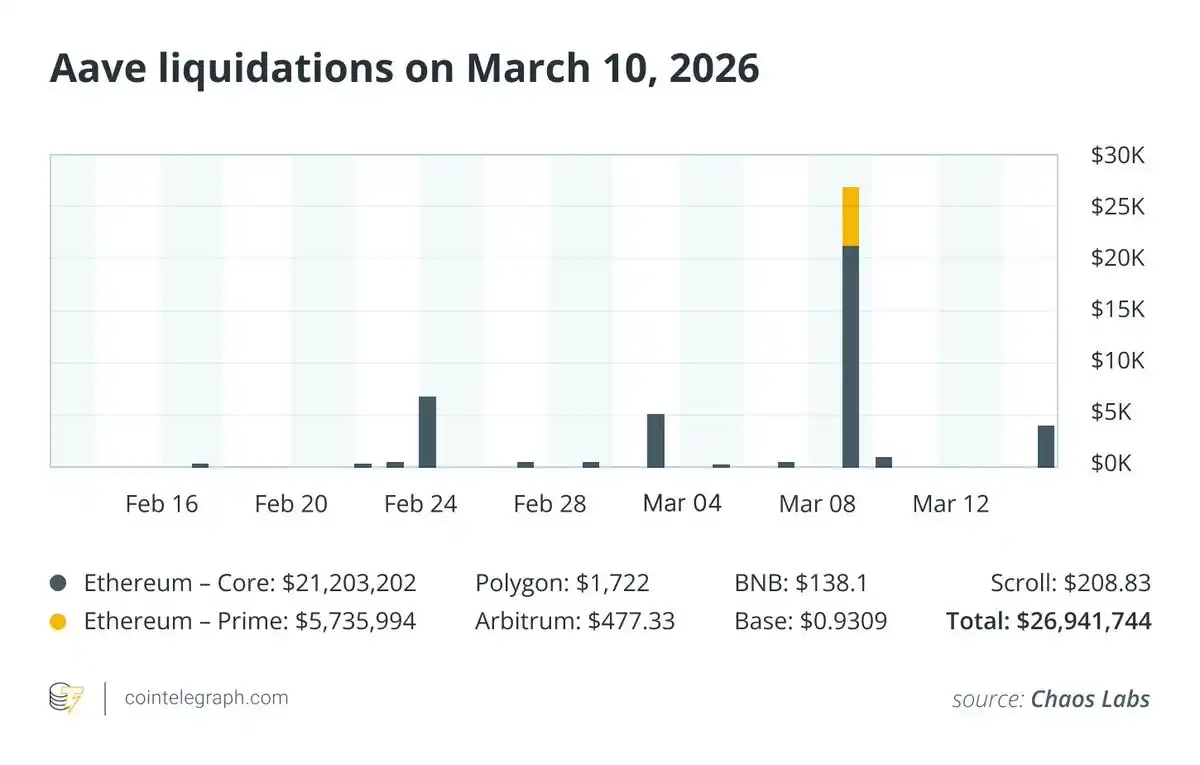

As reported by risk monitoring firm Chaos Labs, the market downturn on March 10, 2026, triggered approximately $27 million in borrower position liquidations on Aave, clearly demonstrating this fragility. Within 24 hours, user positions worth about $27 million were liquidated. Surprisingly, this event was not caused by a large-scale market sell-off but by a brief 2.85% price deviation in wrapped staked ETH (wstETH) collateral.

This event is a powerful reminder that the reliability of price oracles and a robust risk management framework are crucial for maintaining the stability of the DeFi ecosystem.

This article explains how a 2.85% pricing deviation in wstETH collateral triggered approximately $27 million in liquidations on the Aave lending protocol. It focuses on analyzing how oracle configuration, smart contract parameters, and automatic liquidation mechanisms amplified a minor pricing error in the DeFi market.

The Sudden Surge in Liquidations

When a wave of liquidations appeared on the Aave market, Chaos Labs, which closely monitors abnormal activity on lending protocols, quickly identified and reported the situation. Initially, market observers speculated that a price oracle failure might have caused the mispricing of collateral assets on the platform.

Price oracles play a key bridging role, providing external market prices for on-chain applications. In lending protocols like Aave, this price data directly determines whether a borrower's collateral is sufficient to cover their loan. Once the collateral value falls below the required safety threshold, the system automatically liquidates the position.

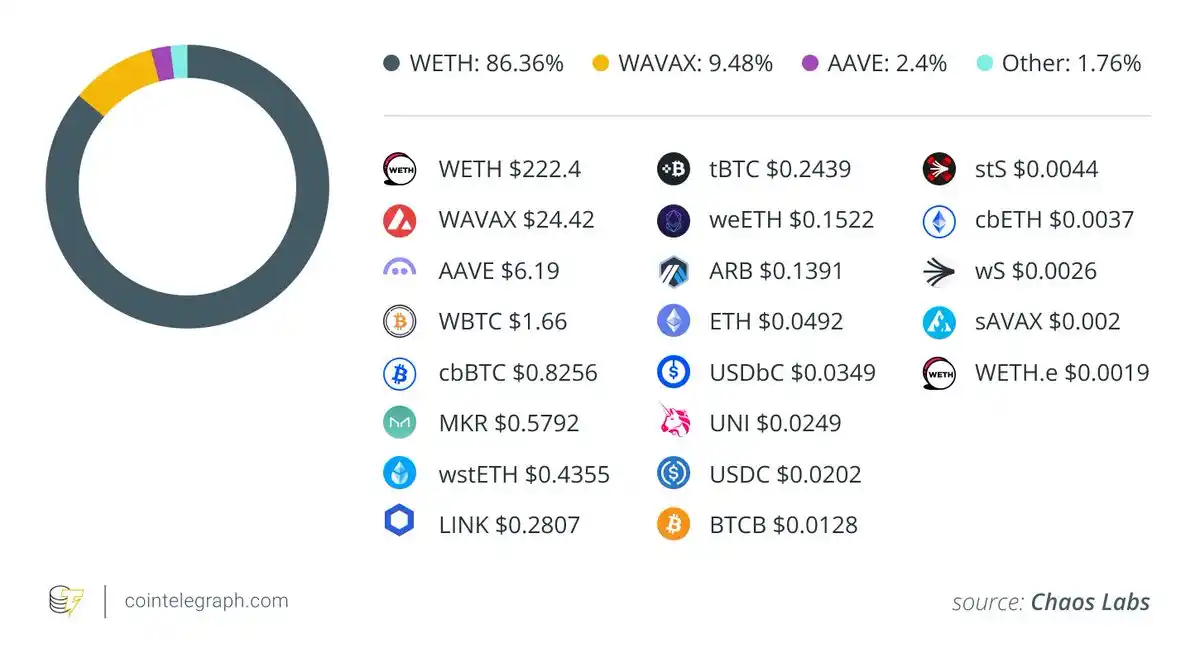

The core asset in this event was wstETH, a token widely used as collateral in the DeFi lending ecosystem.

Liquidation speeds on lending protocols like Aave are typically much faster than traditional margin calls. Because DeFi markets operate 24/7 through automated smart contracts, once the collateral ratio falls below the specified threshold, positions can be liquidated within seconds.

What is wstETH?

wstETH (wrapped staked Ether) is a token issued by the liquid staking protocol Lido.

When users stake Ether through Lido, they first receive stETH, a token representing their staked ETH principal and accumulated staking rewards. To enhance compatibility with various DeFi applications, stETH can be "wrapped" into wstETH.

Due to the continuous accumulation of staking rewards, the value of 1 wstETH is typically slightly higher than 1 ETH. This characteristic makes it an attractive and widely adopted type of collateral in the DeFi lending market.

The Pricing Deviation Event

During this liquidation wave, a deviation emerged between the actual market value of wstETH and the valuation used by Aave's risk system. Aave's algorithm priced wstETH at approximately 1.19 ETH, while the broader market valuation at the time was around 1.23 ETH.

The valuation difference of about 2.85% made positions collateralized with wstETH appear more undercollateralized than they actually were.

Consequently, some borrowing positions fell below the required safety threshold, triggering Aave's automatic liquidation process.

Why Price Oracles are Crucial in DeFi

Price oracles are the underlying infrastructure of DeFi. Because blockchains themselves cannot access real-world market data, they must rely on oracle services to provide external price information for assets. This price data directly impacts:

- Valuation of collateral

- Health of borrowing positions

- Decision-making basis for triggering liquidations

Once a reported drop in collateral price occurs, the protocol may judge the loan as undercollateralized and automatically liquidate the relevant position.

Because this mechanism is entirely algorithm-driven, even minor pricing deviations can trigger serious chain reactions.

In the DeFi space, minor price deviations can also have huge impacts. Brief fluctuations in oracle prices or market prices, even by just a few percentage points, can trigger cascading liquidations. This risk is particularly pronounced when a large number of borrowers use highly leveraged positions collateralized by volatile cryptocurrencies.

The Real Cause: CAPO Risk Oracle Misconfiguration

In-depth investigation confirmed that Aave's main price oracle was functioning normally.

The problem actually lay in the "Correlated Asset Price Oracle" (CAPO) risk module, an additional protection layer for specific assets.

The primary function of CAPO is to set a rate cap on the value increase of yield-bearing tokens like wstETH, aiming to guard against sudden price spikes or potential oracle attack risks.

However, in this event, inconsistent configuration within the CAPO module led to the problem.

Technical Analysis of the Error

Chaos Labs disclosed that the problem stemmed from outdated parameters stored in the smart contract.

Two key parameters failed to update synchronously:

- Reference exchange rate

- Timestamp associated with that rate

Because these two parameters were not refreshed in sync, the CAPO calculated an allowed exchange rate cap that was temporarily lower than the actual market rate at the time.

This caused the protocol to value wstETH approximately 2.85% lower than the market price.

Aave relies on price oracles, which are data sources that provide real-time asset prices to smart contracts. If these data sources briefly reflect anomalous market prices from exchanges, the protocol automatically recalculates collateral values and may trigger liquidations.

The Chain Reaction of Liquidations

Once the collateral ratio fell below the safety threshold, Aave's automatic liquidation engine immediately activated.

Liquidators (typically high-speed trading bots) quickly stepped in, repaying part of the borrower's debt in exchange for the corresponding collateral at a predetermined discount.

In this event, a total of approximately $27 million in borrowing positions were liquidated.

Liquidators exploited this brief price misalignment, collectively profiting about 499 ETH (including liquidation bonuses).

No Bad Debt Incurred by the Protocol

Despite the large scale of liquidations, the Aave protocol itself did not incur any bad debt. Aave founder Stani Kulechov stated, "No impact on the Aave protocol."

Chaos Labs pointed out that once positions breached the safety threshold, the platform's core risk control and liquidation mechanisms all operated as designed. Therefore, the impact of this event was limited to the relevant borrowers and did not threaten the overall solvency and stability of the Aave protocol. It was the brief, artificial depression of the collateral value that caused some borrowing positions to fall below the liquidation line.

The Aave governance layer subsequently proposed compensating affected users by utilizing recovered funds and the Decentralized Autonomous Organization (DAO) treasury. This approach reflects a new trend in DeFi governance: protocols are beginning to view such technical events as systemic infrastructure risks and tend to compensate受损 users rather than having them bear the full loss.

Another Warning on DeFi Oracle Risks

This event highlights that oracle mechanism design is both one of the most critical links in DeFi infrastructure and one of its most vulnerable weak points.

When automated mechanisms manage tens of billions of dollars in collateral value, even minor configuration errors can trigger consequences far exceeding expectations.

Similar events have occurred on other DeFi platforms. For example, one platform once briefly valued Coinbase's wrapped staked ETH (cbETH) at approximately $1 (actual value ~$2200) due to an oracle configuration error, causing widespread chaos.

These cases all indicate that maintaining reliable, accurate price data sources remains an ongoing challenge in decentralized financial systems.

wstETH and Lido Itself Are Not Responsible

Contributors related to the Lido ecosystem clearly stated that these liquidations were not caused by any failure or defect in the wstETH token itself.

The token functioned normally throughout the event, and the underlying Lido staking protocol remained fully available and unaffected.

The core of the problem lay in how the Aave lending protocol, through its own risk management configuration, processed and interpreted the price data, which deviated.

Implications for the Development of DeFi

As decentralized finance continues to develop, protocols are deploying increasingly sophisticated risk management systems to accommodate yield-bearing assets like wstETH.

These assets present unique pricing challenges because their value continuously grows with the accumulation of staking rewards.

Therefore, effective risk models must properly handle the following elements:

- Dynamically changing exchange rates

- Continuously accumulating staking rewards

- Time-dependent parameter updates

- Precise synchronization of various smart contract parameters

Even minor inconsistencies between these elements can escalate into large-scale liquidation events.