Author:Zhou,ChainCatcher

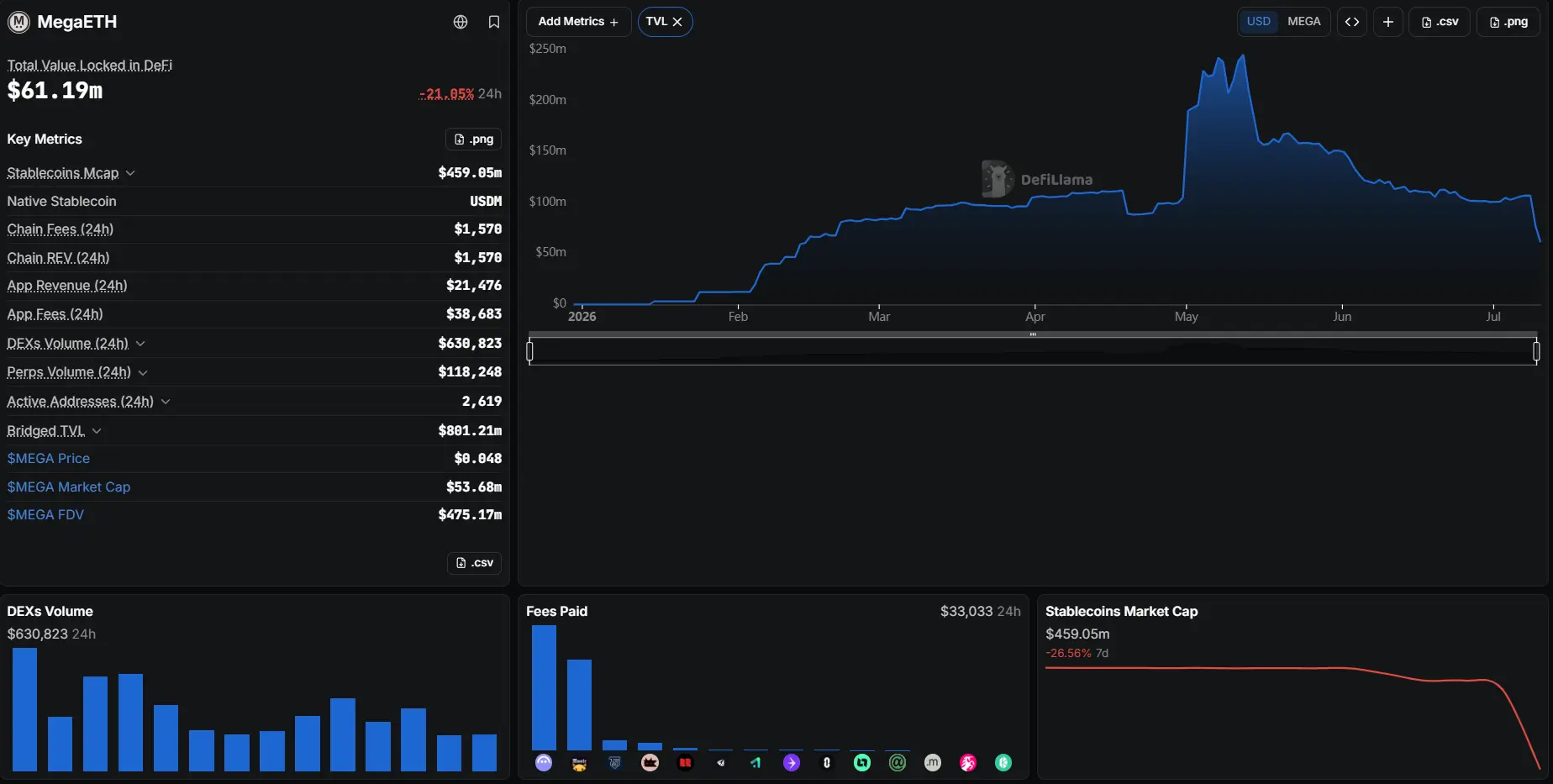

According to the latest data from DefiLlama, the full-chain TVL of MegaETH experienced violent fluctuations from July 9 to 10, once falling to just over $30 million, a drop of nearly 60% in 24 hours. Compared to the peak in May, it has evaporated about 70%. On-chain, the leading protocol Aave V3 withdrew 80% of its liquidity within the day.

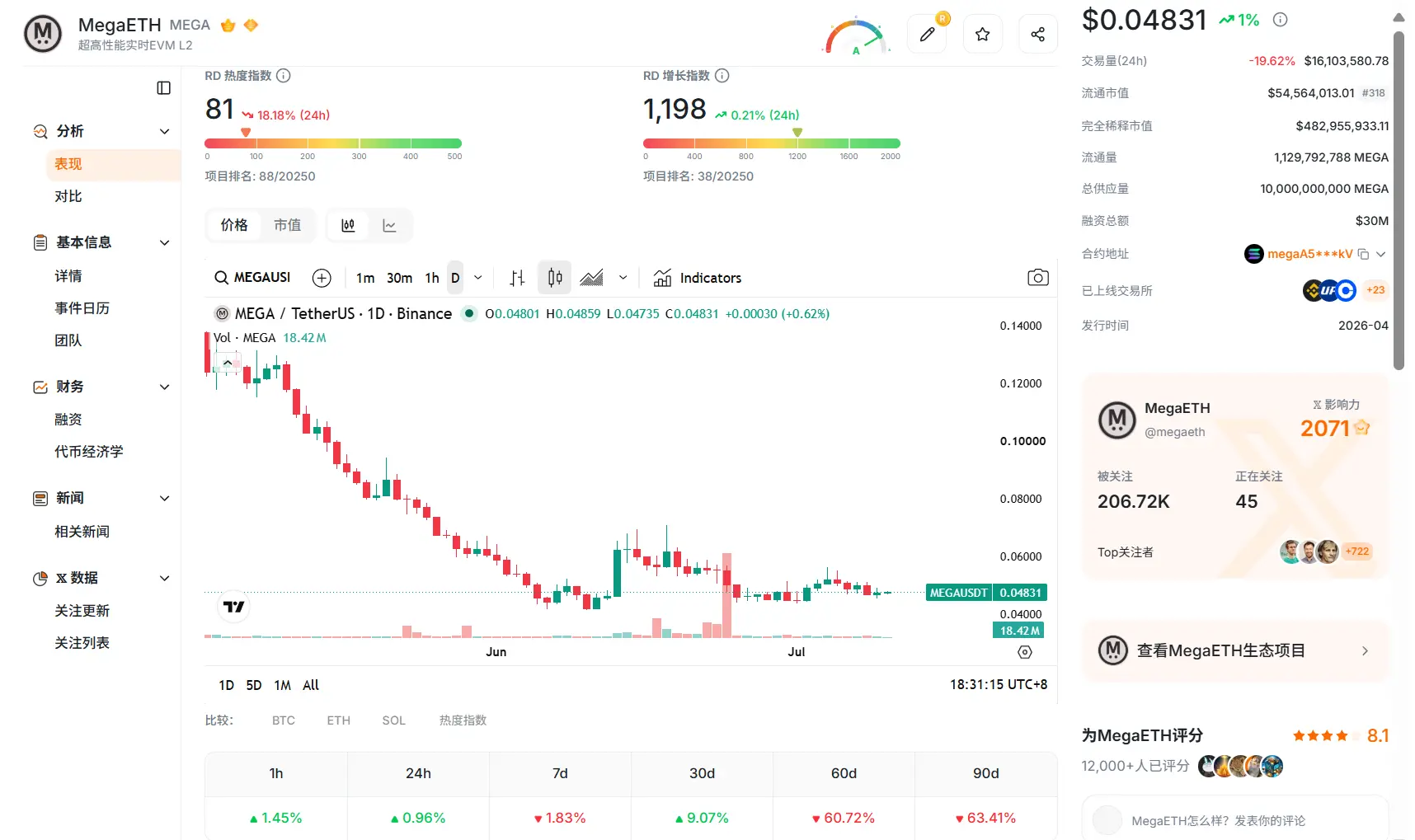

In terms of market performance, the MEGA price fell to around $0.048, with a market cap of only about $54 million and an FDV of approximately $4.8 billion.

MegaETH was once one of the most anticipated new public chains in this cycle. It hit market trends upon launch, backed by an impressive VC lineup and KOL's enthusiasm for new token listings, with its token FDV once soaring to about $2 billion. In May of this year, its DeFi TVL reached $245 million, briefly entering the top 11 in the public chain TVL rankings.

From a widely anticipated star public chain to experiencing a sharp TVL retreat in a short time, MegaETH only took a few months. As the capital base supporting its valuation loosens, has its price already bottomed out? Or does its valuation still lack support after the paper prosperity fades away.

TVL Highly Dependent on a Single Protocol and Circular Strategies

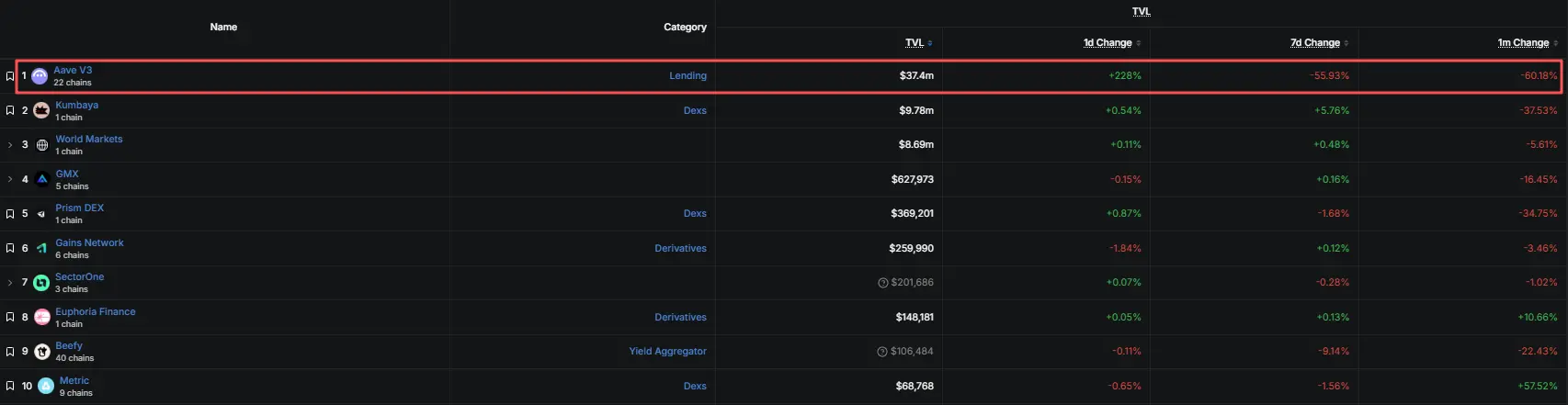

In MegaETH's ecosystem, Aave once contributed about ninety percent of the chain's TVL at its peak. The current total TVL fluctuates around $60 million, with Aave still accounting for about 65%.

In fact, just over two months ago, the largest source of MegaETH's TVL was someone else. On the day of the token listing, MegaETH's native DEX protocol Kumbaya accounted for $59.03 million out of the total chain TVL of $98.43 million, a share of about sixty percent.

At the same time, projects like Aave V3, GMX, and Chainlink Scale were integrated and launched. After that, Aave gradually became the dominant force in TVL.

The risk assessment agency LlamaRisk previously pointed out that MegaETH's TVL is highly dependent on Aave, while its stablecoin structure is also highly concentrated on USDm and USDe. In its view, after excluding native assets, the proportion of external assets entering MegaETH through third parties and specific asset channels is high. The sources of funds, asset types, and protocol methods are relatively concentrated, raising questions about stability.

Specifically regarding the strategies, the market widely suspects that a significant portion of this volume comes from circular strategies related to Ethena's stablecoins. That is, repeatedly collateralizing, borrowing, and re-collateralizing stablecoins, artificially inflating the book value through leverage stacking.

This means that when the yield of USDe falls below the borrowing cost on Aave, this arbitrage mechanism loses its profit margin, circular positions begin to unwind, and funds subsequently withdraw.

Whether it's point incentives during the launch period or interest rate spreads in circular strategies, such funds are essentially yield-seeking. Once the expected yield disappears, they leave. This is common business practice in DeFi and is not surprising in itself.

What truly alarms the market is what remains on the MegaETH chain after this huge proportion of funds is withdrawn, and whether what remains can support its current valuation.

Three Layers of Mismatch Between Valuation and Fundamentals

The first layer of mismatch occurs between valuation and real usage

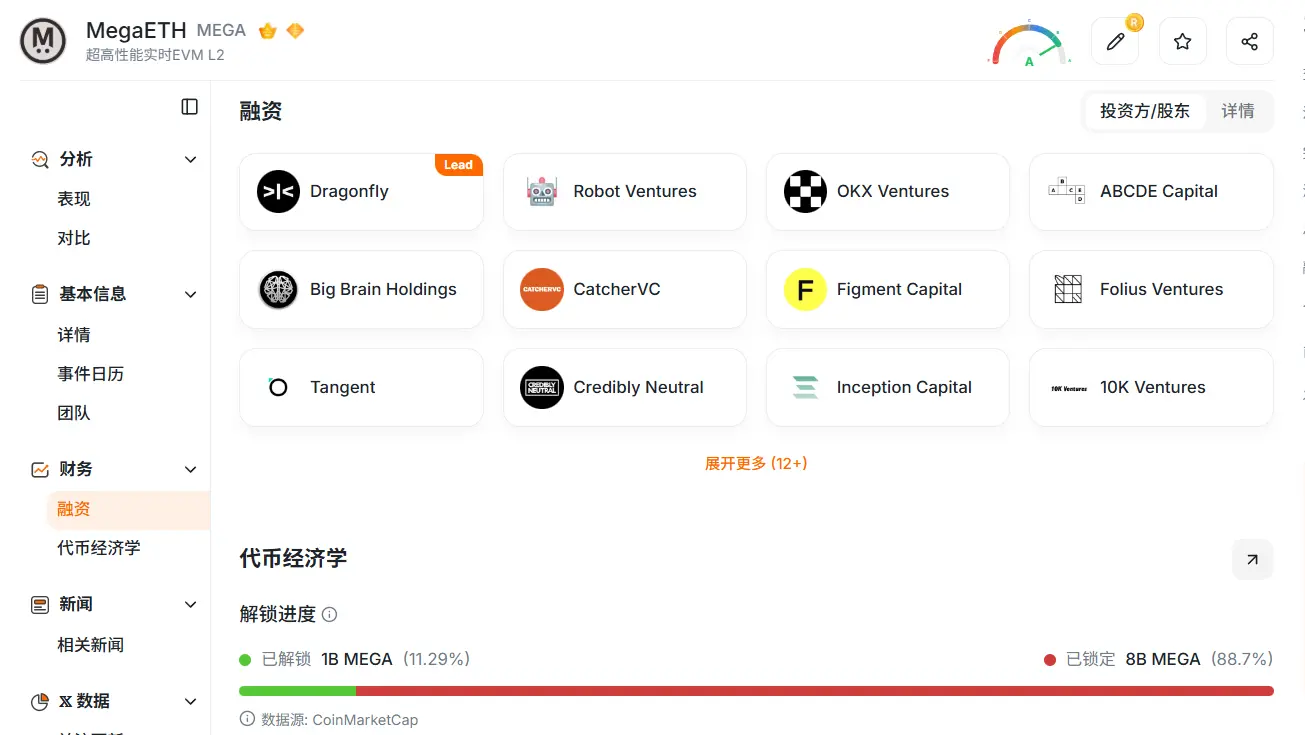

As of press time, MEGA's market cap is about $54 million, and its FDV is approximately $4.7 billion. According to RootData, currently 88.7% of MEGA tokens have not been circulated, with a large number of holders unable to exit due to a one-year lock-up arrangement. There remains a batch of potential selling pressure in the future.

Looking at how much real usage corresponds to the current valuation, data shows that the real revenue of MegaETH's full-chain protocols in the last 30 days is less than $900,000, annualized to about $10 million, with only 2,619 daily active addresses.

On average, each daily active address carries an FDV of about $180,000 on MegaETH, while each address contributes less than $350 in real protocol revenue per month.

Clearly, its price is not anchored to the current scale of real economic activity, but rather to the market's imagination of its future. However, this expectation is collapsing step by step.

The second layer of mismatch is between token narrative and ecosystem quality

The market buys MEGA based on the story of a high-performance DeFi public chain. However, looking at the revenue structure, there is some discrepancy.

DefiLlama data shows that the highest-earning protocol on MegaETH is Monster, a physical trading card game, with 30-day revenue of about $670,000, accounting for nearly 80% of the entire chain's protocol revenue.

Meanwhile, Aave, which carries the DeFi narrative and once accounted for about ninety percent of the chain's TVL at its peak, only generated about $90,000 in revenue during the same period.

A similar misalignment is reflected in stablecoins. The supply of MegaETH's native stablecoin USDM on the chain is about $460 million, with daily DEX volume of only about $630,000 and daily perpetual contract volume of just about $120,000. Moreover, this supply is also draining; USDM's market cap has dropped over 26% in the last 7 days, indicating that real funds are leaving more convincingly than TVL.

A long-term participant @OlricOnlyfornft pointed out that MegaETH once had a very strong community early on. However, the team has long been more focused on technology and applications, with insufficient communication with the community. Many promising projects ultimately migrated to other chains. Now, there are not many applications that can be clearly identified as success cases, and only a few remain committed to building.

Such views may not alone form a conclusion, but they indicate that after the market hype fades, MegaETH still needs clearer application examples to prove the quality of its ecosystem.

The third layer of mismatch lies between short-term expectations and long-term delivery

MegaETH initially carried excessively high expectations upon launch: TGE, blue-chip project integrations, KOL participation in new listings, and surging TVL collectively formed the early valuation anchor. However, looking back a few months later, the chain's delivery capability has never kept pace.

In February of this year, Uniswap deployed v2, v3, and v4 on MegaETH. As of press time, Uniswap's TVL on MegaETH is less than twenty thousand dollars, having evaporated about 97% in the last 7 days. In the past day, Aave V3's TVL once rebounded over 240% in a single day, but over a 7-day period, it still fell over 50%.

The significant inflows and outflows of funds precisely indicate that this portion of TVL is driven by arbitrage funds, not stable, sedimented real demand.

Notably, MEGA's situation is not an isolated case. Another star new public chain highly valued in this cycle, Monad, has also seen its token MON decline all the way. MON is currently around $0.022, down over fifty percent from its November 2025 high, with a current market cap of about $2.69 billion.

Although Monad's recent TVL has rebounded due to capital inflows into lending protocols, the market reaction has been tepid. This points to the same judgment as the MegaETH situation: when pricing this category of public chains, the market is increasingly not recognizing paper TVL but rather looking for real value support.

In other words, this round of adjustment may not just be a single-point slowdown for MegaETH. It seems more like the market is reducing the premium given to paper TVL and star narratives, instead demanding clearer transaction volumes, revenue, and ecosystem traction as support.

Furthermore, competition in the public chain track is still intensifying. New players including Robinhood continue to enter, continuously diverting market attention and funds.

For MEGA, although the decline has been significant, any rebound that may occur is more likely to come from short-term market sentiment repair rather than genuine improvement in fundamentals.

As Paper Prosperity Fades Away, MEGA Still Awaits a Value Anchor

Looking at these mismatches together, the conclusion becomes clearer.

When the paper prosperity propped up by incentive and arbitrage funds recedes, what's missing between MEGA's current market capitalization and its real on-chain fundamentals is a solid value anchor.

Market sentiment has also clearly turned cautious. One view holds that this is a normal valuation reversion after incentive funds recede. Point incentives stop, the interest rate spread for circular arbitrage disappears, and capital outflow is an inevitable result. MegaETH just leveraged this strategy higher, hence the particularly severe pullback.

At the community level, many users continue to question the team's communication and transparency, pointing out that Discord has closed community discussions, Telegram is only open to users holding a large number of tokens, and the team's public appearances are far less frequent than before the launch.

However, these statements are mostly user accounts and have not been officially confirmed. As of press time, the MegaETH team has not publicly responded to the related questions.

For MEGA, whether it is seen as still in the process of reverting to fundamentals or having already fallen into an obvious mismatch between valuation and fundamentals, the subsequent focus falls on the same thing: whether the team can convert short-term liquidity into real usage and deliver the previously raised massive funds into tangible ecosystem results.

Before these deliverables appear, aside from short-term rebounds driven by market sentiment, there seems to be no other solid reason for its valuation to stabilize again.