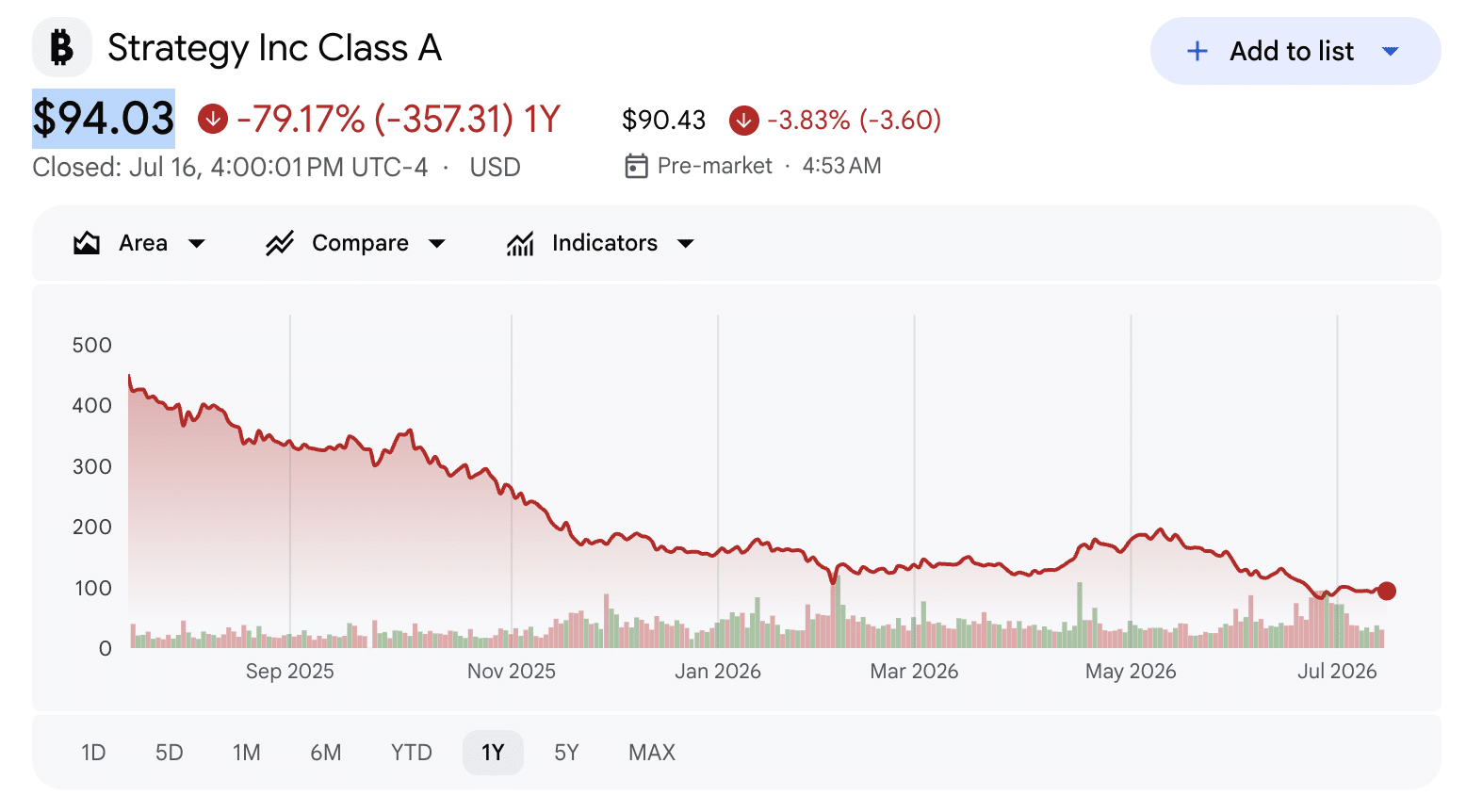

MSTR, the common stock of Michael Saylor’s Strategy, has declined by 79.17% over the last 12 months.

In fact, after falling 3.53% over the previous day, it was trading at $94.03 at the time of writing.

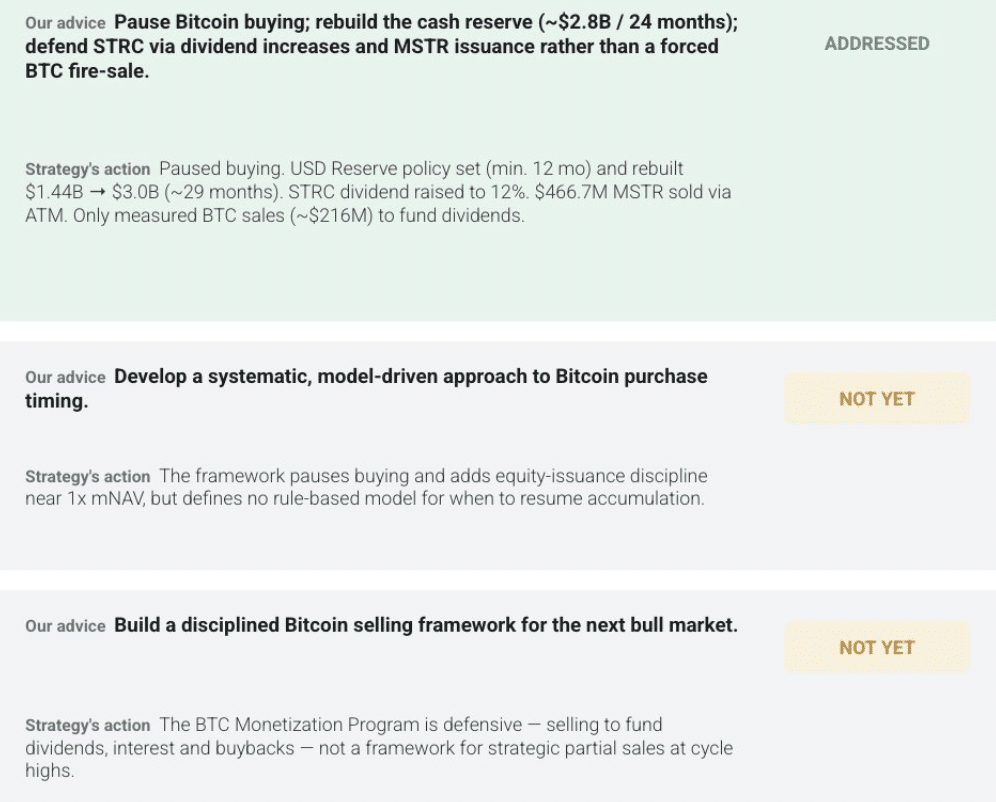

The decline occurred as Strategy shifted from aggressive Bitcoin accumulation toward defensive capital management. However, its limited Bitcoin sales represented only a fraction of its total holdings.

Strategy’s current market dynamic

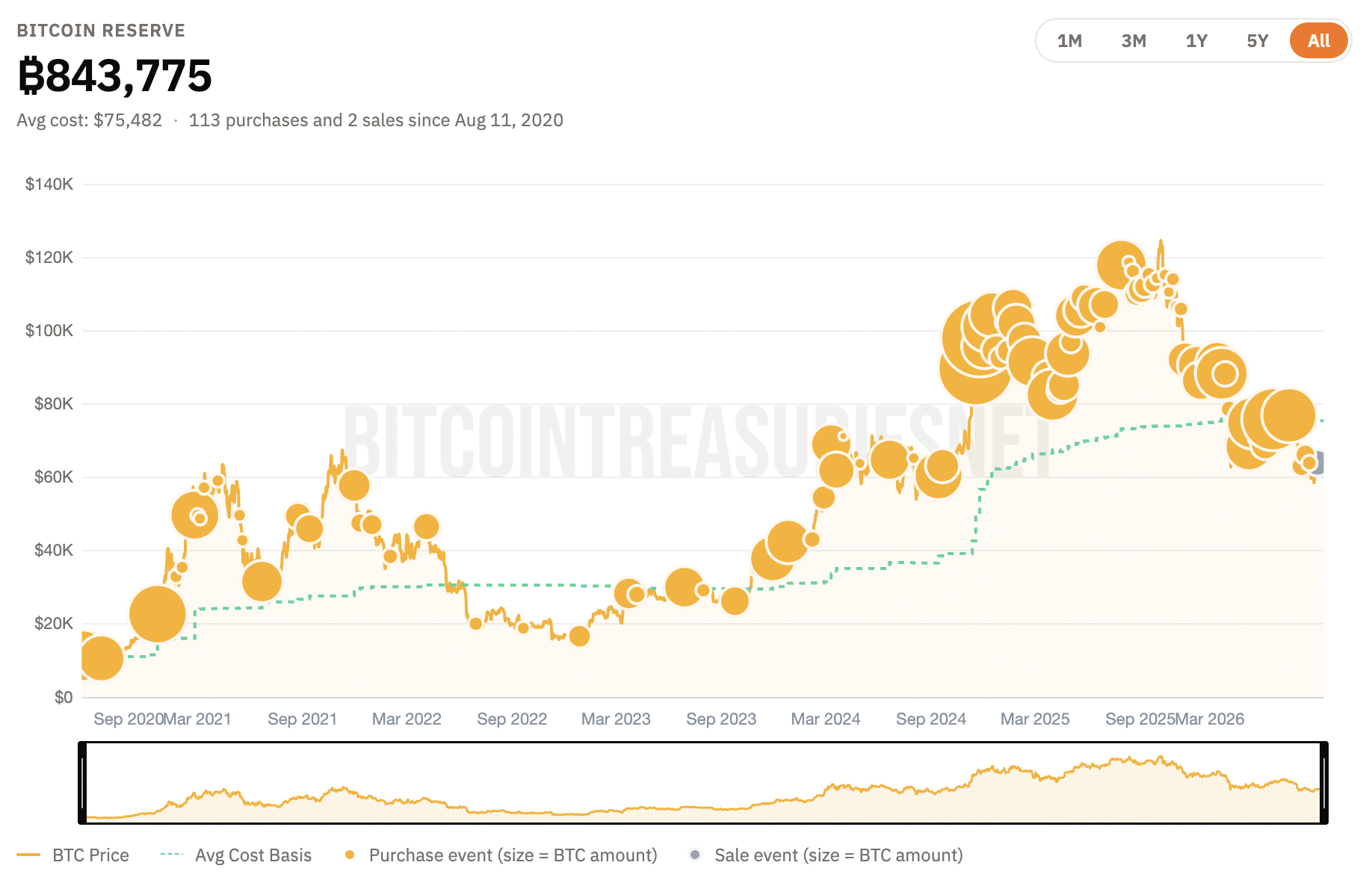

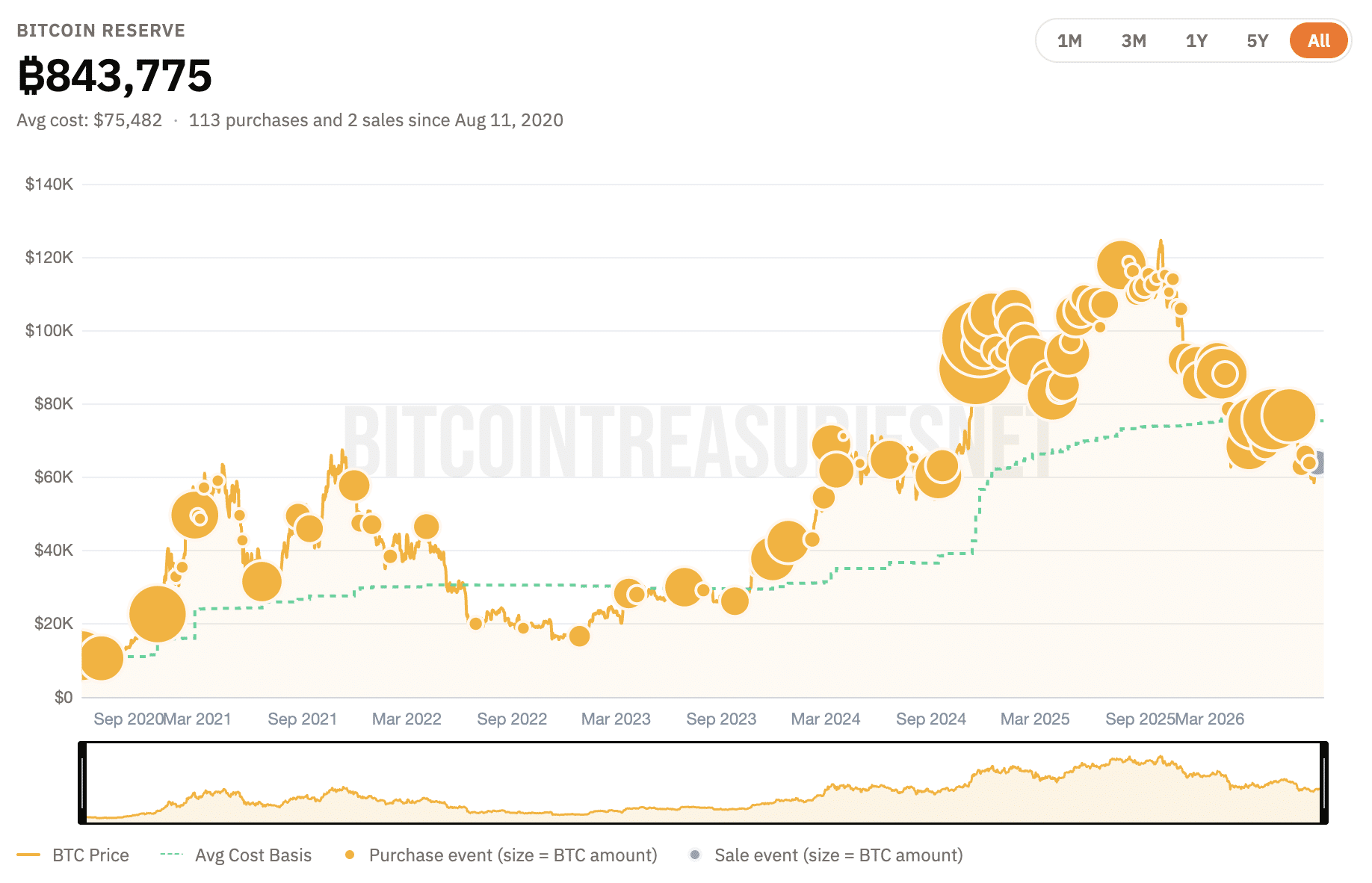

Following the initial sale of 32 Bitcoin [BTC] in June 2026, Strategy went on to sell 3588 Bitcoin in July. Strategy now owns 843,775 BTC, which is worth $53 billion, after making no new purchases in July.

The 3,620 BTC sold represented only 0.43% of Strategy’s remaining holdings. Therefore, the sales suggested liquidity management rather than a broader Bitcoin exit.

Additionally, with no share repurchases during that time, Strategy also sold 4.82 million MSTR shares through its at-the-market (ATM) equity program, generating about $466.7 million in net proceeds.

Remarkably, a recent 8-K filing revealed that the company’s USD Reserve, a cash reserve meant to cover debt interest payments and preferred stock dividends, has increased to $3.0 billion.

Change of plans

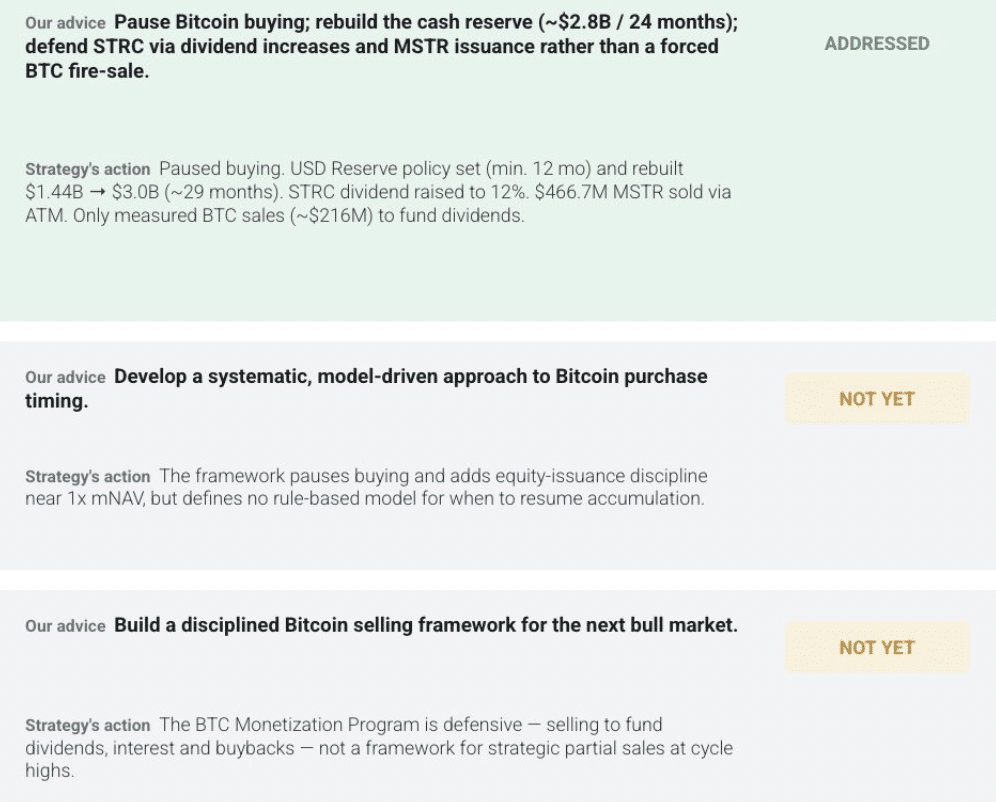

Meanwhile, CryptoQuant also highlighted the change in Strategy’s model, pointing out that the company has adopted a more cautious approach to capital management.

By raising its USD Reserve from $1.44 billion to $3.0 billion, the company has temporarily halted Bitcoin purchases in favor of fortifying its balance sheet.

Because of this increased cash cushion, the company has been able to raise STRC’s annual dividend to 12%, nearly doubling the coverage for dividend payments from approximately 14 months to approximately 29 months.

Even though STRC shares have since rebounded from roughly $75 to $85, CryptoQuant thinks the company’s next big problem will be determining when to start buying Bitcoin again and whether to sell some of its holdings during the next bull market to lock in gains instead of sticking to its buy-and-hold approach.

As expected, Peter Schiff took this opportunity to criticize MSTR’s investment case and said,

Supporters of Saylor’s Strategy

Yet, not everyone agreed with Schiff’s criticism, as Bitcoin wizard Adam Livingston contends that if Strategy starts aggressively raising money again through its STRC preferred stock, call options may yield the highest returns.

Livingston thinks that Strategy could raise the price of Bitcoin per share without diluting common shareholders if it can continue to fund Bitcoin purchases with preferred stock instead of issuing more MSTR common shares. This would make leveraged MSTR call options particularly alluring.

THE MSTR CALL BECOMES A WEAPON IF THE STRC MACHINE RESTARTS

Although he offers potential recovery scenarios, he also notes that they are merely speculative estimates, concluding that the post is “financial entertainment,” and not investment advice.

This coincided with Saylor recently shedding light on Bitcoin and putting it best when he stated,

Major-bank Bitcoin adoption is accelerating, but still early: 32% overall as measured by the index.

Final Summary

- Strategy sold only 0.43% of its remaining Bitcoin while doubling its USD Reserve.

- STRC financing could restart Bitcoin purchases, but MSTR dilution remains the central shareholder risk.