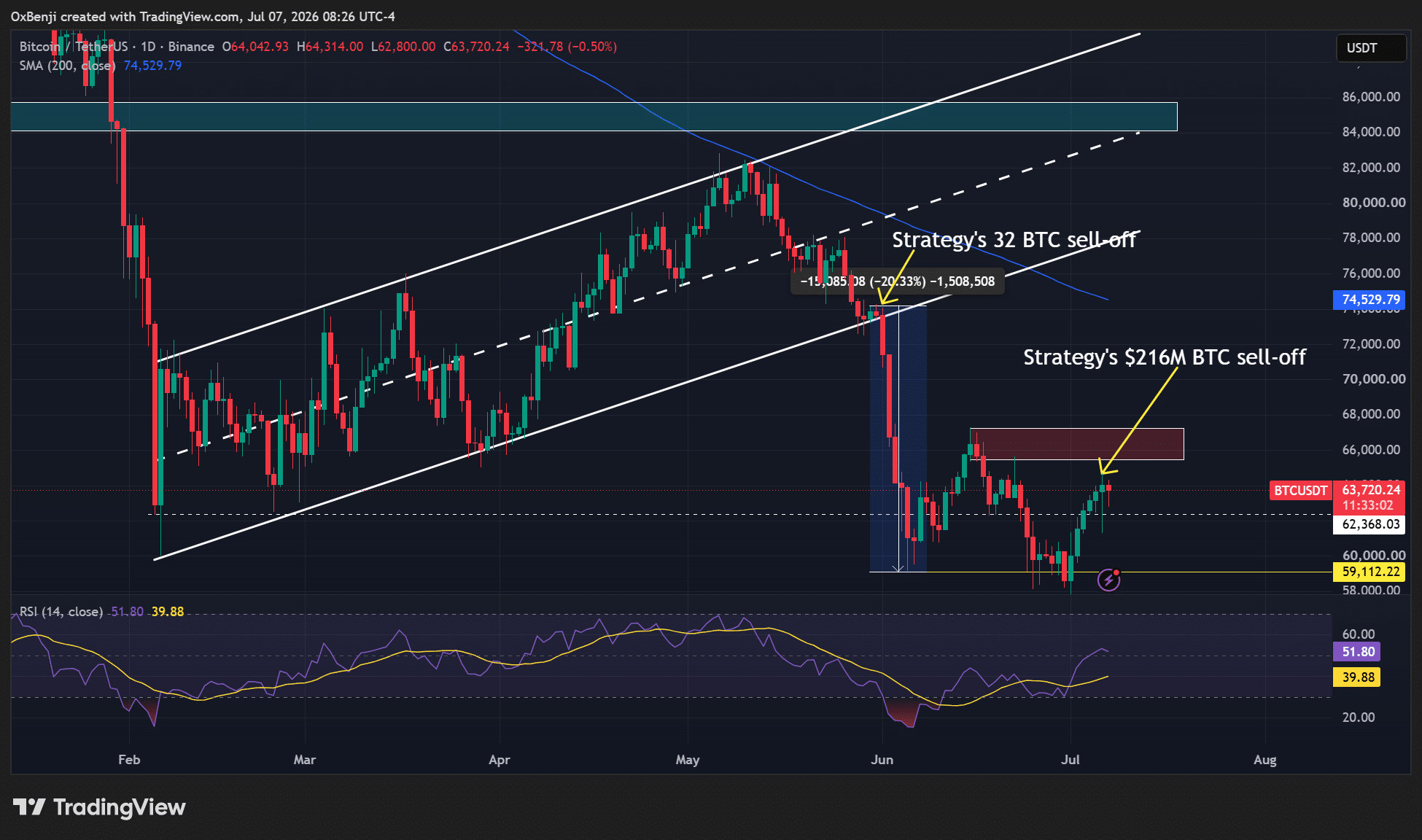

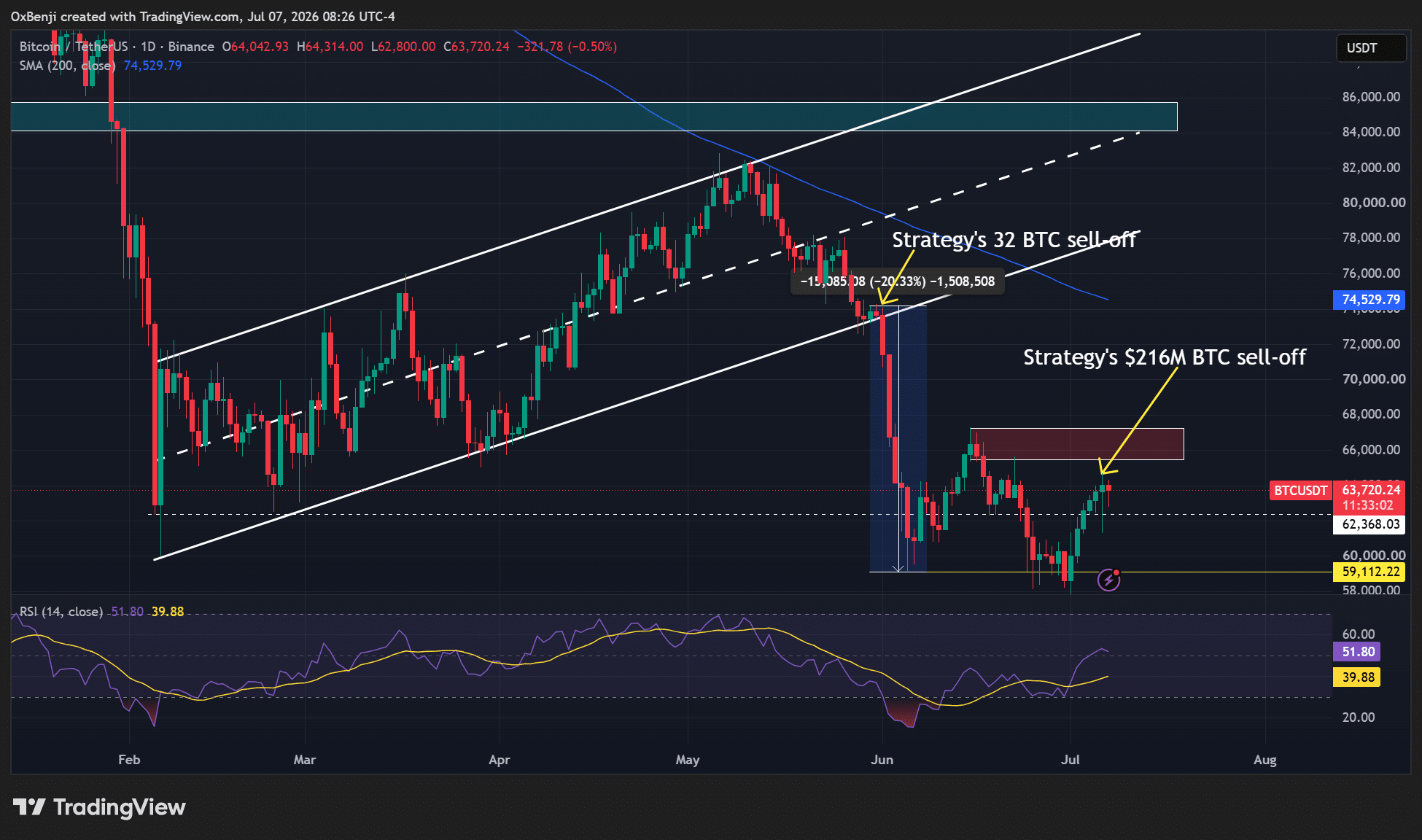

战略公司披露的2.16亿美元比特币抛售计划,并未引发部分分析师上周预测的"死亡螺旋"。

事实上,灰度公司现在认为,该公司12.5亿美元的BTC出售计划可能有助于"支撑BTC价格稳定"。

在其最新报告中,灰度研究主管Zach Pandl指出:

STRC价格的反弹表明投资者现在对该工具更有信心。战略公司正在出售更多比特币。但我们认为,这将恢复其融资结构的市场信心,并帮助比特币找到更持久的底部。

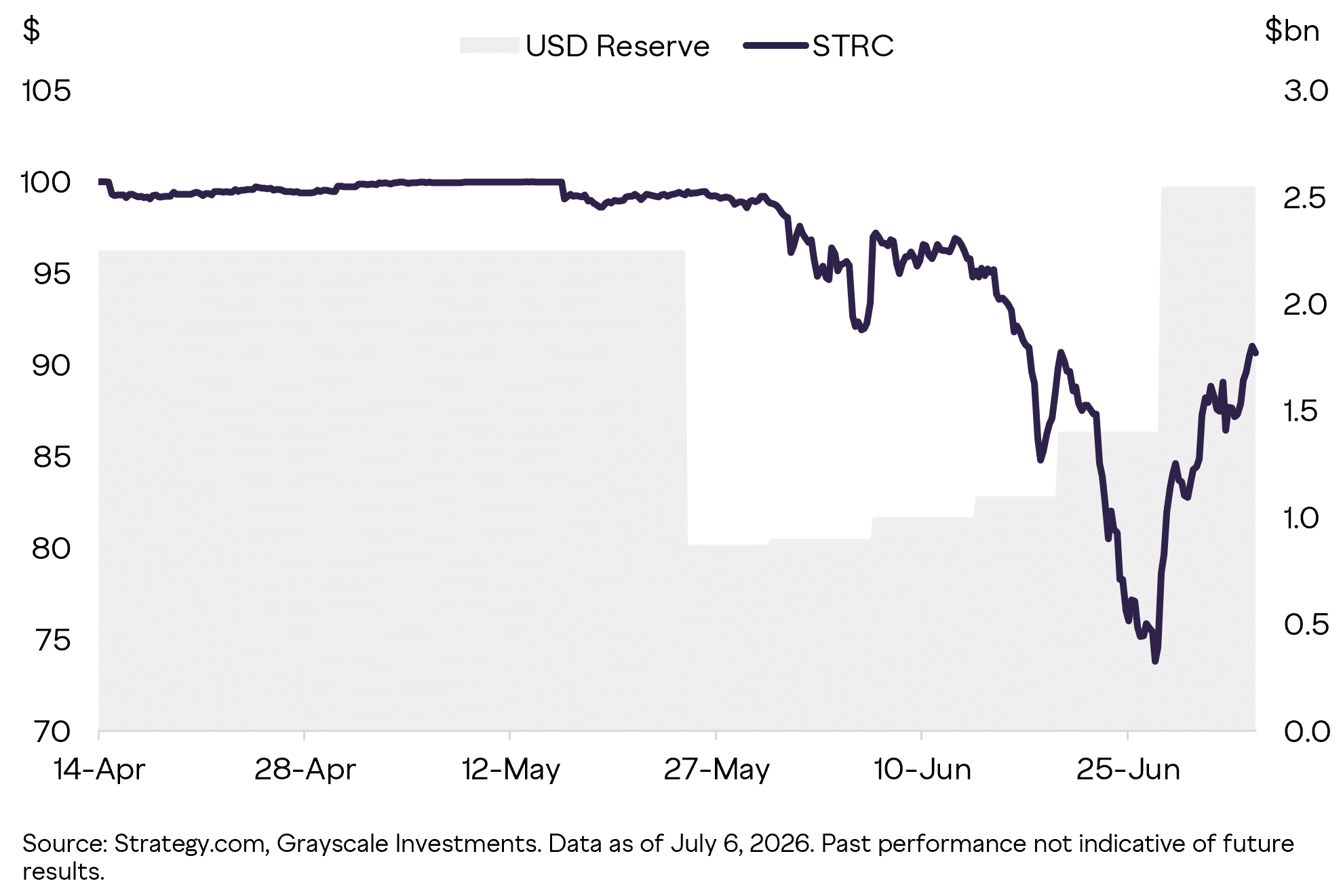

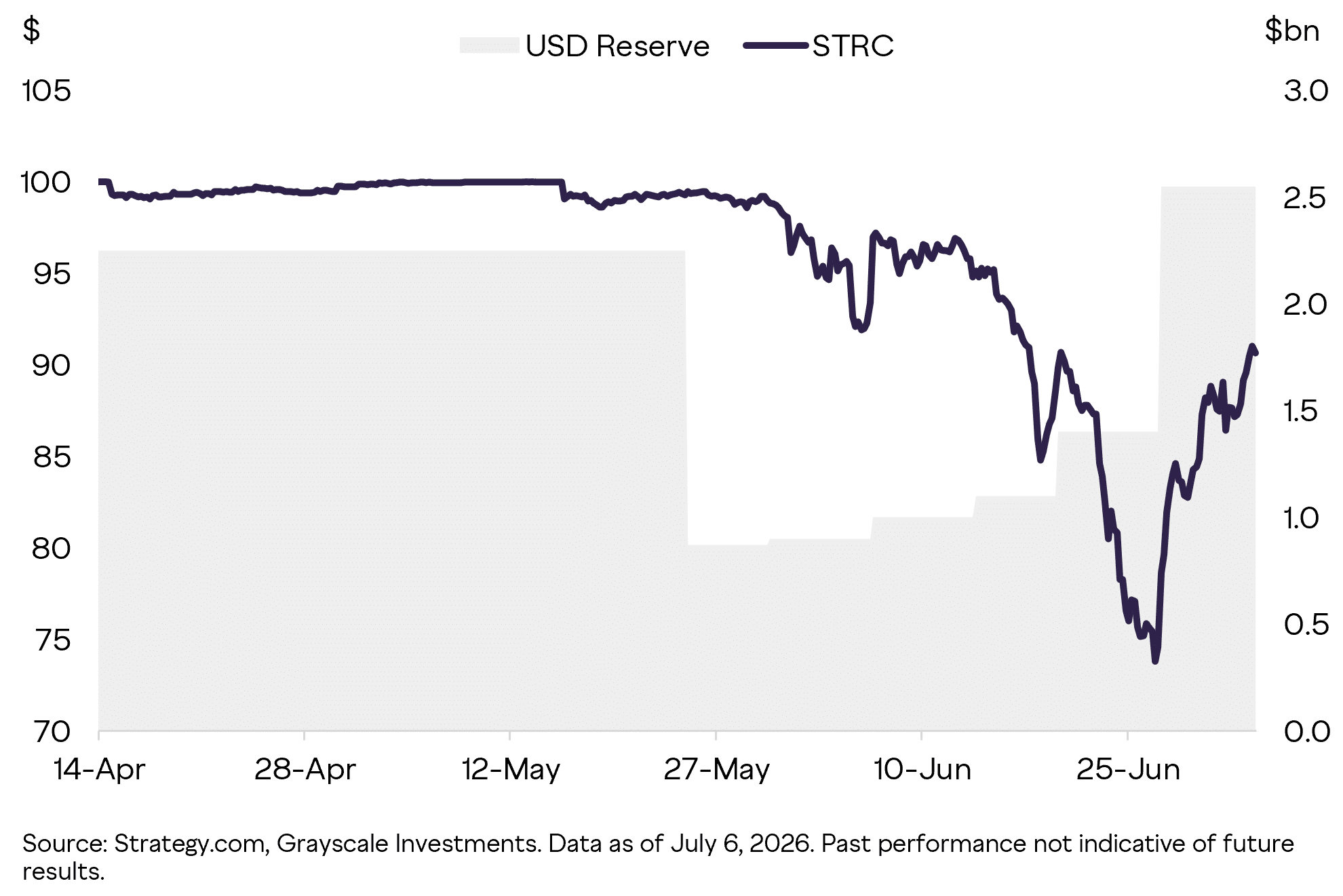

在战略公司周一披露信息后,其付息优先股Stretch (STRC)自6月22日以来首次短暂攀升至90美元以上。

STRC在6月中旬曾与100美元面值脱钩,当时市场普遍担忧随着加密寒冬持续,该公司将如何履行股息支付义务。此外,部分初始美元储备被用于清偿可转换债务,这进一步加剧了担忧。

为解决这些问题,战略公司宣布了一项新计划,包括正式执行12.5亿美元的BTC出售。2.16亿美元的BTC抛售只是第一步,旨在建立缓冲资金以覆盖股息支付义务。

市场无视战略公司2.16亿美元抛售

令人意外的是,市场并未像战略公司出售32枚BTC时那样做出负面反应。在6月第一周,战略公司披露出售32枚BTC后,BTC价格暴跌超过20%,至5.9万美元。

本周一,BTC价格虽走低,但迅速收复失地,当日收盘仅微涨0.6%。

多数分析师此前预期,如果该公司推进12.5亿美元的BTC出售计划,市场将出现类似的负面反应。事实上,摩根大通曾警告不要这样做,并建议通过出售MSTR股票来将美元储备增加至足以覆盖3年支出的水平。

摩根大通认为,如此大规模的BTC抛售将直接导致市场下跌。

Galaxy Research也发出了类似警告,并补充说出售BTC无法解决该公司的"结构性问题"。事实上,Galaxy补充称,此举将引发BTC抛售,进而拖累STRC和MSTR的价格。

截至目前,市场已经消化了这些担忧。事实上,分析师James Van Straten表示,这可能预示着BTC市场已经触底。

当坏消息不再推动价格下跌时,底部可能就出现了。

然而,对于长期批评战略公司的Peter Schiff而言,该公司可能仍在承受损失,因为它一直以低于平均买入价的价格出售BTC。

考虑到MSTR的平均成本,这意味着每枚比特币实际亏损约1.5万美元,总计约5400万美元。鉴于还有超过84万枚比特币待售,总亏损将大得多。

值得注意的是,BTC的短期复苏将取决于定于7月8日公布的FOMC会议纪要。

最终总结

- 市场无视战略公司2.16亿美元BTC抛售,价格维持在6.3万美元上方

- 灰度将此举措视为有助于BTC找到更"持久底部"的支撑因素