Author: Nancy, PANews

Hyperliquid's battle has "spread to" Wall Street, while the internal dynamics of its ecosystem are also rapidly diverging.

Thanks to the permissionless market deployment capability brought by HIP-3 and the continuous enrichment of tradable asset types, Hyperliquid has rapidly broken through this year, becoming a new battleground for "weekend warriors."

While the HIP-3 market scale is expanding at high speed, its ecosystem is undergoing a brutal reshuffle. Trade.XYZ has almost monopolized the market by leveraging its first-mover advantage, holding over 90% of the market share. In contrast, the survival space for other ecosystem projects is constantly being squeezed. Several projects, including Feilx and Ventuals, have successively announced their closure.

HIP-3 Secures Over $300 Billion in Trading Volume, Trade.XYZ Monopolizes 90% of the Market

The rise of HIP-3 has unlocked a new growth curve for Hyperliquid.

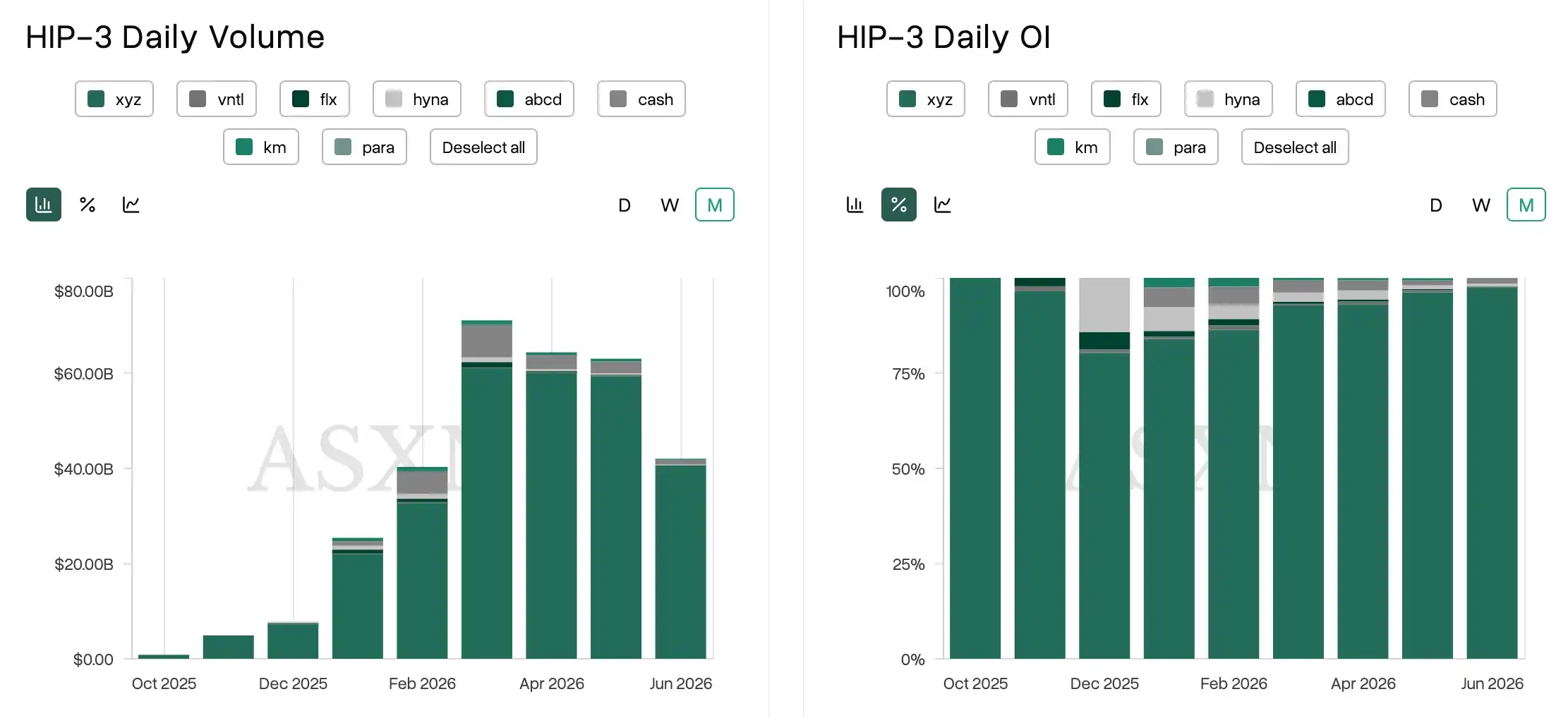

Hyperscreener dashboard data shows that in the past 24 hours, Hyperliquid's full-platform Perp trading volume reached $8.77 billion, with the HIP-3 market contributing about $3.5 billion, accounting for 39.9% of the total trading volume. In other words, for every approximately $10 of perpetual contract trading volume generated on Hyperliquid, nearly $4 comes from HIP-3.

In fact, since its launch last October, HIP-3 has accumulated a trading volume exceeding $319.8 billion in just over half a year, far exceeding market expectations in terms of growth speed. However, what expanded alongside the trading scale was not a blossoming ecosystem but an increasingly obvious head effect, with Trade.XYZ devouring almost the entire market's incremental cake.

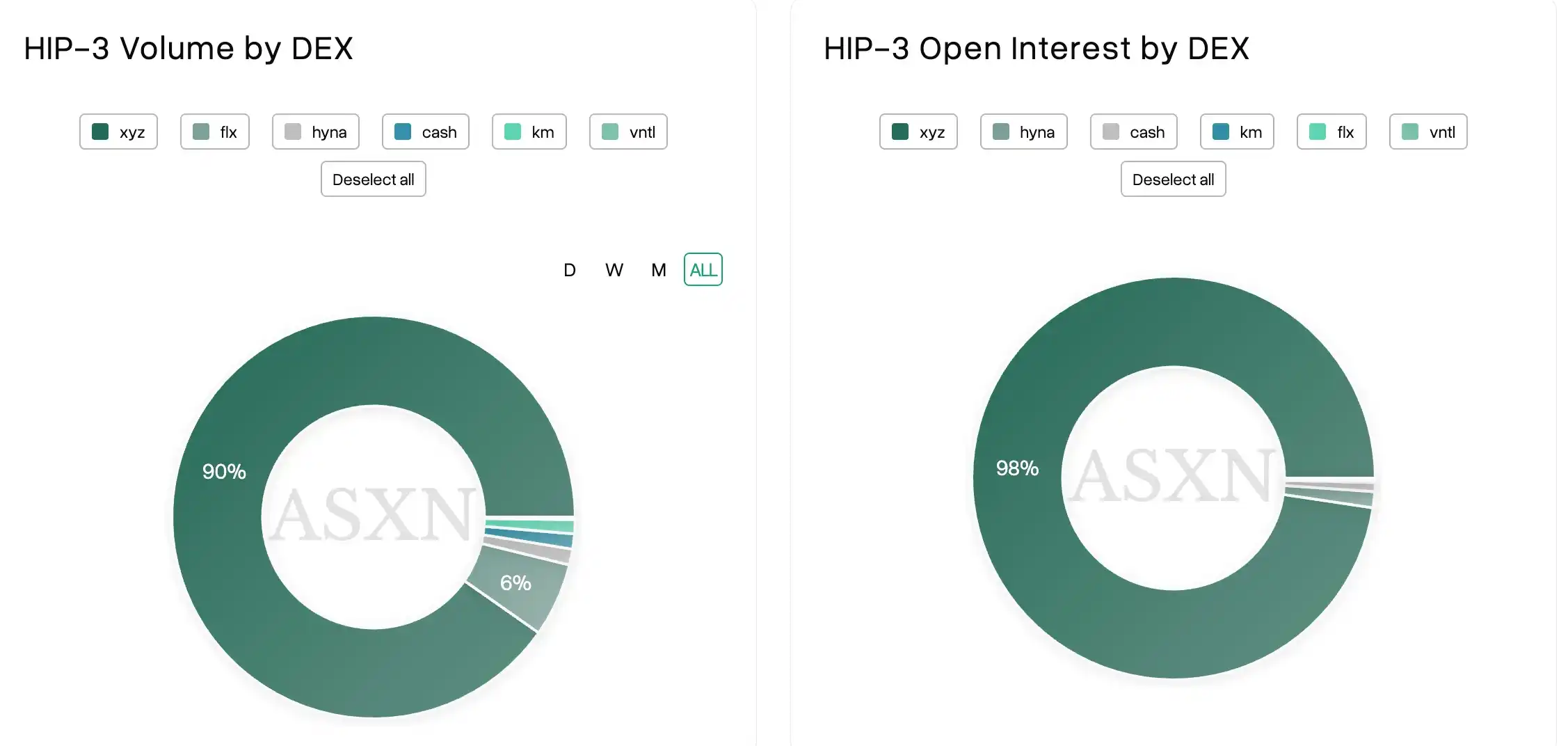

Looking at open interest, Hyperscreener data shows that as of June 16, the cumulative open interest in the HIP-3 market was approximately $29.4 billion. Trade.XYZ alone contributed $28.7 billion, accounting for a staggering 97.6% market share. In contrast, other projects like DreamCash, HyENA, Ventuals, and Felix mostly account for less than 1%, almost negligible.

The trading volume dimension confirms this trend. In terms of cumulative historical trading volume, Trade.XYZ firmly holds about 90% market share, with DreamCash second at about 6%. The remaining projects jointly vie for less than 5% of the market space. In June alone, the head effect intensified further, with Trade.XYZ's market share climbing to 96.65%. The other seven markets, including Felix Exchange, Ventuals, and HyENA, collectively accounted for only 3.35%, with some projects even holding less than 0.1%.

Looking further at the trading activity of assets, this gap becomes even more apparent. This month, the cumulative trading volume of all assets on HIP-3 reached $11.21 billion. The core product on Trade.XYZ, XYZ100 (an index tracking the top 100 companies), contributed $10.64 billion alone, meaning a single asset supports most of the trading activity in the entire HIP-3 market.

The divergence in user activity is equally significant. Data shows that this month, Trade.XYZ attracted over 46,000 unique trading addresses to participate in trading, while other markets mostly had only a few hundred unique traders, some even fewer than a hundred. In terms of transaction frequency, Trade.XYZ has accumulated over 22.03 million trades this month, while most other markets had only tens of thousands to over a hundred thousand trades, a stark contrast to the leading platform.

To some extent, the growth story of HIP-3 at this stage can almost be seen as the growth story of Trade.XYZ alone.

HIP-3 Starts an Elimination Race, Ecosystem Projects Exit Successively

As Trade.XYZ continuously siphons market liquidity, HIP-3 is transforming from an open innovation arena into an elimination race dominated by top players, making it increasingly difficult for newcomers to get a piece of the pie.

Recently, several HIP-3 projects have been shutting down. Last week, Charlie, co-founder of the Hyperliquid lending protocol Felix, posted an announcement stating that Felix's HIP-3 DEX and all spot markets would begin shutting down on June 19, with full deactivation completed by June 20. All traders need to close their positions before then. This adjustment will not affect Felix's lending and spot stock businesses. The future focus will be on core products, and they do not rule out returning as a HIP-3 deployer once a new user growth path is found.

In his review, Charlie frankly admitted that although Felix, leveraging its first-mover advantage in markets like crude oil, gold, and silver, had accumulated approximately $3 billion in trading volume and earned substantial fee revenue, its market share was gradually overtaken after Trade.XYZ launched similar markets denominated in USDC.

In his view, Trade.XYZ's ability to quickly establish a moat was key: choosing the more liquid USDC over USDH, seizing the HIP-3 launch window, rapidly expanding the number of markets, and the brand effect and liquidity flywheel created by airdrop expectations. With USDH gradually fading out, continuing to maintain HIP-3 deployment can hardly form a differentiated competitive edge, hence the team's decision to scale back related operations.

Felix is not an isolated case. Shortly after, Ventuals, one of the largest participants offering private company stock trading on Hyperliquid, also announced it would gradually cease operations, with the team joining another building team within the Hyperliquid ecosystem. The platform will successively close markets for OpenAI, Anthropic, commodities, indices, etc. vHYPE holders can redeem HYPE at a 1:1 ratio and claim staking rewards. Ventuals is also terminating its points and referral programs and confirmed it will not issue a token.

Ventuals disclosed that during its operation, the project raised over 500,000 HYPE and achieved over $650 million in trading volume, once becoming one of the most representative innovative applications in the Hyperliquid HIP-3 ecosystem.

Although the team did not publicly explain the reason for the closure, the market generally believes that Trade.XYZ's siphoning of liquidity for popular assets, coupled with the inherent liquidity and pricing challenges of Pre-IPO assets themselves, were significant reasons for the project's eventual exit.

Most Deployers Need Four Years to Break Even, Pressure on HIP-3 Ecosystem Intensifies

Beyond the competitive pressure from the head effect, HIP-3's own deployment mechanism is further squeezing the survival space for latecomers.

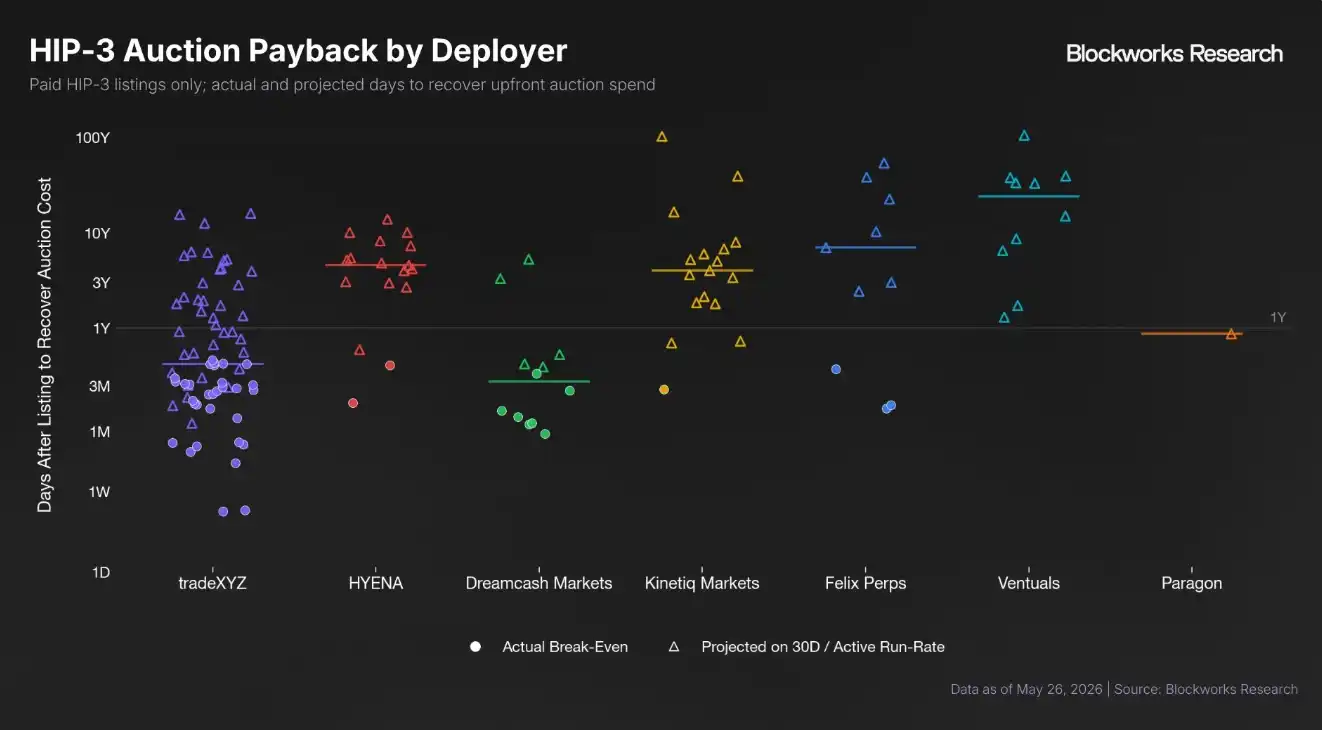

According to HIP-3 rules, any team wanting to create a DEX must first stake 500,000 HYPE as a security deposit. Calculated at the current price, this capital outlay amounts to approximately $35.89 million, and must be locked for at least 183 days after deployment. Meanwhile, only the first three assets for each deployer do not require an auction. Any subsequent new assets must acquire deployment rights through a Dutch auction, with a minimum starting bid of 500 HYPE (currently worth about $36,000, though significantly lower than the 1,750 HYPE in January). The HYPE paid for the auction will be directly burned by the protocol.

For new entrants, under the condition of liquidity highly concentrated towards top players, the high upfront investment, continuously increasing expansion costs, and lengthy payback period are becoming increasingly burdensome to bear. It's worth noting that Hyperliquid disclosed in May of this year that it would gradually lower the 500,000 HYPE staking threshold.

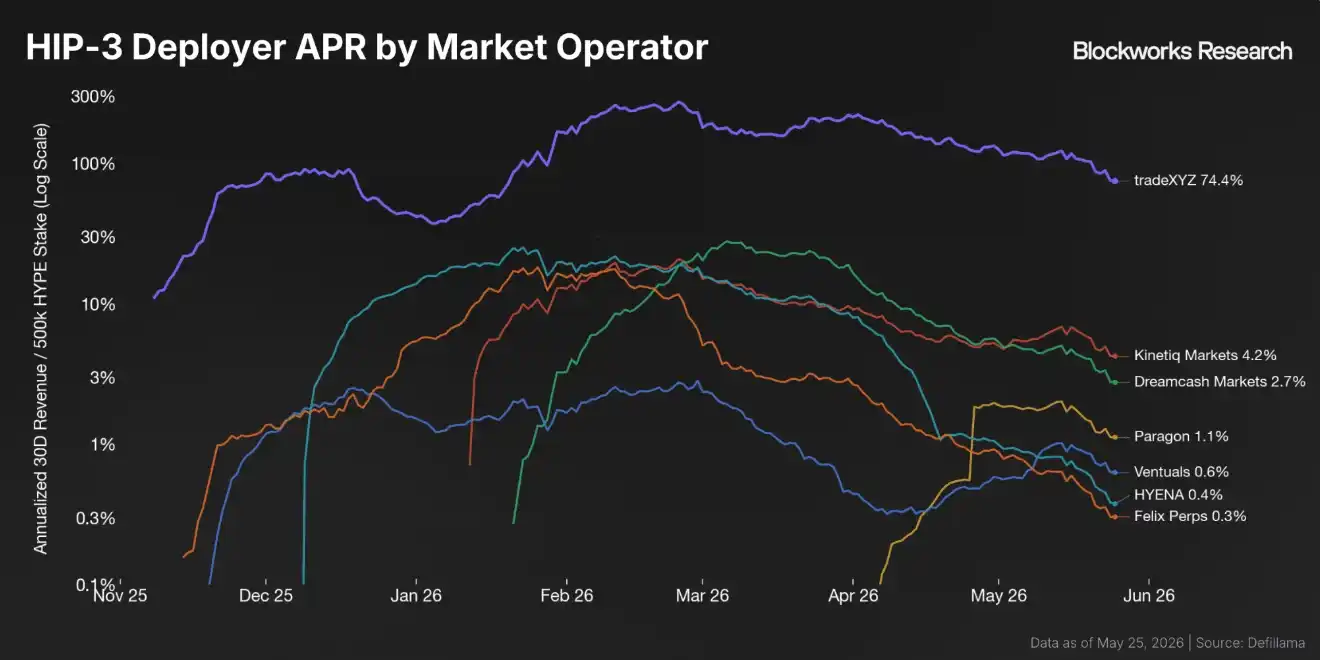

According to Blockworks Research analyst shaunda devens, except for Trade.XYZ, most HIP-3 deployers have an annualized yield based on their staked HYPE close to or even below 1%, with a median recovery period for market auction costs as long as four years. In stark contrast, Trade.XYZ is a clear exception, with an estimated yield on its staked HYPE as high as 74% and a median recovery period for auction costs of only 5 months.

In other words, Trade.XYZ's success stems not only from the product itself but also from a self-reinforcing network effect. More users bring stronger liquidity, stronger liquidity attracts more assets to be listed, and more high-quality assets further consolidate its market position. Meanwhile, marginal deployers lack the incentive to expand further due to low returns, which also dampens demand for new HYPE staking and participation in market auctions.

For Hyperliquid, this situation is not without its concerns.

Undeniably, Trade.XYZ has brought huge incremental space for Hyperliquid, even becoming the most successful showcase case for HIP-3. However, if the listing rights and liquidity for the vast majority of popular assets are concentrated in the hands of a single deployer, then HIP-3 competition will remain top-heavy, struggling to evolve into an open and diverse ecosystem competition.

In the long run, this will not only compress the survival space for innovative projects but may also trap Hyperliquid in the single narrative of perpetual contracts. Especially as competition in the Perp DEX track intensifies, relying solely on perpetual contract trading makes it difficult to build a sufficiently rich on-chain application ecosystem and sustainable network effects. It is noteworthy that Hyperliquid has already ventured into the currently hot prediction market via HIP-4, attempting to further diversify its business portfolio.

Addressing the current dilemma, shaunda devens proposes two mechanism optimization suggestions to enhance the sustainability of market creation and strengthen HYPE's value capture capability.

First, introduce a tiered exchange mechanism. Allow new deployers to launch a HIP-3 DEX with a threshold lower than the current 500,000 HYPE, but with correspondingly restricted permissions, such as lower open interest caps, lower leverage multiples, and stricter risk control rules. As the deployer increases their HYPE stake size, gradually unlock higher-level functionalities.

Second, adjust the HIP-3 market auction economic model. Before a new market recovers its auction costs, allow the deployer to receive up to 100% of trading fee revenue; or, before the cumulative revenue of the entire DEX covers auction costs, prioritize returning transaction fees to the deployer, and revert to the standard 50:50 split between protocol and deployer only after reaching breakeven.

For Hyperliquid, HIP-3 has proven that decentralized market creation is a viable path. Trade.XYZ's success has not only validated product demand but has also become Hyperliquid's significant growth engine at this stage.

However, compared to relying on a single super-app to continuously siphon liquidity, a more resilient, healthier, and open ecosystem perhaps needs to ensure that innovators of different stages and types can all find a space to survive, allowing new assets, new play styles, and new business models to continuously emerge.