作者:Nancy,PANews

当存储板块杀疯了,美光和海力士齐破万亿美元市值大关时,马斯克个人也在加速创造万亿美元身家的神话。

SpaceX携天价估值加速迈向资本市场,这场可能改写财富史的超级IPO,正将马斯克推向全球首位万亿富翁,也让早期盟友斩获百倍甚至千倍的惊人回报。

然而,这场人类历史上最昂贵的太空叙事,若想继续讲下去,终究需要新的买单者。随着体量巨大的养老基金将“被迫买入”,美国人的养老金,成为马斯克逐梦太空的燃料。

马斯克,正让美国退休老头老太太们“爆金币”。

史上最大IPO倒计时,早期盟友赚翻了

华尔街等SpaceX上市,已经等了很多年。

过去十年,这家公司从一家估值仅2700万美元的创业公司,一路成长为如今估值逼近1.75万亿至2万亿美元的超级独角兽,成为全球估值最高的私营企业之一。

如今,这场超级IPO终于最快将在6月12日正式挂牌。这不仅是人类史上规模最大的IPO事件,也意味着财富盛宴进入兑现时刻。马斯克的长期跟随者,终于等来了丰厚的回报。

比如,谷歌通过早期投资或成最大外部赢家。截至2025年底,其持有SpaceX约6.11%的股份。当年仅9亿美元的投资,如今对应价值已接近1200亿美元;Valor Equity Partners作为仅次于马斯克的重要股东,持有超过5亿股SpaceX A类股票,权益价值区间约在900亿至1400亿美元之间;Peter Thiel旗下Founders Fund通过多轮追加投资,持有约3.5%的股份,账面收益已超过600亿美元;富达作为2015年联合注资的主要机构之一,其持有的股份价值约350亿美元;即便入场相对较晚的红杉资本回报同样可观,预计获得超过200亿美元。

至于马斯克本人,也有望成为全球首位万亿美元富翁。

美国银行策略师Michael Hartnett在最新报告中警告,SpaceX和OpenAI等超级IPO一旦落地,科技股在股票基准指数中的权重将轻易突破约48%,超越1920年代"咆哮年代"、1970年代"漂亮50"、1980年代日本泡沫以及1990年代科网泡沫等历史上所有重大泡沫时期的市场集中度水平。

然而,如此庞大的估值,最终需要谁来接盘?

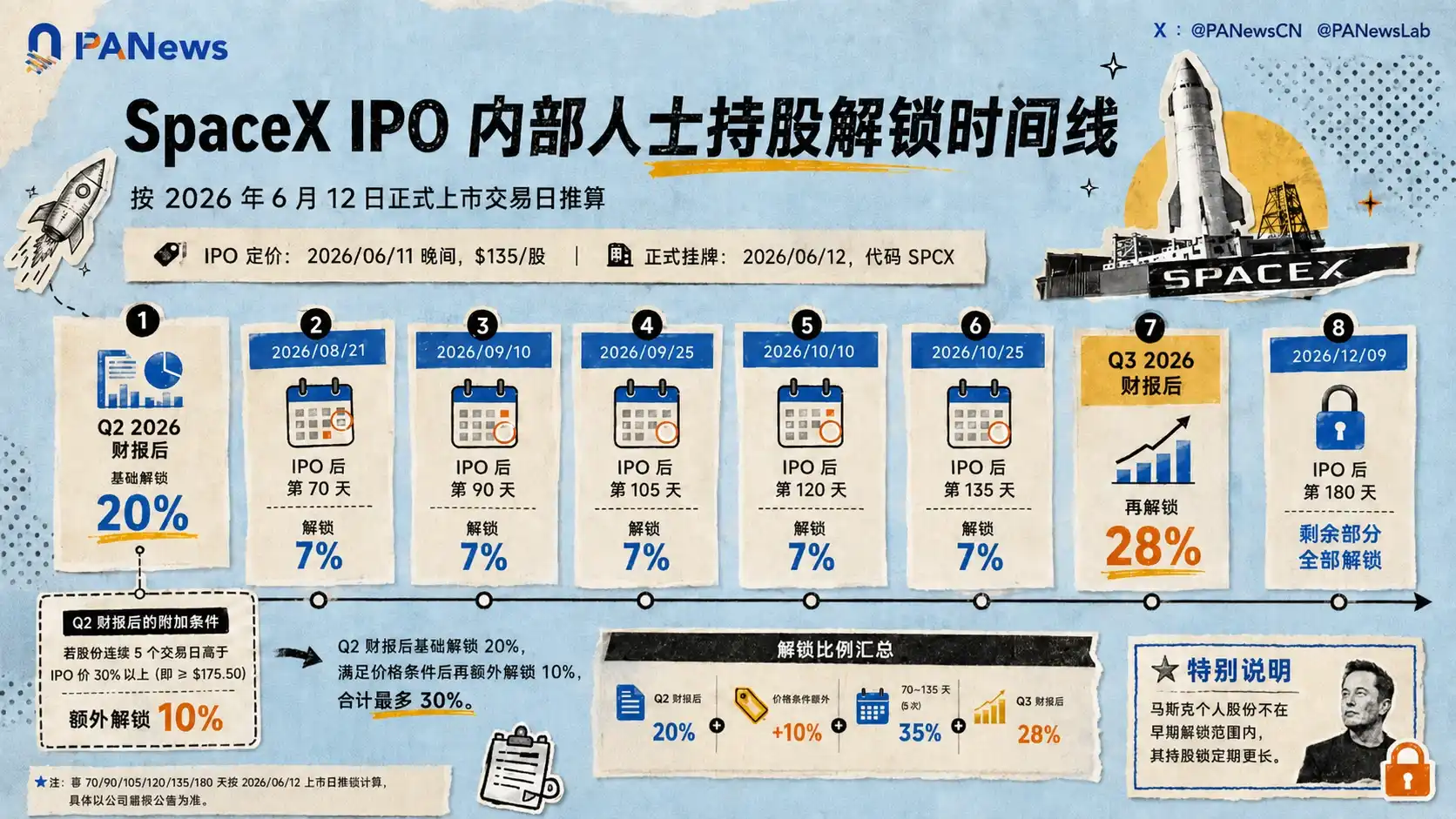

为了减少上市后的抛售压力、维持股价稳定,SpaceX也进行了一定调整。例如,内部人士股份将采用分阶段解锁机制,而非传统IPO常见的统一6个月锁定期;同时,公司还批准了普通股1拆5的拆股方案,以降低散户心理门槛、提升流动性。马斯克更是公开表示,自己不会出售任何SpaceX股份。

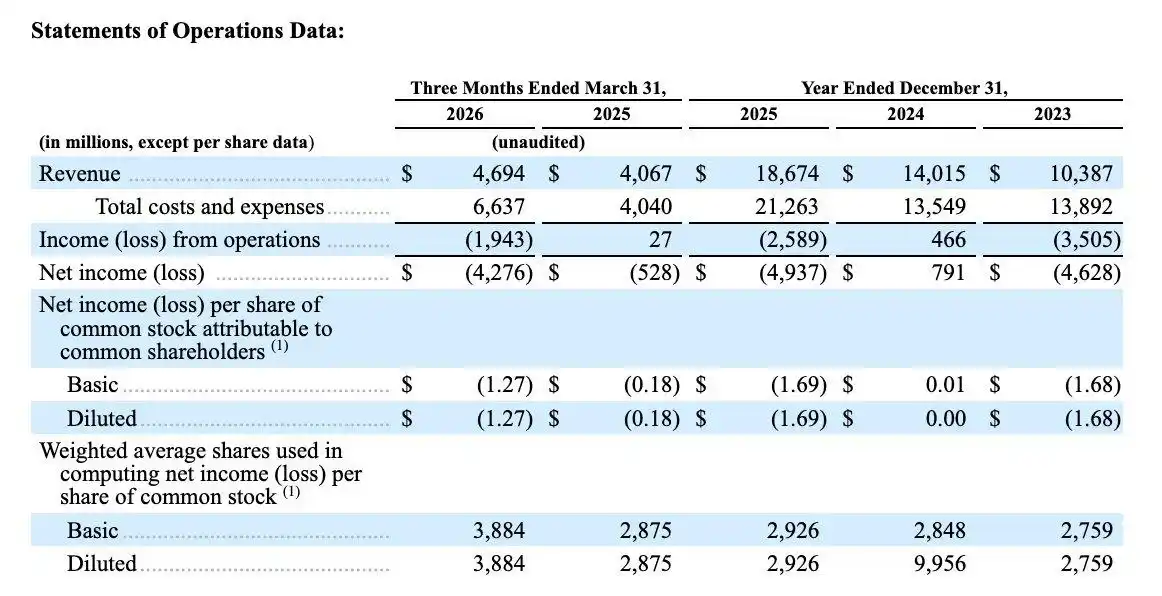

但市场的担忧并未因此消失。抛开火星宏大叙事的不确定性,单看财务数据,SpaceX依然是一家高速烧钱的公司。招股书显示,仅2026年第一季度,SpaceX净亏损就接近43亿美元,几乎相当于上一年度全年亏损水平。与此同时,马斯克掌控85%绝对投票权,这意味着董事会几乎不可能解雇他,外部股东也几乎无法推动任何重大商业决策。

某种程度上,SpaceX算是一家高度马斯克化的公司,其估值、治理乃至未来预期,都与马斯克个人深度绑定。

当所有早期投资人都已经赚得盆满钵满之后,谁还愿意高位买入这张已经贵到离谱的太空船票?

华尔街铺设指数快车道,美国养老金成“接盘侠”

美国人的养老金 ,或将成为马斯克太空梦的潜在燃料。

华尔街,已经开始为超级IPO打开高速通道。今年5月1日,纳斯达克新规正式生效,新上市公司若市值排名进入纳斯达克100指数前40名,只需15个交易日即可被纳入指数,此前通常需要等待约3个月。

标普也在5月启动意见征询,拟将纳入所需的最短上市时间从12个月缩短至6个月,并考虑对超大型公司豁免盈利能力要求。富时罗素同样放宽限制,允许大型IPO在上市后第5个交易日即可快速评估纳入Russell U.S. Equity Indexes(包括Russell 1000、Top 200等),无需等待季度审核。

美国各大指数悄然放宽规则,无疑是为SpaceX铺设专属跑道。

据Business Insider披露,SpaceX上市后可能迅速进入主流指数及ETF,被动资金配置速度或远超以往大型IPO,比如Vanguard VTI与成长ETF VUG所对应的CRSP指数最快可能在SpaceX上市后5个交易日内纳入;QQQ所跟踪的纳斯达克100指数,最快可在SpaceX上市后15个交易日纳入;SPY所跟踪的标普500指数,则可能在规则修改后于2027年纳入SpaceX等。

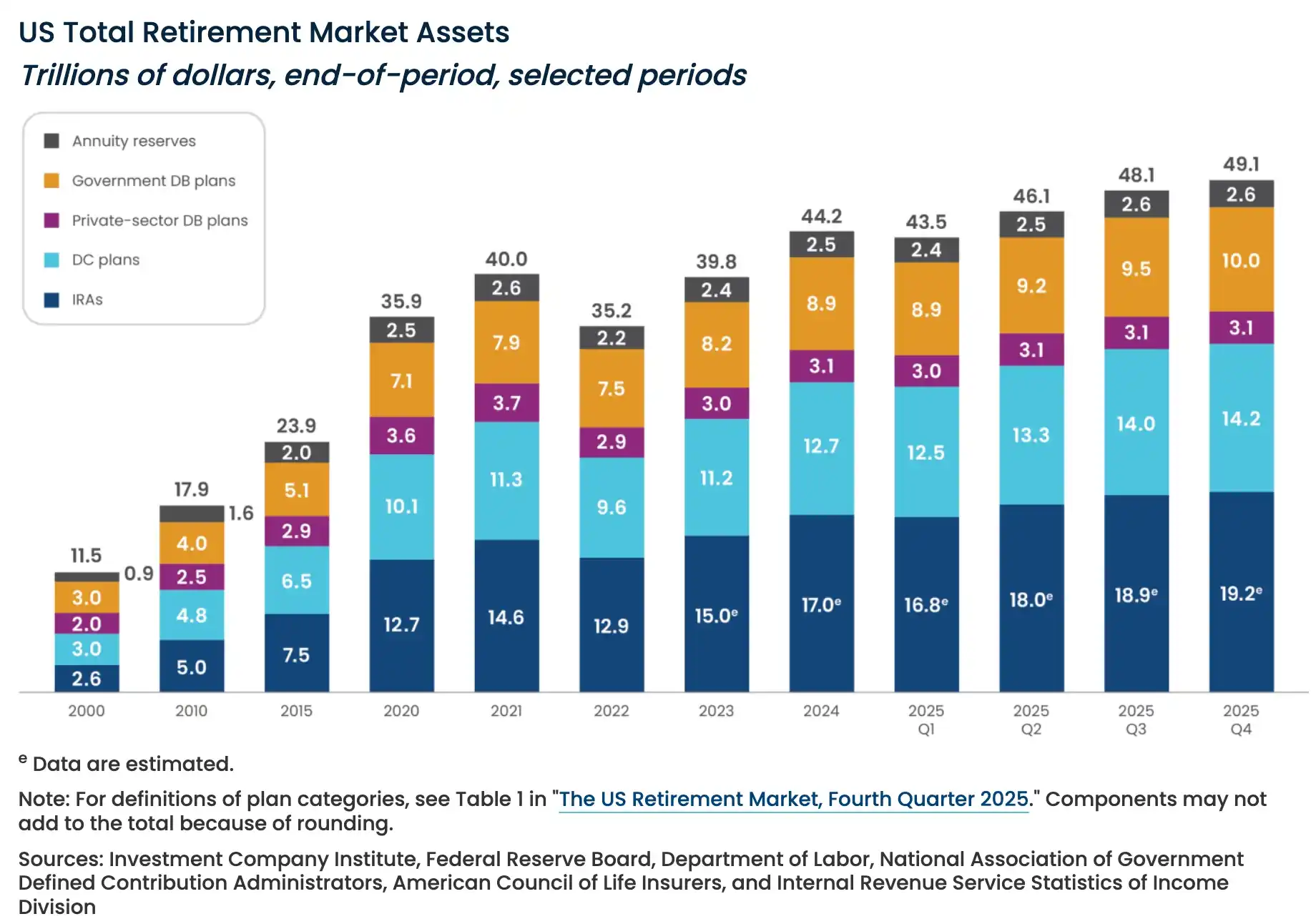

美国退休体系中,大量401(k)、养老金以及长期储蓄账户,都采用被动指数投资策略。基金通常按照指数成分股及其市值权重自动配置资产。

这种策略起源于指数基金教父John Bogle于1976年推出的首只普通投资者指数基金,核心理念是“复制市场而非击败市场”。凭借极低的管理费用和高度分散化,它成为养老金和401(k)账户的首选配置方式。截至目前,美国退休资产总额已超过49万亿美元。

这意味着,一旦SpaceX被纳入指数,所有跟踪这些基准的基金不分析估值、不判断泡沫,甚至不关心公司是否盈利,按权重强制买入。

然而,这场游戏已引发养老金系统的强烈不满。

不久前,美教师联合会致信SEC,敦促加强对SpaceX上市的审查,警告劳动者终身积蓄可能被一家更像马斯克家族企业而非透明上市公司所操控。

同时,管理资产超1万亿美元的三大美国公共养老基金(CalPERS、纽约州和纽约市养老系统)也联名致信马斯克,强烈反对SpaceX的极端治理结构,包括超级投票权、对自身被免去CEO的一票否决权,以及拥有免受诉讼的权利。

他们指出,马斯克同时掌管SpaceX、Tesla、xAI、Neuralink等多家公司,精力分散风险巨大。信中要求SpaceX在未来七年内逐步转向一股一票、设立外部股东占多数的董事会、分离CEO与董事长职务,并取消马斯克的自我否决权。

这场华尔街为超级IPO定制的规则修改,最终将数千万美国人的退休储蓄与马斯克宏大的太空梦想紧密捆绑。在早期投资人坐享百倍回报之后,剩下的“接盘”成本,被转移到无力做出选择的被动投资者身上。

史上最大的”崩老头“游戏,正借指数之名,正式拉开帷幕。