Двое бывших руководителей обанкротившегося сервиса криптокредитования Cred признали себя виновными в мошенничестве с использованием электронных средств связи, связанном с крахом компании.

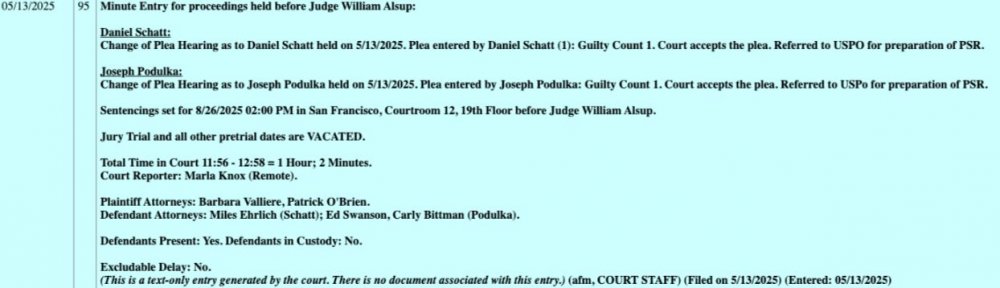

Бывший генеральный директор Cred Дэниел Шатт и финансовый директор Джозеф Подулка признали себя виновными в мошенничестве с использованием электронных средств связи в рамках соглашения о признании вины с прокурорами, согласно текстовому заявлению от 13 мая в окружном суде Калифорнии.

Окружной судья Уильям Алсап принял соглашения о признании вины и назначил слушание по вынесению приговора на 26 августа. Мошенничество с использованием электронных средств связи может повлечь за собой до 20 лет тюрьмы и штраф в размере 250 000 долларов для физических лиц и 500 000 долларов для предприятий.

После принятия признания вины ответчиком судья Уильям Алсап назначил слушание по вынесению приговора на август. Источник: PACER

Law360 сообщил, что в рамках соглашения о признании вины Шатт и Подулка признали, что выборочно представляли положительную «информацию при утаивании негативных новостей» в рамках плана «побудить клиентов одалживать свою американскую валюту и цифровые валюты Cred».

Как сообщается, федеральные прокуроры представили возможный диапазон приговоров до 72 месяцев для Шатт и до 62 месяцев для Подулки. Шатт и Подулка обвинялись в 13 случаях мошенничества с использованием электронных средств и отмывания денег.

Убытки клиентов Cred превышают $150 млн

Когда Cred обанкротилась и подала заявление о банкротстве, ее клиенты понесли убытки в размере до $150 млн, но Министерство юстиции США заявило в мае 2024 года, что с тех пор активы выросли до рыночной стоимости, превышающей $783 млн.

В соглашении о признании вины ответчики согласились, что их действия привели к убыткам пользователей в размере от $65 млн до $150 млн.

Бывший главный коммерческий директор Cred Джеймс Александр также был обвинен в мошенничестве с использованием электронных средств связи и отмывании денег.

Прокуроры утверждали, что руководители Cred вводили клиентов в заблуждение относительно кредитной и инвестиционной практики Cred и не раскрывали, что ее кредитный портфель в значительной степени зависел от китайской фирмы MoKredit, которая выдавала необеспеченные микрозаймы китайским геймерам.

Кроме того, Cred якобы утверждала, что занимается только обеспеченным кредитованием, и все ее криптоинвестиции были хеджированы, что, по словам прокуроров, было ложью.

После того, как цена биткоина упала на 40% 11 марта 2020 года, Cred не смог выполнить свои маржинальные требования и приблизился к банкротству, и три руководителя искали новых клиентов, преуменьшая риски, заявили прокуроры.

Когда Cred объявила о банкротстве в ноябре 2020 года, многочисленные пользователи выразили в социальных сетях обеспокоенность, спрашивая в безопасности ли их средства.

Другие основатели криптовалютных компаний также столкнулись с правовыми последствиями в этом году. 8 мая Алекс Машинский, основатель и бывший генеральный директор обанкротившейся платформы криптокредитования Celsius, был приговорен к 12 годам тюремного заключения за мошенничество.

Ранее, 10 января, соучредитель и главный трейдер Wolf Capital Трэвис Форд признал себя виновным в сговоре с целью мошенничества с использованием электронных средств за его роль в привлечении более 9 миллионов долларов от инвесторов с помощью ложных обещаний высокой прибыли.