撰文:papiofficial

编译:zhouzhou,BlockBeats

编者按:本文讨论了以太坊在 Rollup、L2、L3 等技术发展中的角色变化。随着项目通过 Rollup 即服务(RaaS)推出自己的链,团队的焦点逐渐转向产品、用户和代币,而不再关注与以太坊的对齐。作者通过「被遗弃的母亲」比喻,以太坊逐渐成为背离它的项目的「母亲」,ETH 作为资产在这个过程中被稀释。作者提问:如果以太坊不想变成这种「母亲」,它应该如何应对这种变化?

以下为原文内容(为便于阅读理解,原内容有所整编):

以太坊社区花了很多时间在讨论 Rollup、L2 和 L3 是否从以太坊 L1 中提取了价值。在过去的 24 小时里,@ameensol、@haydenzadams、@wmougayar、@siobh_eth、@TrustlessState 等人都深入参与了这场讨论。

我的看法是:任何将交易和活动从以太坊 L1 转移出去的行为,本质上都是一种价值提取行为。

这并不一定是坏事。但我认为,从长远来看,这确实会影响 ETH 这个资产。

让我用两个角度来解释:一个是丰田(Toyota)的类比,另一个是我曾参与顾问的一个现实世界中的 Rollup 项目。

在丰田工作时,我从我的精益导师那里学到一个原则,叫做 Genchi Genbutsu(現地現物)。意思是:「亲自去看。」不要只依赖数据面板或二手信息,要直接去体验事物本身。这个理念深深影响了我分析以太坊等生态系统的方式。

Genchi Genbutsu 教你避免陷入抽象的陷阱。

数据当然有帮助,但如果没有第一手的实际体验,数据就是不完整的。

我参与过几个 Rollup 项目的上线,每次都目睹了同样的变化。而有趣的地方,就在这里开始了。

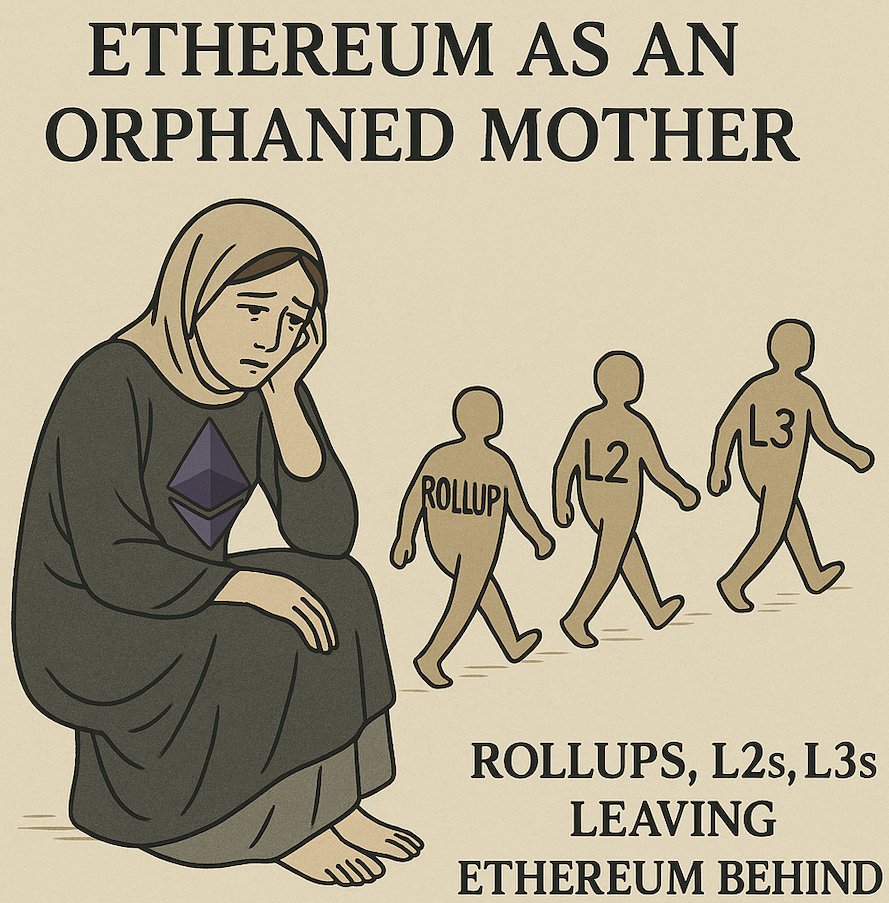

这里我想引入一个概念:「被遗弃的母亲」(Orphaned Mother)。

在哲学中,这个词指的是像物理、数学和经济学这样的学科,最初都是从哲学中诞生的。

哲学孕育了它们,但它的「孩子们」长大后却离开了它,最终她成了被遗弃的母亲。

每一个新的 Rollup、L2、L3 的出现,都会让以太坊逐渐变成那个「被遗弃的母亲」。

几年前,我曾为一个专注于特定领域的 Rollup 项目提供过建议。团队成员全都是坚定的以太坊信仰者——我早在 2017 年 ETH San Francisco 活动上就认识了他们。

起初,他们都是理想主义者。

他们当时用的是像 @gelatonetwork、@alt_layer、@conduitxyz 或 @Calderaxyz 这样的 Rollup 即服务(Rollup-as-a-Service)提供商。这些公司都非常优秀,也很好地服务了他们的客户。

整个过程非常简单,甚至不到 30 分钟,就能搞定:你就拥有了一条属于自己的链。

也就是从那一刻开始,一切开始发生变化了。

上线之后,他们的心态变了。他们不再只是构建者,而是成了创业者。

他们的关注点转向了产品、用户、社区、增长。他们全身心投入在自己的链和代币上。

至于是否与以太坊保持一致?已经排不上前十的优先事项了。

这并不是在批评他们,而是现实的情况。

当你运营自己的链时,你的思维模式会发生改变。你会优化自己的飞轮、自己的激励机制、自己的代币。

以太坊就成了那个被遗弃的母亲。

回到 Genchi Genbutsu——亲自去看。

启动你自己的 Rollup,使用一个 RaaS,尝试去发展它,发行你自己的代币。亲身体验一下,你会发现你的心态是如何从 ETH-maxi 转变为代币创始人的。你会感受到这种变化。

让我总结一下:

(1) 启动你自己的链会把你从一个与以太坊保持一致的构建者转变为一个商业拥有者。

(2) 这种拥有者的心态让 ETH 变得可选。

(3) 不要只听我说,自己去验证一下。

这既不是好事,也不是坏事,它就是这样。但如果以太坊想避免成为模块化堆栈中的「被遗弃的母亲」,它就需要正面应对这种动态。

在这个模型中,ETH 作为资产确实会被稀释。问题是:我们该如何应对?