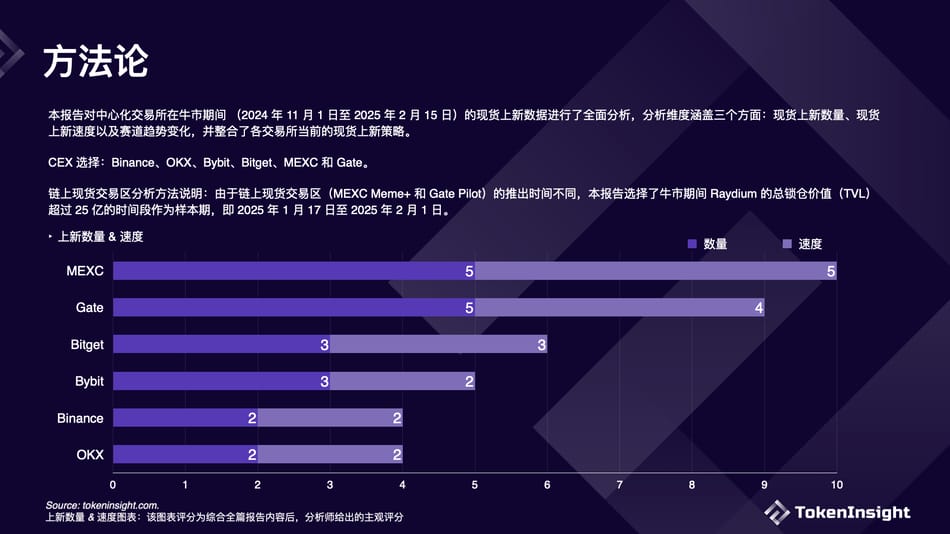

根据统计结果,交易所现货上币数量和速度排名如下:

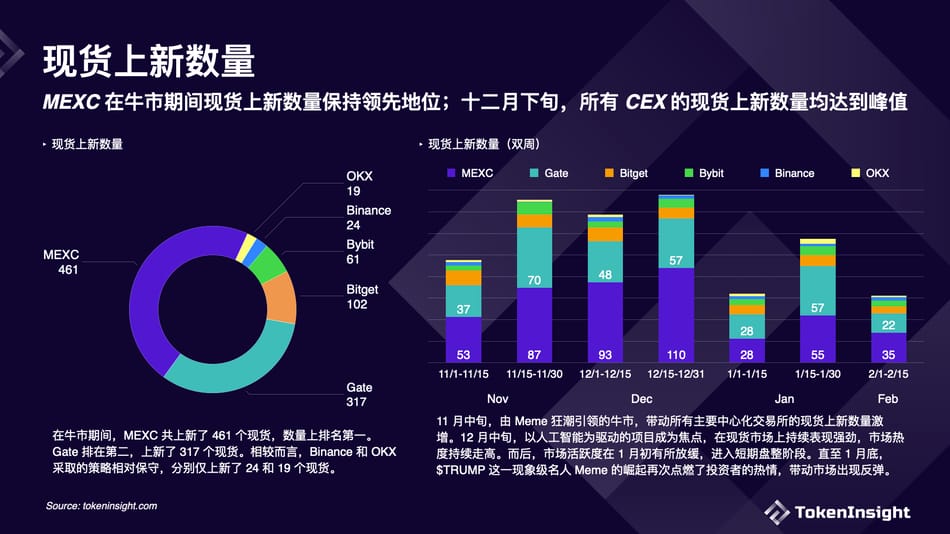

现货上新

在牛市期间,MEXC 共上新了 461 个现货,数量上排名第一。Gate 排在第二,上新了 317 个现货。相较而言,Binance 和 OKX 采取的策略相对保守,分别仅上新了 24 和 19 个现货。11 月中旬,由 Meme 狂潮引领的牛市,带动所有主要中心化交易所的现货上新数量激增。

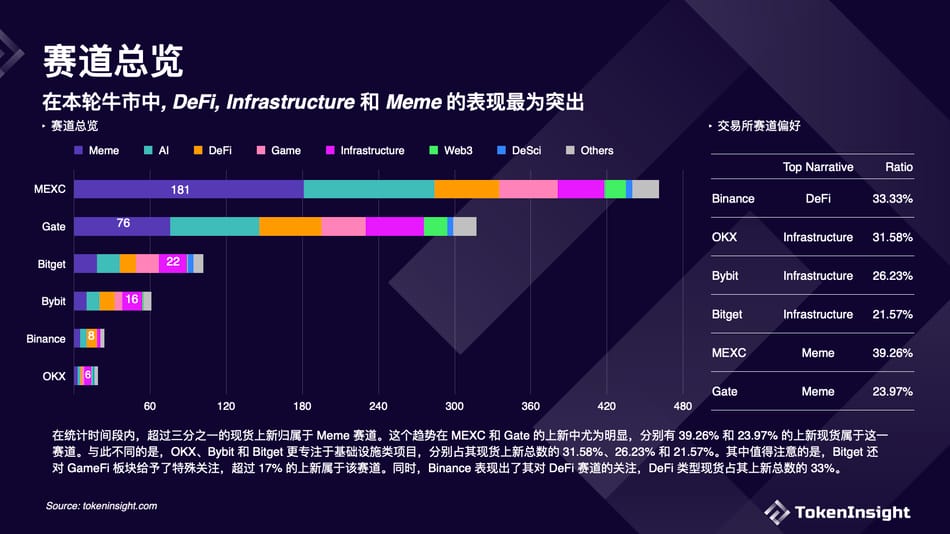

赛道总览

在统计时间段内,超过三分之一的现货上新归属于 Meme 赛道。这个趋势在 MEXC 和 Gate 的上新中尤为明显,分别有 39.26% 和 23.97% 的上新现货属于这一赛道。与此不同的是,OKX、Bybit 和 Bitget 更专注于基础设施类项目,分别占其现货上新总数的 31.58%、26.23% 和 21.57%。其中值得注意的是,Bitget 还对 GameFi 板块给予了特殊关注,超过 17% 的上新属于该赛道。同时,Binance 表现出了其对 DeFi 赛道的关注,DeFi 类型现货占其上新总数的 33%。

链上交易板块

MEXC 和 Gate 分别提供了链上资产交易板块以帮助交易者在牛市期间更快触及链上热门资产:即 MEXC Meme+ 和 Gate Pilot。在选定时间段内,Gate 上新了更多的链上现货资产,而 MEXC 则有着更高的正式现货转化率和更低的破发率。

现货上新速度

根据市场趋势的变化,本报告选出了四个热门赛道:Meme、AI、DeSci 和 Celebrity Meme。每个赛道中选择了两种类型的代币作为代表:一种是较多 CEX 上新的代币,另一种是短期内交易量激增的代币。

$TRUMP and $VINE 是最具代表性的名人 Meme,均已在多个交易所上市。 其中,MEXC 上币最为迅速。

MEXC 在 DeSci 和 Meme 领域的上币速度表现突出,而 Bitget 和 Gate 在 AI 领域上币速度更为迅速。有关详细的上币速度信息,请参阅完整报告。

现货上币策略

根据前置分析,我们汇总了每个 CEX 的现货上币策略。

以上是报告的部分关键内容,详细内容请下载报告全文阅读。想了解更多关于交易所流动性的信息吗?立刻免费下载阅读!