原标题:《We surveyed 42 Solana founders. Here’s what they said.》

作者:Jack Kubinec

编译:白话区块链

Lightspeed 发起了一项匿名调查,并将其发放给 Solana 的创始人、重度使用者等,旨在真实了解他们对其他生态系统、风险投资公司、初创企业等的看法。

调查问题涵盖了多种选项,并提供了写入空格,经过语法和清晰度的编辑。

以下是我们对 42 位创始人的调查结果:

1、除了 Solana,你会选择哪个区块链?

也有创始人们表示: 如果不是 Solana,我就不会涉足加密货币。」

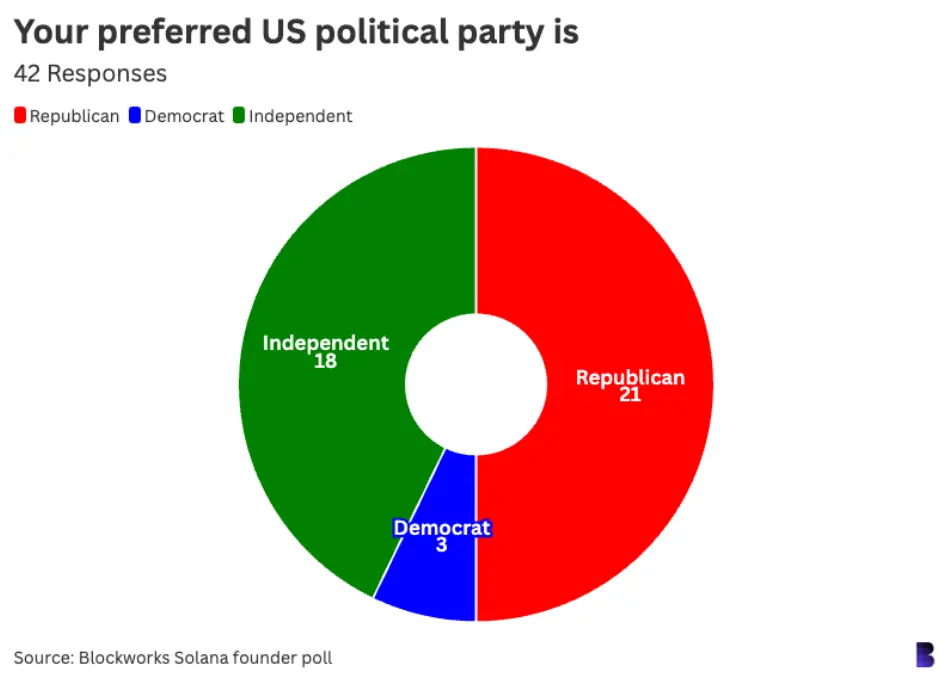

2、你最喜欢的美国政党是?

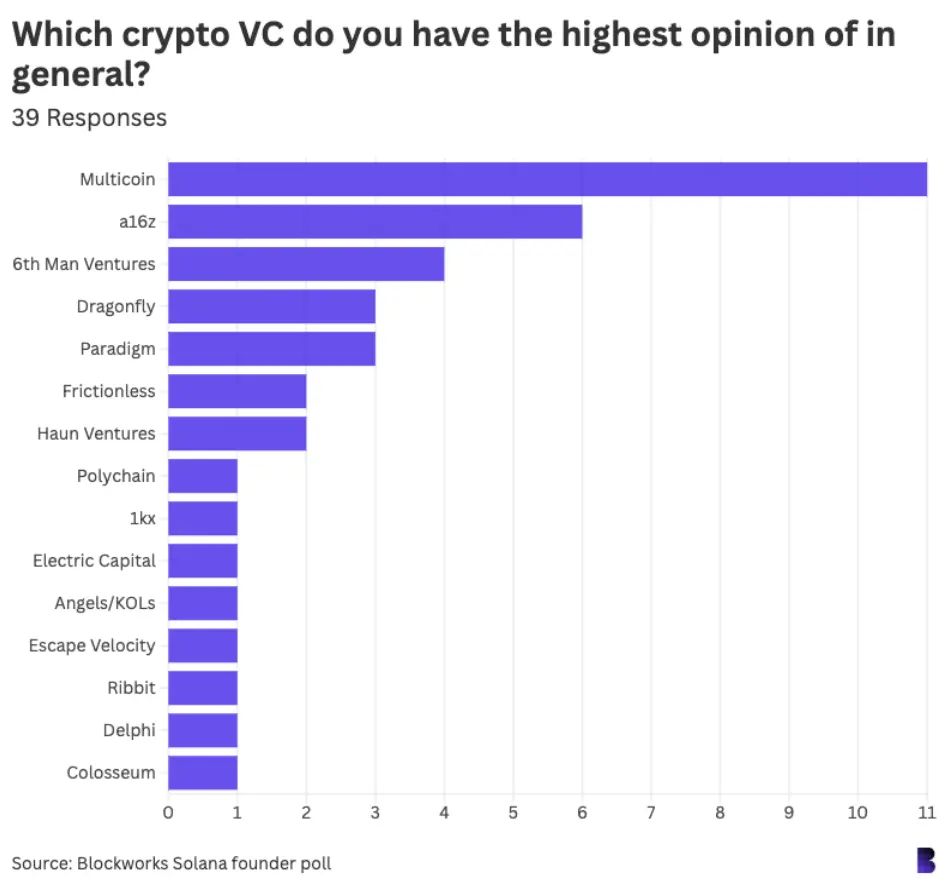

3、你对哪家 crypto VC 评价最高?

创始人们还表示: 「选择一个是不公平的。」

4、你最不看好的 crypto VC 是哪一家?

创始人们还表示:「仅根据领投方是谁而盲目跟投的亚洲风险投资公司也是不太 OK 的」

5、听说 Solana 内部圈子水很深,为了推动圈内项目的发展,常常以牺牲非圈内项目为代价?

创始人们还表示:

「我不知道,反正都一样,没什么太大区别。」

「我不喜欢这个问题,感觉是在挑起争议,而不是为了提供信息。」

「它确实存在,我也是其中一部分,但并不是‘以牺牲非圈内项目为代价’。因为我也投入了大量时间和资金在‘非圈内项目’上。这是双向的——你付出,也会有所回报。」

「它不存在,而我却是其中的一部分。」

「在早期和熊市时期,形成了一些个人关系网络。那些看重合作和帮助 Solana 的人,经过多年的努力,天然地建立了更加紧密的关系。一些人(包括来自 OG Solana Labs 团队的人)后来成为了有影响力的人物,拥有了大批追随者。这是自然的。几乎所有幸存的团队也都得到了风险投资和 Solana Ventures 的资助。这些都是事实,但在我看来并没有恶意。Solana 基金会在积极分散这种影响并支持生态系统中做得很出色的人们(例如 Superteam 等)。在我看来,Toly 特别擅长毫不偏袒地大力支持建设者,而不是根据个人喜好,而是依据 1) 他们所建设的项目很酷,2) 他们的诚意。」

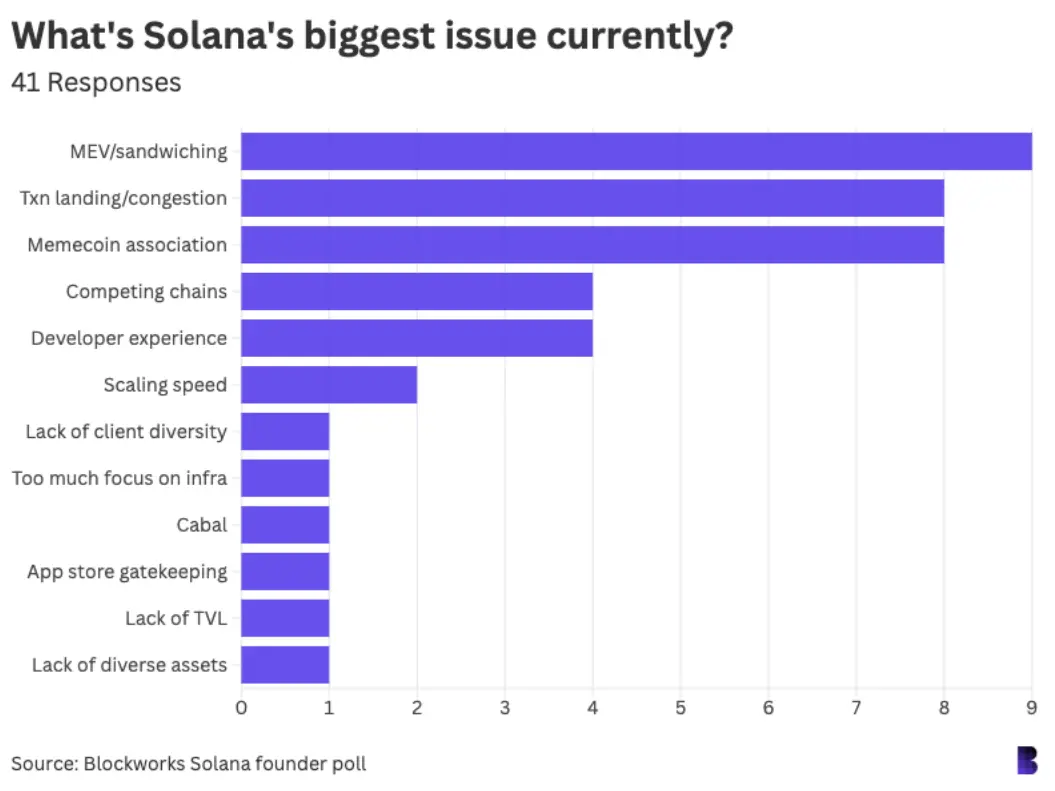

6、Solana 目前最大的问题是什么?

创始人们还表示: 「迫切需要更多的区块空间。需求增加 5 倍 + 价格上涨 2 倍 = 为了保持应用开发者的成本不变,需要将区块大小增加 10 倍!」

7、Memecoins 对于 Solana 的意义你怎么看?

8、Solana 还有很多非你们自创的初创公司,你最希望加入哪家 ?

9、哪家你最不想加入?

创始人们还表示: 「哪些还没有起色的公司也不想加入。」

10、最被高估的 Solana 板块是什么?

创始人们还表示: 「SocialFi、DeSci 和游戏都还要潜力。」

11、最被低估的 Solana 部门?

12、以下哪一项对 Solana 的声誉损害最大?

创始人们还表示:「FTX 在早期既是最出色的,也是最糟糕的,哈哈。」

这其中有很多值得深入探讨的内容,但我发现有几个点特别引人注意:其他创始人对 pump.fun 的评价不高,但他们普遍认为 memecoin 对生态系统是有益的。而 Base 和 Sui 似乎是目前最具吸引力的 Solana 竞争者。

作为一名记者,要让创始人在公开场合坦诚发言并不容易。这次调查帮助我更好地理解了 Solana 创始人们的真实想法——至少从整体来看还算真实。