原文标题:Random Sunday Thoughts on What Comes After Agent Tokenization?

原文作者:Defi 0x Jeff,加密 Kol

原文编译:zhouzhou,BlockBeats

编者按:本文讨论了代币化的趋势及其未来发展,涵盖了资产、艺术、收益、AI 代理等领域的代币化进展,介绍了各类代币化的先驱者如何推动行业变革,并探讨了未来可能的代币化趋势包括数据、注意力和 AI 应用的代币化,代币化不仅是技术创新,更是改变人们互动和创造新机会的力量。

以下为原文内容(为便于阅读理解,原内容有所整编):

代币化的概念一直让我着迷,看起来它很简单,但每当某个新的事物被代币化时,大家的注意力便迅速转向它。

以下是我们迄今为止见到的一些代币化趋势的总结,看看它们是如何发展起来的,以及未来可能会发生什么:

资产的代币化

最初的代币化趋势。

比特币创造了第一个去中心化、安全且透明的账本系统,为资产的数字化表示铺平了道路。随后, 2015 年以太坊的出现引入了智能合约,使得资产可以编程化——无论是房地产、艺术品还是 DeFi。

如今,以太坊的市场价值达到了 4700 亿美元,这就是代币化对资产带来的影响。

艺术的代币化(NFTs)

NFT 的崛起将代币化引入了艺术世界。

2017 年,像 CryptoPunks 和 CryptoKitties 这样的项目让 NFT 走进了公众视野。到了 2021 年,NFT 的交易量达到了 130 亿美元,成为代表数字艺术和收藏品的首选方式。像 CryptoPunks、BAYC、Art Blocks 等许多收藏品在 2021 年巅峰时的价格高达数百万美元。

收益的代币化

另一个重大变化是收益的代币化。

Pendle fi 在 2021 年率先提出了代币化未来收益的概念。它创建了一个市场,允许交易固定和可变收益,为 DeFi 增加了灵活性和流动性。Pendle 在 2023 年开始迅速增长,尤其是在 LST(流动质押代币)和 2024 年初的积分市场中。

如今,$PENDLE 的市场价值为 16 亿美元。

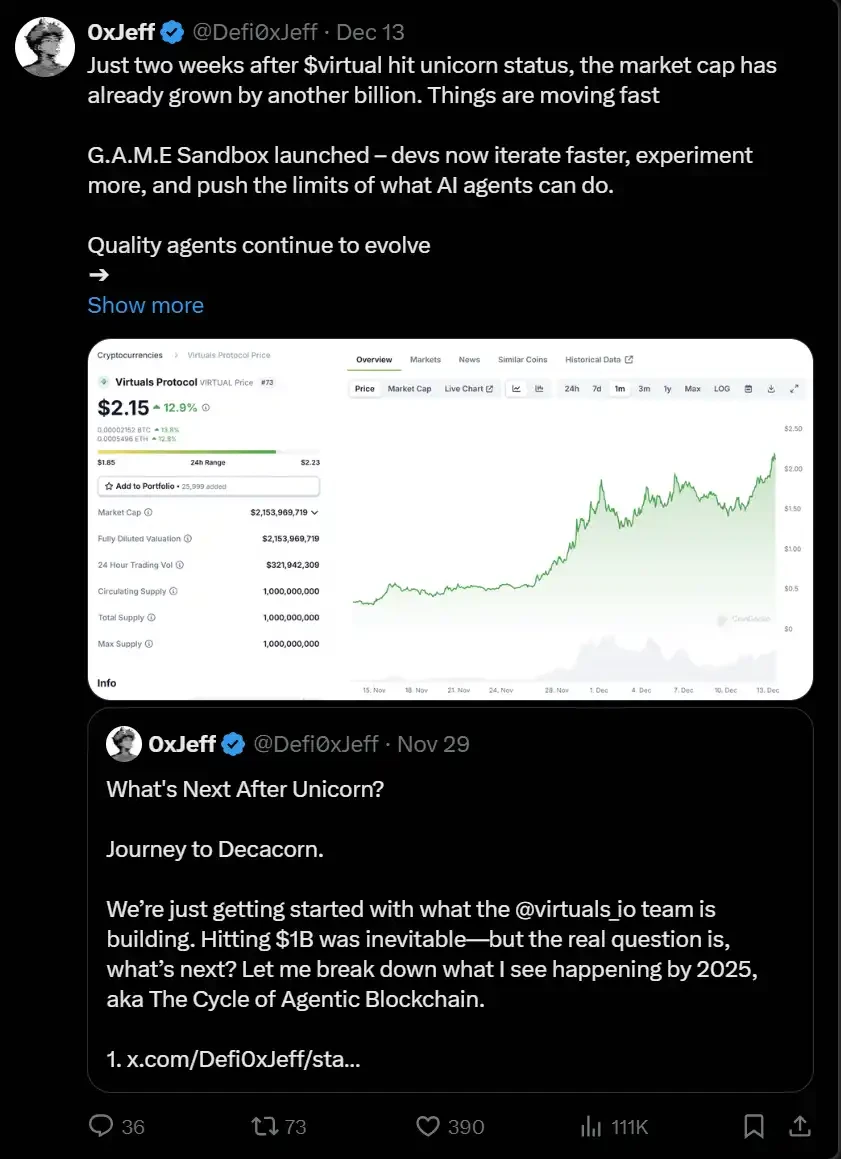

AI 代理的代币化

现在,我们看到了 AI 代理的代币化。

Virtuals io 推出了一个平台,用户可以在上面创建 AI 代理并将其代币化,从而有效地为其开发成本提供启动资金。

AI 代理的概念始于 2024 年 10 月,Virtuals 为代理所有权创造了市场。时至今日,$VIRTUAL 的市场价值已达到 25 亿美元。

代币化的下一个大趋势是什么呢?

在这些领域——资产、艺术、收益、AI 代理——我们可以看到一个明显的模式:每个领域的先驱者通常会经历快速的采纳和显著的价格波动。

以下是我正在关注的一些想法:

数据的代币化

withvana 正在探索 DataDAOs 和数据流动性池(DLPs)。

用户可以将数据贡献到这些池中,保持数据所有权,并根据贡献的质量获得奖励。

本质上,它将数据转化为一种流动的、可交易的资产。

$VANA 12 月 16 日上线,数据所有权代币化的概念可能会非常庞大。

注意力的代币化

kaitoai 正在致力于 Web3 中的注意力代币化,他们展示了通过平台、心智共享仪表板以及最近的 Yap-to-Earn 功能来生成并促进更多注意力的能力。

他们的 Yapper 排行榜激励思想领袖更多发声,赚取 Yap 积分,最终获得空投的$KAITO 代币。

基本上,Yap = 注意力 = $KAITO。这是一种有趣的方式,展示 Web3 如何重新定义用户参与度。

AI 应用的代币化

这看起来是 AI 代理趋势的自然延伸。

随着像 Replit 这样的工具和代理生态系统的崛起,我们离个性化软件创建越来越近。

代币化的 AI 应用可以让用户启动开发,并拥有应用产生的收入份额。

该领域的竞争者包括 alchemistAIapp 和 myshell ai,它们都赋能创作者构建创收的 AI 应用,提供实际和可扩展的用例。

Myshell 更进一步,允许投资者直接投资这些应用,并在未来获得应用产生的收入份额。这个模型不仅支持开发,还将创作者和投资者的利益对齐。

最终想法

代币化趋势总是带来新的创新和采纳浪潮,但它们令人兴奋的地方不仅仅是技术本身——而是它们如何将人们聚集在一起,并将焦点转向新的机会。