撰文:ParaFi Capital

编译:1912212.eth,Foresight News

我们正在深入研究以太坊在 EIP-4844 之后的发展情况,主要关注点在于以下三个重要方向:

-

ETH 销毁量最新进展如何?

-

L2 网络的吸引力怎么样?

-

L2 和以太坊之间的经济关联是什么?

EIP-1559 与合并升级之后,人们对 ETH 作为产生现金流资产的经济性感到兴奋。在最初两次升级后,ETH 的供应量确实下降了,从 2022 年 9 月到 2024 年 4 月,下降了约 0.38%。不过从那时起,随着销毁率的放缓,ETH 供应量就开始一路攀升。

过去的 12 个月里,ETH 质押奖励率一直呈下降趋势,因为以太坊验证者的数量在过去一年中增长了 79%,而 L1 交易费用却有所下降。

虽然销毁速度有所放缓,但 Uniswap、Tether、1inch 和 MetaMask 等应用或协议继续推动以太坊上的大部分 Gas 消耗。2023 年,Arbitrum 和 ZKsync 是主要的 Gas 消耗者,但今年其数据明显下降,这是因为 EIP-4844 提案使得 L2 可以更高效地发布数据,降低了其数据存储要求。

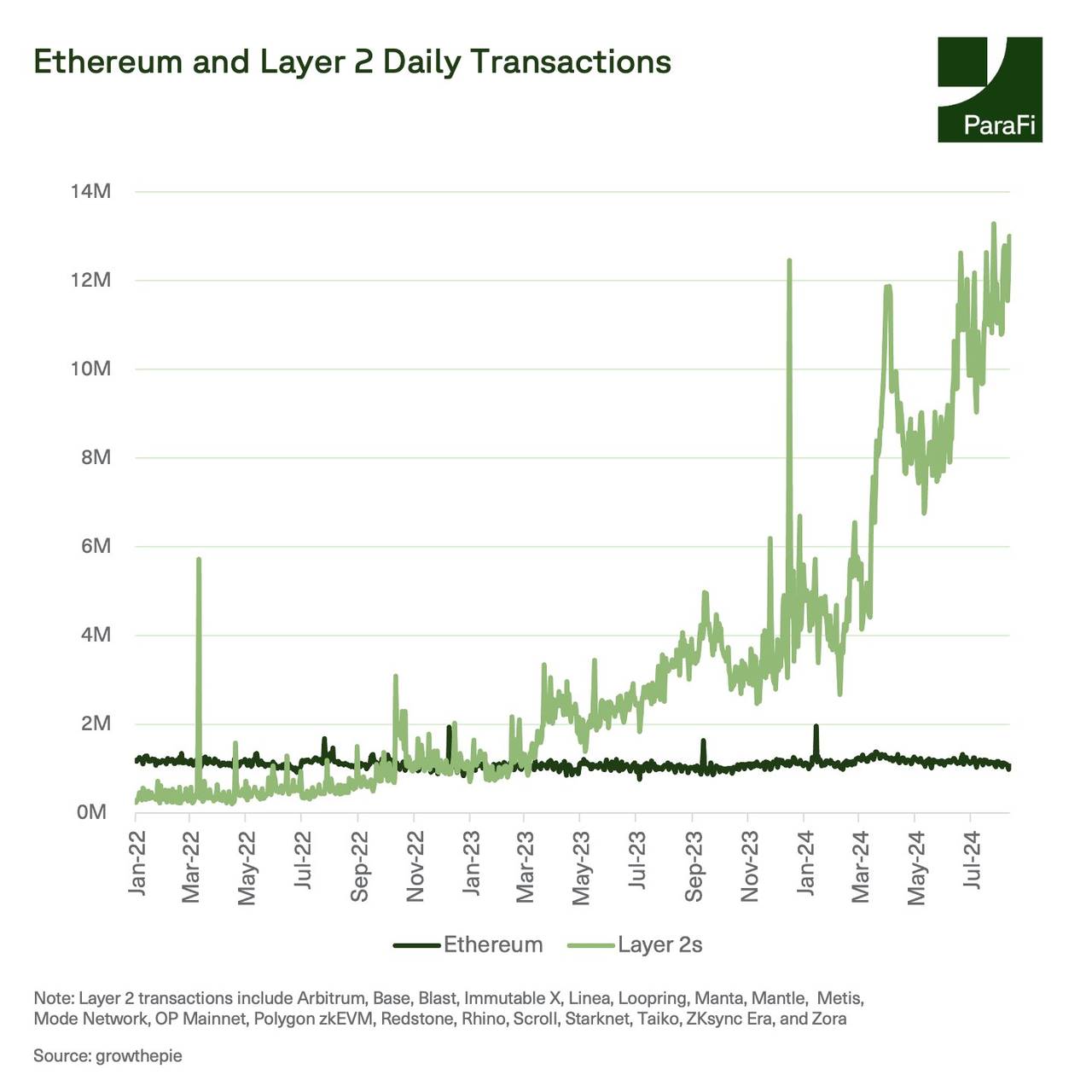

过去的两年半时间中,以太坊的交易笔数相对停滞,而 L2 的总交易笔数在 2024 年 8 月超过 L1 的 10 倍。

L2 活动的增长可以归因于新 L2 的推出和一些现有 L2 的爆炸式发展。3 月以来,Base 和 Arbitrum 的单日交易笔数都超过了以太坊。虽然这张图表汇总了多个 L2 的交易,但每个 L2 都在为以太坊提供替代的区块空间,突显出 L1 向 L2 转移的大趋势。

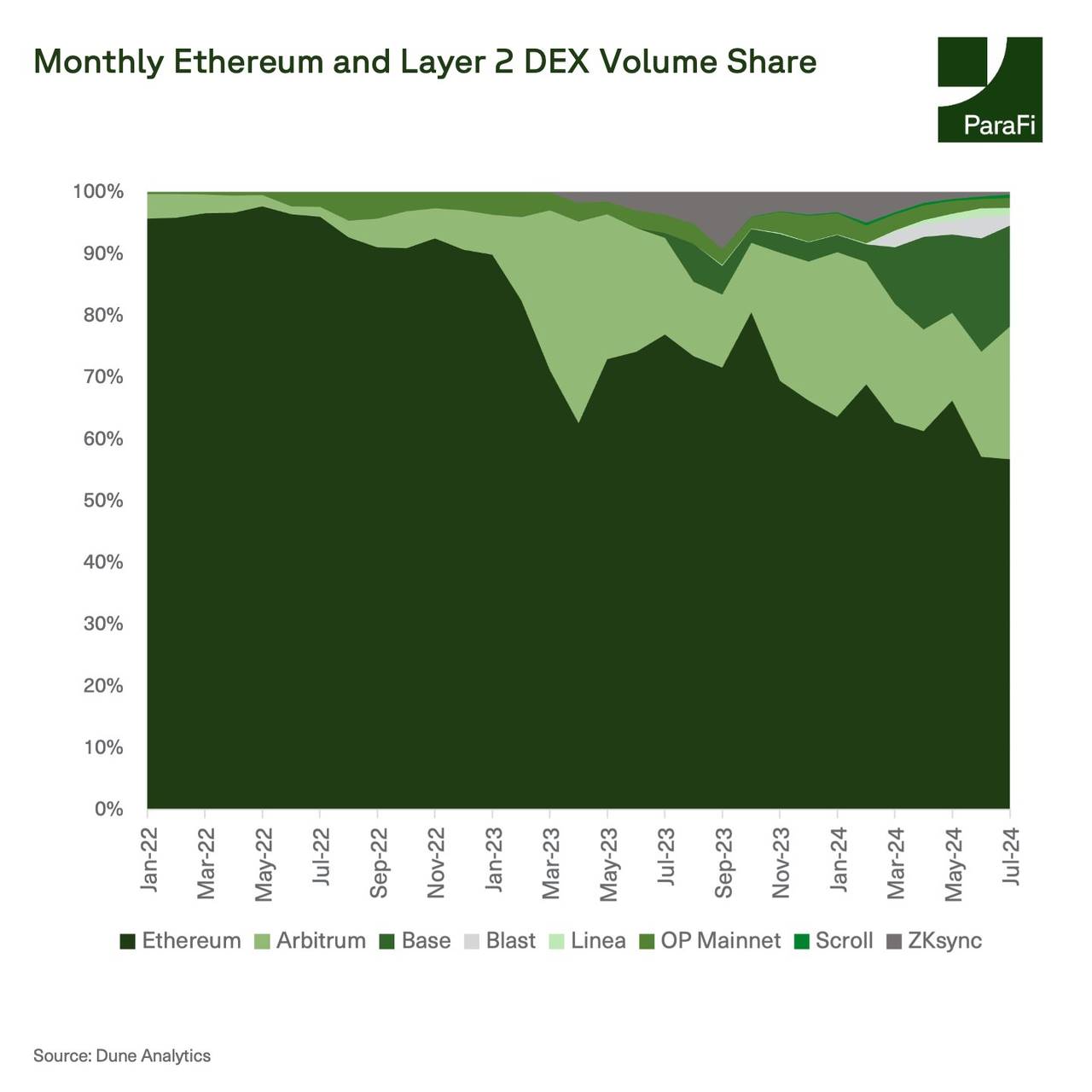

以太坊 L2 的日益增长也体现在它们从以太坊吸引了大量的 DEX 市场份额。EIP-4844 升级后,L2 已经将以太坊主网上的 DEX 市场份额压低至 60% 以下。

不过,这也突显了由于 Rollup 网络不断发展,而导致的流动性碎片化问题。尽管这些 L2 取得了巨大成功,但由于 EIP-4844 的升级,它们在以太坊上发布数据的花费相对较少。EIP-4844 于 2024 年 3 月实施,为以太坊引入了一种名为「blobs」的新数据存储机制,这是对之前的 Calldata 结构的更廉价替代方案。

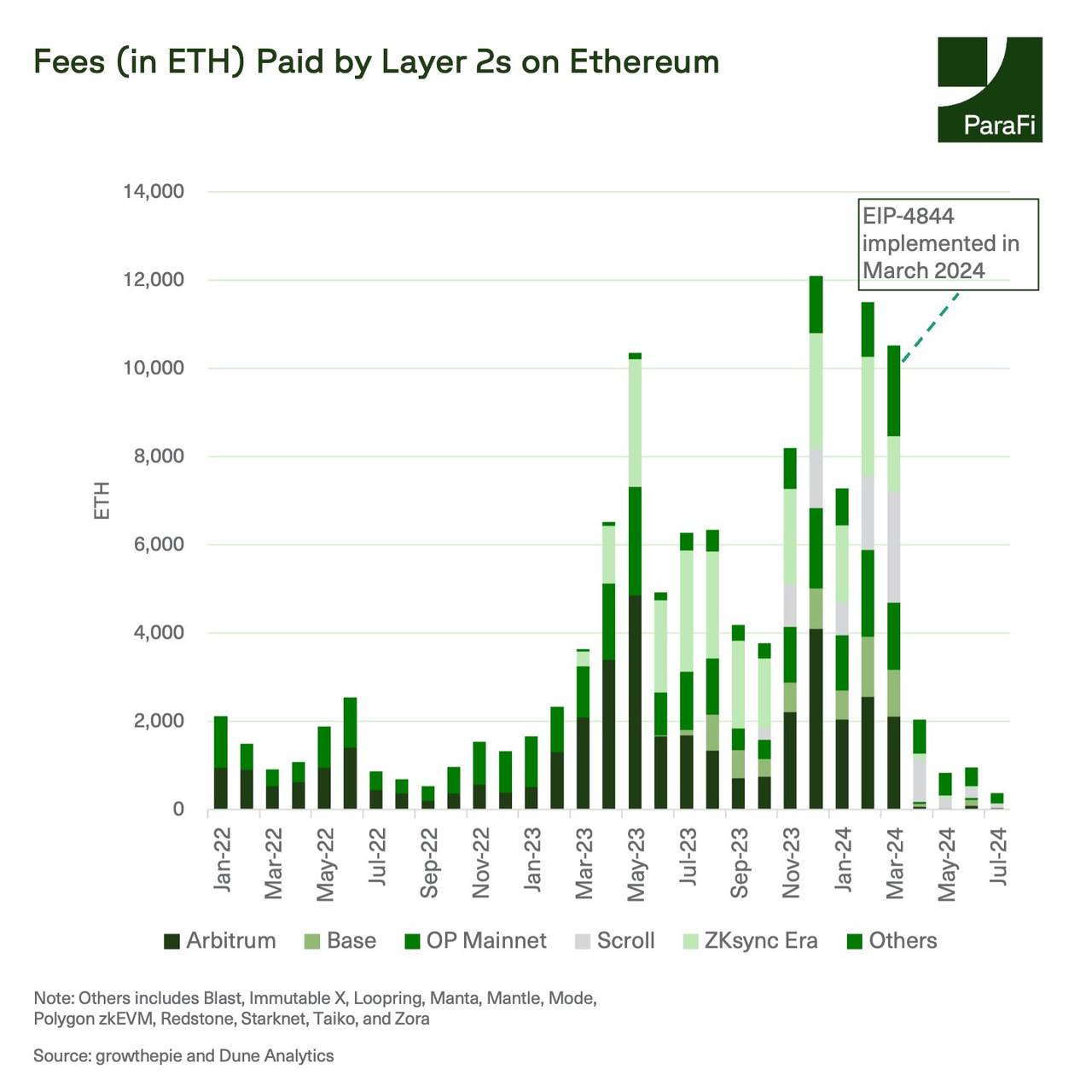

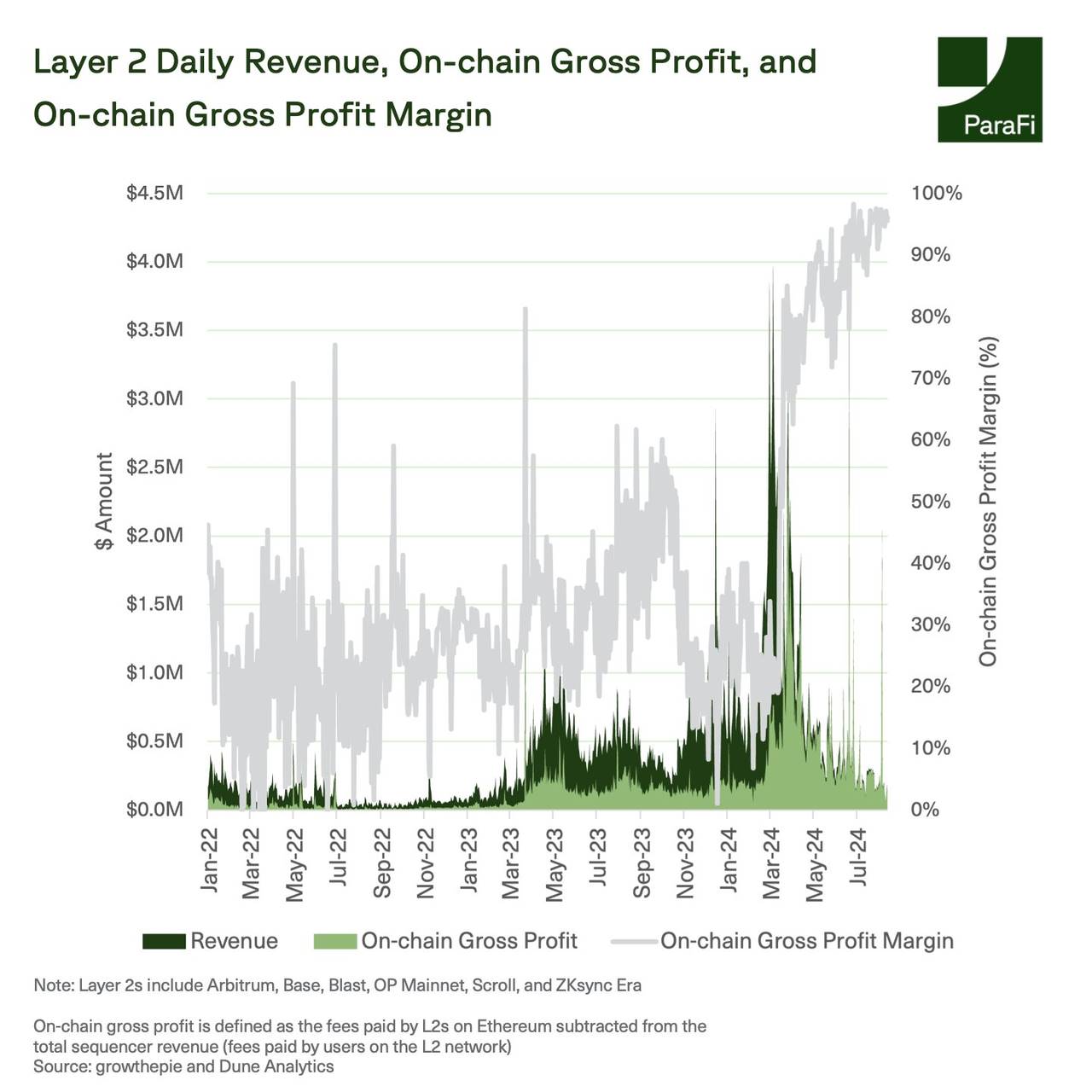

2024 年 3 月,L2 在以太坊上支付的费用超过了 1 万枚 ETH,但在 7 月份,它们支付的费用不到 400 枚 ETH,下降了约 96%。随着成本的下降,L2 现在对 ETH 的销毁贡献更少,也降低了主网上的 Gas 费。

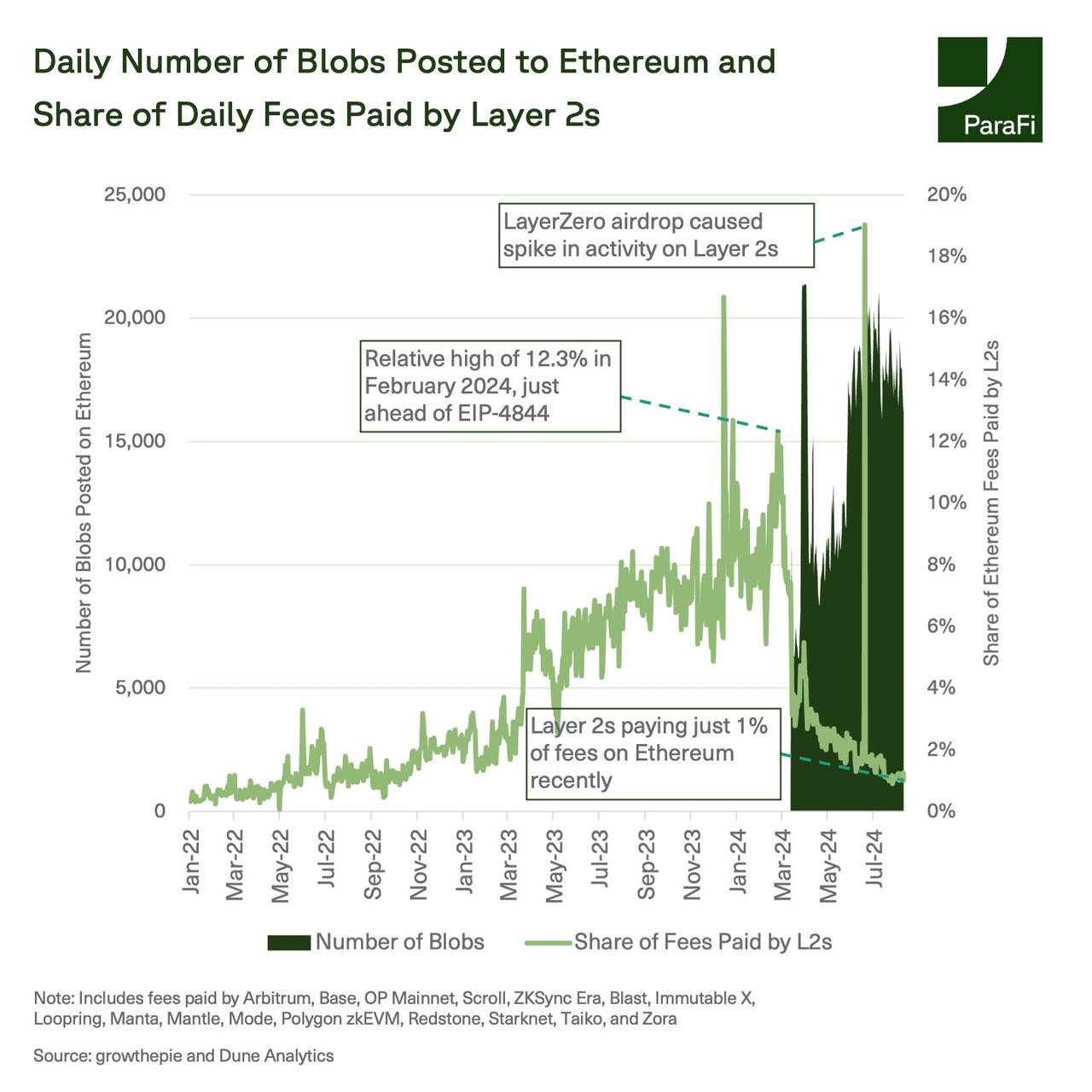

由于 L2 需要在链上发布大量的交易概要数据,它们迅速采用了 blobs。自 6 月初以来,以太坊每天至少有 1.6 万个 blobs 被发布。这导致主要 L2 所支付的总费用比例下降,从 2024 年的 12% 降至 1%。

自 EIP-4844 实施以来,L2 的运营利润率大幅提高。尽管扩展解决方案的总排序器收入(即在 L2 网络上支付的费用总和)今年以来平均下降了约 48%,但运营成本下降了约 87%,这意味着 Rollup 现在保留了大部分收入。主流 L2 现在的运营利润率都超过了 90%,即使在将大量的成本节省发送给用户之后也是如此。用户从中受益,在使用 blobs 的网络上,过去一年中费用下降了约 90%,其中中位数交易成本通常低于 0.01 美元。

EIP-4844 对以太坊 L1 产生了明显的影响。

尽管 L2 使用量激增,但对 ETH 作为资产的直接收益尚不明确。过去几个月中,尽管 L2 的利润大幅上升,但 ETH 的销毁率下降,导致流向 ETH 的价值减少。

这给以太坊生态系统留下了很多需要思考的问题:

-

随着 L2 使用量的持续增长,L2 代币将发挥什么作用?L2 代币与 ETH 相比,将捕获多少价值?

-

Rollup 相对于以太坊的收益是否过多?或者这种结构是否理想,以吸引更多用户和开发者进入更广泛的以太坊生态系统?

-

随着更多 L2 的推出,用户和流动性将如何在这些不同的网络之间互操作?

-

由于以太坊主网的费用现已处于历史地位,我们是否会看到开发者重新考虑直接在 L1 上部署,还是 L2 仍然更具吸引力?