BitMine Immersion Technologies is moving deeper into the public-market crypto treasury trade, filing for a preferred stock offering that could help fund additional Ethereum purchases and validator infrastructure. The structure puts the company closer to the capital-markets model popularized by Michael Saylor’s Strategy, but with ETH rather than Bitcoin as the core reserve asset.

The Norwalk, Connecticut-based company said it intends to offer 3,000,000 shares of 9.50% Series A Perpetual Preferred Stock in a public offering registered under the Securities Act. The preferred shares carry a stated amount of $100 per share, implying a potential $300 million stated-value issuance if sold at that level, though the company said the deal remains subject to market and other conditions.

BitMine Files Yield Offering As It Builds Ethereum Treasury

BitMine framed the proceeds broadly, but Ethereum sits at the center of the filing. The company said it intends to use net proceeds “for general corporate purposes, which may include the acquisition of additional ETH and other digital assets; the expansion of the Company’s staking and validator infrastructure, including through MAVAN; working capital; strategic investments aligned with the Ethereum ecosystem and broader digital asset adoption; and/or repurchases of the Company’s common stock under its share repurchase program.”

BitMine has committed to ETH as its primary treasury reserve asset and says it is using native protocol-level activity, including staking and decentralized finance mechanisms, as part of that strategy. In 2026, the company launched MAVAN, or Made-in America VAlidator Network, as dedicated staking infrastructure for BitMine assets.

The comparison with Saylor’s Strategy comes from the financing mechanism. Strategy built its Bitcoin treasury model not only through common stock and convertible debt, but also through preferred equity products (STRC and STRF) designed to attract yield-oriented investors while raising capital for digital asset accumulation.

BitMine is now applying a similar template to Ethereum: issue a yield-bearing security in the public markets, use the proceeds flexibly, and route part of the capital toward a crypto treasury asset with institutional-market packaging around it.

The preferred stock itself is structured as a cash-paying instrument. BitMine said the Series A Preferred Stock will accumulate cumulative dividends at a fixed rate of 9.50% per year on the $100 stated amount, whether or not dividends are declared or funds are legally available for payment. “Regular dividends on the Series A Preferred Stock will be payable when, as and if declared by BMNR’s board of directors, out of funds legally available for their payment, weekly in arrears,” the company said. “Declared regular dividends on the Series A Preferred Stock will be payable solely in cash.”

The filing also includes a penalty mechanism if dividends are not paid on schedule. Any unpaid accumulated regular dividend would itself begin accumulating additional dividends, compounded weekly. The compounded dividend rate initially equals 9.50% plus 5 basis points, based on a weekly regular dividend period, and increases by another 5 basis points for each subsequent period until paid in full, capped at 15% per year.

BitMine will retain redemption flexibility. The company can redeem the preferred stock in whole or in part for cash at 110% of stated amount during the first 18 months after issuance, 105% from 18 months to three years, and 100% after three years, plus accumulated and unpaid dividends. It can also redeem all outstanding preferred shares if the total remaining falls below 25% of the original issuance, or if certain tax events occur.

Holders also receive protection in the event of a “fundamental change.” If such an event occurs under the certificate of designations, preferred shareholders can require BitMine to repurchase some or all of their shares for cash at the stated amount, plus accumulated and unpaid regular dividends.

BitMine has applied to list the preferred stock on the New York Stock Exchange under the ticker BMNP. If approved, the company expects trading to begin within 30 days after the shares are first issued. Moelis & Company and Cantor are acting as joint lead bookrunners.

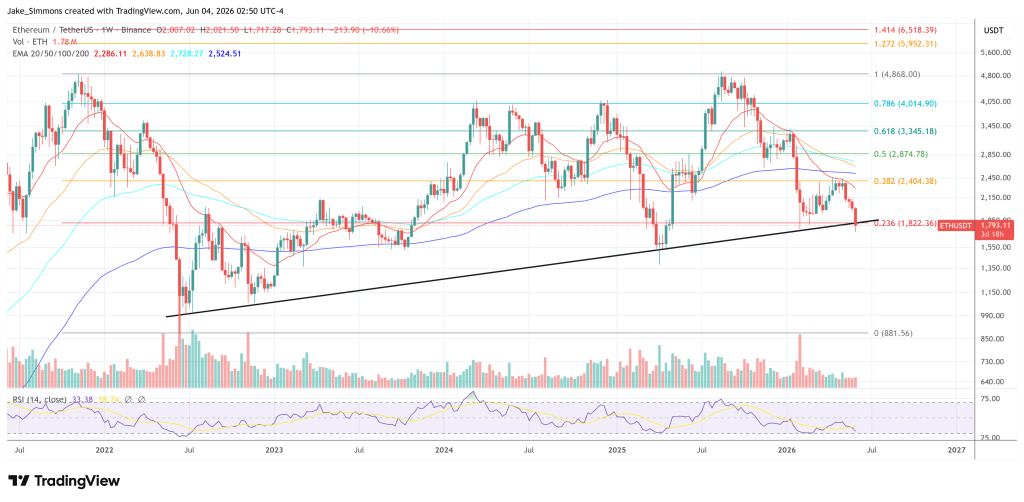

At press time, Ethereum traded at $1,793.