Author: Prathik Desai

Original Title: Crypto’s Revenue Recipe

Compiled and Edited by: BitpushNews

I've always loved the "seasonal" traditions of the crypto community. Like Uptober (October surge) or Recktober (October crash). Community members always love to throw around a ton of statistics around these times. After all, humans are naturally fond of trivia, aren't they?

And the trend analysis and reports that unfold around this data are even more interesting. You always hear arguments like: "This time, the ETF fund flows are completely different"; "Crypto industry funding has finally matured this year"; "BTC is ready for this year's pump", and so on.

Recently, while reading a report called State of DeFi 2025, I was drawn to a few charts about how crypto protocols generate "real revenue".

These charts show the top protocols with the highest revenue across the industry over the past year. They prove a fact that has been discussed repeatedly in the industry over the past year: the crypto industry is finally starting to find "generating revenue" to be a very sexy thing. But what exactly is reshaping this revenue landscape?

Hidden behind these charts is another little-known story worth digging into: where do these collected fees ultimately flow?

I dug deep into DefiLlama's fee and revenue data (revenue refers to the retained fees after deducting payments to liquidity providers and suppliers), trying to find the answer.

In the quantitative analysis of this article, I will try to add some dimensions to these numbers, to show you how money flows and where it goes in the crypto world.

2025: Revenue Doubles, Old Guard Dominance Remains

Last year, the total revenue generated by crypto protocols exceeded $16 billion, more than double the approximately $8 billion in 2024.

Value capture capabilities have been expanding throughout the crypto industry. Over the past 12 months, decentralized finance (DeFi) has seen the emergence of many new categories, such as decentralized exchanges (DEXs), token launch platforms (Launchpads), and perpetual futures exchanges (Perp DEXs).

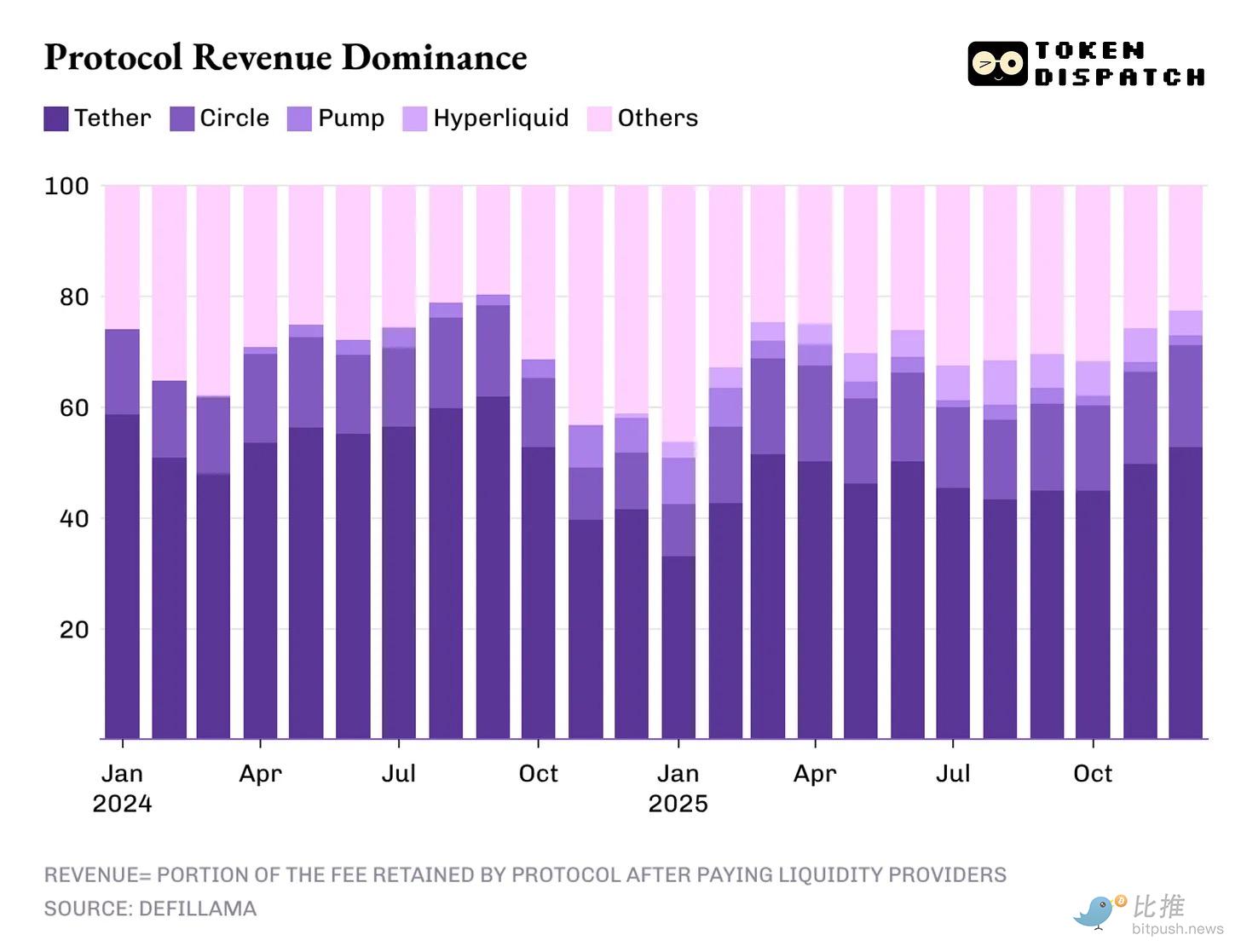

However, the "profit centers" generating the highest revenue are still concentrated in those established categories – most notably stablecoin issuers.

The two stablecoin giants Tether and Circle accounted for over 60% of the total annual crypto industry revenue. By 2025, this share only slightly decreased from about 65% the previous year to 60%.

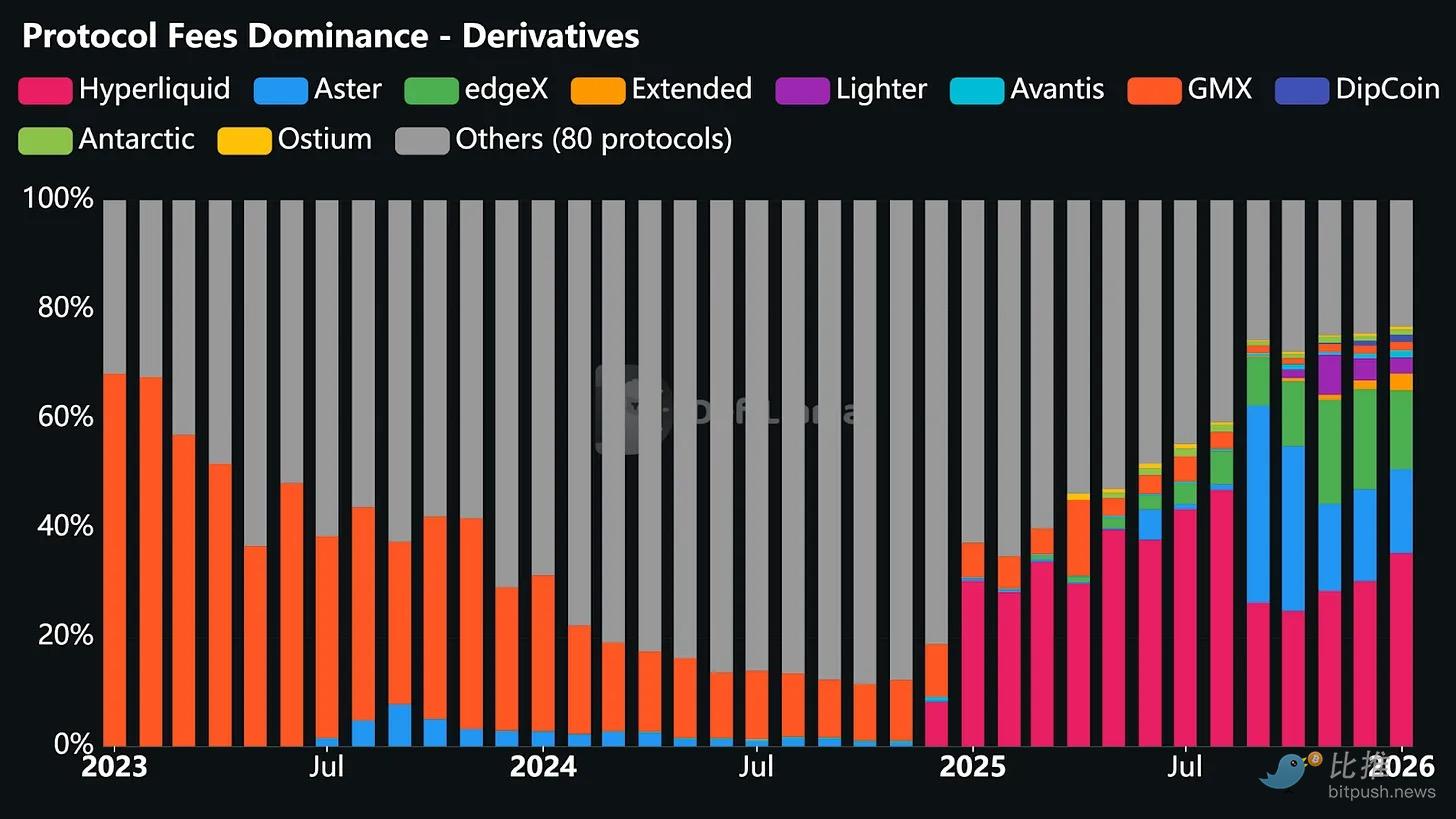

However, the achievements of perpetual futures exchanges (Perp DEXs) in 2025 should absolutely not be underestimated – remember, they were almost "non-existent" in 2024. Hyperliquid, EdgeX, Lighter, and Axiom together contributed 7% to 8% of the industry's total revenue, a share far exceeding the combined total of mature DeFi categories like lending, staking, cross-chain bridges, and DEX aggregators.

2026's Revenue Engines: Carry, Execution, and Distribution

So, what will drive revenue in 2026? I found the answer in three core elements that influenced last year's revenue concentration: Carry, Execution, and Distribution.

1. Carry Trade

Carry trade means that whoever holds and transfers funds can earn returns through this holding and transfer.

The revenue model of stablecoin issuers is both "structural" and "fragile".

-

Structural: Because it scales with the growth in supply and circulation. Every digital dollar they hold is backed by treasury bonds, which generate interest.

-

Fragile: Because the model relies on a macro variable that the issuer has almost no control over: the Federal Reserve's interest rates. And the "rate cut cycle" has just begun. As rates fall further this year, the revenue dominance of stablecoin issuers will weaken accordingly.

2. Execution

This is where DeFi protocols build perpetual futures (Perp DEXs), the most successful DeFi category of 2025.

The simplest way to understand why perpetual futures exchanges have been able to capture market share so quickly is to see how they help users execute actions. They build a venue that helps users enter or exit risk according to their needs at any time, with minimal friction. Even if market volatility is low, users can still hedge, trade on leverage, arbitrage, rotate capital, or simply open positions for research purposes to plan for the future.

Unlike spot DEXs, they allow users to conduct continuous, high-frequency trading without the inconvenience of moving the underlying assets.

While "execution" sounds simple and extremely fast, there's a lot beneath the surface. These futures exchanges must build a robust trading interface that doesn't crash under high load, host a matching and liquidation system that can stand firm in market chaos, and provide sufficient liquidity depth to retain traders. In perpetual futures exchanges, liquidity is the "secret sauce." Whoever can offer consistent and ample liquidity will attract the highest trading activity.

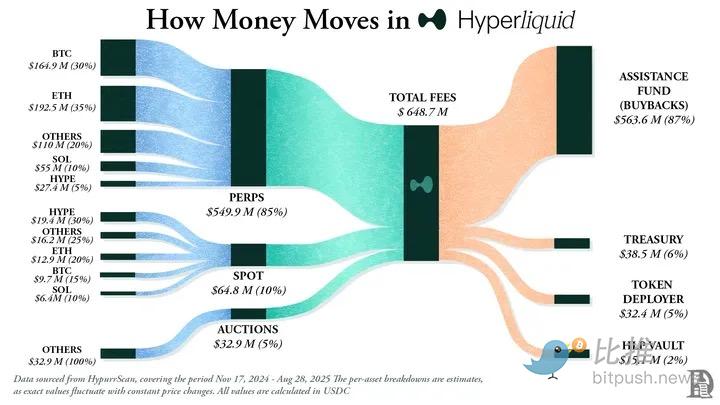

In 2025, Hyperliquid dominated the futures exchange track by attracting the largest number of market makers on its platform to provide ample liquidity. The result was that Hyperliquid dominated fee collection for 10 out of the 12 months last year.

Ironically, these DeFi category futures exchanges succeeded precisely because they don't require traders to understand blockchain and smart contracts, instead operating more like those familiar traditional exchanges.

Once the above issues are resolved, the exchange can generate revenue on "autopilot" by charging marginal fees on traders' high-frequency, high-volume trading activity. This continues even if spot prices are consolidating, simply because the options available to traders on the platform are so diverse.

This is precisely why I believe that, although futures exchanges' revenue share was only in the single digits last year, they are the only category that can remotely challenge the dominance of stablecoin issuers.

3. Distribution

The third factor – distribution – drives incremental revenue for crypto projects (like token issuance infrastructure). Think pump.fun and LetsBonk.

This isn't much different from what we see in Web2 companies. While Airbnb and Amazon don't own any inventory, their powerful distribution capabilities have helped them transcend the role of "aggregators" and reduce the marginal cost of adding new supply.

Crypto distribution infrastructure similarly does not own the assets (like Memecoins, tokens, and micro-communities) created through its platform. However, by making the user journey frictionless, automating the listing process, providing ample liquidity, and simplifying trading, it becomes the default place for people to create crypto assets.

In 2026, two questions may determine the trajectory of these revenue drivers: Will the revenue share of stablecoins fall below the 60% range as rate cuts eat into carry trades? Can futures exchanges break through their 7-8% stronghold as the execution layer consolidates?

Transforming "Revenue" into "Ownership"

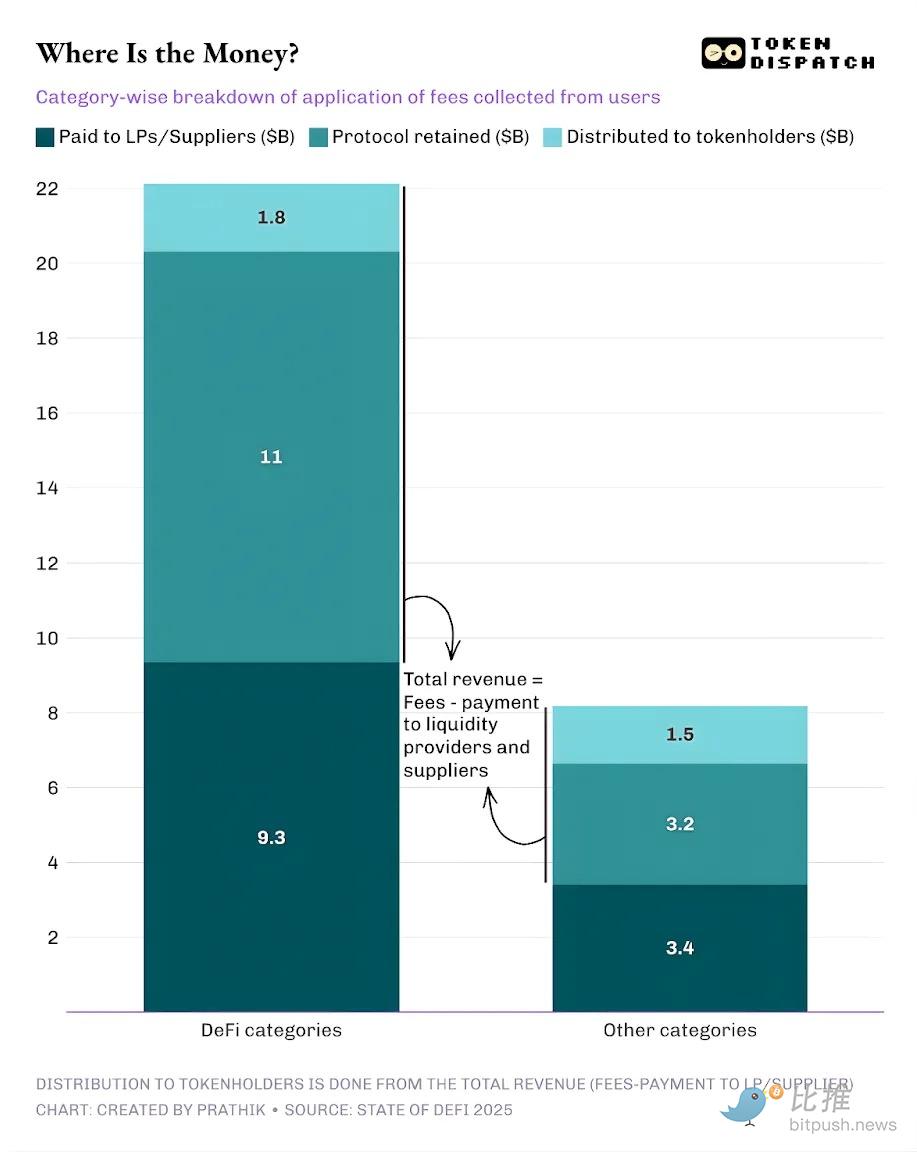

The three factors of carry, execution, and distribution reveal how crypto revenue is generated. But that's only part of the story. Equally important (if not more so) is: what proportion of the gross fee is allocated to token holders before the protocol retains net revenue?

Value transfer achieved through token buybacks, token burns, and fee sharing marks a token as an "economic ownership claim," not just a "governance medal."

In 2025, users of DeFi and other protocols paid approximately $30.3 billion in fees. Of this, $17.6 billion was retained by the protocols as revenue after payments to liquidity providers and suppliers. About $3.36 billion of the total revenue was returned to token holders through staking rewards, fee sharing, buybacks, and token burns.

This means: 58% of fees were converted into protocol revenue, and about 19% of that revenue was captured by token holders.

This is a significant shift from the last cycle. We are seeing more and more protocols trying to make tokens behave like claims on operating performance. This gives investors a tangible incentive to hold long-term and be bullish on the projects they believe in.

I wrote about how Hyperliquid and pump.fun did this last year here: Burn Baby Burn.

The crypto world is far from perfect, and most protocols still don't distribute any earnings to token holders. But when you zoom out, you see the needle has moved considerably, a signal that times are changing.

2026 Outlook: A Return to Fundamentals

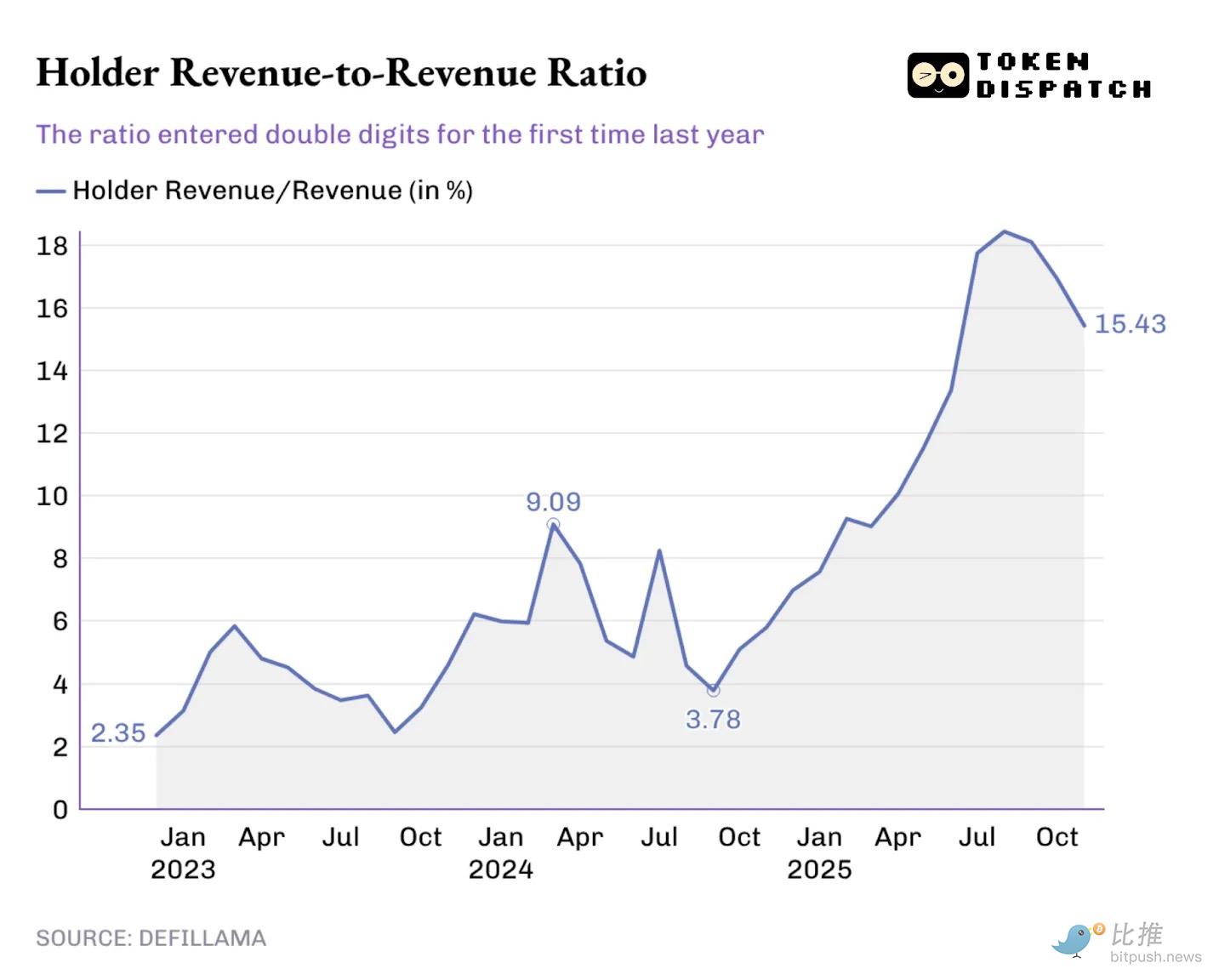

Over the past year, the proportion of holder yield to total protocol revenue has been steadily climbing. It broke the previous all-time high of 9.09% early last year and even peaked at over 18% in August 2025.

This impact is directly reflected in token trading. If I hold a token that never rewards me, my trading decisions can only be based on the media narrative surrounding it. But when I hold a token that pays me (whether through buybacks or dividends), I start to treat it as an interest-bearing asset. Even if it's not as safe and reliable, it still changes how the market prices that token. Its valuation is pulled towards "fundamentals," rather than just dancing to the tune of media narratives.

When investors look back at 2025 to try to understand where money will flow in 2026, they will heavily consider "incentive mechanisms." The teams that prioritized value transfer did indeed stand out last year.

-

Hyperliquid built a culture of giving back approximately 90% of its revenue to users through its "Hyperliquid Aid Fund".

-

Among token launch platforms, pump.fun reinforced the idea of rewarding the platform's active community. It has already offset 18.6% of the circulating supply of its native token $PUMP through daily buybacks.

In 2026, "value transfer" is expected to cease being a niche choice and become "table stakes" for any protocol that wants its token to trade on fundamentals. Last year, the market learned to separate protocol revenue from token holder value. Once token holders have seen tokens operate like ownership claims, going back to the old model would seem utterly irrational.

Conclusion

I don't think the State of DeFi 2025 revealed anything brand new about crypto industry revenue – "revenue discovery" has been a widespread focus in the industry for the past few months. The real value of this report is that it illuminates reality with data, and when we examine these numbers further, we can see the paths most likely to achieve revenue success in the crypto world.

By deeply examining the revenue concentration trends of various protocols, the report clearly points to one fact: whoever masters the "pipeline" – whether it's carry yield, trade execution, or traffic distribution – will earn the most revenue.

Looking ahead to 2026, I expect more projects to start converting protocol fees into sustainable, disciplined yield distribution mechanisms, returning value to token holders. This trend will be even more pronounced, especially against the backdrop of a global interest rate cut cycle reducing the appeal of carry trades.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush