In 1887, American railroad companies received "good news": Congress passed the Interstate Commerce Act, attempting to end the chaos of fragmented state-level regulations—varying track gauges, disjointed rate systems, and interstate transportation operations that were almost equivalent to operating between different countries. The business community cheered, but they soon realized that this was not just about order but also a restructuring of power dynamics: instead of dealing with 50 states, they now had to face a single, centralized federal regulator.

A century and a half later, Silicon Valley's AI companies are standing at the same crossroads.

Over the past few years, fragmented state-level rules have imposed high costs on entrepreneurs and given competitors like China opportunities to catch up. On March 20, the White House released the "National Artificial Intelligence Policy Framework," promising to establish nationwide unified standards—at first glance, it seems like a relief, but in essence, this is not a regulatory retreat but a consolidation of regulatory power. In other words, Washington is not taking its hands off the steering wheel but is instead reclaiming it: replacing 50 uneven hands with one larger, steadier, and harder-to-avoid hand.

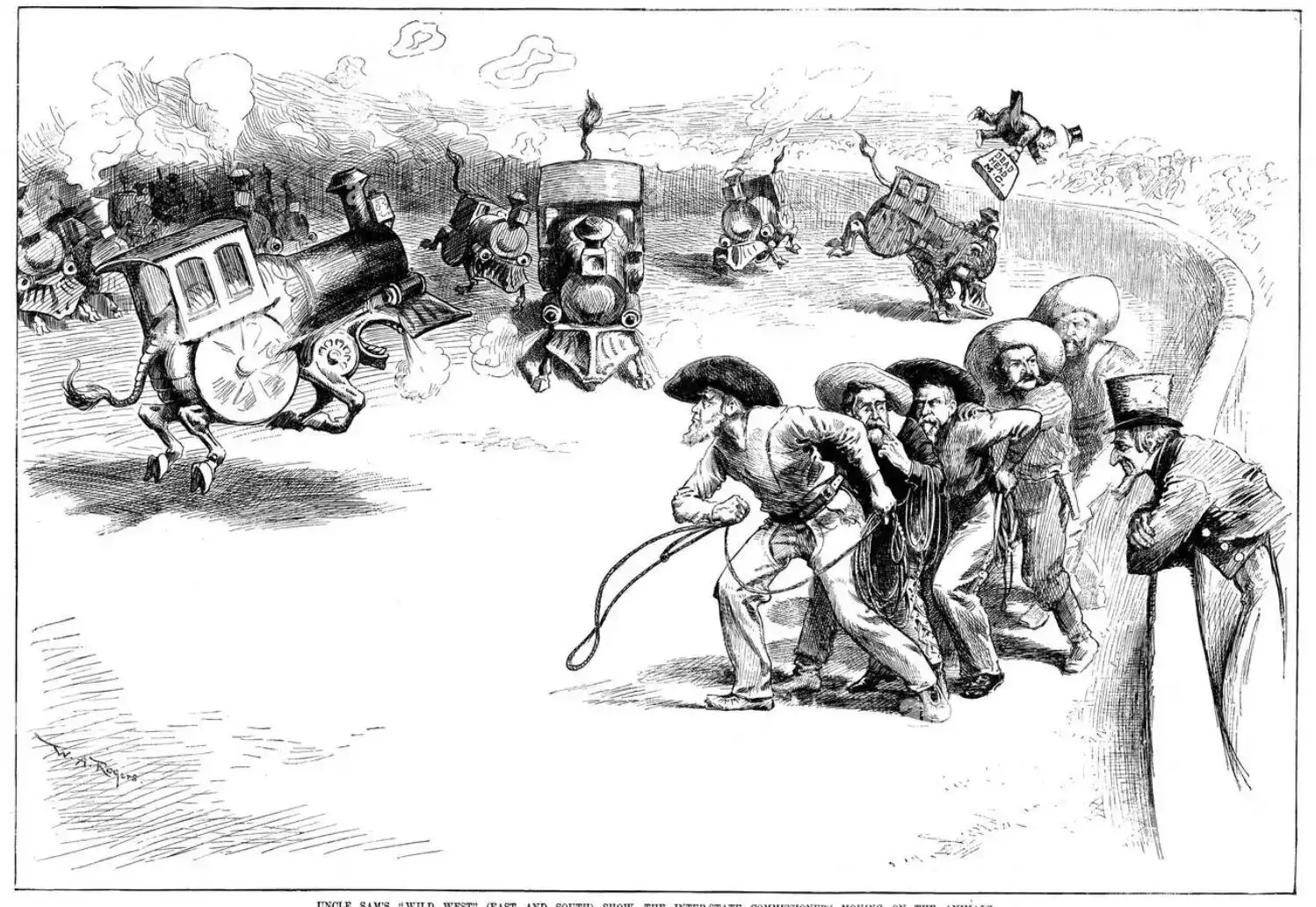

In 1887, American cartoonist W.A. Rogers depicted, in a satirical illustration, the scene of Congress passing the Interstate Commerce Act and establishing the "Interstate Commerce Commission" (ICC) to regulate the railroad industry.

I. 50 Laboratories: When Federalism Meets Economies of Scale

"States are laboratories of democracy"—this phrase has held true in the United States for over a century. Minimum wage, healthcare expansion, environmental standards—states experiment first, with local losses if they fail and nationwide replication if they succeed. Federalism functioned like a distributed innovation system, working well in traditional industries.

But AI is not like minimum wage or chimney emissions. It is not suited for "distributed trial and error."

The core characteristic of AI is increasing returns to scale: the more data, the larger the market, and the broader the iteration, the more intelligent the model becomes, with lower costs and higher barriers. In this structure, compliance is no longer just a cost but can evolve into a competitive barrier—small companies bear uncertainty, while large companies bear expenses.

Requiring a ten-person startup to navigate 50 conflicting state laws is like asking it to play chess on 50 boards simultaneously: every move could trigger compliance risks in another state. Industry giants, on the other hand, can spread audit and legal costs into their budgets, even productizing compliance processes to form entry barriers.

Thus, a counterintuitive outcome emerges: regulatory fragmentation in the AI era will not lead to a flourishing of innovation but will instead cede the market to the players best able to handle complexity—often not the most creative but the most resource-rich.

The White House framework attempts to break this logic chain. But its approach may be more worthy of caution than the problem itself.

II. The Counterintuitive Truth: This Is Not "Less Regulation" but Reclaiming the Whistle to Washington

The core of this framework is not a specific technical standard but a legal lever: Federal Preemption.

Simply put, federal law trumps state law. Congress aims to abolish state-level rules that "impose undue burdens on AI development" and establish a nationwide minimum burden standard. It appears to be a loosening of constraints: compliance manuals shrink from 50 to 1, and entrepreneurs no longer have to repeatedly navigate pitfalls at state borders. But if you zoom out, it looks more like a power reclamation: in the past, 50 states blew whistles and made judgments separately; now, it’s one entry point, one whistle, one chief referee.

The more subtle point is: today’s "light touch" can become tomorrow’s "heavy-handed channel."

The tension lies in this: a unified entry point can make the market smoother but also make control more centralized. Today, it is packaged as a "light-touch framework"; tomorrow, it could become an institutional channel for any administration to "tighten as desired"—because the switch is already installed; it just depends on who flips it.

This script is not unfamiliar in history. In the late 19th century, the railroad industry was mired in chaos under fragmented state-level regulations: rate discrimination, differential pricing for short and long hauls, and inefficient interstate transfers. Congress passed the 1887 Interstate Commerce Act under the pretext of "unifying the market and eliminating chaos," establishing the Interstate Commerce Commission (ICC) to reclaim regulatory power at the federal level. The railroad companies initially welcomed it: they no longer had to battle with individual states. Soon, however, they realized they were facing a stronger, more persistent, and harder-to-circumvent regulatory opponent.

The AI industry is standing at a similar crossroads. You can see it as a relief or as the establishment of a "unified entry point." And once the entry point is established, who guards it, how it is guarded, and how strictly are no longer up to you.

III. Six Keys: Who Benefits, Who Is Constrained?

The White House condensed this thinking into six directions. They are not like a thick legal code but more like a set of keys to the gate—each determining who enters more smoothly and who gets stuck.

Federal Uniformity and State Law Preemption

Compliance manuals shrink from 50 to 1, providing immediate benefits for interstate products. But at the same time, your fate becomes more deeply tied to Congress and the federal political cycle: national uniformity means nationwide synchronized swings. You no longer have the option to "try another state."

Child Protection

Requiring platforms to add age verification mechanisms is one of the few areas with bipartisan consensus. But it also places clear costs on consumer-facing products—especially teams working on C-end applications, education, and social platforms, whose compliance budgets will immediately thicken. Age verification is not a technical challenge but a liability challenge: if something goes wrong, who bears the responsibility?

Energy Cost Protection

Data centers cannot pass electricity costs on to residents, which sounds "public-friendly" but translates into hard constraints for infrastructure-layer companies. Electricity, site selection, peak load management, and contract structures with local utilities become more about regulatory issues than engineering ones. The subtext of this rule is: you can build data centers, but don’t let residents’ electricity bills grow thicker.

Intellectual Property

The White House tends to believe that "training AI with copyrighted content is not illegal," but it also acknowledges opposing views and leaves key rulings to the courts. Translation: gray areas persist, risks haven’t disappeared but are deferred to litigation and case law for resolution—and the timeline for case law is typically measured in "years." For entrepreneurs, this means you can continue using data to train models but must also be prepared to face lawsuits at any time. What you can do is risk management, not risk elimination.

Freedom of Speech

Prohibiting the use of AI to censor lawful political expression sets red lines for content moderation. For platforms, this is both a constraint and a protection: it becomes harder to "actively filter" and easier to use rules as a shield under political pressure. But where is the boundary of "lawful political expression"? Who defines it? This is another question left to the courts.

Workforce and Education

Expanding AI skills training attempts to turn social pressure into retraining programs. It doesn’t directly address distribution conflicts but at least acknowledges their existence and tries to shorten the shockwaves with policy. But can training keep up with the pace of displacement? Historical experience is not optimistic.

The smartest aspect of this framework is that it deliberately avoids establishing a new federal AI regulatory body: instead, it relies on existing laws, courts, and market self-regulation to operate—lightweight, fast, and with low political resistance.

But it also lacks a "dedicated safety net": once mechanisms fail, there is no specialized agency to provide unified interpretation, rapid correction, or continuous iteration. The cost of errors may manifest as lawsuits, industry chilling effects, or sudden policy reversals.

IV. Three Global Paths: The Choices of the EU, China, and the U.S.

Placing the U.S. framework in a global comparison makes it clearer: AI governance is diverging into three institutional paths.

EU: Safety First

The Artificial Intelligence Act categorizes systems by risk level, with high-risk systems requiring strict certification. The result is higher public trust, but innovation speed and entrepreneurial flexibility are often compressed, especially for teams with insufficient resources. The EU chooses to "build guardrails first, then let the vehicles run."

China: State-Led

Resources are concentrated, progress is rapid, and synergy can be formed in infrastructure, data organization, and industrial mobilization; but transparency, diversity, and debatable spaces at certain boundaries are smaller. China chooses "state direction, industry follow-up."

U.S.: Scale First

This framework bets that the combination of "unified market + court precedents + market self-regulation" will continue to attract computing power, capital, and talent. As David Sacks, Special Advisor to the White House on AI and Crypto, stated, 50 uncoordinated state regulations are eroding the U.S.’s leading position in the AI race—and leading advantages are particularly fragile in the face of economies of scale: if you slow down even a bit, you may never catch up.

There is no absolute right or wrong among the three paths, only different risk structures:

- If the EU fails, it may lose part of its industry, but societal stability is higher;

- If China fails, it may form a "silo effect" in computing power and ecosystems, but internal mobilization capacity is stronger;

- If the U.S. fails, the cost is more "nationwide synchronized"—because it actively unified the rules. Once the direction is wrong, the cost of correction will be higher.

More critically, these three paths are shaping each other. The EU’s strict standards will force U.S. companies to raise compliance levels when exporting; China’s state investments will accelerate technological iteration; the U.S.’s market scale will continue to attract global talent. The ultimate competition is not "whose rules are better" but "whose rules allow the industry to run faster, steadier, and more sustainably."

V. The Real Implications for Entrepreneurs: A Window or New Fences?

For entrepreneurs currently in the AI industry, short-term signals are likely favorable: compliance costs decrease, interstate deployment becomes more predictable, and narratives for financing become smoother—"We no longer need to prepare 50 compliance plans for 50 states" itself can make a business plan look more like a company and less like a legal exam.

But behind this favorability, three unanswered questions remain:

- Is the congressional timeline reliable?

Political agendas are always crowded. AI is hot, but legislation is slow. The implementation of federal preemption requires sufficient consensus and time windows, and windows are not always open. More troublesome, the legislative process itself may introduce new variables: amendments,附加条款, lobbying by interest groups—the final passed version may differ significantly from the White House framework.

- Can federal standards remain "light-touch" in the long term?

Today’s promises are not constitutional firewalls. The other side of centralization is stronger reversibility: a change in administration or committee members could turn a light touch into heavy pressure. And once federal preemption is established, you no longer have the option to "try another state."

- When will the gray area of intellectual property be resolved?

Court rulings may take years. During this period, "the legality of training data" remains a variable hanging over products and financing. You can continue using data to train models, but you must also be prepared to face lawsuits at any time. Investors will ask: if precedents are unfavorable, is your moat still there?

Entrepreneurs are getting a wider door, but there are still invisible beams behind it. You can run faster, but you must also be prepared to brake at any time.

VI. The Final Question: Laboratories Close, Factories Open

The era of "50 laboratories" is coming to an end. Back then, each state was a narrow door: entrepreneurs could find gaps between states, experiment, and accumulate experience, but efficiency was low, and the market was fragmented.

Now, Washington is building a "national AI factory"—higher efficiency, clearer rules, and nationwide uniformity. This is a wide door: you can enter faster, deploy across states more easily, reduce friction, expand the market, and make products truly cross-state with one click.

The door is open, but the keys and switches are all in Washington’s hands. You can walk in, but whether you pass through smoothly depends on when they turn the lock.

The real question worth asking is not "Is federal regulation good or bad?" but: When the U.S. chooses "the market is smarter than regulation," who defines the moment of market failure?

Before that moment, the window is open;

After that moment, new laboratories—perhaps only this one in the factory—remain.

And the key to that laboratory is not in your hands, nor in the hands of the 50 states—it is in Washington.

This is not just regulation. This is consolidation.