Author: Claudia

Compiled by: Jiahuan, ChainCatcher

The rules of payments in Latin America are being rewritten. 500 hours of on-the-ground investigation. Things most fintech companies haven't seen.

I spent almost a month in Latin America with broken Portuguese and worse Spanish. Over 500 hours on the ground, over 100 hours in the air, speaking with over 100 local users, developers, and more than 10 regulators.

The notes I brought back are different from what most payment professionals on this platform say. Some things even contradict my understanding before the trip.

In Brazil, the airline lost my luggage. In Mexico, a wheel broke off when the bag came down the conveyor belt. Friends kept saying that as an Asian woman traveling alone, this was brave.

But what I really want to say is: Latin Americans are the warmest people I've ever met. Strangers helped me with directions, translation, and fixing my broken luggage. In Peru, a taxi driver waited 20 minutes for me to figure out which hotel I had booked. In São Paulo, a bartender drew me a map on a napkin to direct me to a meeting I was late for.

For every story about Latin America being "dangerous," there should be a story about a stranger walking me to the right taxi. Even when the language didn't connect, the hearts did.

Here's what I learned, some of which I got wrong before this trip.

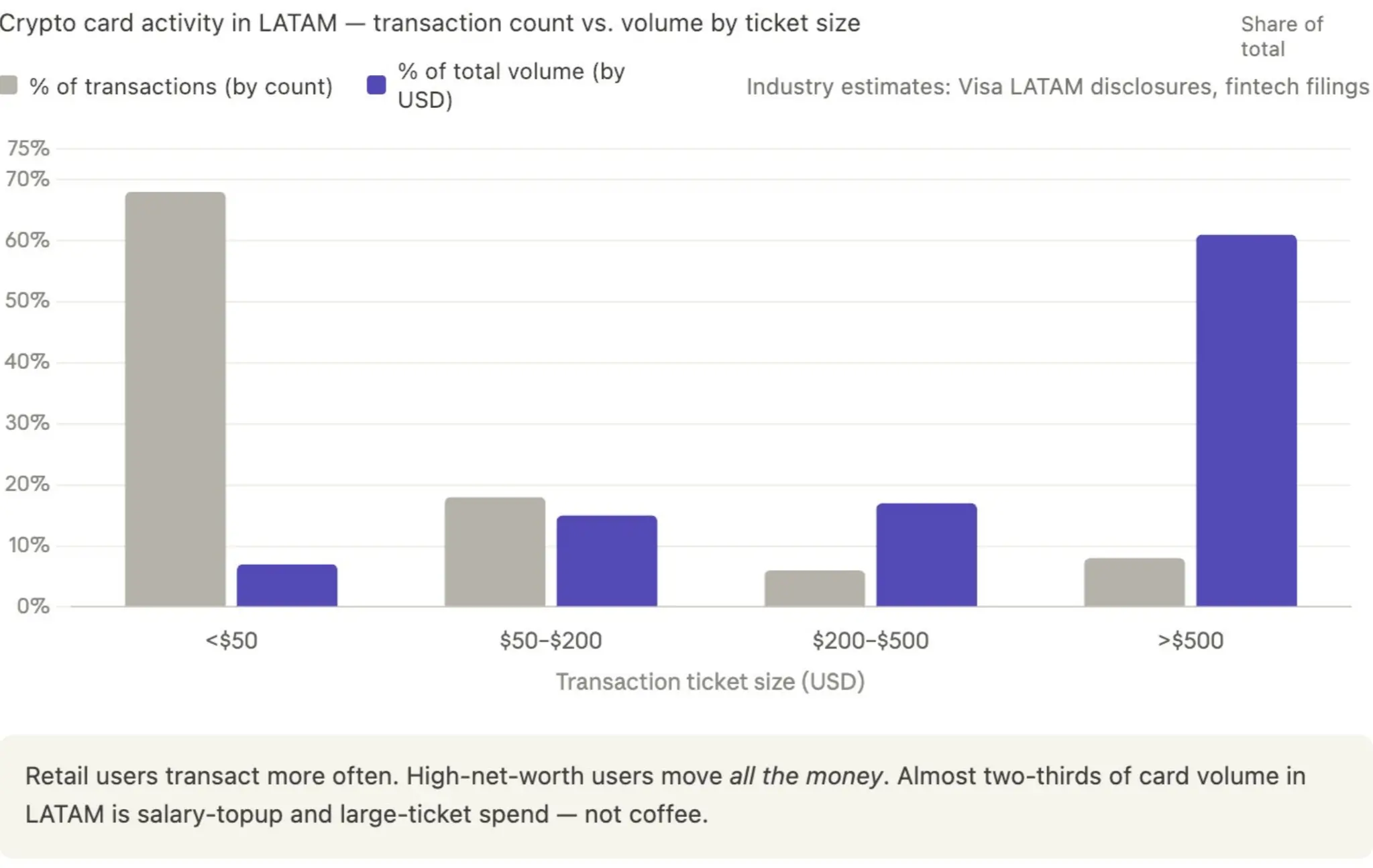

1. Do Crypto Cards Win on Cashback?

The real transaction volume of crypto cards doesn't come from retail users' high-frequency, small-amount spending, but from high-net-worth clients.

The typical pattern I saw repeatedly in Brazil is: A professional receives salary in USD or USDT (usually from a multinational employer or crypto company), loads it into a crypto card, and then withdraws to a local bank account via Pix when they need Brazilian Reais (BRL).

Whether it's Kast, RedotPay, or any other crypto card, the majority of volume comes from this group, not the person buying a $4 coffee with stablecoins.

Brazil received about $5 billion in personal inbound remittances in 2024 (Central Bank of Brazil data), with the proportion arriving in stablecoin form rising rapidly, as employers pay in USDC or USDT to avoid FX friction. Latin American crypto card transaction volume is highly concentrated in amounts over $500, which is typical for professional salary top-ups, not retail spending.

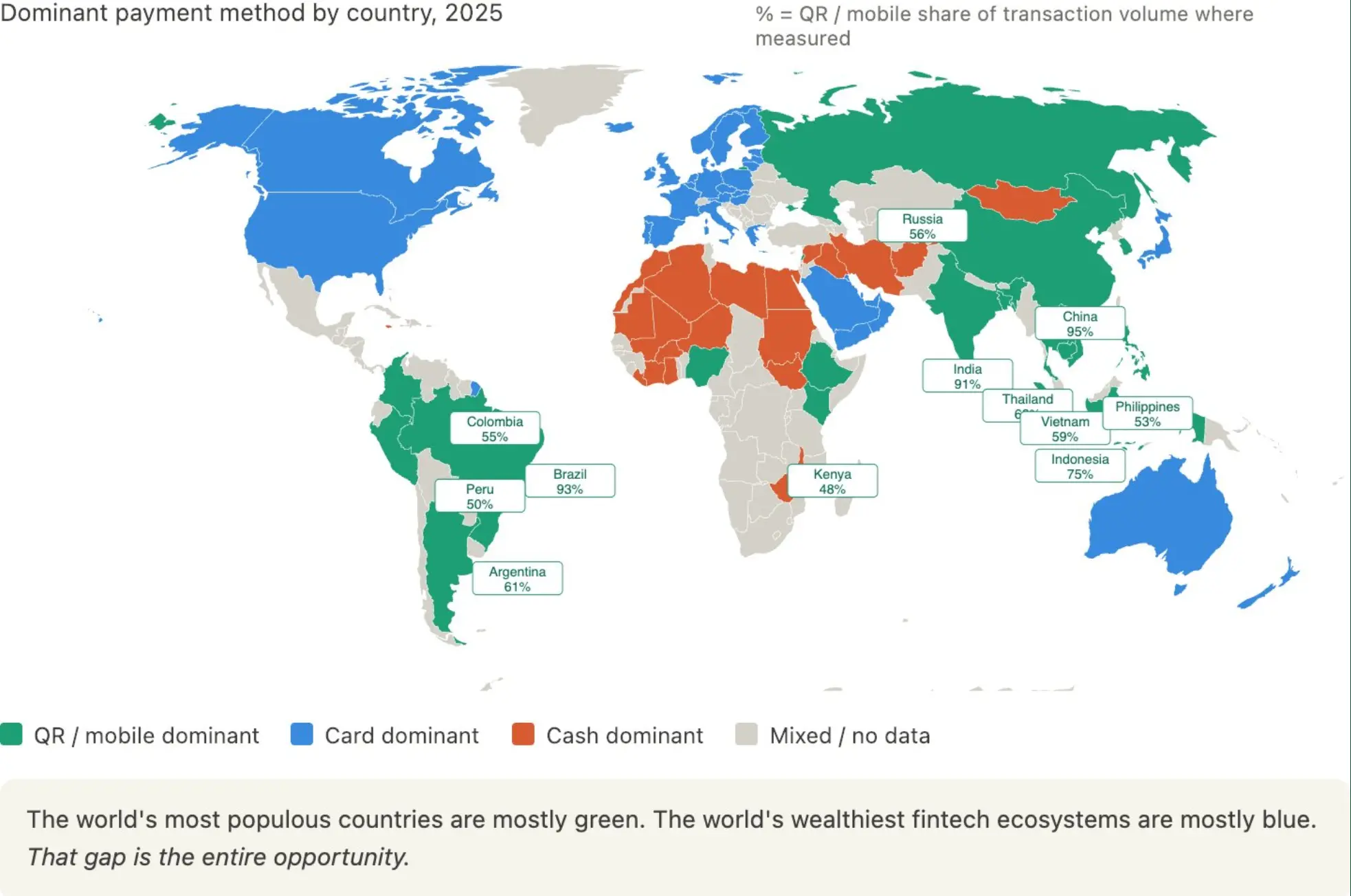

2. QR Codes Are Eating the Next Decade

Everyone is competing on issuing cards, on user acquisition. They're missing the structural shift happening underneath.

In emerging markets, QR code payments are quietly taking over the entire payment market. Brazil's Pix now processes over 6 billion transactions monthly. Argentina is covered with Mercado Pago QR codes. Peru has Yape and Plin. Mexico has CoDi. Merchants don't need POS terminals, customers don't need cards.

This isn't just a Latin American story. Look at the map of global payment dominance:

→ Brazil: 93% QR code. Pix dominates.

→ China: 95% QR code. Alipay and WeChat Pay have essentially flattened cards.

→ India: 91% QR code. UPI processes more transactions than all US card networks combined.

→ Indonesia: 75%. Thailand: 62%. Argentina: 61%. Vietnam: 59%. Colombia: 55%. Philippines: 53%. Peru: 50%.

Meanwhile, the US, Canada, Western Europe, and Australia remain card-dominated. Most of Africa and the Middle East remain cash-dominated.

One thing most Western fintech practitioners overlook: QR code payments are already the dominant payment method for the majority of the world's population. Card-dominated markets are becoming a shrinking minority, and these are precisely where venture capital, payment company HQs, and most fintech Twitter users are located.

The world's most populous countries are mostly green (QR code), the world's richest fintech ecosystems are mostly blue (cards). This gap is where all the opportunity lies.

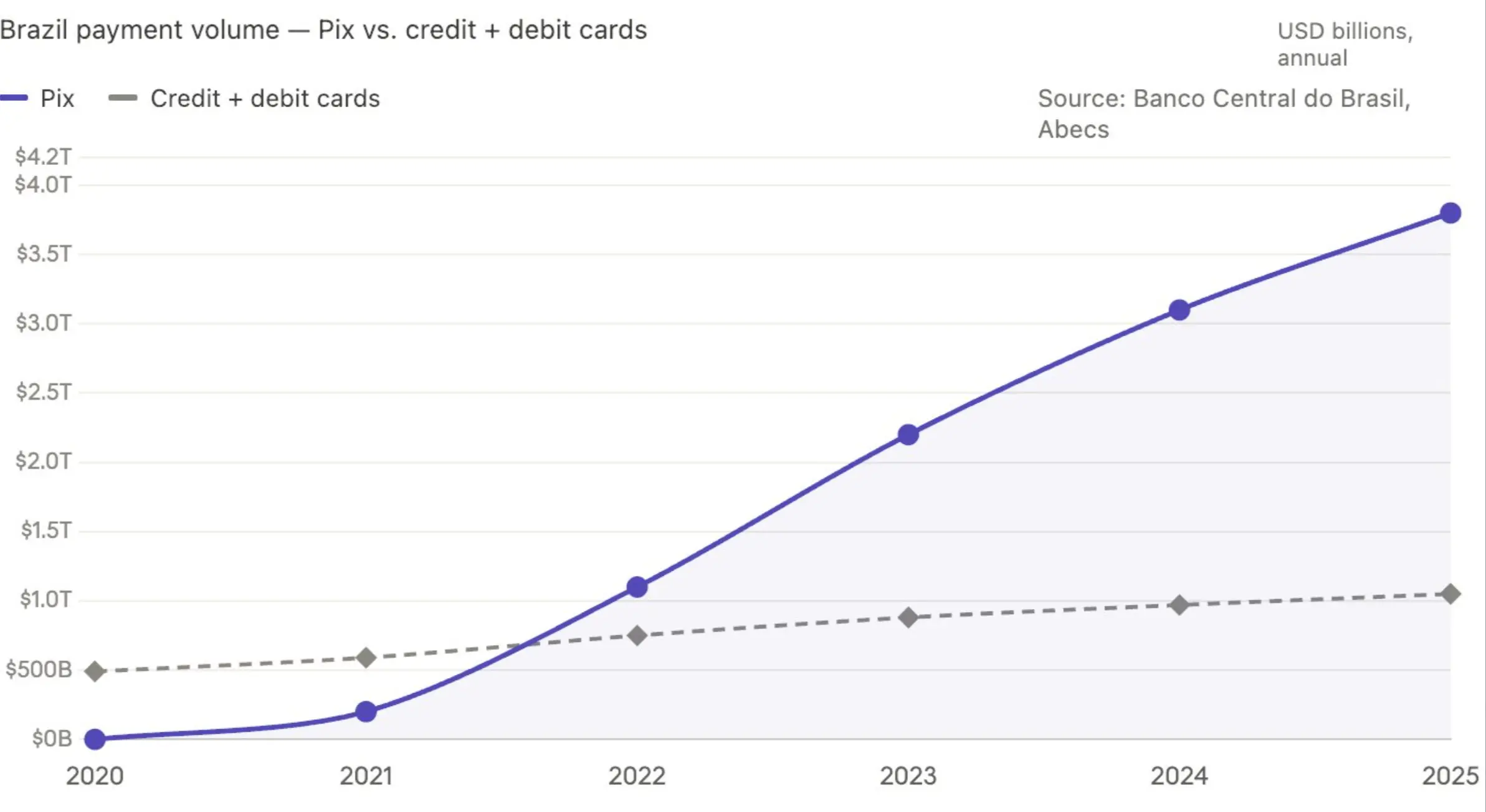

Bringing the focus back to Brazil. Pix processed over $3 trillion in transaction volume in 2024, used by about 80% of Brazilian adults. Pix transaction volume already surpassed the sum of credit and debit cards in 2023, and the gap is widening. Mexico's CoDi grew 67% year-over-year in 2024. Argentina's Transferencias 3.0 transaction volume doubled in the same year.

The logic of crypto cards assumes that the Visa and Mastercard card network rails will always be the main settlement layer in emerging markets. But the data says that's no longer the case. And this gap is widening faster than card networks can reinvent themselves.

If you're building a crypto card for emerging market users in 2026, your competitor isn't other crypto cards, but those payment rails that don't require a card at all.

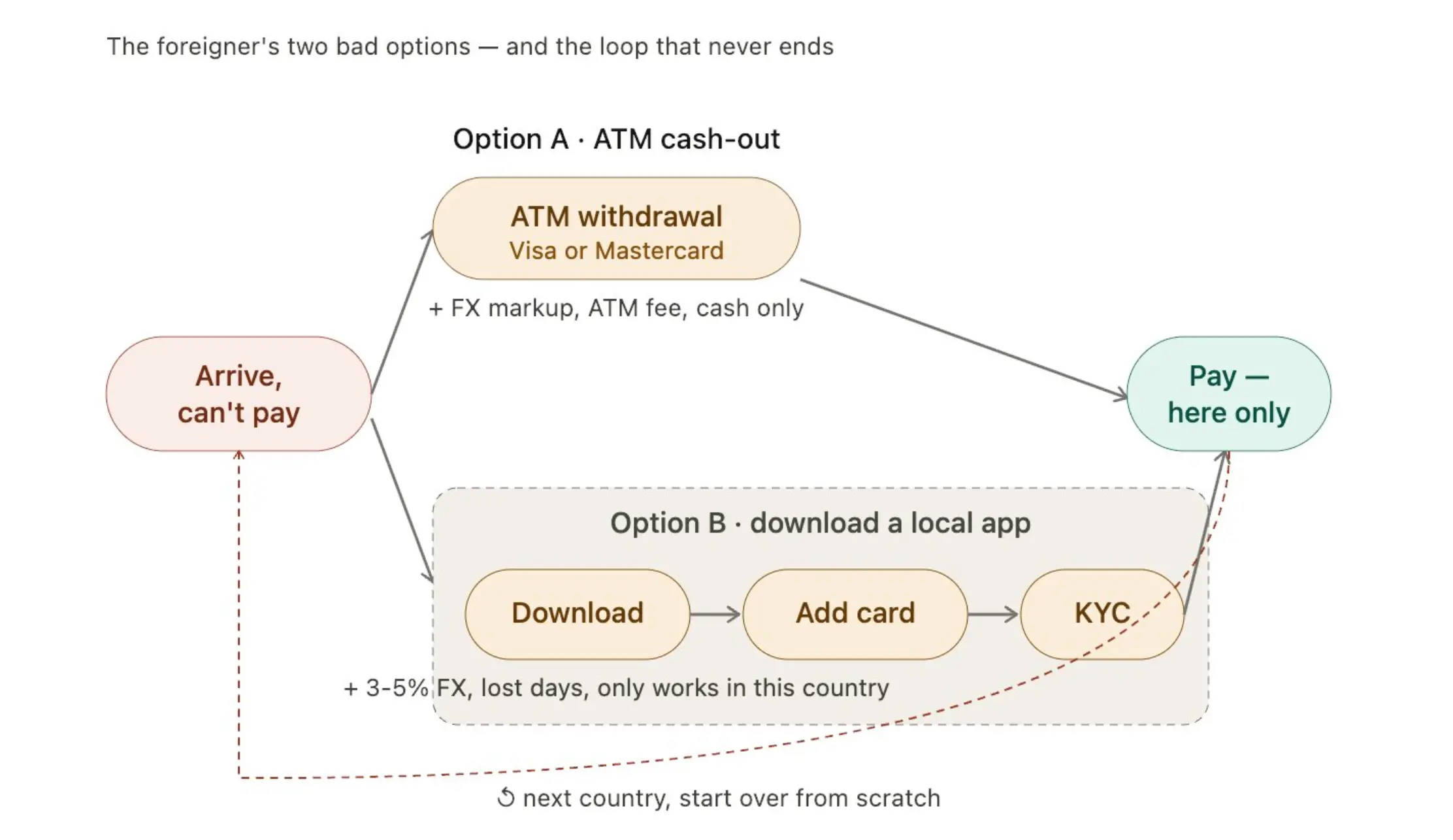

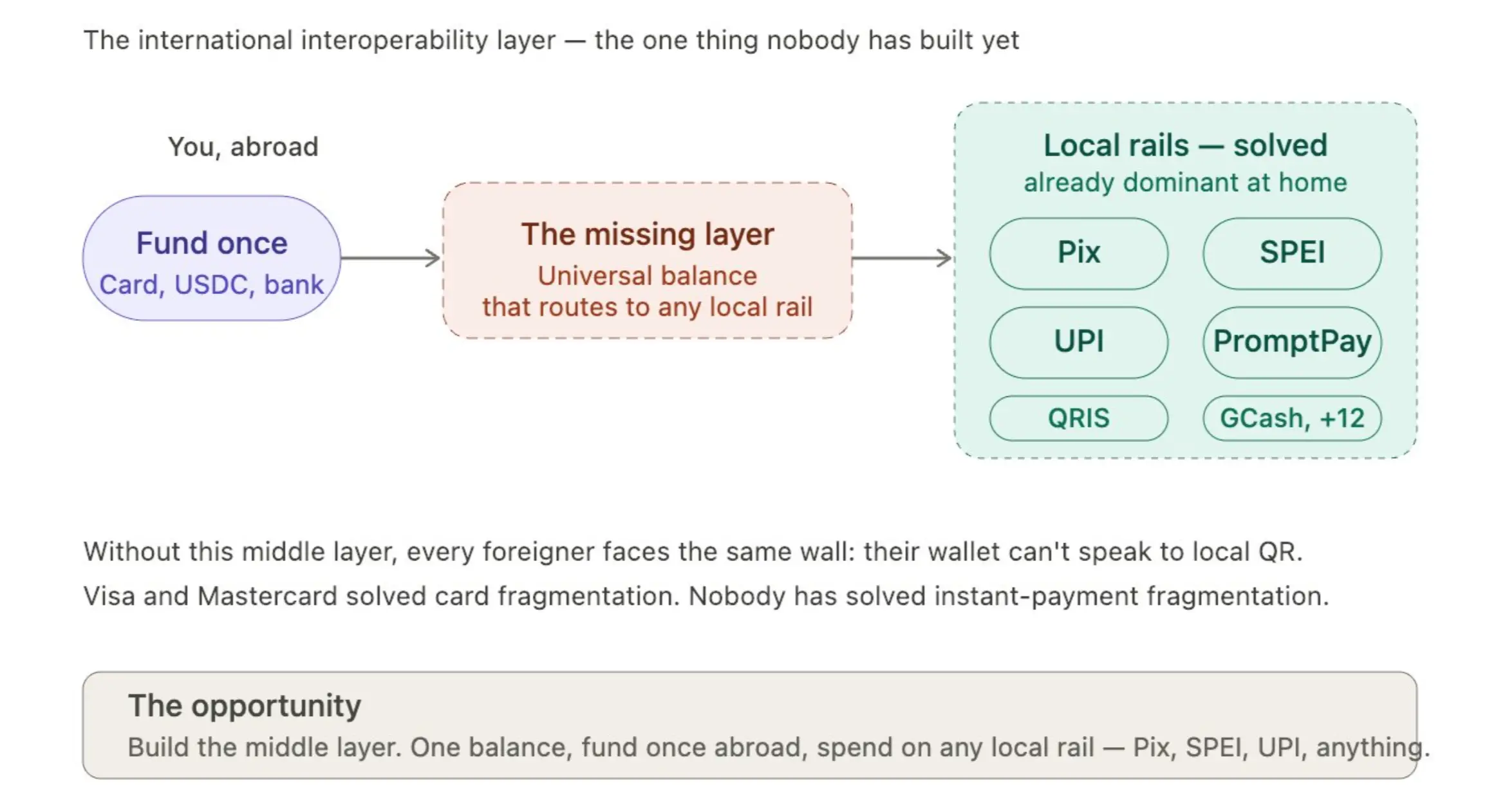

3. The Biggest Unbuilt Opportunity in Payments

Visa and Mastercard unified the fragmentation of card networks, but didn't solve the fragmentation for merchants. Not every small merchant can afford a POS terminal. The cost of acquiring just doesn't make sense for a fruit stand.

QR codes and scan-to-pay solved the "last mile" within each country. Brazil's Pix, Mexico's SPEI, Peru's Yape, each dominates domestically.

But internationally, it's still fragmented. As a foreigner, you effectively have only two choices:

Choice A: Use a Visa or Mastercard to withdraw cash from an ATM. Cost: FX markup, fees, and you can only pay with cash.

Choice B: Download a local app. Link a card, do KYC verification. Cost: 3% to 5% FX loss, takes days, and only works in that one country.

Both paths end the same: you can only pay within that country. Change countries, it all resets, start over.

One rainy night, sitting in a bar in Brazil as a foreigner wanting to order an espresso martini, my Pix didn't work. My non-Brazilian wallet couldn't talk to the bar's POS (they only accept local payments). The layer of "international interoperability" between countries' instant payment systems doesn't exist yet.

This is one of the biggest unbuilt opportunities in payments.

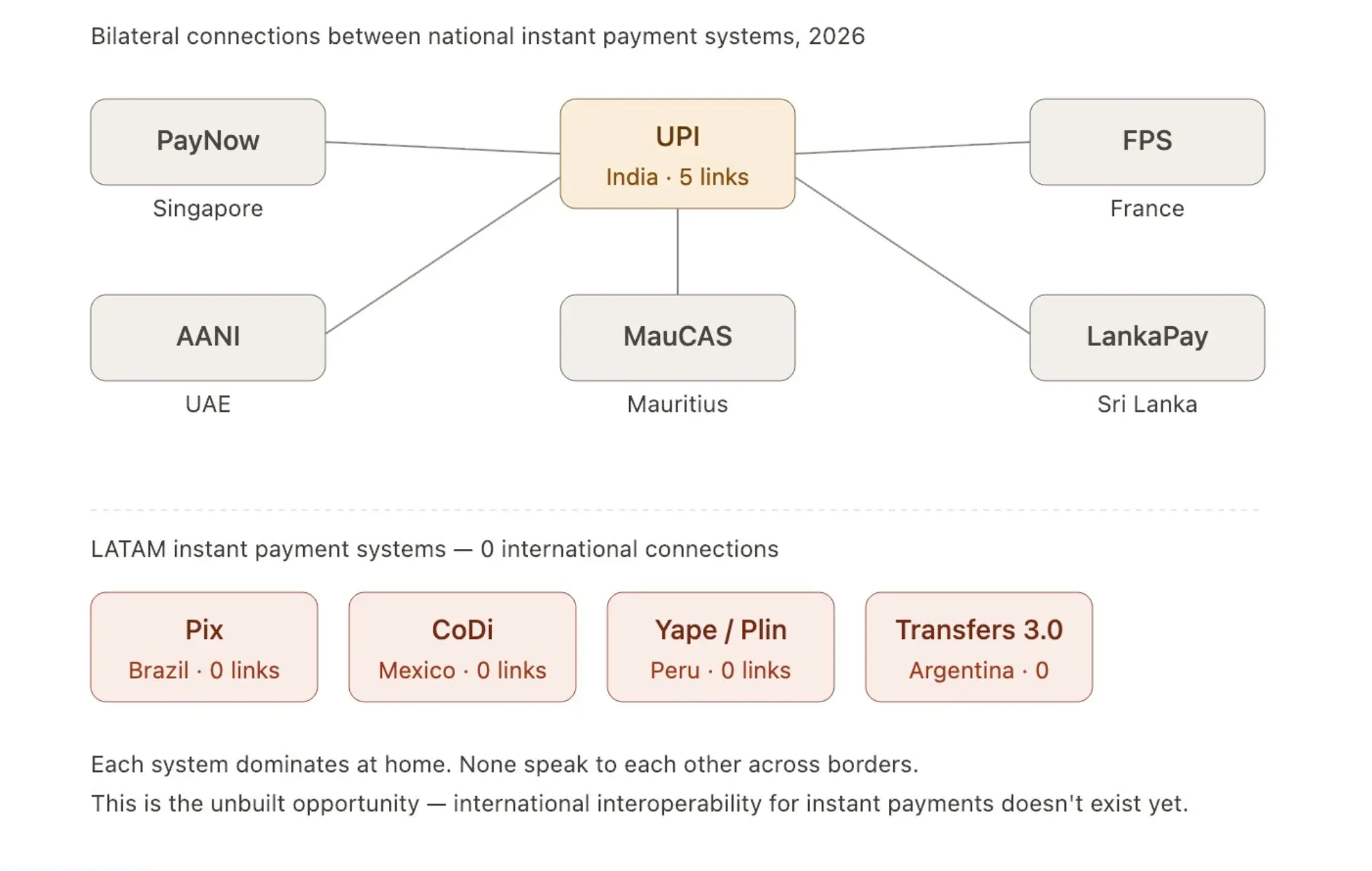

India's UPI already has bilateral connections with Singapore (PayNow), UAE (AANI), France, Sri Lanka, Mauritius. Meanwhile, Latin America's instant payment systems are almost entirely unconnected internationally. The Bank for International Settlements (BIS) Nexus project is working on this, but multilateral interoperability won't happen before 2027.

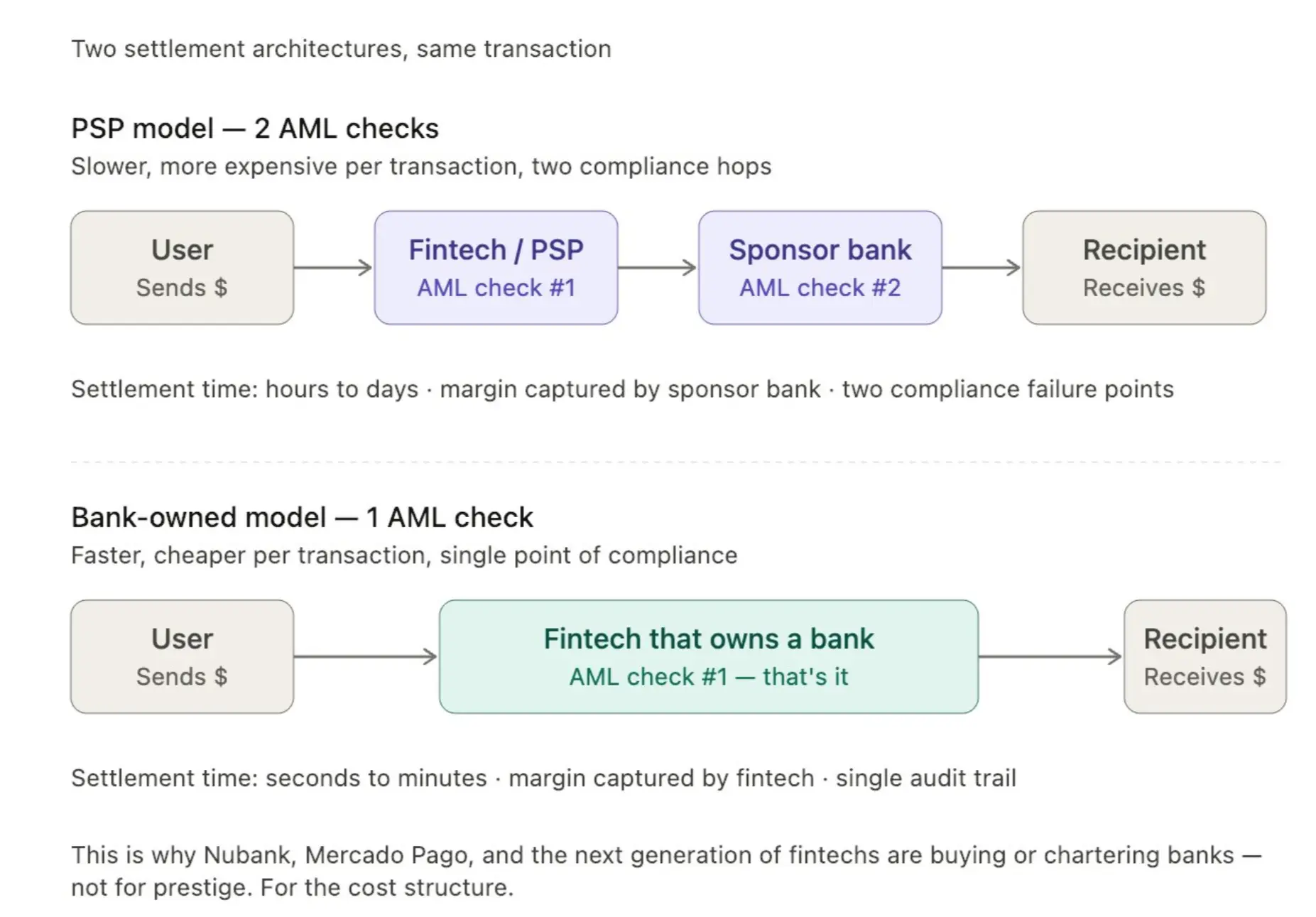

4. Payment Competition Is No Longer About Acquiring Users, It's About Owning Settlement

Most companies integrate a PSP (Payment Service Provider), letting the PSP shoulder the compliance and AML burden. At small scale, this model works.

But leading payment companies are now starting to buy banks directly. Why? Because owning a bank means doing AML checks only once per transaction, not twice. Settlement is faster, profits are earned not rented.

Hence you see Nubank's moves into banking, the wave of Brazilian fintechs acquiring small banks, and several stablecoin companies quietly applying for banking licenses.

Brazil now has over 1,400 licensed payment institutions, over 90 chartered banks. The model of "fintech with a banking license" is growing 3x faster than pure-PSP fintechs (Central Bank of Brazil 2024 data). In Mexico, just having an IFPE license is no longer enough; top players are seeking SOFOM or full banking licenses for cost reasons.

5. "Latin America" Is Not One Market

Most companies hire a Brazilian as a "Latin America BD" or community manager. This is a mistake.

Argentina is a big market, the transaction volume there is real. And because of history, culture, and football rivalry, Argentinians and Brazilians don't really get along, sometimes calling each other "monkeys" (both ways). Each country has its own currency logic, its own informal economy patterns, its own diaspora groups, its own history of capital controls.

If you can't tell the difference between Argentina's capital controls, Brazil's parallel exchange rate, and the Mexican peso's free float, you can't do Latin American payments.

Worth noting data: Argentina's population is only 46 million, yet it has over 5 million crypto users (~11% penetration, among the highest globally). Argentina's parallel FX market ("Blue Dollar") creates a structurally different demand for stablecoins than Brazil.

Mexico's remittance flow ($65 billion annually) is the world's second largest, but is being squeezed by both a US 1% remittance tax (passed Summer 2025) and tighter dollar supply from the Mexican central bank.

6. Neobanks Are Pivoting to Become FX

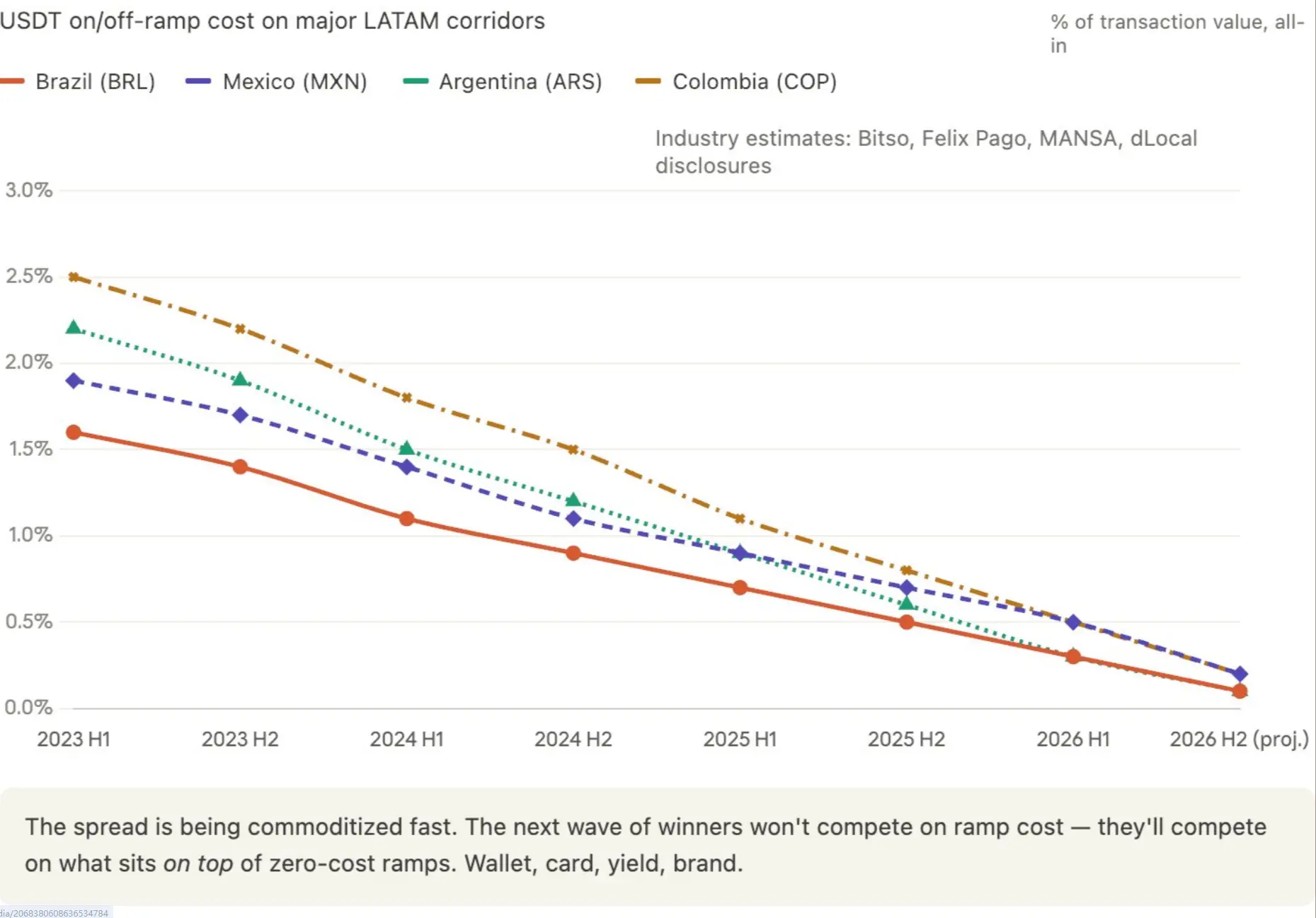

That stablecoin conference held in Mexico City this year was essentially a remittance and FX conference. Money from different countries was flowing cross-border, and that flow is being commoditized, becoming a price war.

Margins are approaching zero. My prediction: Within the next 6 to 12 months, the cost of converting between USD and USDT will drop to zero on major LatAm corridors. Companies trying to make money on spreads will find themselves squeezed by infrastructure players who treat conversion as a loss leader for bigger products.

From July 2023 to June 2024, stablecoin transaction volume in Latin America was approximately $415 billion (Chainalysis data). Currently, about 71% of LatAm institutions use stablecoins for cross-border payments (Fireblocks 2025 data).

Cross-border stablecoin transfer costs dropped from 1.5% to 2% in 2023 to 0.3% to 0.8% in 2025. Cost compression is accelerating, with Bitso, Felix Pago, and a dozen smaller players racing to drive spreads to zero.

7. Cross-Border Expansion Is the New Frontier

Classic payments advice is: Pick a remittance corridor, go deep. Build relationships, get licenses, lock in merchants, become the default.

This advice is breaking down. VCs are telling me payments have become hard to invest in because of over-localization. Every company goes deep in one country, takes local profits, but then can't get out. They become kings of one corridor but can't be invested in as a cross-regional brand.

The next generation of payment companies needs international brand recognition from day one, with tech stacks that can scale cross-border. This is a generational shift in what fintech considers "good."

Stripe's over $90 billion valuation comes from cross-corridor expansion, not single-corridor depth.

Nubank's expansion to Mexico, Colombia, and now eyeing Argentina is precisely this multi-country play that unlocked its valuation, not just its depth in Brazil.

DollarAPP recently started entering Brazil too. Most down-round financings among LatAm fintechs between 2024 and 2025 happened to companies focused on a single country.

8. Brazil and Mexico Are Red Oceans

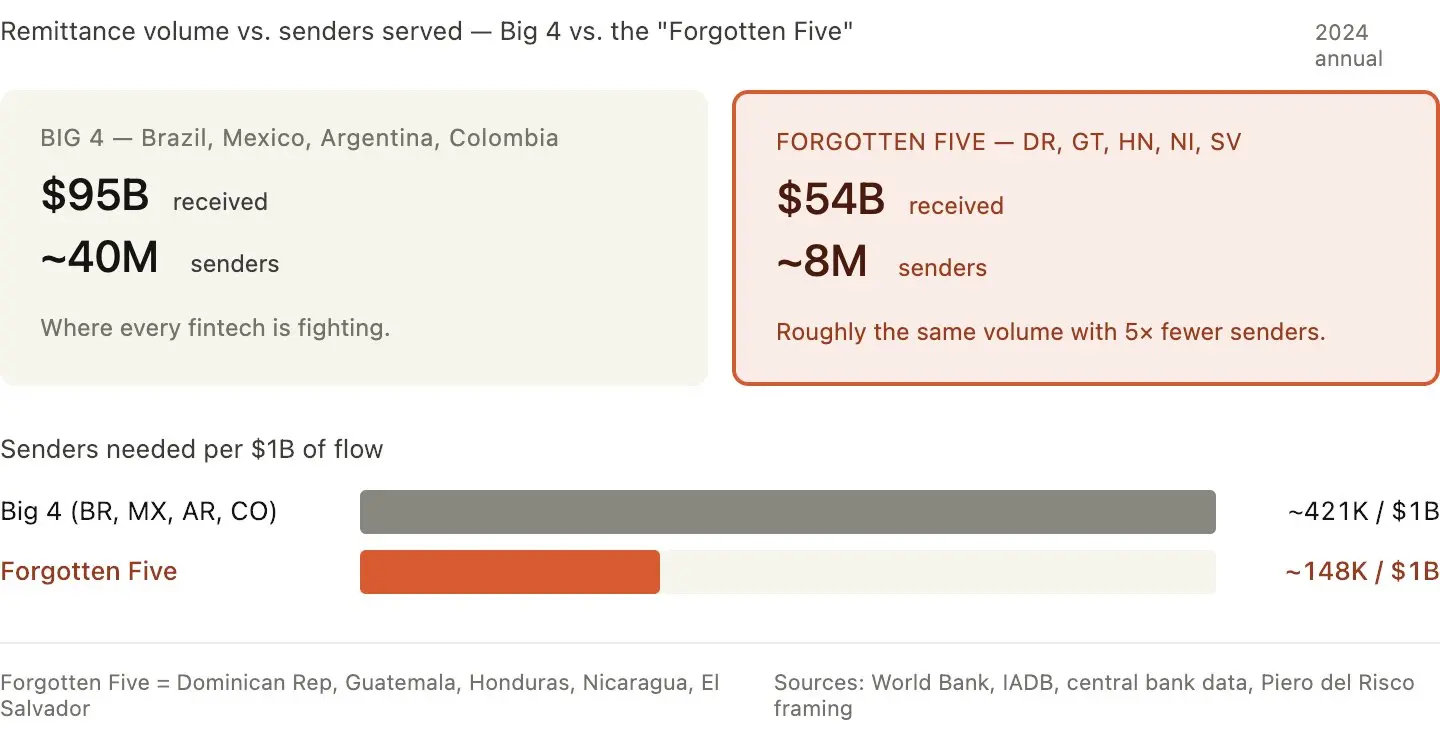

I spoke with Piero del Risco about the "Forgotten Five."

"Think about it: Dominican Republic, Guatemala, Honduras, Nicaragua, and El Salvador collectively receive about $60 billion in remittances. That's roughly equal to the total of Brazil, Mexico, Argentina, and other major markets combined. But serving these 'Forgotten Five' are only 8 million remittance senders, while serving the big markets are 40 million. We moved upstream, becoming program managers in the US, thus gaining a regulatory moat, providing banking services to senders at the top of the funnel, and owning the payment rails in each country downstream."

It's not just these five; there are a few small countries with a small but concentrated group of senders in the US receiving money equal to the entire "big" market. Everyone is fighting for Brazil and Mexico; almost no one is seriously building infrastructure for Guatemala or Honduras. With the same transaction volume, competition density here is 5x lower.

A few other overlooked corridors I'm watching:

Colombia → Europe (Spain, Italy, Netherlands)

Argentina → Bolivia (small but extremely concentrated)

Venezuela → Colombia (largest non-US LatAm corridor)

Guatemala received $20.3 billion in remittances in 2024 (15% of GDP). Other countries: Honduras $9.7b, El Salvador $8.6b, Nicaragua $4.8b, Dominican Republic $10.2b. Total $53.6 billion, about 33% of all LatAm remittances. Their combined population is less than a quarter of Brazil and Mexico's, with almost no fintech competition.

Cost per remittance for the "Forgotten Five" is also higher (6.5% to 8%, vs LatAm average of 6%), meaning more margin to capture.

9. Marketing Budgets Should Be Spent on the Right Places

Take Brazil as an example.

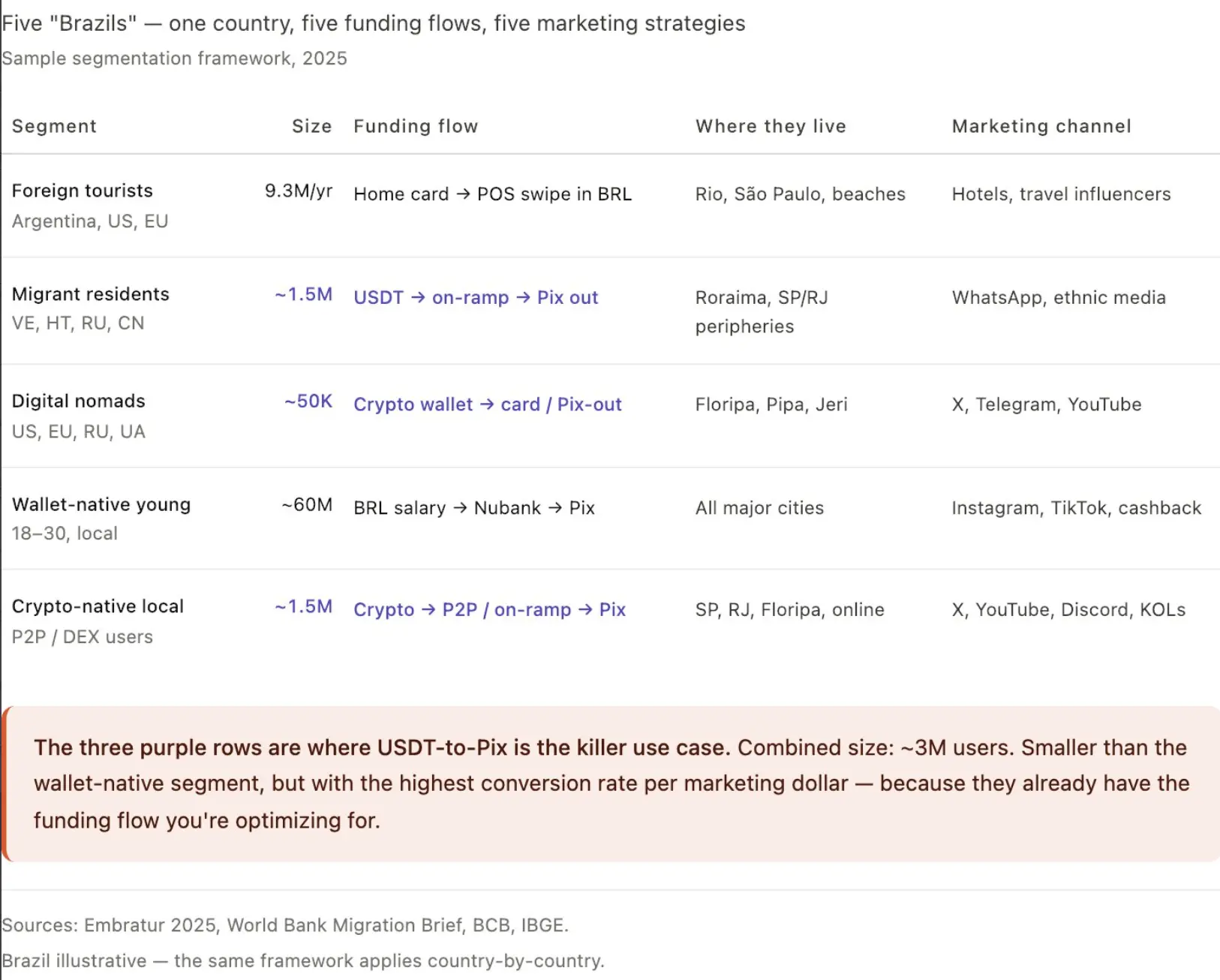

Every fintech pitching "Brazil" treats it as one user group. It's not. This country has at least five different money-flow segments, each requiring a different product, messaging, and payment rail. If you can't draw your user's money flow on a napkin, you're spending your marketing budget on the wrong people.

Here are the five segments I mapped on the ground:

Segment 1: Foreign tourists. 9.3 million people in 2025, total spend $7.9 billion (~$847 per capita).

Main sources: Argentina 3.4 million (price-sensitive, love beaches), Chile 800k (high-value), US 760k (high-spending), followed by Paraguay, Uruguay, France, Portugal, Germany.

Their money flow: home country debit/credit card → swipe on Brazilian POS. They never directly touch BRL.

Effective marketing entry: airport transfers, FX savings vs home bank, one-click payments with no fees for attractions.

Segment 2: Long-term foreign residents without Brazilian bank accounts. Venezuelans (79% of immigrant population in Brazil), Haitians, Bolivians, Russians, Chinese, Syrians, totaling ~1.5 million immigrants. 62% already use digital wallets, not traditional accounts.

Their money flow: international USDT or USD income → conversion → Pix out for BRL spending. This is the highest-value segment for native stablecoin products; USDT to Pix is their killer use case. Zero education cost, direct conversion.

Segment 3: Digital nomads. Concentrated in Florianópolis, Rio, São Paulo, Pipa, Jericoacoara. Mostly Americans, Europeans, Russians, Ukrainians. Income from abroad, often USDT or BTC. Refuse to open Brazilian bank accounts due to bureaucratic hassle.

Money flow: crypto wallet → card spend or Pix out for rent, restaurants, Uber, phone bills. They are not sensitive to FX price, but extremely sensitive to experience. They'll switch providers for one less click.

Segment 4: Brazilian young digital wallet natives. They have "accounts," but with Nubank, Mercado Pago, PicPay, RecargaPay, not Itaú or Bradesco. They don't see themselves as bank customers, but as app users.

Money flow: BRL salary → digital wallet → Pix everywhere. Crypto exposure increasing, but core flow entirely local. Marketing entry is cashback, yield, convenience, not "stablecoin rails."

Segment 5: Crypto-native Brazilians. Hold USDT or BTC, frequent P2P use. Money flow: crypto balance → P2P or conversion → Pix → spending. Brazil has over 1.5 million active crypto users. This is the easiest to convert, but also the smallest.

This is where most fintechs get it wrong: they build one product, run one marketing campaign, targeting all of "Brazil." Result: sky-high CAC because segments 1, 2, 3, 4, 5 require completely different acquisition channels, different messaging, different money rails.

Russian-language YouTube ads targeting digital nomads in Florianópolis have vastly different conversion rates than Portuguese Instagram ads targeting young Brazilians in São Paulo. WhatsApp groups for Venezuelan immigrants in Roraima perform completely differently from US travel influencer partnerships targeting tourists.

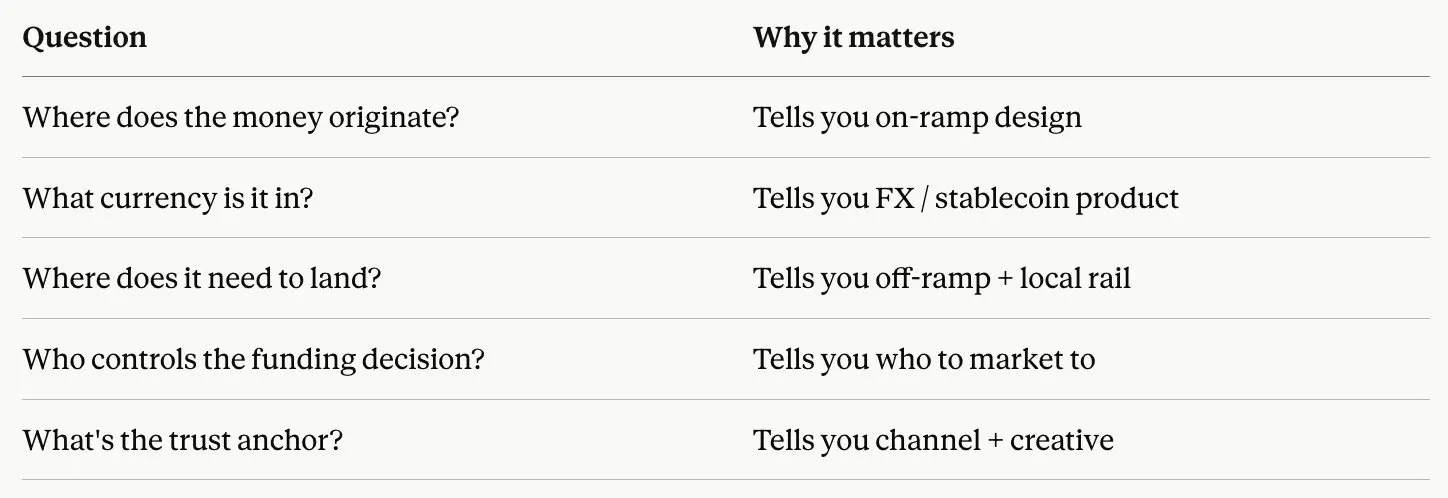

After mapping these segments, the framework I use in any Latin American country is:

If you can't answer these five questions for each priority segment, you're not ready to spend marketing budget. What you should do is more user research.

The same logic applies to every Latin American country.

This Brazil example can be mapped one-to-one to Mexico (remittance senders from the US, Mexican professionals, US-Mexico cross-border SMEs, crypto-native youth, unbanked rural population), to Argentina (Blue Dollar holders, dollarized salary professionals, crypto-native traders, MercadoPago users, tourist arbitrageurs), and every market in the region.

Don't ask "Should I do Brazil?"

Ask "Which of these five Brazils am I doing?"

That's the only question that turns Latin American expansion into a fundable venture, not a money pit.

10. On Regulation, Latin America Is 5 Years Ahead of the US

Throughout the trip, I spoke with over 10 regulators. The biggest surprise: they aren't phased at all by stablecoins, P2P rails, crypto-fiat interoperability.

The Western narrative about LatAm regulation is "fragmented, slow, behind." But on the ground, it's the opposite. The US is playing catch-up.

Brazil. The central bank built Pix in 18 months and made it free on the payment side—something the Fed is still studying. The crypto regulatory framework is now set: Resolutions 519, 520, 521 issued in November 2025, effective Feb 2, 2026. Hard deadline for existing VASPs to apply for authorization is Oct 30, 2026.

After that, every institution regulated by the Brazilian Central Bank, including every Brazilian bank, every payment processor, every Pix service provider, is prohibited from doing virtual asset business with unlicensed counterparties. Read that sentence again.

This deadline isn't "you need a license," it's "if you don't have a license, every Brazilian bank you work with is legally required to cut ties with you." As of writing, about 4 months left.

Mexico. Mexico passed the Fintech Law in 2018, while the US still has no federal fintech law in 2026. The Mexican Central Bank's IFPE plus remittance licensing framework was built specifically for cross-border digital money flows. The US just passed a 1% federal remittance tax in Summer 2025 (the Big Beautiful Act). Mexican regulators noticed this earlier than US fintech practitioners. Several told me they're adjusting licensing strategy to capture money flows that will circumvent US cash channels.

Colombia. The Financial Superintendency approved Bancolombia's COPW peso stablecoin in 2024, a fully regulated end-to-end commercial bank stablecoin. The Fed hasn't approved a single US bank stablecoin yet.

Argentina. Despite the central bank prohibiting banks from touching crypto in 2022, the new VASP licensing sandbox (launched 2025) is more flexible than New York's BitLicense. Argentine regulators told me directly: "We can't stop dollarization, we can only make it safer." This level of candor is something most US regulators wouldn't have publicly.

Costa Rica and Paraguay. Both are running stablecoin remittance sandboxes, with clearer licensing paths than over 30 US states.

The most surprising part: LatAm regulators aren't trying to slow stablecoin adoption. Several proactively asked me "how can we make it safer for our citizens?" not "how can we stop it?"

This isn't a regulatory environment "behind" the US. It's a regulatory environment ahead of the US; they've moved past the existential debate the US is still stuck in.

If you're doing cross-border in LatAm and still waiting for "regulatory clarity," you've misread the situation. Clarity has been here.

The ambiguity is actually on the US side of the corridor.

In fact, most of these points are the opposite of what I believed before the trip.

The biggest shock for me was point 6. I went to LatAm thinking stablecoins were a structurally high-margin business. The reality seen on the ground is they're already racing to zero.

The winner won't be the one with the best conversion channel, but the one that builds the next layer on top of conversion (wallet, card, yield, brand) the best.

To every taxi driver, bartender, bank manager, and regulator who took the time to explain things to a foreigner with bad Spanish and worse Portuguese.

The wheel on my suitcase will get fixed, eventually.

But what I learned on this trip won't get worn down.