Source: Tiger Research

Author: Ryan Yoon

Original Title: Is This a Crypto Winter? Post-Regulation Market Shift

Compiled and Edited by: BitpushNew

As the market enters a downward cycle, skepticism towards the crypto market is growing. The core question at hand is: Have we entered a "crypto bear market"?

Core Views

-

The evolution path of a crypto winter: Major event → Collapse of trust → Brain drain.

-

The particularity of this cycle: Past winters were triggered by internal problems; the current surge and crash are both driven by external factors. It is neither a "winter" nor a "spring".

-

Three-tier market structure post-regulation: The market has split into a compliant zone, a non-compliant zone, and shared infrastructure; the past "Trickle-down effect" has disappeared.

-

Limitations of ETF funds: Funds remain within Bitcoin and do not flow outside the compliant zone.

-

Prerequisites for the next bull market: The birth of a "killer app," coupled with a favorable macroeconomic environment.

1. How Did Past Crypto Winters Evolve?

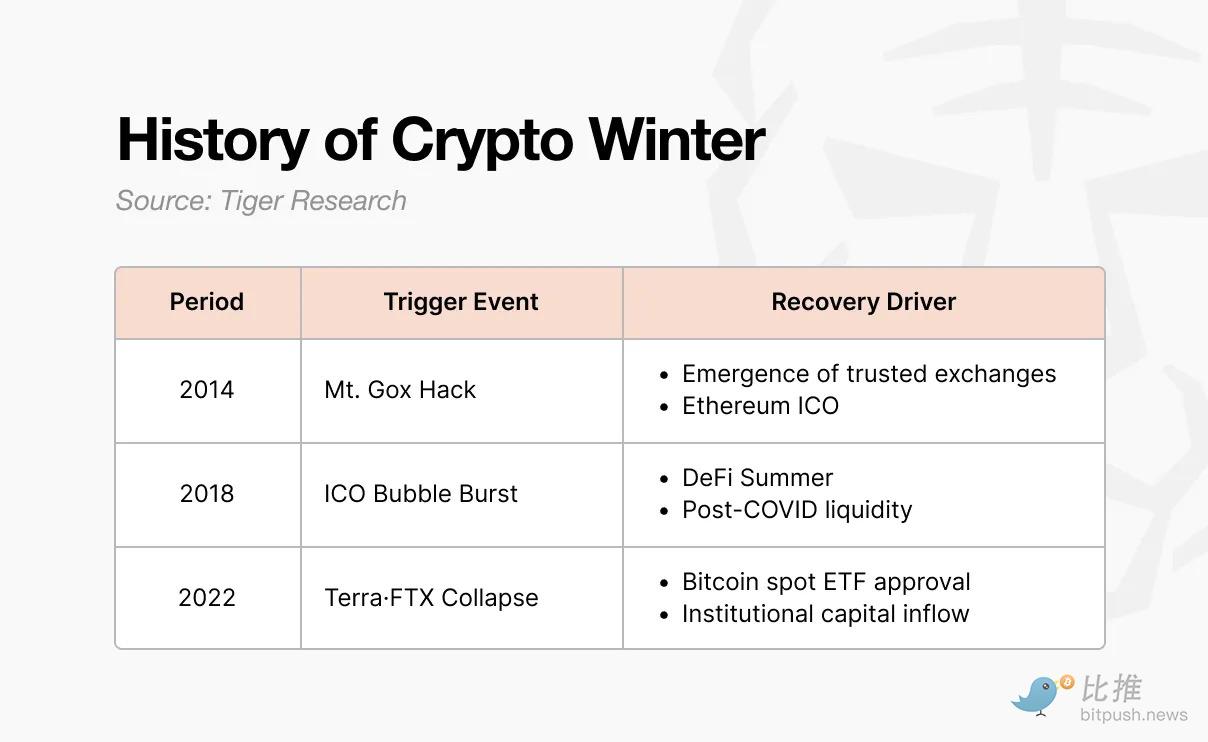

The first winter occurred in 2014. At that time, the Mt. Gox exchange handled 70% of global Bitcoin trading volume. Due to a hack, approximately 850,000 BTC vanished, leading to a complete collapse of market trust. Subsequently, various new exchanges with internal controls and audit functions emerged, and trust was slowly restored. Meanwhile, Ethereum was born through ICOs (Initial Coin Offerings), presenting a new vision and financing method for the industry.

This ICO model became the spark for the next bull market. When anyone could issue tokens and raise funds, the frenzy of 2017 was ignited. Projects raising billions with just a whitepaper were rampant, but most had no substance.

In 2018, South Korea, China, and the US successively introduced strict regulatory measures, the bubble burst, and the second winter arrived. This winter lasted until 2020. After the COVID-19 pandemic, liquidity began to pour in, and DeFi protocols like Uniswap, Compound, and Aave gained attention, leading to a return of funds.

The third winter was the most severe. The Terra-Luna collapse in 2022 triggered the successive failures of Celsius, Three Arrows Capital, and FTX. This was not just a simple price drop but a shake-up of the entire industry's structure. It wasn't until January 2024, when the U.S. Securities and Exchange Commission (SEC) approved the Bitcoin spot ETF, followed by the Bitcoin halving and Trump's pro-crypto policies, that funds began to flow in again.

2. The Pattern of Crypto Winters: Major Event → Collapse of Trust → Brain Drain

The first three winters all followed the same evolutionary logic: a major negative event triggered a collapse of the trust system, ultimately leading to a large-scale brain drain.

-

Starts with a major event: Whether it was the Mt.Gox hack, the ICO regulatory crackdown, or the Terra-Luna collapse and subsequent FTX bankruptcy, the scale and form varied, but the result was the same—the entire market was thrown into turmoil and panic.

-

Spreads to a collapse of trust: This shock quickly turned into a crisis of confidence. People who once discussed "what to build next" began to question whether crypto technology had real value. The collaborative atmosphere among builders disappeared, replaced by mutual blame.

-

Leads to brain drain: Doubts about the前景 led to an exodus of talent. The builders who had once created momentum in the blockchain space fell into pessimism. In 2014, they flowed into fintech and big tech companies; in 2018, they turned to traditional institutions and the AI field. They left here for places that seemed more certain.

3. Is This a Crypto Winter Now?

On the surface, some signs of past crypto winters are still clearly visible today:

-

Major events:

-

Trump memecoin: Its market cap once reached $27 billion in a single day, then plummeted by 90%.

-

The "10.10" liquidation event: The US announced 100% tariffs on China, triggering the largest liquidation wave in Binance's history ($19 billion).

-

Collapse of trust: Skepticism is spreading within the industry, and the focus of discussion has shifted from "building" to "blame-shifting."

极 -

Pressure of brain drain: The AI industry is growing rapidly, offering faster and more lucrative monetization paths than cryptocurrency.

However, it is difficult to define the current situation as a typical "crypto winter." Past winters erupted from within the industry—the Mt. Gox hack, ICOs going to zero, FTX blowing up—these were all cases of the industry destroying its own Great Wall.

The current situation is截然 different:

The approval of ETFs started the bull market, while tariff policies and interest rate changes drove the decline. External factors lifted the market, and external factors also dragged it down.

Builders have not left the field either:

New narratives such as RWA (Real World Assets), perpDEX (perpetual contract exchanges), prediction markets, InfoFi, and privacy protocols are emerging one after another and continue to iterate. Although they have not driven a full-market rally like DeFi did back then, they have not disappeared. The industry's fundamentals have not collapsed; only the external environment has changed.

Just as we did not personally create this "warm spring," there is currently no so-called "winter."

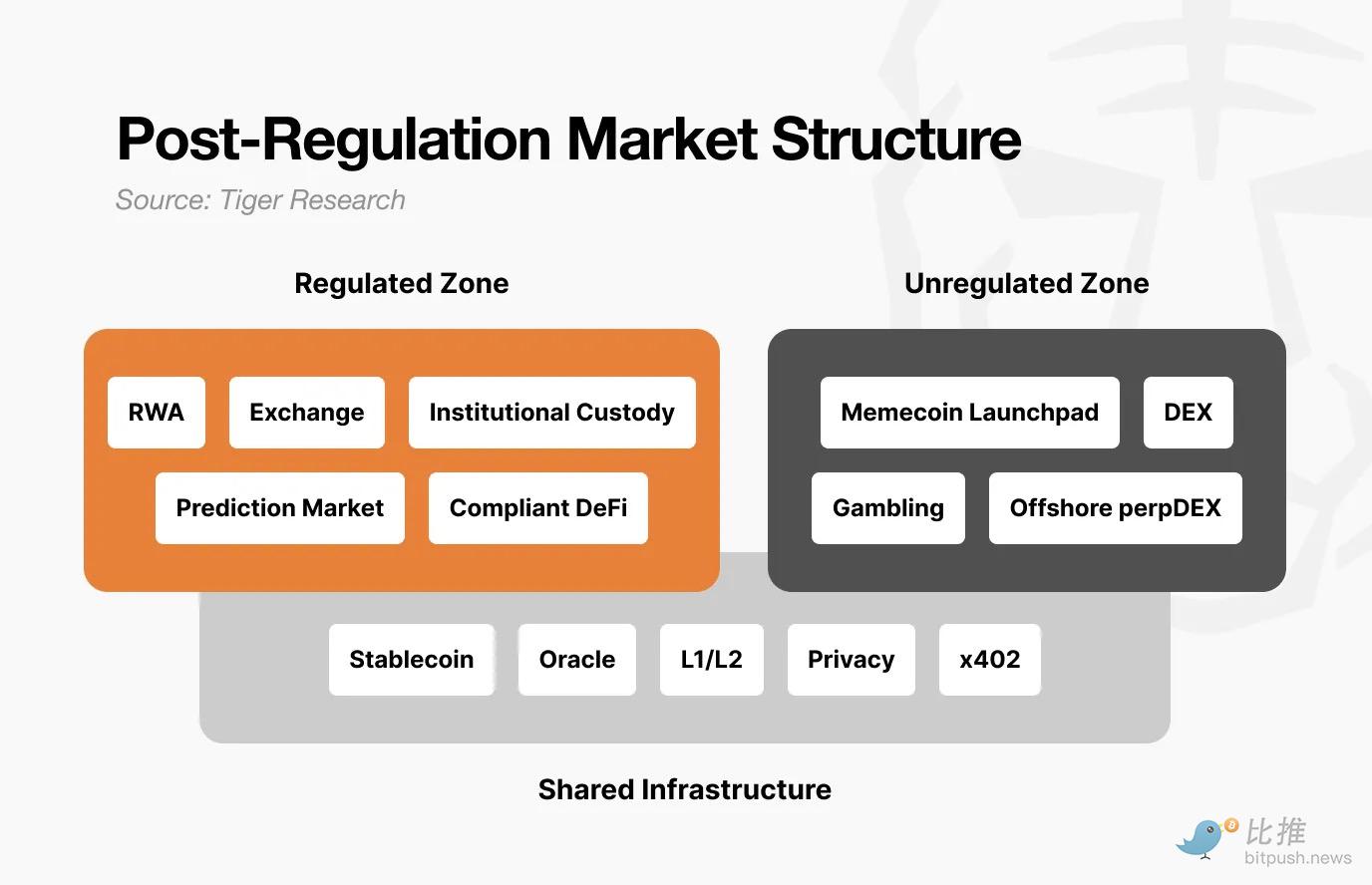

4. Fundamental Changes in Market Structure Post-Regulation

Behind this phenomenon lies the profound evolution of the market structure post-regulation. The market has now split into three levels: 1) The Compliant Zone, 2) The Non-Compliant Zone, and 3) Shared Infrastructure.

-

Compliant Zone: Includes RWA tokenization, licensed exchanges, institutional-grade custody, legal prediction markets, and compliant DeFi. These areas undergo audits, fulfill disclosure obligations, and are legally protected. Although growth is slower, the capital规模 is huge and stable.

-

Characteristics: After entering the compliant zone, it is difficult to expect the explosive 100x returns of the past. Volatility decreases, the上限 is limited, but the下限 is also guaranteed.

-

Non-Compliant Zone: This area will have an even stronger speculative色彩 in the future. Low barriers to entry, fast pace, surging 100x today and dropping 90% tomorrow will become the norm.

-

Significance: This space is not meaningless. The non-compliant zone is a cradle of creativity. Once a track is proven effective, it will migrate to the compliant zone (like DeFi back then and prediction markets now). It serves as an "experimental field," but itself will increasingly剥离 from compliant businesses.

-

Shared Infrastructure: Includes stablecoins and oracles. They serve both zones simultaneously. The same USDC can be used for institutional-grade RWA payments and for speculative trading on Pump.fun; oracles provide data verification for tokenized treasuries and support liquidations for anonymous DEXs.

This differentiation has changed the flow path of funds.

In the past, Bitcoin's rise would带动山寨币齐涨 through the "Trickle-down effect." Now it's different: institutional funds entering through ETFs stop dead within Bitcoin; funds in the compliant zone no longer flow to the non-compliant zone. Liquidity only stays where value is proven. Even Bitcoin itself, its属性 as a safe-haven asset has not yet been fully proven against risk assets.

5. Conditions for the Next Bull Market

The regulatory framework is being完善, and builders are still working hard. Two more conditions need to be met:

-

A new "killer app" is born in the non-compliant zone: Something must emerge that can create全新 value, like the "DeFi Summer" of 2020. AI agents, InfoFi, and on-chain social are potential candidates, but they have not yet reached a scale that触动全局. The良性流动 of "non-compliant zone experiment → successful verification → migration to the compliant zone" must be formed again.

-

Cooperation from the macroeconomic environment: Even if regulation is settled, builders are working hard, and infrastructure is perfect, if the macro environment is not supportive, the upside space is still limited. The 2020 DeFi boom erupted after the pandemic amid global massive liquidity injection; the post-ETF rise in 2024 also coincided with expectations of interest rate cuts. No matter how well the crypto industry does itself, it cannot control interest rates and liquidity. For the value built within the industry to gain widespread recognition, the macro environment must reverse.

A crypto season with "universal上涨" like in the past is unlikely to reappear. Because the market has彻底分裂. The compliant zone will grow steadily, while the non-compliant zone will continue to fluctuate剧烈.

The next bull market will eventually come, but it will not favor everyone.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush