Editor's Note: The article points out that the current global oil supply is only about 20% short, but what is truly escalating the crisis is not the "physical shortage," but rather a triple behavioral chain reaction triggered by scarcity: hoarding, speculation, and the capital logic of "waiting for competitors to collapse to buy assets at bargain prices."

From a 20% supply gap, to disruptions in transport through the Strait of Hormuz, to the short-term "filling" by strategic reserves, alternative pipelines, and production capacity mismatches, the system appears to be functioning on the surface; but at a deeper level, the behaviors of hoarding, speculation, and "waiting for collapse" are amplifying the gap itself, turning a manageable supply-demand issue into a potential systemic risk.

The article further notes that the triggering of such risks does not follow the intuition of "gradual deterioration," but is more akin to a bank run—before confidence shatters, everything seems stable; but once key variables are confirmed (reserves depleting, the gap widening, transport unable to resume), the market will reprice itself in a very short time. The 1973 oil crisis, the 2008 financial crisis, and the 2022 energy shock all followed this highly consistent path.

Within this framework, the current "calm" of the market itself becomes the most alarming signal: the real economy is already showing production cuts, travel restrictions, and supply contractions, but asset prices continue to reflect risk appetite. This divergence is, in essence, the last consensus that "the system is still effective."

The core judgment of this article is: The problem is not whether oil is already insufficient, but that once enough people begin to believe it might be insufficient, the system will prematurely enter contraction and revaluation. Strategic reserves can only buy time, not provide an answer; and this window is closing rapidly.

Mid-to-late April will become a critical juncture. At that point, the market will need to face not "whether it will happen," but "when it will be confirmed."

Below is the original text:

The world is short roughly 20% of its oil. Theoretically, if everyone tightens their belts a little, the economy could keep running.

But "shortage" in reality never works like that. When a critical resource develops a gap, people don't ration rationally; they start hoarding and speculating. And those who have surplus? They wait for you to collapse, then buy your best assets for pennies on the dollar.

These three behaviors can amplify a manageable gap into a civilization-level problem.

Hoarding, Speculation, and Vulture-Like Waiting

First comes hoarding. Once "shortage" hits the headlines, everyone starts panic buying—not because they need it, but because they are afraid. They aren't buying oil; they are buying "security." And this panic itself is enough to double the actual shortage.

Next is speculation. Once oil becomes scarce, traders swarm in, and prices rapidly detach from fundamentals. This isn't theory; it's the iron law of commodity markets. Nearly every energy crisis in history has unfolded along this path.

The final layer, and the cruelest: waiting for you to fall.

Why Those With Oil Won't Sell

Omani spot crude is already trading at $150 to $200 per barrel. But oil-starved countries still might not be able to buy it, because players holding US dollars have already locked up supply.

Some countries, despite having ample reserves, still refuse to sell to their neighbors.

Why? Because they see a larger game: waiting for debt crises to erupt, waiting for social unrest, then acquiring the world's best assets at fire-sale prices. A company worth $50 billion in normal times might be snapped up for $5 billion when a country is on the brink of collapse—no army required.

Berkshire Hathaway currently holds nearly $375 billion in cash, a historical record. This accumulation began long before this war, with 12 consecutive quarters of net asset sales. But the key isn't the accumulation; it's the timing of the deployment.

What is Buffett waiting for?

This Playbook Is 3,000 Years Old

In Genesis Chapter 47, Joseph helps Pharaoh store up grain during seven years of abundance. Then come seven years of famine. The Egyptians first buy grain with money; when the money is gone, they trade livestock; when the livestock are exhausted, they surrender their land.

By the time the famine ends, Pharaoh owns almost all of Egypt.

No war, no violence. Just control of a scarce resource, and enough patience.

The logic of blocking the Strait of Hormuz is the same. Conquering a country by force requires hundreds of thousands of troops; blockading a strait and waiting patiently? Just a navy and time.

Joseph, at least, was trying to save the people. The participants operating around this crisis are not.

This is precisely why a 20% oil shortage is enough to bring down the whole world. The problem isn't "not enough oil," it's that—some are hoarding, some are speculating, and some are waiting for you to fall.

Collapse Never Happens Gradually

Most people think economic crises unfold step by step. But reality is the opposite. Lehman Brothers was operating normally the day before it filed for bankruptcy; Silicon Valley Bank showed no obvious signs of abnormality 48 hours before its collapse.

Systemic collapse is more like a "bank run." When everyone trusts the bank, it operates nearly perfectly; once a crack in trust appears, everyone withdraws their funds at the same time. The bank doesn't die slowly; it collapses instantly within 48 hours.

The current global energy market is in the same state.

Everyone is betting Trump will solve the problem quickly, everyone still "believes the system holds." But once this trust is broken—for example, reserves start to bottom out, or the International Energy Agency confirms the gap is widening—selling will erupt like a bank run.

Not gradual. Instantaneous.

Five Weeks Have Passed

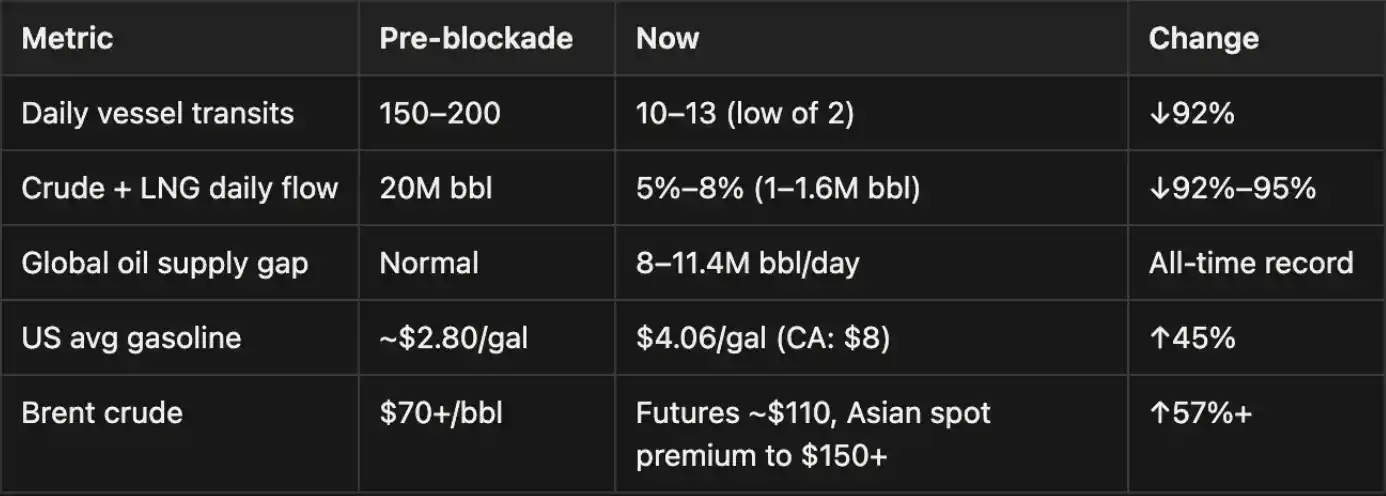

Note: The Strait of Hormuz typically carries about 20 million barrels per day (bpd) of oil transport. Therefore, the current loss of approximately 18–19 million bpd capacity due to the blockade already exceeds the global supply gap of 8–11.4 million bpd. This shortfall is being partially offset by: the release of strategic petroleum reserves (SPR), alternative pipelines (e.g., Saudi East-West Pipeline, UAE bypass routes), and supplies from non-Hormuz oil producers. But this filling is temporary.

The scale of this shock has surpassed the 2022 Russia-Ukraine energy crisis and has even been called "the most severe energy crisis in human history."

Our judgment is: This statement is likely not an exaggeration.

Strategic Reserves: Buffer Time ≠ Safety

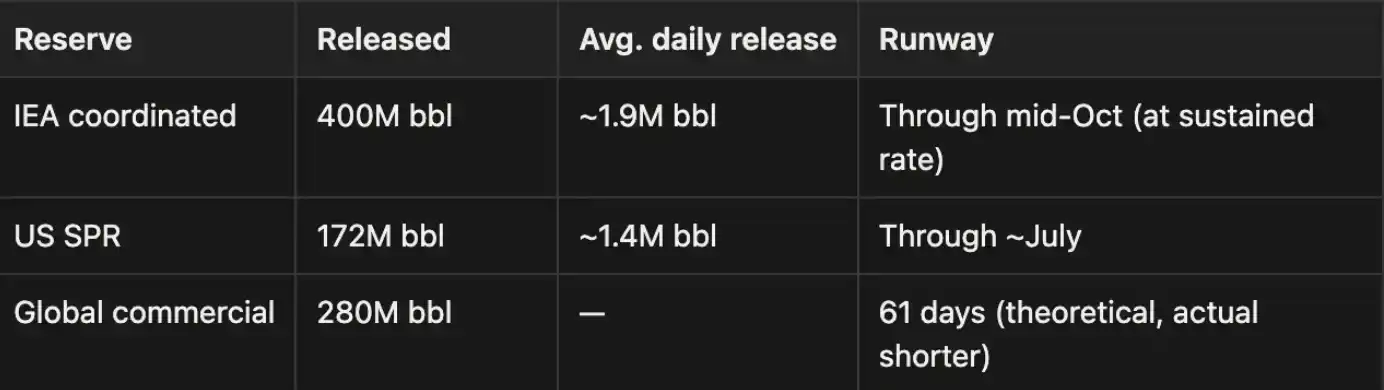

Currently, the market is propped up by only two things: the continuous release of strategic petroleum reserves, and market expectations stemming from Trump's policy statements.

These numbers themselves are also problematic: The release of Strategic Petroleum Reserves (SPR) has a physical upper limit, historically around 2 million bpd. This means the actual capacity to fill the gap is far lower than the headline numbers suggest.

OPEC+ nominally has 2.5 to 3.5 million bpd of spare capacity, but these export routes themselves pass through the Strait of Hormuz; this capacity is effectively trapped.

Reserve data published by some countries also includes delayed deliveries and inventories that are still overestimated. Once the buffer period ends, the supply gap will widen rapidly. Reserves can only buy time, not solutions. The market has a window, but this window is closing.

The Market Is Sleepwalking

The current market state is surreal: Israel just suffered its fiercest missile attack since the war began, yet the stock market barely reacted. Chemical plants in Japan, South Korea, Singapore, Thailand, and elsewhere are reducing production or even shutting down, yet the market hasn't priced this in. Australia is shifting to remote work due to fuel shortages, South Korea is implementing nationwide travel restrictions, yet stock markets are still rising.

Trump says Iran is negotiating every day, Iran denies it every day, yet stocks continue to rebound. Semiconductors are still soaring, AI concepts are still hot, quantitative and algorithmic trading are still amplifying this optimism. But just look closely, and you'll see many things are already turning red; everyone is just pretending not to see it.

This divergence between market performance and the real economy won't last long. It never has in history.

The Cards Iran Holds

Many are betting Trump will solve the problem quickly. But first, look at Iran's current position.

The Islamic Revolutionary Guard Corps (IRGC) has been very clear: "The Strait of Hormuz will not reopen because of Trump's ridiculous performance. We are not conducting any negotiations, nor will we in the future."

There is also the practical issue of communication itself. Iranian senior officials currently will not handle any operational matters via phone or encrypted apps—Israel assassinated Haniyeh in Tehran and also detonated Hezbollah's pagers; this paranoia is not without reason. Thus, real communication between Tehran and Washington can only go back and forth through intermediaries like Oman, Iraq, Switzerland, each round taking days.

Iran's Calculus

Iran doesn't need to win; it just needs to outlast. The Strait blockade is its biggest card; it has found America's soft spot. Russia supports it, China provides it with "humanitarian aid," it won't starve.

Strait transit fee revenue alone could bring in tens of billions annually. If the US backs down or gets bogged down in a long war of attrition, Iran can maintain control of the Strait. Wealth that originally flowed to the Gulf monarchies would be diverted to Tehran.

Trump's Dilemma

Don't fight: The petrodollar system begins to erode.

Fight: Oil prices spike further. If the war drags on, Gulf crude cannot be exported, and the funding pipeline supporting the US stock market will also dry up.

The real risk is: The US dollar could depreciate sharply. If the petrodollar loses its anchor, all dollar-denominated assets will be repriced. And the most frightening thing is, no one inside the White House seems to have a clean, clear answer to this problem.

What to Watch Next

US SPR Weekly Report. The rate of reserve drawdown is the most direct signal. Brent crude spot prices and the futures curve. A deep contango implies the market is pricing in long-term shortage. Trump's rhetoric. The tougher the talk, often the worse the situation.

Asian factory utilization rates. Declines in chemical, auto, and semiconductor production will be the leading indicators. Fertilizer prices. Compared to oil prices distorted by verbal intervention, fertilizer prices are often more honest. IEA Monthly Report. If the mid-April update confirms the buffer is exhausted, market confidence could shatter overnight.

Timeline

According to Dallas Fed data, if the Strait of Hormuz remains closed for the entire second quarter, US annualized GDP would contract by 2.9%. Multiple institutions are also continuously raising recession probabilities. The probabilities below are conditional: they apply if the blockade persists into each phase. If the Strait reopens early, subsequent phases no longer apply.

Now → April 15: Reserves Still Being Released

Strategic reserves are still being deployed, Trump is still making statements. Impact on GDP remains limited for now. But if the April 6 "ultimatum" yields no results, the supply gap will widen rapidly. Probability of global economic disorder: 20%–30%

Late April → Early May: Reserves Bottom Out

National strategic reserves begin to hit bottom, IEA confirms the gap has doubled. Real economic impacts begin to集中显现 (concentrated显现 - manifest集中): fertilizer shortages, delayed spring planting, chemical plant shutdowns, LNG紧张 (tension/shortages), European industrial production cuts. Probability: 45%–65%. This is the critical inflection point.

Mid-May → End of June: Real Economy Deteriorates

Oil prices break $150 to $200 per barrel. High oil prices begin to suppress all economic activity. Countries scramble for Russian and Indian supplies, with limited success. Europe and Asia enter recession first. Probability: 65%–80%

After June: Systemic Collapse

No new alternative supply routes emerge. Stagflation, unemployment, and central bank failure occur simultaneously. Raising interest rates makes the US $40 trillion debt unsustainable; not raising rates lets inflation spiral out of control. Food crises, social unrest follow; gold likely hits new all-time highs. Probability: 80%–90%

Escalation Scenario

If the US directly strikes Iranian energy infrastructure, add 20 percentage points to the probability of each phase above.

The 1973 oil crisis, the 2008 Lehman moment, the 2022 Russia-Ukraine energy shock—the script never really changes: before the data confirms it, everyone pretends not to see it; and once the data confirms it, the real selling begins.

We are now in that "before confirmation" phase. April 15 to 25 is the critical window. The ultimatum is the first catalyst.

If the Strait reopens, the market will gradually return to normal; if it does not reopen, or the situation escalates further, the market will begin trading the collapse itself, ahead of the actual collapse.

The world doesn't need to actually "run out of oil" to have problems. It just needs enough people to believe: it might happen.