Table of Contents:

1.In the Belly Of The Bea

2.EigenLayer Will Be The Most Important Innovation For Ethereum

3.Blob Transactions Will Not Fix Scalability Issues

4.ZK-Rollups Will Not See Significant Traction in 2023

5.Layer 3s Will Be The True Competitor To Cosmos

Our predictions for the Ethereum ecosystem.

In the Belly Of The Bear

2022 was primed to be a big year for crypto. The industry seemed to evolve dramatically as institutional capital poured into crypto-focused initiatives, exciting new financial primitives were developed, and its legitimacy as an asset class grew around the world. Unfortunately, these narratives were overshadowed by the main story: successive waves of financial impropriety, which occurred largely at the hands of bad actors in positions of power. This exposure of pervasive fraud, combined with tightening global monetary policies, led crypto markets into a mercilessly bearish winter comparable to 2018.

For crypto, 2022 was the year when mercenary capital took hold - entities and actors that move from opportunity to opportunity as value extractors seeking outsized short term profits without any interest in participating in communities or building the infrastructure of the future. This existed within most stakeholders in the crypto space, ranging from end users to liquidity providers to crypto VCs - all engaging in various forms of rugpulling and dumping. However, the three implosions in particular brought the industry to its knees:

Do Kwon’s Terra-Luna took an inherently flawed algorithmic stablecoin model and bribed people to use it with artificial staking yield. Its de-peg wiped $60B in market value and eviscerated the savings of retail investors around the world.

3 Arrows Capital, founded by Su Zhu and Kyle Davies, was an FX arbitrage fund that borrowed aggressively to fund its directional crypto bets. When the severely over-leveraged firm collapsed under adverse market conditions, its $1B in bad debt left massive holes in the balance sheets of lenders across the crypto space.

Finally, the FTX exchange imploded when it was revealed that Sam Bankman-Fried had been appropriating customer deposits and lending them to his trading firm, Alameda Research. Billions were lost as its FTT token cratered, and multiple lenders have gone bankrupt from their losses.

So what does this mean for the industry in 2023? First, we expect the unwinding of FTX positions and pervasive bad debt to continue to negatively impact the cryptocurrency markets through the entirety of the year. Liquidity issues and insolvencies will likely continue to be discovered in both CeFi and DeFi services as bankruptcy and criminal proceedings move forward. Second, the breach of trust involved in this bankruptcy will significantly set back regulatory progress, investor activity, and consumer confidence.

Looking Forward

Despite the serious setbacks to our industry, our outlook for 2023 is optimistic. While mercenary capital has taken its toll on our credibility, we also have an industry full of devoted builders with substantial sweat equity being invested into this burgeoning Web3 world. These are the actors we call visionary capital, the ones still building while most of the industry speculators have left. The ones investing their long-term efforts to bring Web3 to the cusp of breaking irreversibly into daily life. We believe that 2023 is the year of visionary capital, and the year when cryptocurrencies transition from speculative investments to core components of a society built around Web3.

To some extent, this transition is already underway. Between DeFi protocols integrating with the traditional financial system, DAO treasuries accumulating real world assets, and legacy gaming companies breaking into Web3, one of today’s emerging narratives is the blurring of lines between decentralized solutions and the real world. This process will only continue, and 2023 will likely be the year Web3 projects gain traction into the mainstream.

A few examples. In an age when data breaches are ubiquitous, companies will likely start to employ decentralized identity technology to allow users to self-custody data. Consumer-oriented applications of blockchain technology will appear in media, where marketing, storytelling, and gaming will converge to produce immersive and interactive worlds. By building blockchain networks on top of existing power grids, utility companies will be able to incorporate distributed energy resources into new networks of decentralized energy.

While none of this is news to crypto natives, these examples represent the introduction of massive new user bases and suggest that the cloistered world we have occupied over the past decade is preparing to go public. Behind these radical changes to our daily lives will be a wave of technical developments that advance the capabilities of crypto and prepare it for its place at the center of metaverse life. These events are unfolding in real time, and our expectations are summarized below. The following are our predictions for how crypto and Web3 will leap forward in the year 2023.

EigenLayer Will Be The Most Important Innovation For Ethereum

One of the most noticeable discrepancies in blockchain development is seen in the level of permissionless activities that are possible between the infrastructure and application layers. Infrastructure upgrades and changes are lagging behind the application layer as app deployment is permissionless while core network upgrades are permissioned. Consensus, core, sharding, p2p and middleware layer changes are based on democratic voting of appointed parties, while applications can be freely deployed on the core consensus logic and be experimented with.

Established and well capitalized network systems require prudent risk analysis prior to a core upgrade or change. This results in innovative solutions to consensus problems and core hurdles being constrained and/or late to market. Once the sovereign trust network of a system is established, the protocol becomes very rigid and much less prone to innovative upgrades. When innovative consensus mechanisms or middleware layers such as Snowman, Chainlink, or Nomad emerge there is no way to permissionlessly use an existing trust layer to operate the new network.

Moreover, new networks are often bound by inevitable capitalization boundaries. In order for a decentralized network to ensure security of the core consensus logic, it needs to be cost prohibitive for malicious actors to self-impose changes or take control of assets. Thus, it is not sufficient to have breakthrough technology - builders are also required to source a large capital foundation for network security, often becoming the single biggest hurdle in infrastructure innovation.

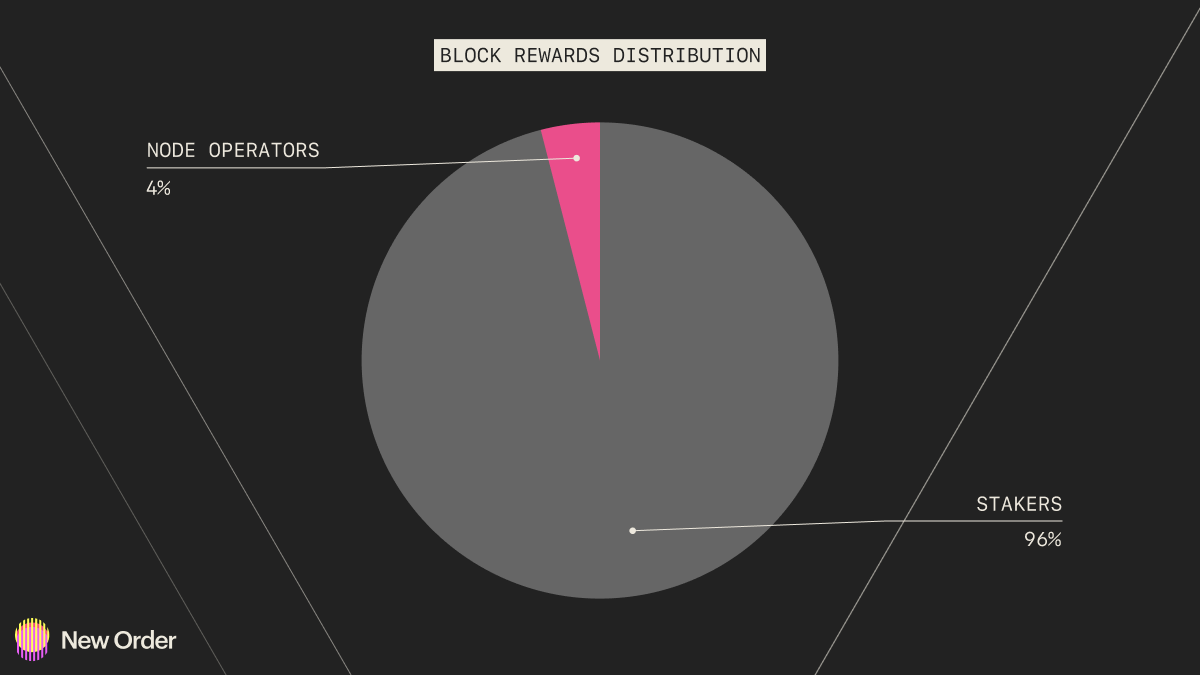

Reward distributions further highlight the capitalization issue in network bootstrapping. In the Ethereum validator stack, 96% of total rewards are allocated to capital providers while only 4% are allocated to node operators. The reward distributions are far from arbitrary and reflect the implicit cost of capital in proof of stake networks. The implied risk of staking a volatile asset for network security is fundamentally more expensive than running a generalized node that can be repurposed.

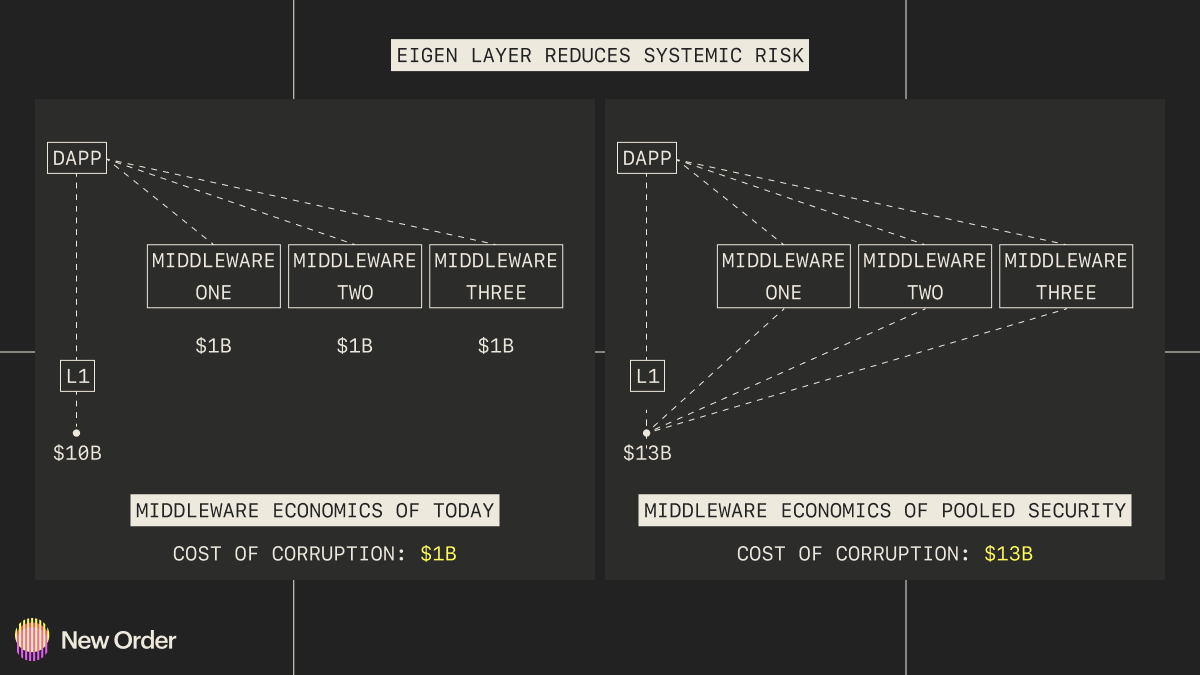

It is important to mention that bootstrapping core infrastructure security is the primary consideration for decentralized networks. That being said, applications built upon it are always constrained by the least secure denominator in their infrastructure stack. Applications that are incorporating middleware layers such as bridges and oracles, which are secured by their own sovereign trust networks, are decreasing the overall security of the system to that of the least secure dependency.

To tackle the core divergence of innovation from infrastructure to the application layer EigenLayer is introducing a simple, yet extremely effective, solution to the prohibitive cost of capital problem: re-staking.

The EigenLayer Approach

EigenLayer is a smart contract layer on Ethereum that allows users to leverage an existing trust network to secure other core infrastructure and middleware layers through the use of re-staking. At its core, re-staking is utilizing the same staked ETH that is used for Ethereum network validation to secure other networks. This allows ETH stakers to have much more flexibility with their staked capital while extending the trust layer to periphery infrastructure like side chains, middleware, or even other non-Ethereum networks.

EigenLayer is introducing a two-sided marketplace where ETH stakers are able to provide services to networks in need of a trust layer. This introduces the ability for new networks to cut the cost of network security while simultaneously gaining access to a vast pool of capital. In practice, this eliminates the least secure denominator problem in the application layer. Oracle and bridge networks would source security and trust from the same infrastructure layer that the applications themselves are built on. EigenLayer allows for consolidation of trust which ultimately increases the security of all networks interacting with the layer. For example, a brand new entrant into the asset bridge sector can interact with EigenLayer and immediately gain access to an $18.7B security base.

Given that ETH stakers do not incur any marginal cost of capital while validating other networks, restaking substantially improves the range of possibilities that stakers have. EigenLayer does come with several leverage and slashing risks as the underlying staked assets could be slashed across multiple secured networks if malicious behavior is encountered. Whenever the same capital is used to validate more than one network, the asset base is intrinsically leveraged, opening the system to potential cascades.

Slashing risk is compounded and can result in slashing contagion. The slashed stake, as a result of malicious behavior or downtime, inherently reduces the security consideration on all validated networks. If not controlled and potentially restricted the contagion can be detrimental to the systems architecture. At launch, EigenLayer will be introducing prudent leverage guidelines and limits to ensure stability of the trust system.

EigenLayer is also developing a data availability layer for Ethereum called EigenDA. This layer is similar to the current danksharding specifications, including features such as data availability sampling (DAS) and proof of custody. However, EigenDA is an opt-in middleware rather than a core component of the protocol. Being a middleware layer allows for stress testing without a need for a hard fork which offers several advantages: permissionless experimentation with the DA layer and allowing validators to participate on an opt-in basis. If the pseudo-danksharding implementation is successful at scale with EigenDA, it could become the de-facto DA layer for all optimistic and zk-rollups built on top of the Ethereum ecosystem ahead of the lengthy process of Ethereum-level protocol changes.

During the protracted 2022-2023 bear market liquidity is expected to continually seek safety within Ethereum, further solidifying the network as a safe haven and central trust layer in crypto. The run for safety will further build out the Ethereum capital base, widening the gap among alt-L1s and pushing the cost of capital for new native validation networks to borderline prohibitive levels.

Access to re-staked ETH security will result in a dramatically reduced cost of scaling for middleware, sidechains, and the general decentralized tech stack. We believe Eigen will offer the most dramatic change to how decentralized networks are built since the initial introduction of Ethereum in 2015.

Blob Transactions Will Not Fix Scalability Issues

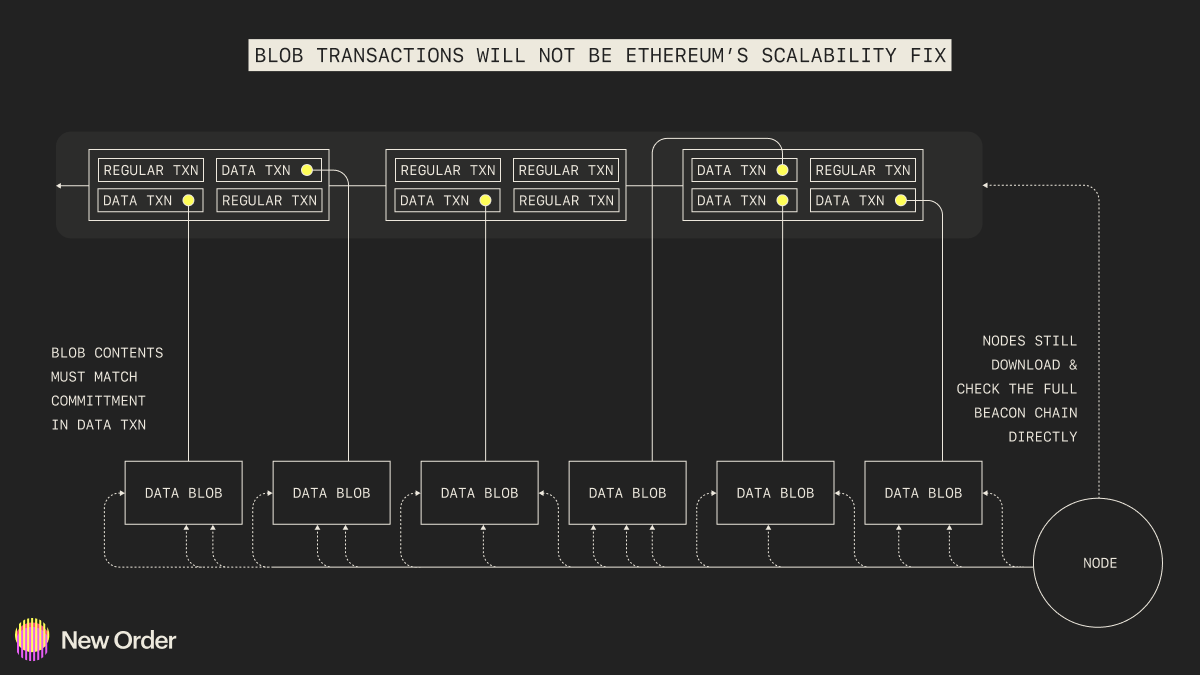

Blob transactions aren’t going to be the magical fix to Ethereum scalability until modularity is reached. Reaching modularity will come with considerable technical hurdles and delays. The dramatic increase in on-chain data is also going to drive the need for state expiry to alleviate state bloat and might even lead to changes in the peer-to-peer structure of Ethereum. Blob transactions are introducing a new data format for calldata (on which rollups depend) which contains large amounts of additional data that won't be accessed by EVM execution, but rather only accessed for commitments. This new data market is going to become increasingly competitive as the amount of rollups and modular execution demand grows. This implies that we will likely see price competitiveness just like we've seen competitive gas prices on Ethereum, we will likely see competitiveness around Data_gas, which is the new type of gas being implemented. There's also quite a few kinks to iron out, such as whether the gas should be time or slot based, since if slot based there's the possibility of missed slots without blob transactions which would make it look like demand has increased, and this would affect gas prices.

https://www.eip4844.com/

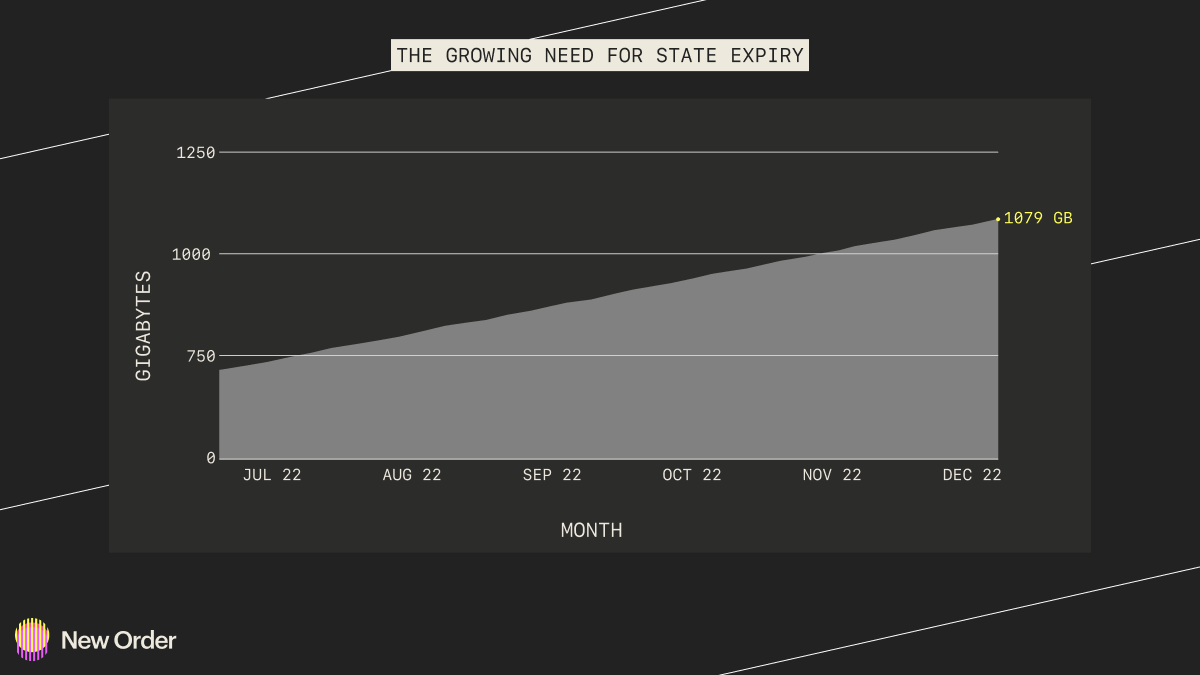

There's also the problem of the actual gossiping of blob transactions on the peer-to-peer network since the sizes of these blobs are much larger than anything currently being gossiped. This needs further research which Paradigm is currently exploring. It will be interesting to see where this lands, and whether or not the Ethereum network can handle this further state bloat and data. Regardless, state expiry will most likely be needed to limit the growth of the state of Ethereum - which currently sits at a wild 1079 GB for a chain full sync, and grows larger every day. State expiry would either be implemented with state rent, so renting out state to be stored off-chain, or through removing state on a monthly or weekly basis, that then gets stored on archival nodes (which are sadly quite centralized at this point).

https://ycharts.com/indicators/ethereum_chain_full_sync_data_size

What becomes clear as Ethereum and many others position themselves for the coming years is that in order to retain decentralization and “keep up with the times”, they have to move towards modularity.

ZK-Rollups Will Not See Significant Traction in 2023

Zero-knowledge (ZK) rollups will not gain significant traction in 2023 due to their lack of production readiness and inability to achieve sufficient decentralization. By production readiness, we mean especially their VMs and the proving times of proofs.

Instead, it is expected that ZKPs will see widespread usage, particularly in non-interactive state proofs. Projects such as Herodotus, Axiom, ETHStorage and Lagrange will use them for various data sharing purposes that require on-chain or cross-chain storage proofs.

Many bridges are expected to begin using ZKPs for interoperability purposes, with several already moving in this direction, including Wormhole, Polymer, and the ZKBridge collective.

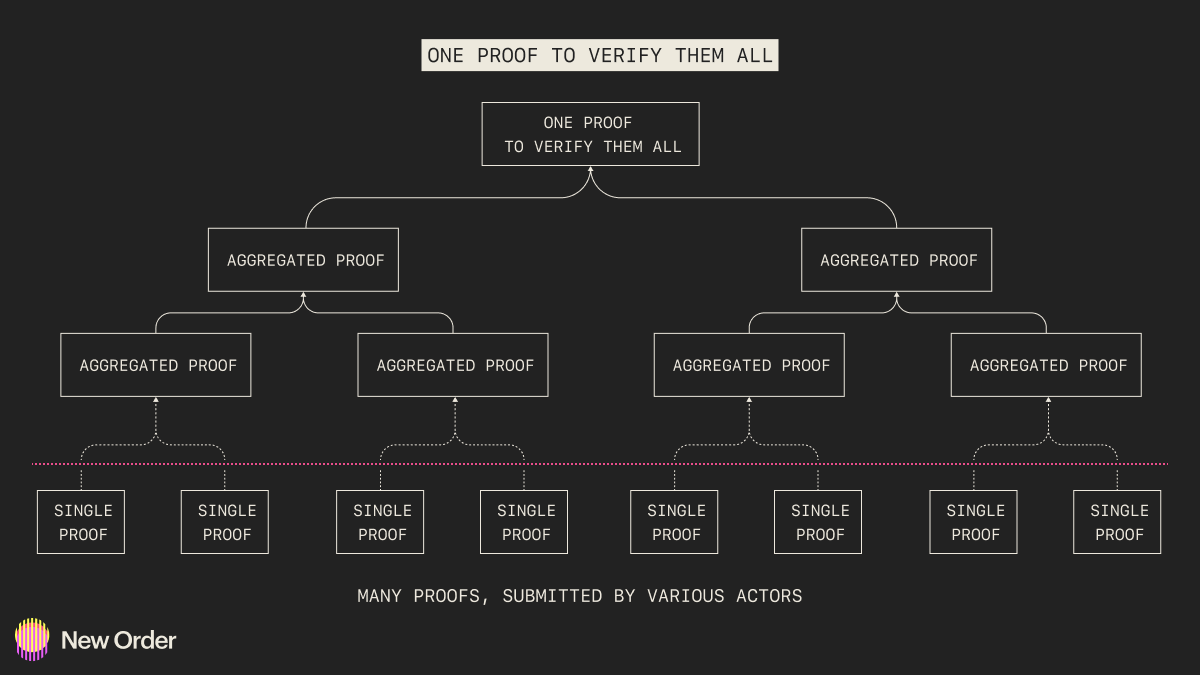

These applications of ZKPs are almost ready for use and are expected to have reasonable pricing for on-chain verification. These uses of ZKPs improve efficiency through recursion, which involves aggregating multiple proofs into a single, smaller proof. Most protocols have recognized the need for recursive ZKPs to reduce costs and increase efficiency, though some proof schemes are more efficient than others. However, it does come with some caveats, as some proof schemes are more efficient than others.

https://ethresear.ch/t/reducing-the-verification-cost-of-a-snark-through-hierarchical-aggregation/5128

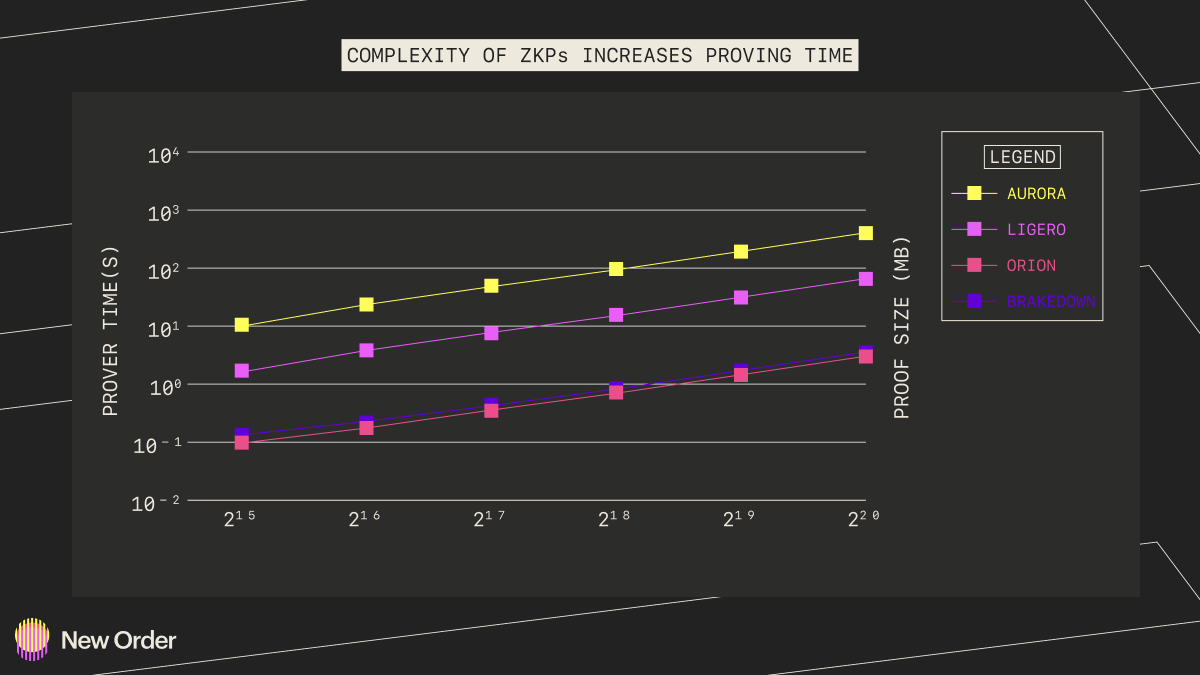

Many existing ZK schemes and algorithms with succinct proof sizes experience high overhead during proof generation time (also known as proving) which limits their efficiency and scalability. To address this issue, projects such as Supranational, Ingonyama, and DZK are working to improve the efficiency of proof generation. However, what's important to realize is that this hardware acceleration is only partially responsible for efficient proving. There's optimisations to be made on the algorithm level, software level and others. It is also important that said systems are kept sufficiently decentralized, which is hard to achieve in practice.

https://eprint.iacr.org/2022/1010.pdf

Lastly, the proving time also increases with the complexity of the ZKPs in question. Considering all the factors mentioned, it is undoubtedly difficult to build a sufficient ZKRollup that will gain significant traction in 2023. For now, the most efficient use of ZKPs are in smaller scale operations such as the non-interactive state proofs and interoperability mentioned earlier.

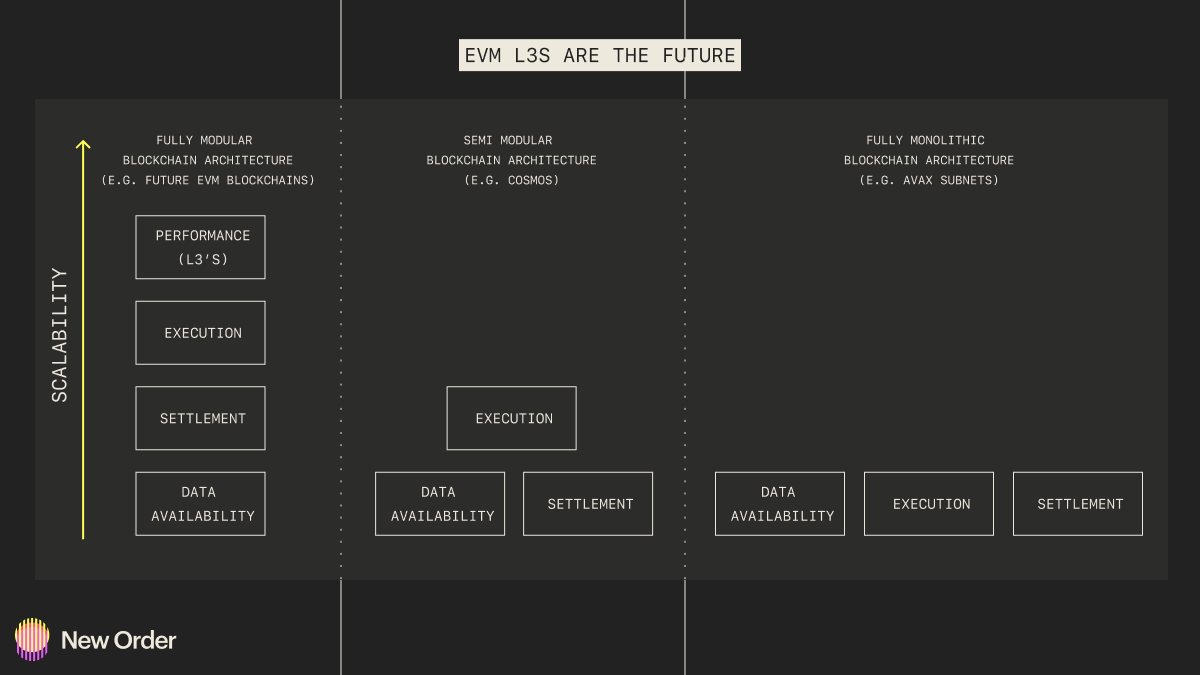

Layer 3s Will Be The True Competitor To Cosmos

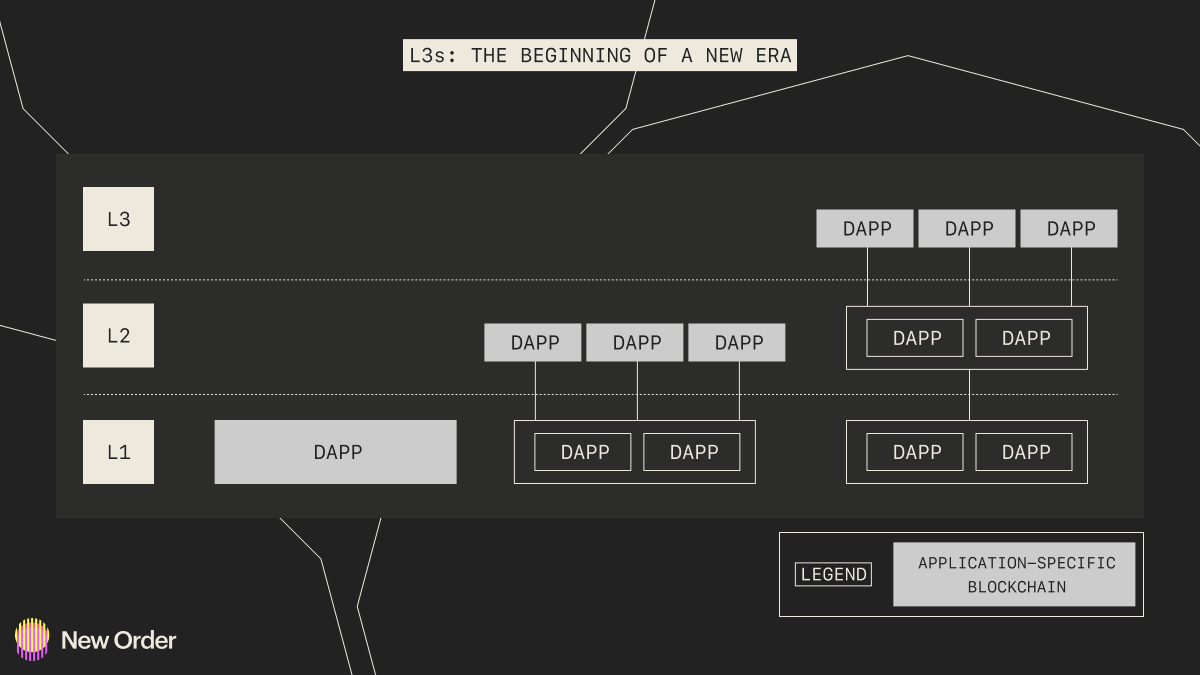

Layer 2s (L2s) improve Ethereum's scalability by lowering gas fees and increasing throughput. Due to these scalability factors, tradeoffs exist, and L2s must choose to optimize for particular items. Layer 3s (L3s) are application-specific blockchains built on L2s, purposed to mitigate these tradeoffs and make more improvements. They are similar to app-chain environments like Cosmos, Avalanche, and Polkadot but benefit from being built on modular blockchain protocol stack instead of monolithic ones. Thus, deploying a fully modular blockchain infrastructure stack that includes a general-purpose L2 with customizable L3s will mark the end of the monolithic app-chain ecosystem era and the beginning of a new era in decentralized application development.

https://medium.com/1kxnetwork/application-specific-blockchains-9a36511c832

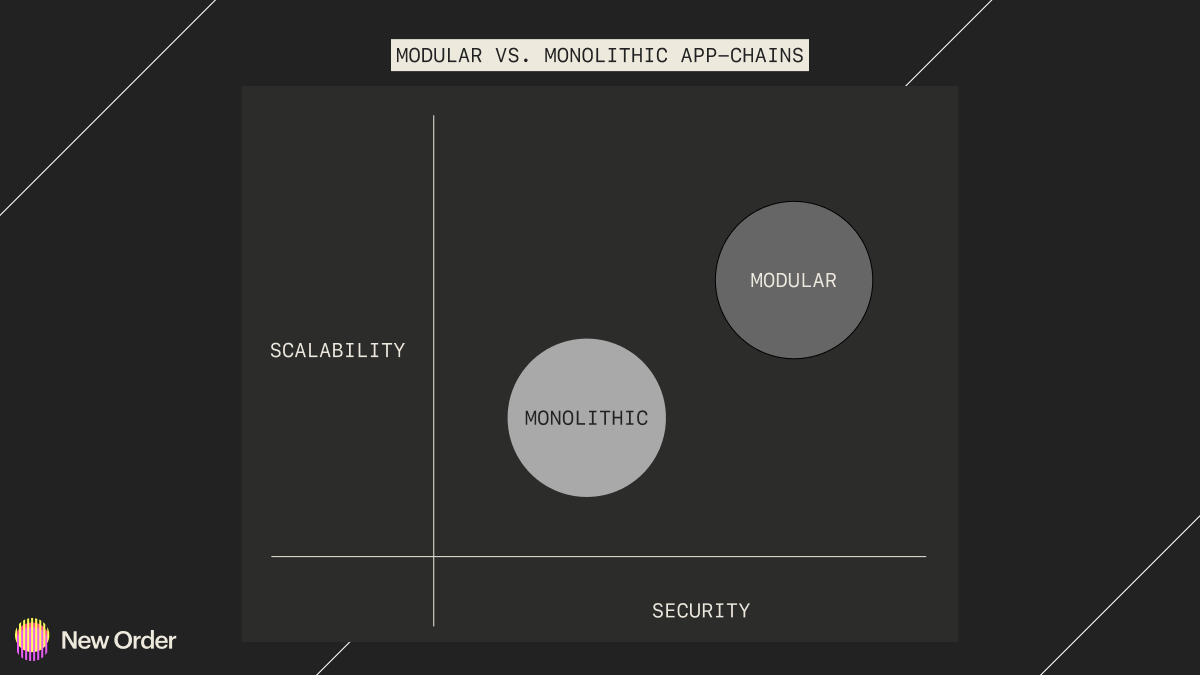

At the moment, monolithic app chains are the preferred choice for many applications because of the freedom it allows them to create their custom logic and smart contracts while achieving better execution. Additionally, app chains own their block space, so they do not have to compete with other chains on execution. But this is not as efficient as it could become. Utilizing any piece of monolithic blockchain architecture like app chains built on modular software (e.g., Cosmos) or as an entirely monolithic app chain (e.g., Avax Subnets) limits their ability to decrease transaction costs and increase computational throughput.

Comparatively, app chains built on fully modular blockchain protocols deduct unnecessary frictions since they can leverage optimized blockchain layers constructed for a specific function. Suppose you compare an L3 built on top of the L2 zkSync, utilizing Celestia for data availability and Ethereum for settlement proofs and consensus, to a monolithic app chain that combines all or some layers. In that case, the only way forward is to build modularly to achieve better scalability while retaining decentralization.

Notably, the measure of these benefits outweighs what monolithic app chains can theoretically achieve. For example, An L2 receives a 100x cost reduction compared to an L1, and an L3 can receive a 10,000x cost reduction compared to an L1. A real-world implementation is being built by zkSync—their zkPorter L3 increases scalability with a ~100x fee reduction and 20,000+ max TPS. L3s offer not only improved performance, but also the ability to be customized for specific purposes. This includes adding privacy features in using ZKPs, designing custom DA models, and enabling efficient interoperability solutions.

Almost every related EVM L2 plans to develop customizable L3s on top of their L2. Further, opportunities will arise for more modular blockchains to be built using Celestia's shared data availability base layer. Yet, for this prediction, the vital thing to note is that the future development of app chains will occur as L3s on modular blockchain stacks, not monolithic ones. Combining the EVM's decentralization and security with scalable L3s makes the modular environment far better than monolithic app-chain ecosystems. Significant interoperability issues still need to be addressed, particularly for cross-rollup transactions. However, progress is being made, and it is anticipated that L3s will be available in late 2023.

Thus, if L3s can solve interoperability issues, deploying app chains built on a modular blockchain tech stack will be the monolithic app-chain thesis killer. L3s will retain a certain extent of Ethereum security, increase speed and scalability, and allow the Dapps to be customized toward specific use cases. App-chain ecosystems like Cosmos are positioned to continue gaining traction in 2023. However, with the eventual deployment of L3s in 2023, we will see the app-chain narrative switch from monolithic to modular ecosystems.