On Wednesday, July 27th at 14:00 pm ET, the Fed chairman will talk about his views on the next interest rate hike, and global market sentiment is tense. On the next day, the US GDP data for the second quarter will be released. Both will guide the market between a rate hike and a recession, respectively.

1. Interest rate hike on Wednesday, GDP data outlook

(1) The market's speculation on interest rate hikes is divided, and a rate hike of 75 may be the most suitable

1) Market view

Last week, Fed watcher Nick Timiraos, the Fed's "buzzer"--"Wall Street Journal" , hinted that the Fed may continue to raise interest rates by 75 basis points at its July meeting to actively combat high inflation.

This Monday, the British "Financial Times" analyst Colby Smith also issued an article saying that the Federal Open Market Committee (FOMC) meeting will be as expected by the market, raising interest rates for the second consecutive month by 75 basis points. That would lift the federal funds rate to a target range of 2.25% to 2.50%, in line with Fed officials' long-term estimate of "neutral" policy.

Goldman Sachs, Reuters, Westpac and Austrian Sberbank currently believe the Fed will raise interest rates by 75 basis points in July, due to the possibility of peak inflation in the United States and the fact that many hawkish Fed officials have previously given the Expectations of a 100 basis point hike poured cold water.

Goldman Sachs chief economist Jan Hatzius said the FOMC is not expected to accelerate the pace of interest rate hikes in the near future due to softening inflation expectations and falling gasoline prices, and should only raise interest rates by 75 basis points at its July meeting . To put it another way, the 100 basis point interest rate hike this time, the reduction in the rate hike in the remaining 3 meetings during the year is not much different from the 75 basis point rate hike this time.

"The atypical swing in policy expectations reflects the fact that all real growth data, except the jobs report, show signs of a clear slowdown, that Fed tightening is already having a significant impact on the economy," said Mizuho Securities' chief U.S. economist Home Steven Ricchiuto wrote. " But as long as payrolls remain a contradictory indicator, investors can't be confident that the Fed is about to end its rate hike cycle. "

2) What will happen to the market if the rate hike exceeds expectations?

The short-term reaction to Wednesday's 100-basis-point rate hike could be a sharp sell-off in the market. Growth stocks' valuations will be affected by rising interest rates, and further Fed tightening will increase the likelihood of a recession, hurting cyclical stocks. Defensive utilities or consumer staples may be the best bets, but even those in the bond agency industry are not immune. Bond prices fall as yields rise. In this case, the dollar may be the only winner.

A weaker-than-expected 50-basis-point gain could point to a short-term rebound , as higher interest rates weigh less on valuations and the Fed shows caution about the economic pressure it causes. But the rebound may not last, as commentators will start to worry that the Fed is not doing enough to fight inflation — and whether smaller rate cuts are a warning sign for the health of the economy.

A 75 BP hike is a middle ground acceptable to both pessimists and optimists.

(2) The Fed's opinions on raising interest rates are quite different, and Powell may not provide forward guidance

is currently difficult for the Fed to agree on the extent of future interest rate hikes, which increases the difficulty of providing forward guidance. Fed officials widely believed last month that the U.S. federal funds rate would need to rise to at least 3 percent this year, but some officials recently said it should rise to 4 percent by December.

The Fed has revised its rate hike expectations several times this year as forward guidance has not kept pace with changes in inflation data.

by 50 basis points at its June meeting . However, after the June inflation data deteriorated (released a few days before the meeting), the Fed changed its tone again and raised interest rates by 75 basis points (finally) two days before the meeting, using the "new Fed News Agency".

And after the June meeting, the Fed began to let the possibility of raising interest rates by 50 or 75 basis points in July, saying that a 75 basis point rate hike would not be very common (tends to 50). But the previous guidance was slapped in the face again after the unexpected June inflation data came out. Markets even started betting that the Fed could raise rates by a full 100 basis points, an expectation that didn't cool down until the Fed officially came forward . The Fed is now widely expected to raise interest rates by 75 basis points in July.

At a news conference after the May meeting, Powell acknowledged that trying to give forward guidance 60, 90 days in advance is very difficult . He said he hoped to give the Fed enough room to watch the data and ultimately make a decision.

2. Mid-term market observation

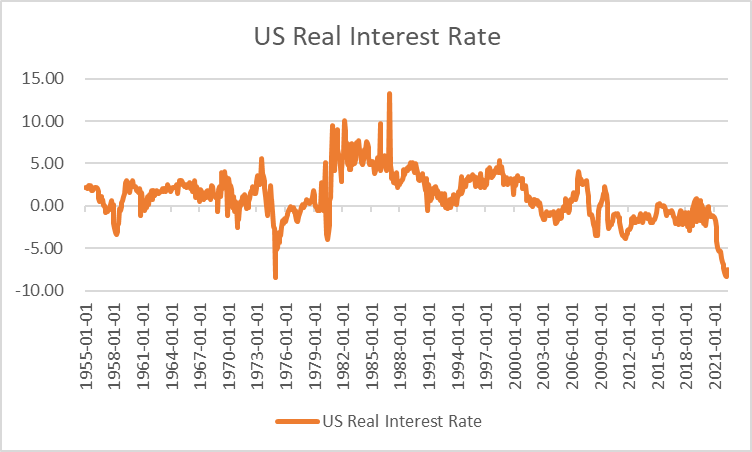

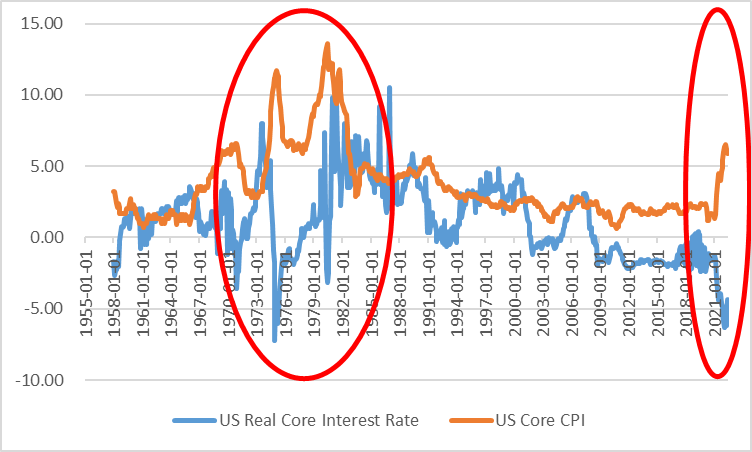

(1) The real interest rate hit a record low, and the labor market performed strongly

1) Real interest rates hit a new low

Due to the one-time disruption of the Russian- Ukrainian incident , the real interest rate (Federal Base Rate - CPI ) began to dive. In recent months, real interest rates have basically touched the level of the first oil crisis in the 1970s.

It is precisely because of this that the Fed had to continuously raise interest rates during the year to ease the pressure from inflation.

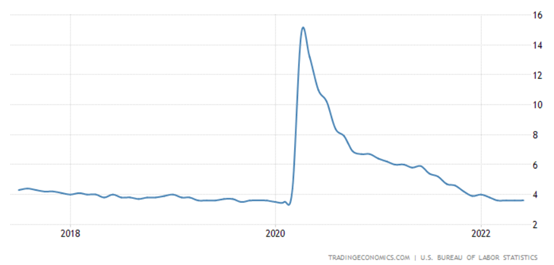

2) Strong labor market

U.S. labor market cooled in late spring but remained strong amid falling job openings, fewer layoffs and more layoffs, the Labor Department's May hiring demand and worker turnover data showed.

Chart: US Unemployment Rate

"These historically unusually tight labor market conditions may actually be prolonged for a long time," said Julia Pollak, chief economist at jobs site ZipRecruiter .

Economics 101 : According to the Phillips curve, inflation and employment have a negative relationship in the short run. A strong U.S. job market has allowed the Federal Reserve to ease concerns about raising interest rates on the job market.

(2) Fiscal policy is difficult to underpin the US economy, and liquidity may not be able to improve in the short term

1) U.S. fiscal policy space is limited

Ukraine incident is painful, which directly causes stagflation due to the tightening of the supply side. Due to excessive borrowing, the United States has no way to use fiscal policy to eliminate the threat of recession and rapidly rising inflation, and the rise in interest rates has brought about a weakening of the United States' ability to repay its debt .

2) If you increase fiscal spending, it will also worsen inflation

The previous recessions in the United States involved massive monetary and fiscal easing. But this time, due to a one-time external shock, prices have risen rapidly. Rapid inflation has discouraged the US Treasury from increasing investment.

3) The direction of stagflation is relatively determined

From the perspective of the next six months, the Fed is likely to strive to find a seemingly balanced point between interest rate hikes and recession - stagflation.

4) The capital market is expected to be stable

Fed still has room to continue to tighten monetary policy, and the strength of the dollar and the tightening of the currency may not be able to ease in the short term . The near-term market should mainly rely on the trend of CPI .

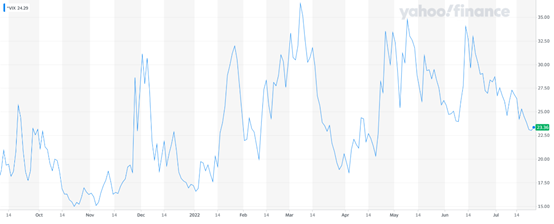

Chart: The VIX Index

The market's recent VIX index hit a new recent low, proving that market sentiment is gradually picking up. The rapid rebound in the market last week is also the release of optimism in this market .

The market is betting that the marginal improvement brought by the recession will lead to a rapid rebound in currency prices, but it seems that concerns about raising interest rates may not be relieved in the short term. If Ballmer can't come up with a lower expected rate hike this week , the market may not be able to turn around before the next rate meeting.

5) I am afraid that there will be no liquidity benefits in the short term

Despite the specter of a recession, we still don't expect the Fed to ease its targets anytime soon, as the job market remains strong and real interest rates remain negative.

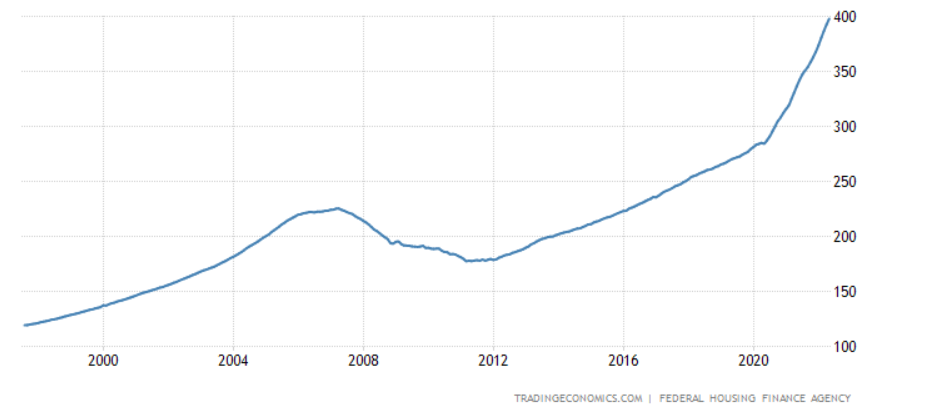

In addition, we believe that US core inflation is also expected to remain relatively sticky . The reason for this high stickiness is that the housing CPI, which accounts for the highest proportion of the U.S. core service CPI, will continue to rise, and wage growth and changes in consumer habits may make it difficult for the U.S. core service CPI to fall sharply.

Chart: United States FHFA House Price Index

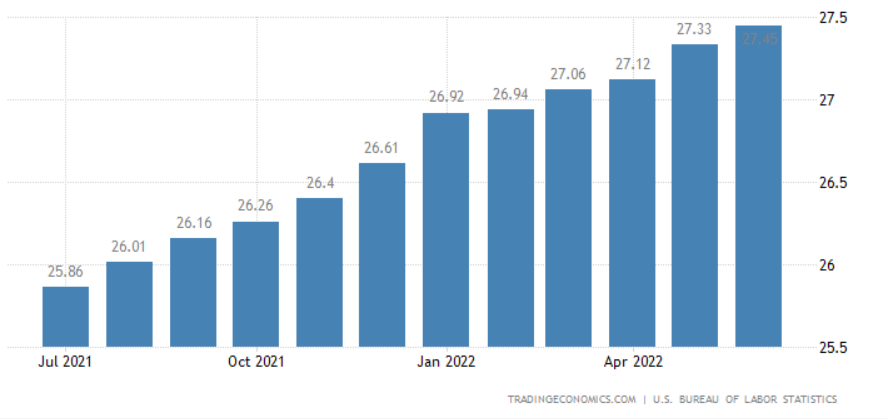

Although wage growth has slowed, wage growth is one of the stickiest factors in inflation, and it may be difficult to reverse in the short term.

Chart:United States Average Hourly Wages

(3) There is no hard foundation for the market to fall

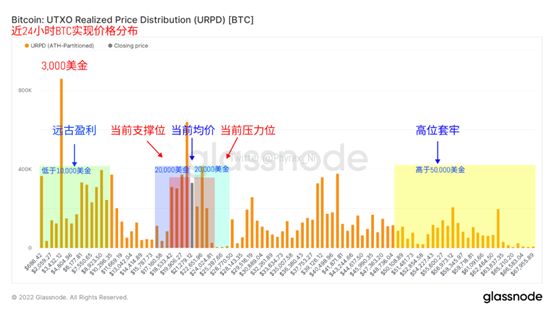

1) Bitcoin has price support

At present, the chips in the market are concentrated in the middle stage, and the market has entered a relatively stable support level. Even if Bitcoin continues to fall, the space is relatively limited.

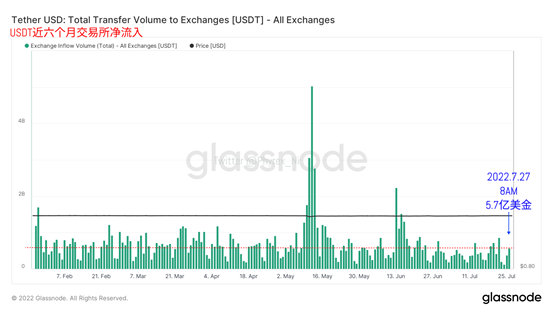

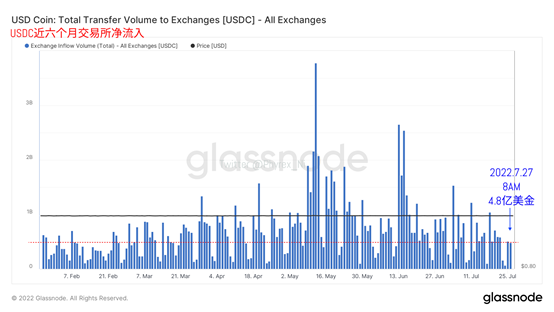

2) From the perspective of stablecoins, the market has a strong willingness to hunt for dips

USDT, which is the main buying force, has more inflows than Monday , and it is the highest level in the past month.

through USDC is not strong, and it is currently maintained at a relatively stable trading level.

3. The currency price may remain volatile in the short term, and long-term investors can buy dips

When inflation has not yet reached an inflection point and the currency price has received strong support, maintaining a certain range of oscillation may be a high probability event.

The current market odds are relatively good, and the winning rate space is still imaginative. It is recommended that long-term investors can build positions on dips.