The price of Ethereum [ETH] reached $1,700 on 17 February after five months. Is this ascent an indicator of things to come? Or will the whale accumulation result in dumping before the Shanghai upgrade?

“”

ETH witnesses brief surge

“”

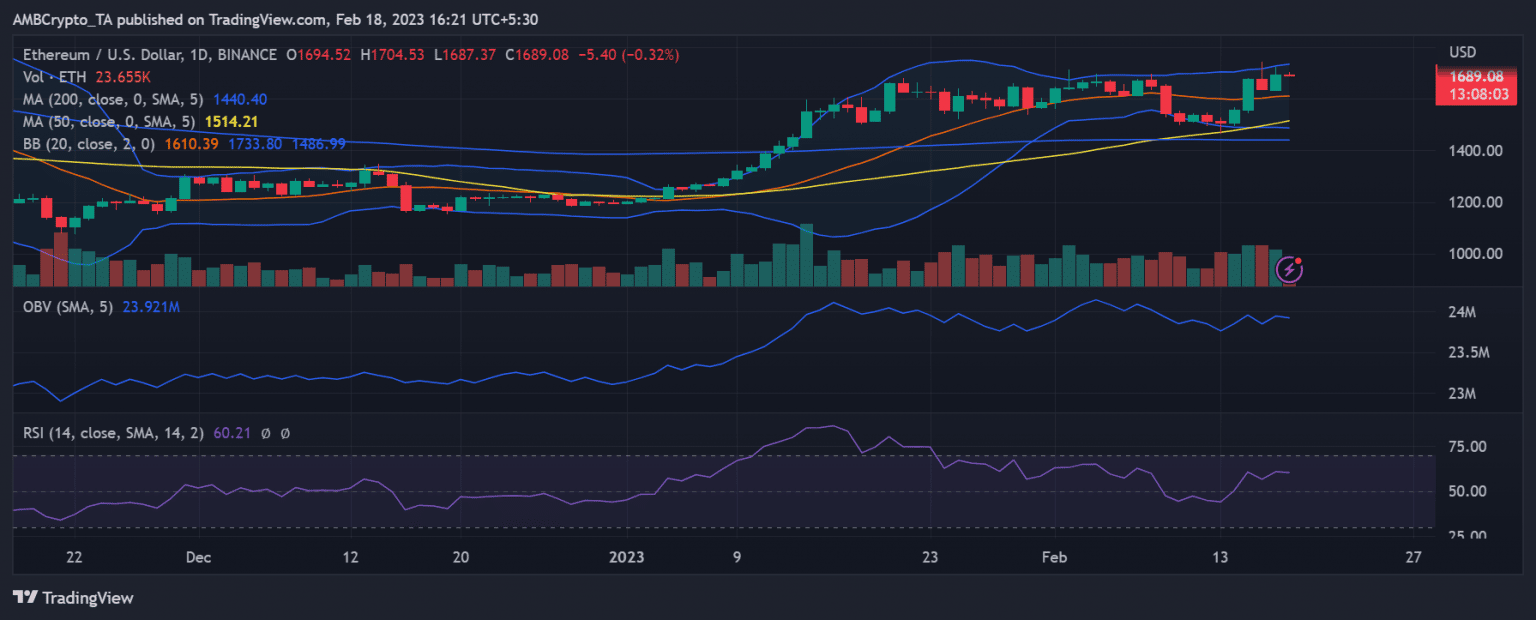

Ethereum gained 3.45% on 17 February, according to a daily period analysis of the cryptocurrency. According to additional research into that trading period, it peaked at $1,721 before ending trade at $1,694.

“”

It was five months since ETH’s price had last reached the $1,700 range during that trading period. Its price was roughly $1,694 at the time of writing.

Source: Trading View

“”

Furthermore, the Relative Strength Index (RSI) indicated that ETH was in a bull trend because its line was above the 60 mark. The price movement was also noted above both the long and short Moving Averages (blue and yellow lines). Therefore, the asset’s price moving above the (MAs) suggests a good price move and may also point to a possible future uptrend.

“”

Shark and whale hold on

“”

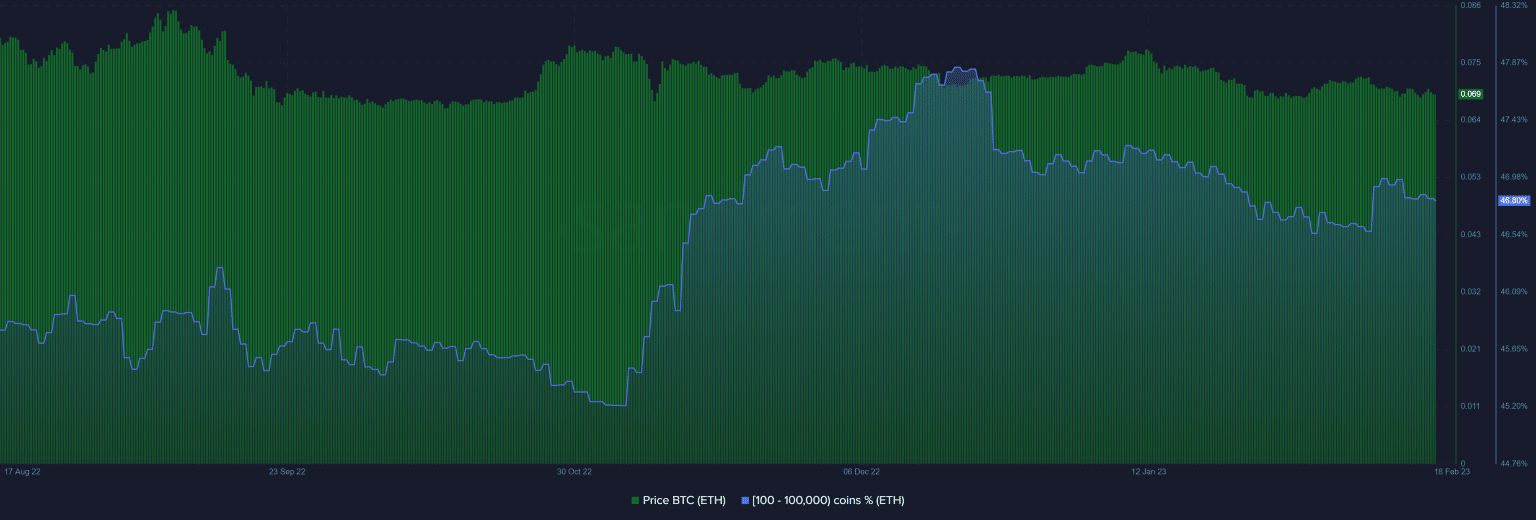

Recent data from Santiment showed that whale and shark addresses were still tightly clutching onto their ETH bags. The graph shows that whale and shark addresses with 100–100,000 ETH still retained close to 47% of the entire supply of ETH. Furthermore, the absence of a sell-off following the most recent price increase suggested that investors anticipated further price increases.

Source: Santiment

“”

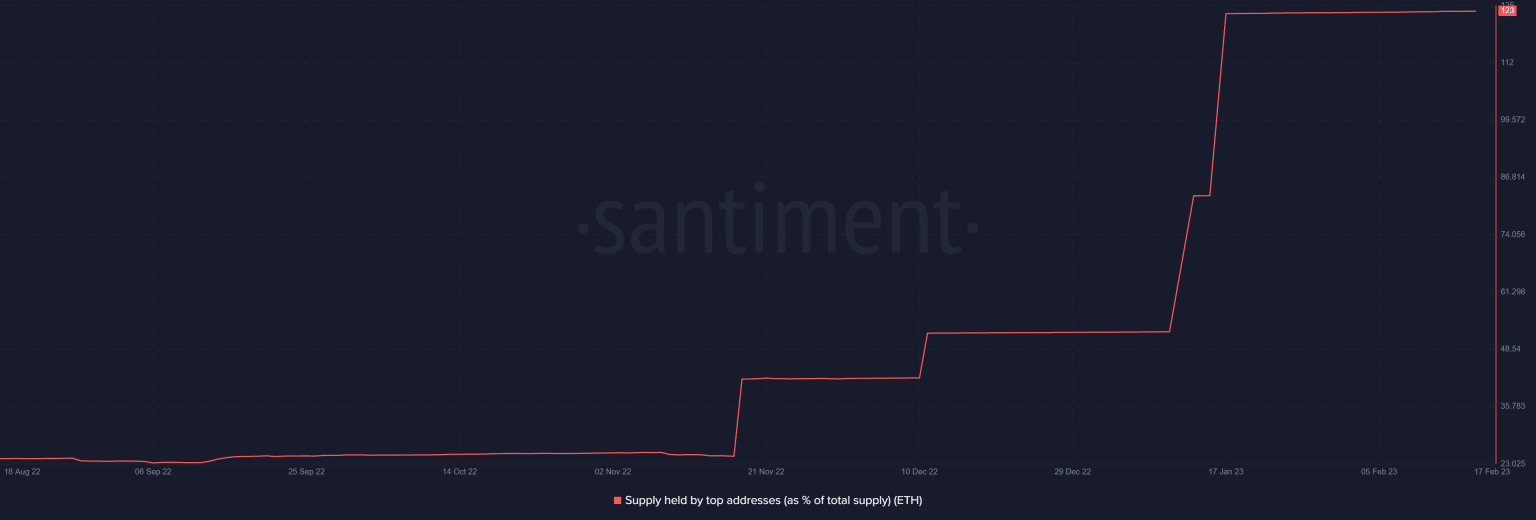

In addition, an examination of the supply owned by the top addresses revealed that the addresses at the top had been on an accumulating binge. For most of January, the graph showing the quantity held by the top addresses as a proportion of the overall supply of Ethereum was rising. It has now leveled off, but at the time of writing, it was at 123.

Source: Santiment

“”

Volatility incoming?

“”

Ethereum’s Shanghai upgrade will be the next big thing for the cryptocurrency sector. In March, users can withdraw more than $16.5 million worth of Ethereum (ETH) off the blockchain. The Merge was the last significant improvement to the network; however, it had little effect on the price of Ethereum.

“”

The Shanghai upgrade will affect the supply and demand of ETH, whereas the Merge was a purely technological development with no apparent economic consequences. However, because of the long-term and short-term nature of the upcoming development, it has the potential to affect the ETH price significantly.

“”

When staked ETHs are released, it is unknown how the shark and whale addresses will respond. But if they, too, decide to sell their assets, ETH’s value will plummet. So, in terms of Ethereum’s price movement, March will be a crucial month.