I. Conceptual Evolution: From Crypto Leverage Tool to Mainstream Financial Infrastructure

On-chain lending is not a new concept. In 2020, Compound introduced liquidity mining, propelling DeFi beyond niche communities into the mainstream and ushering in the “DeFi Summer”. At that time, on-chain lending functioned primarily as a high-leverage crypto-native tool: users over-collateralized crypto assets to access liquidity, then deployed that liquidity into yield aggregators or automated market makers to chase annualized returns far exceeding traditional finance. This model performed well in bull markets but exposed structural fragility during downturns. The Terra/Luna collapse and FTX bankruptcy in 2022 revealed the vulnerability of high collateralization ratios and cascading liquidations. After two years of market restructuring, on-chain lending has completed a critical transition from a leverage primitive to a capital allocation infrastructure. This transformation is driven by three forces: 1) Regulatory clarity: Frameworks such as MiCA in the EU and growing acceptance of crypto ETFs have lowered compliance barriers for institutional capital; 2) RWA tokenization wave: U.S. Treasuries, tokenized corporate bonds, and real estate income streams are now entering on-chain lending as core collateral, reshaping asset composition and user profiles; 3) Interest rate market evolution: From pure floating rates → fixed-rate protocols (e.g., Notional, Yield Protocol) → hybrid systems (e.g., Pendle), on-chain rate formation is converging with traditional financial markets.

As of early 2026, the on-chain lendinge market has crystallized into a clear three-tier asset architecture: at the base lies stablecoin lending dominated by USDC, DAI, and USDT, which represents the largest, lowest-risk segment, with typical loan-to-value (LTV) ratios reaching 80%-90%; the middle layer consists of volatile-asset lending backed by major cryptocurrencies like ETH and BTC, where LTVs are typically capped at 50%-70% to mitigate liquidation risks amid sharp price swings; at the apex sits RWA-backed lending including tokenized U.S. Treasuries (e.g., Ondo Finance’s OUSG), corporate credit (e.g., Maple Finance’s private debt), and real estate income rights, which is rapidly emerging as on-chain lending’s new growth engine, particularly attractive to institutional investors seeking compliant capital entry points. Geographically, user profiles are diverging: Asian markets remain dominated by retail investors and arbitrageurs who favor high leverage and complex strategies; European and U.S. markets exhibit clear institutionalization trends, with heightened demand for compliant custody, KYC verification, and audit transparency. This divergence directly shapes regional protocol design priorities.

II. Competitive Landscape: One Dominant Player with Structural Differentiation

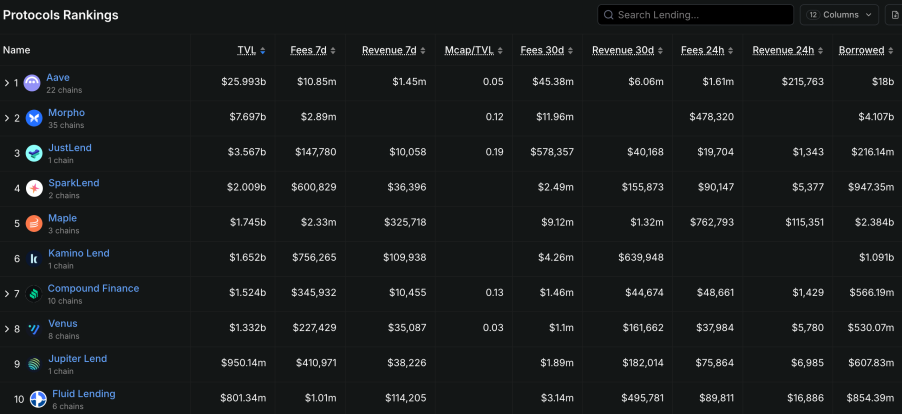

The market exhibits a classic “one dominant player with multiple strong challengers” structure. Aave leads decisively with approximately $32.9 billion in TVL, far exceeding competitors such as Compound (with about $2.6 billion), while capturing over 50% of lending TVL. Nevertheless, its moat is not brand or network effects—largely irrelevant in open-source ecosystems—but continuous product iteration and ecosystem expansion. From Aave V1’s floating-rate model, to V2’s credit delegation and flash loans, to V3’s Portal cross-chain liquidity and isolation mode, each Aave generation precisely addresses prevailing market pain points. The upcoming V4 release—scheduled for mid-2026—will further enhance cross-chain liquidation capabilities and embed institutional-grade compliance frameworks. Against Aave’s dominance, a cohort of differentiated protocols is carving out their own niches. Morpho Labs pursued an unconventional evolutionary path: beginning as an optimization layer atop Aave and Compound (boosting capital efficiency via P2P matching), it gradually evolved into independent offerings such as Morpho Blue (oracle-free, governance-free lending) and Morpho Vaults (professional risk managers curating yield strategies), transitioning from “optimization layer” to “standalone protocol”. Spark Finance, meanwhile, leverages MakerDAO’s DSR (DAI Savings Rate) ecosystem to establish a robust user base in stablecoin lending, with its technical synergy with Aave V3 positioning it as a key conduit for institutional adoption.

Technologically, on-chain lending protocols are diverging along three distinct pathways. First is the “liquidity aggregation” path (P2Pool), represented by Aave, Compound, and Kamino Finance. Its core premise is pooling lenders’ funds into shared liquidity reserves, dynamically adjusting interest rates algorithmically based on utilization to enable efficient capital allocation. Advantages include deep liquidity and streamlined UX; drawbacks include relatively lower capital efficiency (lenders cannot negotiate terms directly with borrowers). Second is the “peer-to-peer matching” path (P2P), exemplified by Notional Finance and Myso Finance. Its core idea is direct lender-borrower matching to deliver fixed-term, fixed-rate borrowing experiences. While offering superior rate stability, this path suffers from comparatively thin liquidity, making it better suited for borrowers with clearly defined funding timelines. Third is the “permissionless pools” path, led by Euler Finance (V2) and Ajna Finance. Its philosophy is to fully delegate risk management to the market—no oracles, no governance votes—allowing borrowers and lenders to set parameters autonomously and bear risks individually. Though maximally decentralized, this approach entails higher user education costs and elevated smart contract risk.

III. Core Risks: The Triple Challenges of Liquidation, Credit, and Cross-Chain Security

The risk landscape of on-chain lending is significantly more complex than traditional finance. Unlike banking systems, on-chain protocols lack deposit insurance, central bank lender-of-last-resort facilities, or regulatory window guidance—when crises strike, liquidation mechanisms become the sole price discovery mechanism, and their “ruthless automation” often amplifies downturns during market panic. Liquidation cascades represent the most typical systemic risk. On March 12, 2020—the “Black Thursday”—Ethereum’s price plunged 37% in a single day, triggering massive MakerDAO liquidations; insufficient liquidity led to zero-price auction executions, with ETH collateral clearing at just 50%-60% of market price. Similar events recurred during the May 2022 UST/LUNA collapse, forced liquidations of highly leveraged positions on Aave and Compound further intensified market sell pressure. To counter liquidation cascade risk, protocols have adopted varied strategies: Aave V3 introduced “Efficiency Mode”, enabling borrowers to optimize collateral efficiency for specific asset pairs; Isolation Mode quarantines high-risk assets in separate pools, preventing contagion across the protocol; Ajna Finance completely eliminated oracles, instead using supply-demand dynamics between collateral and debt for automatic pricing—fully delegating price discovery to the market.

Credit default risk forms the second major challenge. Unlike over-collateralized “machine-executed” models, uncollateralized or under-collateralized on-chain credit lending inherently faces evaluation difficulties. Goldfinch and Maple Finance employ a hybrid off-chain KYC + on-chain settlement model, leveraging real-world credit assessment firms (e.g., Blackstone Credit Partners, Van Eck) to score borrowers—resolving on-chain information asymmetry. However, this “centralized endorsement” fundamentally contradicts DeFi’s permissionless ethos. In November 2022, crypto trading firm Orthogonal Trading defaulted on Maple Finance, leaving $36 million or so in non-performing debt—an event exposing the fragility of on-chain credit lending: when borrowers are institutions rather than individuals, their asset allocation and risk management capabilities vary widely, undermining the reliability of “credit scoring”. A deeper tension arises: on-chain credit lending attempts to replicate traditional finance’s credit assessment systems within a decentralized world, yet this path confronts inherent friction between regulatory compliance (GDPR, KYC/AML) and on-chain anonymity. Building effective credit assessment mechanisms while preserving user privacy remains a core long-term challenge.

Cross-chain security constitutes the third major challenge. Aave’s Portal functionality, Morpho’s cross-chain deployment, and Ajna’s multi-chain expansion reflect how leading protocols are extending on-chain lending beyond single chains into multi-chain ecosystems. Yet this expansion exponentially increases complexity and thus security risks. The 2022 Ronin Bridge hack ($625M loss) and Harmony Horizon Bridge attack ($100M loss) revealed how cross-chain bridge vulnerabilities propagate throughout the DeFi ecosystem. When Aave V3 incorporates assets from BNB Chain, Avalanche, and Arbitrum into its lending pools, those assets must be transferred across chains via bridges whose security is often weaker than the underlying chains themselves. More critically, cross-chain assets depend on price oracles: if an oracle on any connected chain malfunctions or lags, positions collateralized by that asset may face untimely liquidation. This “weakest-link effect” means an on-chain lending protocol’s overall security hinges on the most vulnerable chain in its expanded footprint. For investors, evaluating a protocol’s cross-chain expansion strategy and bridge security is a critical dimension for assessing long-term risks.

IV. Innovation Trends: Fixed Rates, RWA, Institutionalization

Despite persistent risks, the on-chain lending innovation engine remains active. Between 2024 and 2026, three forces are reshaping the sector’s rules of engagement. First is the breakthrough in fixed-rate lending. Traditional P2Pool models are inherently floating-rate—interest rates adjust dynamically with pool utilization—exposing borrowers to surging interest costs when market rates spike. Such an uncertainty is unacceptable for enterprises and institutions seeking stable financing. Notional Finance pioneered fixed-term and fixed-rate loans, enabling borrowers to lock in rates for 12 months or longer upon loan creation, while lenders achieve term-matching by purchasing complementary yield tokens (fCash). Pendle Finance took an alternative route—tokenizing yield rights: splitting future asset yields into “Principal Tokens” (PT) and “Yield Tokens” (YT), allowing lenders to purchase PTs for guaranteed returns while transferring rate volatility risk to speculative YT holders. Both approaches jointly advance on-chain interest rate marketization.

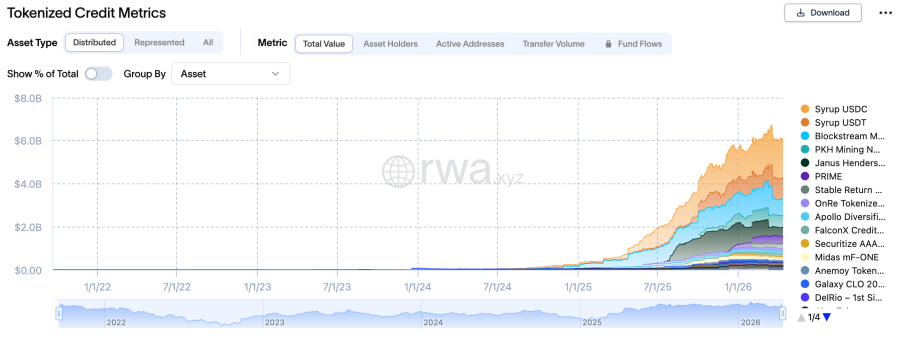

The second force is the explosive growth of RWA lending. In early 2024, BlackRock’s tokenized fund BUIDL surpassed $5 billion, while Ondo Finance’s OUSG (U.S. Treasury yield token) exceeded $1 billion—these compliant assets are now being integrated into on-chain lending protocols as core collateral. Compared to ETH and BTC featuring extreme volatility, U.S. Treasuries offer low volatility, strong liquidity, and regulatory compliance, making them a “green lane” for institutional capital entering on-chain lending. Protocols including Maple Finance, Pendle, and Flux Finance already support borrowing against tokenized U.S. Treasuries, enabling users to unlock liquidity while retaining Treasury yield. Aave’s V4 specifically introduces an “Institutional Market” (Horizon Institutional Market) tailored for RWA assets, providing on-chain lending services to SEC-registered compliant borrowers. As of early 2026, on-chain RWA lending volume has surpassed $18.5 billion and is projected to exceed $50 billion by 2027.

The third force is accelerating institutionalization. Unlike DeFi natives’ preferences for anonymity, permissionlessness, and complex strategies, institutional capital demands compliance, auditability, and risk control. RWA lending platforms such as Centrifuge and RWA.xyz have designed product frameworks explicitly meeting institutional needs: KYC/AML verification, off-chain credit assessment, custodial clearing, and regulatory reporting—transplanting traditional finance’s infrastructure onto-chain. A deeper shift is underway: institutional participation is altering on-chain lending’s strategic dynamics. Traditional DeFi players habitually exploit leverage, flash loans, and arbitrage to extract protocol value, whereas institutional capital favors conservative “hold-lend-rehold” strategies. This divergence will fundamentally reshape lending protocols’ capital structures and yield curves, driving more long-term locked capital, more stable rates, and fewer speculative liquidations. For protocols, balancing institutional service excellence with retail liquidity retention remains a persistent, delicate challenge.

V. Investment Framework: Three Strategic Tracks and Risk Warnings

For investors and practitioners targeting the on-chain lending sector, the current market offers three clear participation tracks. The first is investment extension within the Aave ecosystem. Beyond holding AAVE tokens directly, monitoring Morpho Labs (an independent protocol evolving from Aave’s optimization layer, with Morpho Blue pioneering oracle-free lending), Spark Finance (a stablecoin lending protocol deeply integrated with MakerDAO’s DSR ecosystem, benefiting from DSR’s expansion), and new functionalities enabled by upgraded Aave V4 (e.g., Institutional Market, cross-chain liquidation) offers superior risk-adjusted returns. Historical data shows AAVE tokens consistently generate significant alpha following major Aave version upgrades or record-high TVL milestones.

The second is beta exposure to the RWA lending sector. Ondo Finance (OUSG), Maple Finance (institutional credit), and Centrifuge (physical asset financing) represent three distinct RWA entry points. Ondo’s advantage lies in deep integration with BlackRock’s BUIDL fund and stable yield from compliant U.S. Treasuries; Maple’s strength stems from established credit files with real institutional borrowers (e.g., Coinbase Ventures, Framework Ventures); Centrifuge’s edge resides in genuine physical asset financing demand and low default rates. Investors seeking RWA exposure should adopt diversified allocation strategies to mitigate black-swan risks tied to any single protocol.

The third is structural opportunities in fixed-rate innovation protocols. Pendle Finance and Notional Finance represent two distinct fixed-rate approaches: Pendle achieves “yield separation” through yield-tokenization, catering to advanced users fluent in DeFi Lego logic; Notional delivers “rate locking” via traditional fixed-term loans, better suited for institutions prioritizing stability. Notably, Pendle’s TVL surged tenfold in 2024 from under $100 million to over $1 billion, with its highly volatile YT tokens creating fertile ground for arbitrage and speculative strategies.

While pursuing these opportunities, three risks warrant close attention. First is smart contract risk—lending protocols’ massive TVL makes them high-value targets for hackers. The 2023 Euler Finance hack ($197M loss) serves as a stark reminder that even top-tier protocols may harbor undiscovered vulnerabilities. Second is liquidity concentration risk—if a single collateral type (e.g., stETH, Lido’s staked ETH) comprises an excessive share of a protocol’s TVL, extreme volatility in that asset could trigger systemic liquidations. Third is regulatory policy risk—the “permissionless lending” functionality of on-chain protocols may be classified by regulators as unregistered securities issuance or illegal fundraising, especially under U.S. and EU MiCA frameworks, significantly inflating compliance costs. For portfolio allocation, we recommend capping on-chain lending exposure at 20%-30% of overall DeFi allocations, prioritizing mature protocols with extensive audits, stable TVL, and transparent team backgrounds.

VI. Conclusion: Infrastructure Value and Investment Timing

On-chain lending is the DeFi sector closest to embodying the definition of “infrastructure”. Unlike perpetual futures chasing extreme leverage, liquidity mining dependent on token-incentive-driven artificial booms, or NFT markets facing cyclical asset obsolescence, its value is rooted in authentic financing demand, steady interest income, and gradually built institutional trust. Behind the $64.3 billion TVL lies countless individual and institutional acts of borrowing, depositing, and risk management—the scale effect of this “grassroots finance” represents DeFi’s most fundamental and powerful value proposition. Looking ahead, the on-chain lending investment timing is transitioning from the “proof-of-concept phase” into the “institutional adoption phase”. RWA inflows, institutional market formation, and regulatory framework refinement are collectively transforming this sector from a playground for crypto natives into a new battlefield for traditional finance. During this transition, striking the right balance between “DeFi-native innovation” and “institutional compliance requirements” will determine the rise and fall of individual protocols. For long-term investors, on-chain lending merits strategic allocation: core positions should focus on Aave ecosystem’s foundational assets, satellite positions can moderately capture alpha from RWA and fixed-rate innovations, while maintaining disciplined risk management and healthy respect for smart contract vulnerabilities.