It has been three and a half years since ChatGPT burst onto the scene.

Back then, many people realized for the first time that a dialog box might become the next-generation internet portal. Today, it has long since become the fastest application in human history to reach 1 billion monthly active users. Yet, at the same time, it has reached a symbolic turning point:

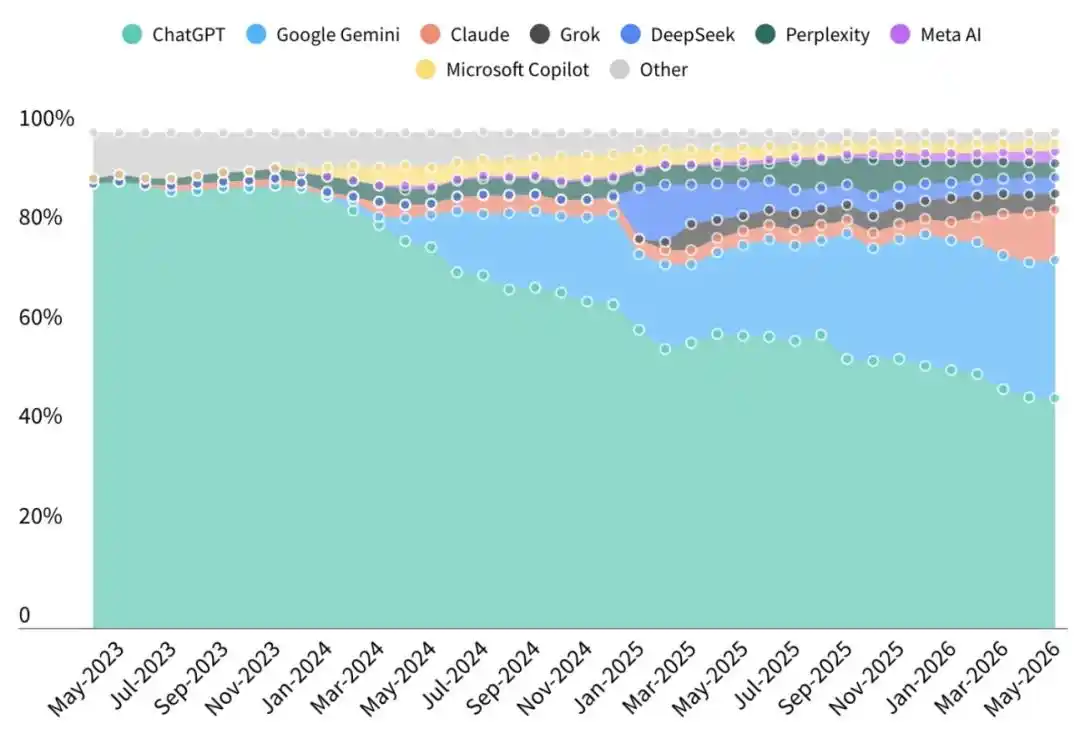

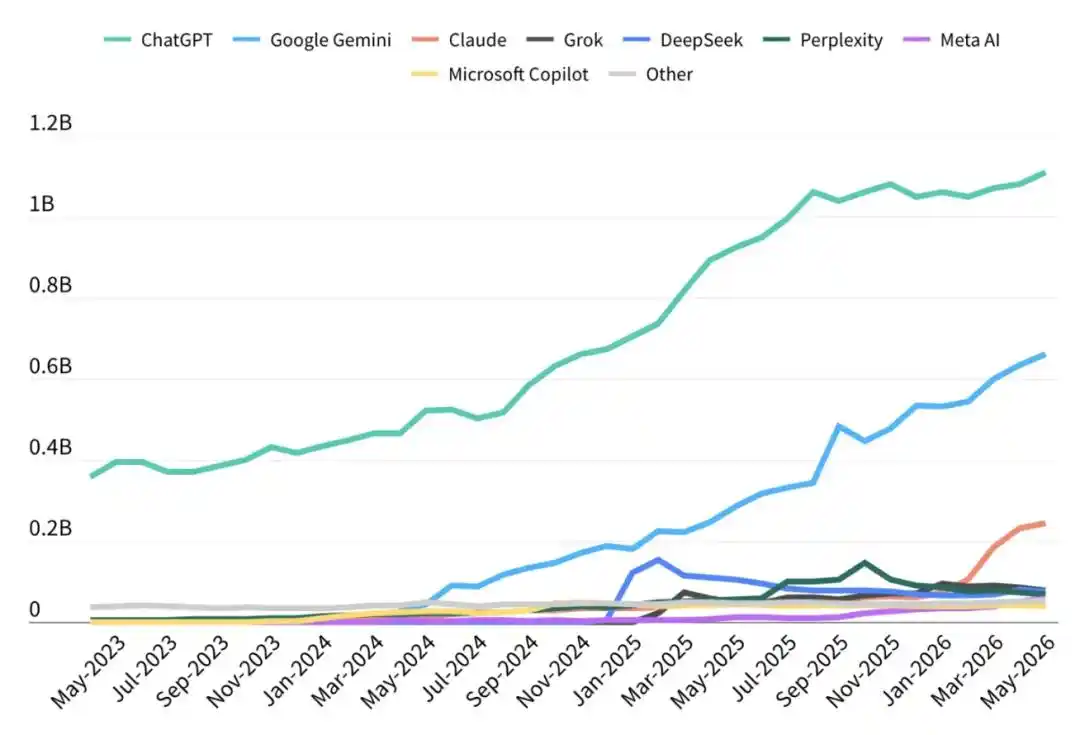

ChatGPT's global market share has dropped below 50% for the first time.

According to the analytics firm Sensor Tower in its "State of AI 2026 Report," as of the end of May this year, ChatGPT's share of the global AI assistant market fell to 46.4%. Prior to January this year, this figure was still above 50%.

ChatGPT remains the world's largest AI assistant. But leading no longer equals monopoly. The AI assistant boom ignited by OpenAI has moved from wonder, trial, and awe into the stage of product comparison, ecosystem lock-in, paid conversion, and commercialization.

Loyalty is a False Promise; Users are 'Players'

In 2023, having a ChatGPT account still carried a certain identity as an AI trendsetter. By 2026, AI assistants are increasingly becoming infrastructure in internet life, much like search, email, and office suites.

The most noteworthy change in Sensor Tower's report is not just that ChatGPT still ranks first. More importantly, users are becoming more willing to migrate. As long as another assistant is more convenient in a specific scenario, users will immediately allocate their time to that other product.

The main rivals pulling ChatGPT's share below 50% are Gemini and Claude.

As of the end of May, Gemini's global share reached 27.7%, and Claude reached 10.3%. Products like Grok, Perplexity, DeepSeek, and Meta AI each remain below 5%, but they are also continuously squeezing the remaining market.

Gemini's growth is not hard to understand.

It stands on the foundation of Google's complete ecosystem. Search, Gmail, Docs, Calendar, and Android are all natural entry points. When AI is embedded into tools users must use daily, many ordinary users don't need to specifically open another webpage to summon ChatGPT.

Especially after the release of Gemini 3.0, Google also achieved its first real major victory, officially joining the AI game table and entering the view of more mainstream users.

Claude's path is more like a victory for productivity tools.

It doesn't have a distribution system like Google's, but it has built a strong reputation in scenarios such as writing, coding, long-text processing, and complex task collaboration. Sensor Tower states that Claude is approaching ChatGPT's user retention levels. For heavy users, AI assistants have shed their toy-like attributes and are starting to genuinely impact work efficiency.

A more subtle change is that users are no longer judging AI products solely based on model capability.

As AI assistants increasingly take on personalized interactive characteristics, users are also beginning to discuss work, emotions, judgments, and decisions with them. Brand trust, value orientation, and institutional relationships may all become part of user choice.

And the slightest bit of negative publicity can trigger a wave of massive uninstalls. This is something OpenAI CEO Sam Altman has likely felt deeply over the past year.

AI companies used to believe that as long as the model was stronger, users would stay. The reality of 2026 is much more complex. Capability, ecosystem, price, scenario, and brand trust are now collectively determining whether an assistant will be used continuously.

The Free Lunch is Over; AI Apps are Starting to Talk Money

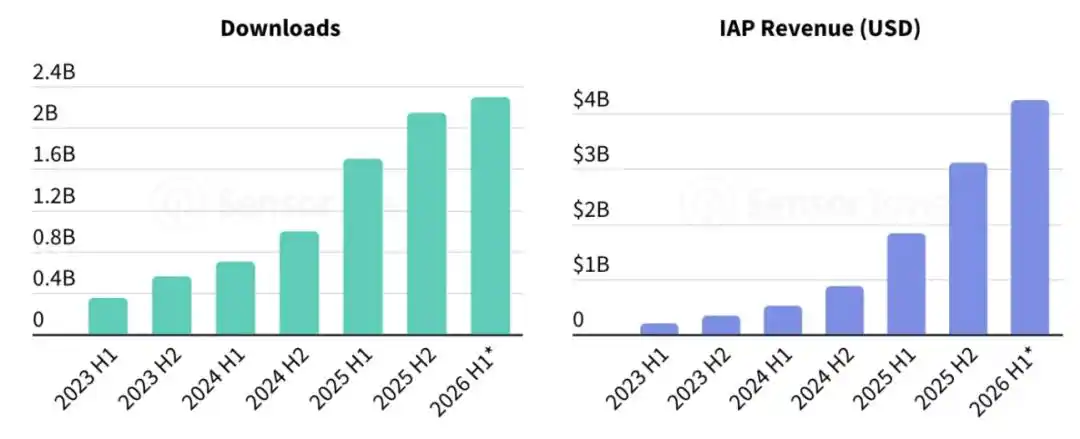

Beyond market share, another set of data from Sensor Tower's report better illustrates the stage change in the industry: AI apps are still growing, but the growth logic has changed.

Sensor Tower estimates that in the first half of 2026, global AI app downloads will approach 2.3 billion, and in-app spending will exceed $4.2 billion. In comparison, AI app in-app spending in the first half of 2025 was $1.83 billion.

Users are still downloading AI apps and are willing to pay for AI.

But the growth rates for both downloads and spending have slowed. Meanwhile, the industry has moved from a period of rapid expansion into a more realistic competitive phase. Companies can no longer just talk about user growth; they must also prove they can turn traffic into revenue.

Regional differences are also beginning to show.

Asia remains the highest market for AI app downloads, but in Q1 2026, it saw its first-ever download decline, dropping by 3.3%, mainly influenced by markets like India.

In contrast, North America and Europe are stronger in in-app consumption. For AI companies, what truly determines the business model is often the ability to pay; installation scale can only solve part of the problem.

The trend in the US market is even more pronounced.

Users are increasingly using AI assistants for productivity tasks and are more willing to pay for advanced features. Claude performs well here. Sensor Tower states that Anthropic has 13% of its users subscribing to paid plans, with a conversion rate among the highest in the industry.

A 13% subscription conversion rate explains why Claude can continue to expand its presence amidst the squeeze from giants. As long as AI helps users save time, write code, organize documents, and handle complex tasks, a subscription fee of twenty or even two hundred dollars per month is actually within an acceptable range.

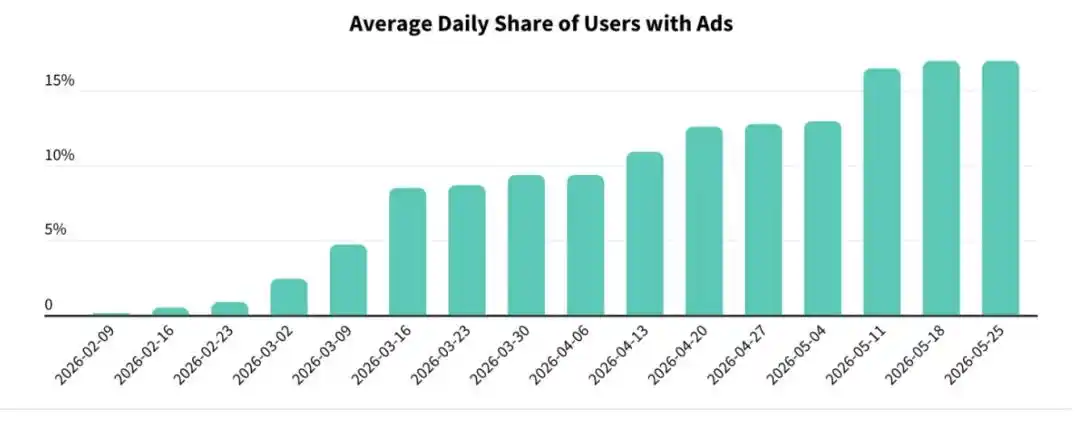

ChatGPT's commercialization path is more diverse and also more controversial. Sensor Tower states that OpenAI began testing ads in ChatGPT starting in February this year, gradually expanding ad display scale and user coverage.

By May, an average of 17% of users saw ads daily. Software and shopping are currently the largest advertiser categories, followed by media & entertainment, and food & beverage.

From subscriptions to ads, ChatGPT is moving towards a more typical internet business model. Early users were familiar with a clean dialog box, a portal imbued with the dream of Artificial General Intelligence (AGI).

Unfortunately, even the smartest AI on the planet ultimately can't escape the fate of becoming a shopping guide. For OpenAI, advertising and shopping have become experiments that must be pursued. Now, this portal is also beginning to carry ads, shopping guides, recommendations, and transaction conversions.

Model inference, training, and compute expenditures are extremely expensive; relying solely on subscription revenue can hardly cover long-term investment. Advertising and shopping are becoming the next pieces of the puzzle for ChatGPT's commercialization.

As AI begins to penetrate core scenarios like shopping, office work, and search, the imagination of AI becoming a unified super portal is also encountering increasingly realistic platform boundaries.

Sensor Tower estimates that in the first half of 2026, global AI app usage time will grow from 17.2 billion hours in the same period last year to approximately 36 billion hours. Among these, the top three AI assistants account for 89% of the total usage time of AI assistant apps.

There is still opportunity for later players, but it exists more in fragmented scenarios, such as AI companions, AI content generation, and vertical industry tools. The main battlefield for general assistants has largely been occupied by ChatGPT, Gemini, and Claude.

Farewell to the Altar; AI Moves Towards the Everyday

The decline in ChatGPT's share occurs at a somewhat paradoxical point in time: OpenAI's revenue is still growing rapidly, its user base is still expanding, and its capital reserves far exceed those of most startups.

According to a report by The Information based on documents disclosed by OpenAI to shareholders, OpenAI's cash consumption reached $3.7 billion in the first quarter, exceeding half of its $5.7 billion revenue. Both cash consumption and revenue roughly tripled year-over-year.

This is also a common challenge facing the current AI industry. Users and revenue continue to grow, yet massive capital investment is required to maintain model training, inference services, and infrastructure construction.

Furthermore, OpenAI expects its cash consumption in 2026 could reach $25 billion, rising further to $57 billion in 2027. Even though OpenAI has secretly submitted IPO filing documents, the listing timing may still be adjusted based on market conditions.

In other words, as one of the world's strongest AI brands, OpenAI still needs to answer a question: when models are getting more expensive, competition is getting fiercer, and users are becoming more willing to migrate, how high a profit margin can ChatGPT's business model ultimately generate.

However, even though ChatGPT's share has fallen below 50%, it remains the world's largest AI assistant and is still the most frequently mentioned name when people talk about AI. But this milestone is symbolic.

The AI assistant market has moved past the era where a single product defined the industry. In the past, ChatGPT was responsible for making the masses believe AI could change the internet. Now, Gemini, Claude, Grok, DeepSeek, and various vertical AI assistants are collectively dividing user time, usage scenarios, and commercial revenue.

User demands are also subtly changing.

By now, you probably are no longer satisfied with just asking AI to write a poem or tell a lame joke. Instead, you're starting to demand it writes code with fewer errors, processes documents more accurately, facilitates office collaboration more conveniently, and offers more reasonable subscription prices.

When a technology no longer elicits repeated amazement but instead begins to be scrutinized, compared, and replaced, it has truly begun to enter mainstream life.

ChatGPT has lost its dominant half of the market, but AI has truly begun to win the world. It's just that in this new world, there are no eternal kings, only us, forever ready to migrate for the sake of a more useful tool.

This article is from the WeChat public account "ifanr," author: ifanr, discovering tomorrow's products.