Written by: KarenZ, Foresight News

A countdown clock is rewriting the UK crypto market.

If a platform helps users buy crypto, facilitates trading, custodies assets, or issues stablecoins in the UK, the core questions it faces next are straightforward: does its business fall under the FCA's new regulatory scope? Does it need to apply for authorization? Can it continue operating during the application review period?

At the end of June 2026, the UK Financial Conduct Authority (FCA) issued a set of crypto asset regulatory policy statements covering stablecoin issuance, custody, trading platforms, intermediaries, staking, lending, market abuse, disclosure, prudential capital, and the applicability of the FCA Handbook.

According to the FCA's Crypto Roadmap, this marks the transition of UK crypto regulation from years of consultation to the final rule-making stage.

From Registration to Authorization

The UK has previously regulated the crypto industry, but its scope was relatively limited. Since January 2020, crypto asset trading service providers and custodian wallet providers operating in the UK have needed to register with the FCA under anti-money laundering regulations; in 2023, financial promotion rules began to apply to crypto asset marketing.

This change goes further. The FCA stated that the UK Parliament passed the *Financial Services and Markets Act 2000 (Cryptoassets) Regulations 2026* on February 4, 2026, bringing a broader range of crypto asset activities into the FCA's regulatory perimeter for the first time. Under the new regime, the full scope of regulated activities will be extended from October 25, 2027.

This regime covers a significant number of entities. The relevant activities listed by the FCA include: issuing qualifying stablecoins, custodying crypto assets, operating qualifying crypto asset trading platforms, trading qualifying crypto assets (as principal or agent), arranging qualifying crypto asset trading services (including crypto lending), arranging qualifying crypto asset staking services, and more.

In other words, regarding crypto-specific regulation, the UK regulator is not targeting just one segment. Issuance, trading, matching, brokerage, custody, staking, lending—if an activity falls within the definitions of the new regime, it will likely need to enter the FCA's authorization system.

The Most Critical Window, Determining Whether Business Can Continue During Review

For crypto companies already operating in the UK market, the period from September 30, 2026, to February 28, 2027, is the most crucial to watch.

The FCA stated that if a firm wishes to rely on the *savings provisions*, which are transitional grandfathering clauses, the application window is planned to open on September 30, 2026, and close on February 28, 2027. Eligible companies that submit applications within this window can continue to carry out specified activities before the FCA makes its decision.

This is not a mere date reminder. It determines whether existing firms can continue operating while awaiting authorization review. Missing the window may cause a company to lose the protection to continue relevant business during the transition period.

The FCA also explicitly stated that existing registrations will not be automatically converted. Firms currently registered under the *Financial Services and Markets Act 2000 (FSMA)* or the *Money Laundering Regulations*, authorized under payment service or electronic money rules, or relying on FSMA s.21 approval for financial promotions—if their business falls within the scope of the new regulated crypto asset activities—will still need to obtain the corresponding authorization.

This will force many companies to re-evaluate their business boundaries. Models that were sufficient under anti-money laundering registration or financial promotion rules may no longer suffice under the new regime. Companies must first determine if they fall within the regulatory scope, then prepare authorization applications, capital arrangements, risk control systems, and client asset protection mechanisms.

Beyond Authorization: Capital and Risk Control Thresholds

Obtaining authorization is not the only challenge. This time, the FCA has broken down many compliance requirements that were previously easily relegated to slogans into more concrete rules.

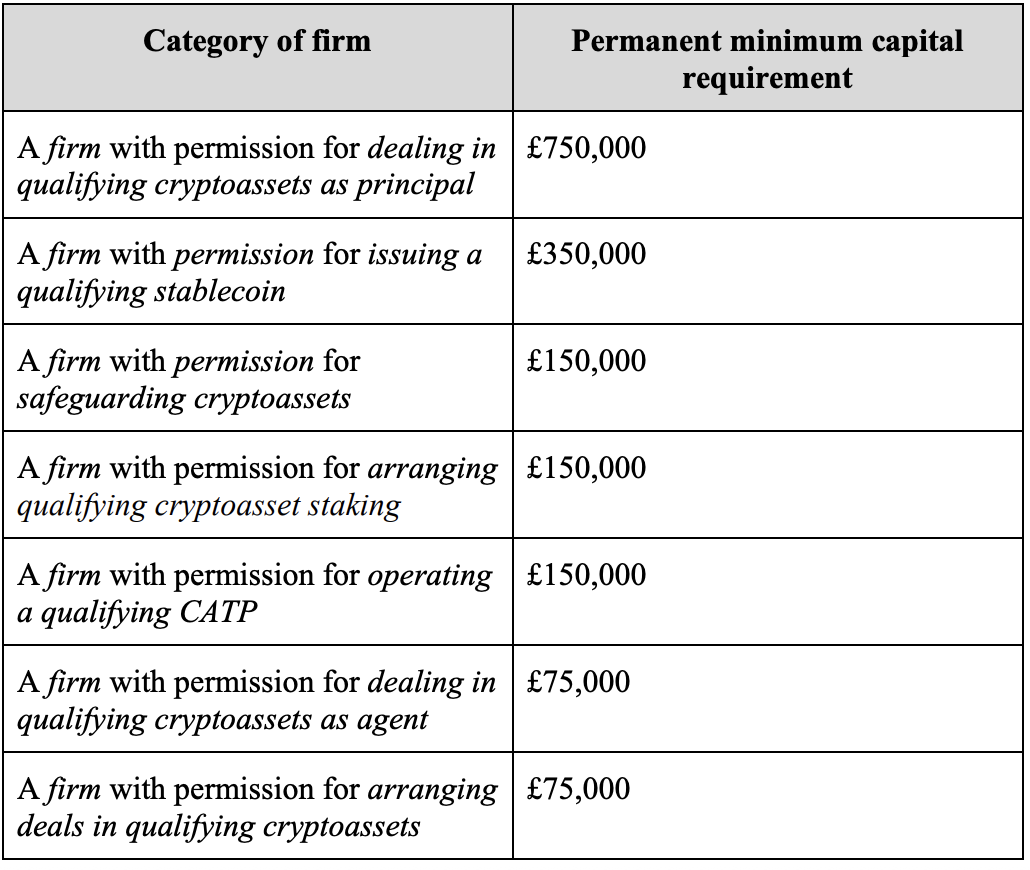

Regarding prudential capital, PS26/12 sets out the permanent minimum capital requirements for different businesses. Firms trading qualifying crypto assets as principal: £750,000; issuing qualifying stablecoins: £350,000; custodying crypto assets, providing qualifying crypto asset staking services, operating qualifying crypto asset trading platforms: £150,000; trading as agent and arranging trades: £75,000.

These figures may not seem high, but they are just the baseline. The FCA explained that a firm's minimum own funds requirement is the highest of three values: the permanent minimum capital requirement, the fixed overheads requirement, and the K-factor requirement. The permanent minimum capital is the baseline, while the K-factor is further calculated based on the scale of business activities and risk exposure. The FCA also emphasized that the permanent minimum capital is an authorization threshold; firms cannot obtain authorization first and then gradually meet the requirement in phases afterwards.

The FCA has also introduced a basic liquid asset requirement. Relevant firms must hold core liquid assets amounting to one-third of the fixed overheads requirement plus 1.6% of the total value of client guarantees. The purpose of this liquidity buffer is pragmatic: firms cannot meet capital requirements only on paper; they must also have sufficient liquid assets to support operations, orderly wind-down, or handling client-related obligations under stress scenarios.

Trading platforms and intermediaries also face more detailed market conduct rules. In its press release, the FCA stated that the new framework will introduce market integrity rules covering areas like insider trading and market manipulation; in the regime overview, the FCA also included trading platforms and intermediaries within the scope of activity rules in PS26/11, specifically mentioning requirements such as best execution and price checks across multiple execution venues. PS26/11 further stipulates that relevant firms need to establish client order handling procedures to ensure client orders are executed promptly, fairly, and expeditiously, and to reference prices from at least 3 reliable UK authorized execution venues for price checks where possible.

If there are fewer than 3 UK authorized venues where the order can be executed, existing available venues should be checked. The FCA simultaneously emphasized that this is not a mechanical price comparison for each trade, nor does it require orders to be executed only at the 3 venues checked. It requires firms to use reliable price sources to validate their execution policies and be able to demonstrate that the execution outcomes delivered to clients are at least as good as those that would have been achieved in comparable circumstances at these UK authorized venues.

The focus for custody businesses is client asset protection. In PS26/11, the FCA confirmed that CASS 17 protection requirements will apply to client crypto assets, with rule focuses including ownership, record keeping, asset reconciliation, and private key management. In short, platforms cannot merely state that "assets are transparent on-chain"; they must also prove they know which assets belong to which clients, whether their ledgers match on-chain assets, and that private key control will not be compromised due to internal processes or external attacks.

The FCA's cost-benefit analysis provides a more tangible figure: it estimates that custody protection rules could prevent approximately £60 million in consumer losses annually.

Lending and staking are also brought into a more detailed consumer protection framework. For crypto lending, the FCA retains core protection requirements for retail clients, including enhanced disclosure, client consent, appropriateness tests, record keeping, over-collateralization, and negative balance protection. Negative balance protection means that a retail client's losses in a crypto borrowing arrangement should not exceed the market value of the collateral they have specifically provided for that borrowing.

For staking services, the FCA retains requirements for disclosure, contract terms, client consent, and record keeping, but makes adjustments for automatic staking arrangements, allowing clients to consent to ongoing staking covering current and future holdings, provided relevant conditions are met and annual notifications are given.

Stablecoins Placed Beside Payment Ambitions

Stablecoins are a category of activity treated separately within this regulatory framework.

The FCA stated that qualifying stablecoins issued in the UK will be required to be fully backed and redeemable at par value, to support their use as "money-like instruments."

The core of PS26/10 is to require stablecoin issuers to establish an auditable mechanism around backing assets, redemption, disclosure, and asset protection. The FCA's final rules require UK stablecoin issuers to provide full backing for their stablecoins from the moment they are minted, including tokens held by the issuer itself; tokens that have been permanently destroyed no longer require backing asset coverage. The FCA's reasoning is direct: stablecoins are liquid, and if unsupported tokens enter the market, it could undermine confidence in their 1:1 peg.

Regarding redemption, the FCA requires UK stablecoin issuers to provide the right to redeem at par value and complete redemptions within a T+1 timeframe. However, the final rules adjust the starting point: T+1 no longer starts from the submission of a complete redemption request, but from when the issuer receives the stablecoins to be redeemed into its wallet. This allows AML/KYC checks to be completed before T+1, avoiding squeezing anti-money laundering reviews into the redemption timeline.

Regarding backing assets, the FCA divides stablecoin reserves into two tiers: core backing assets and expanded backing assets.

Core backing assets include demand deposits and short-term government debt instruments; expanded backing assets include longer-term government debt instruments, shares in public debt CNAV money market funds, and repo or reverse repo arrangements with government debt instruments as the underlying and a maturity not exceeding 7 days.

The FCA sets two liquidity requirements: First, issuers must meet the On-demand Deposit Requirement (ODDR), meaning they must hold at least 5% of the backing asset pool as demand deposits. Second, issuers must also meet the Core Backing Asset Requirement (CBAR), meaning they must hold an additional percentage of core backing assets, with the percentage being the higher of 5% and the highest single-day redemption ratio over the past 180 redemption days. Demand deposits used to meet the ODDR cannot also be used to meet the CBAR.

The focus of this design is to prevent issuers from allocating more to long-term or complex assets for yield, yet being unable to provide sufficient high-liquidity assets during concentrated user redemptions.

Beyond this, there is a larger regulatory division of labor. The FCA and the Bank of England issued a joint statement on the same day explaining the regulatory pathway for systemic stablecoin issuers. "General UK stablecoin issuers" are regulated by the FCA; if a UK stablecoin issuer is designated by HM Treasury as having "systemic importance," it may transition from sole FCA regulation to joint regulation by the FCA and the Bank of England.

PS26/10 also mentions that in the Bank of England's draft rules, the backing asset composition for systemic stablecoins may shift to a maximum of 70% UK sovereign debt with a remaining maturity of less than 6 months, and a minimum of 30% central bank deposits; individual stablecoins may also be subject to a provisional issuance cap of £40 billion and required to offer T+0 redemption.

This indicates that the UK does not view stablecoins solely as exchange-denominated tools. As long as they continue to approach payment and settlement scenarios, regulatory focus will expand from investment risk to reserve safety, redemption stability, and financial infrastructure reliability.

Summary

The FCA still cautions that the vast majority of crypto assets are highly speculative, and consumers may lose all their principal. The new rules do not eliminate such risks, nor do they endorse crypto assets. What they change is another matter: the UK is beginning to address crypto business using more comprehensive financial regulatory language.

Under the new framework, crypto-related companies must also demonstrate whether capital is sufficient, how client assets are protected, whether trade execution is fair, if stablecoins can be redeemed according to rules, and who is responsible if risks get out of control.

By October 25, 2027, when the countdown ends, those that truly remain will be the companies that can clearly articulate their business boundaries, client assets, capital buffers, and risk responsibilities.