Every Monday, Wednesday, and Friday, we focus on the crypto market, Japan, South Korea, A-shares, and Hong Kong stocks, reviewing the market with data and seizing opportunities through trends. Presented by PANews.

BTC Tests 200-week Moving Average After Days of Rebound

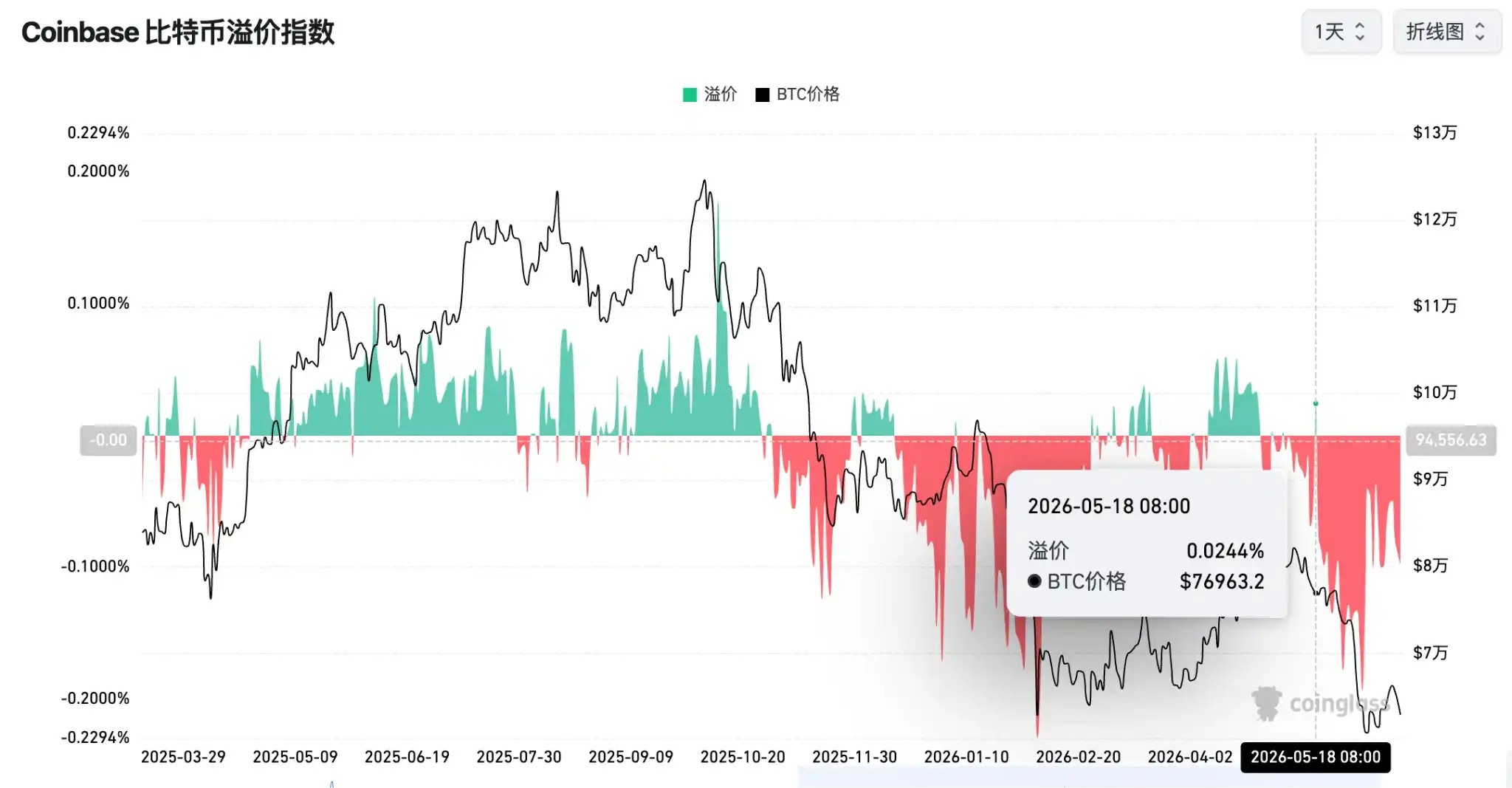

Bitcoin has entered a period of consolidation and repair after rebounding over 11%, with market sentiment easing from extreme panic but still facing tests of support. The Coinbase Bitcoin Premium Index has been in negative premium for 50 consecutive days, setting a record for the longest duration, reflecting significant selling pressure in the U.S. market and an overall risk appetite that has not fully recovered. Market maker Wintermute noted that this rebound is more of a "textbook repair" driven by macro easing, a dovish Fed tone, and institutional adoption benefits for Ethereum, rather than a structural shift. Short-term prices may rise slightly, but continued capital inflows are needed to confirm the trend.

On-chain data also fails to give a clear optimistic signal. A CryptoQuant analyst indicated that the Bitcoin NUPL indicator remains at 0.158. Although close to levels seen in early 2023, the 30-day and 100-day EMAs have not yet entered the negative territory typical of historical bear market bottoms, suggesting there may be further downside risks in this cycle. The Galaxy research team believes Bitcoin is gradually entering a value zone with limited downside, but prices could still fall back to the $40,000-$46,000 range if global liquidity tightens.

From a technical perspective, several traders are watching the support level near $63,000. If it holds steadily, there is potential to challenge the resistance zone around $64,600 to $65,000 again. If it falls below $63,000, the market may retest support near $60,000 or even $58,000. Short-term movements will remain highly dependent on capital flows and macro policy changes.

Looking ahead, Federal Reserve policy will be the core variable affecting the trend of digital assets. The market will focus on the latest meeting minutes, the U.S. Dollar Index, Treasury yields, and ETF fund flow changes. If institutional funds resume net inflows and U.S. market risk appetite improves, Bitcoin may continue its challenge towards $65,000 or higher. Conversely, the $63,000 support level will face a test.

Key Points Today:

-

Bitcoin L2 network Botanix will gradually shut down, users need to withdraw assets by July 9.

-

Base will activate the B20 token standard on the mainnet on July 9.

-

Movement (MOVE) will unlock approximately 165 million tokens worth about $2 million on July 9.

-

Upbit 24-hour trading volume ranking: XRP, SLX, BTC, ETH, AI.

-

Bitcoin Spot ETF: +$21.435 million, net inflows for 3 consecutive days.

-

Ethereum Spot ETF: +$26.9252 million, net inflows for 4 consecutive days.

-

HYPE Spot ETF: +$4.3227 million.

-

SOL Spot ETF: +$1.6720 million.

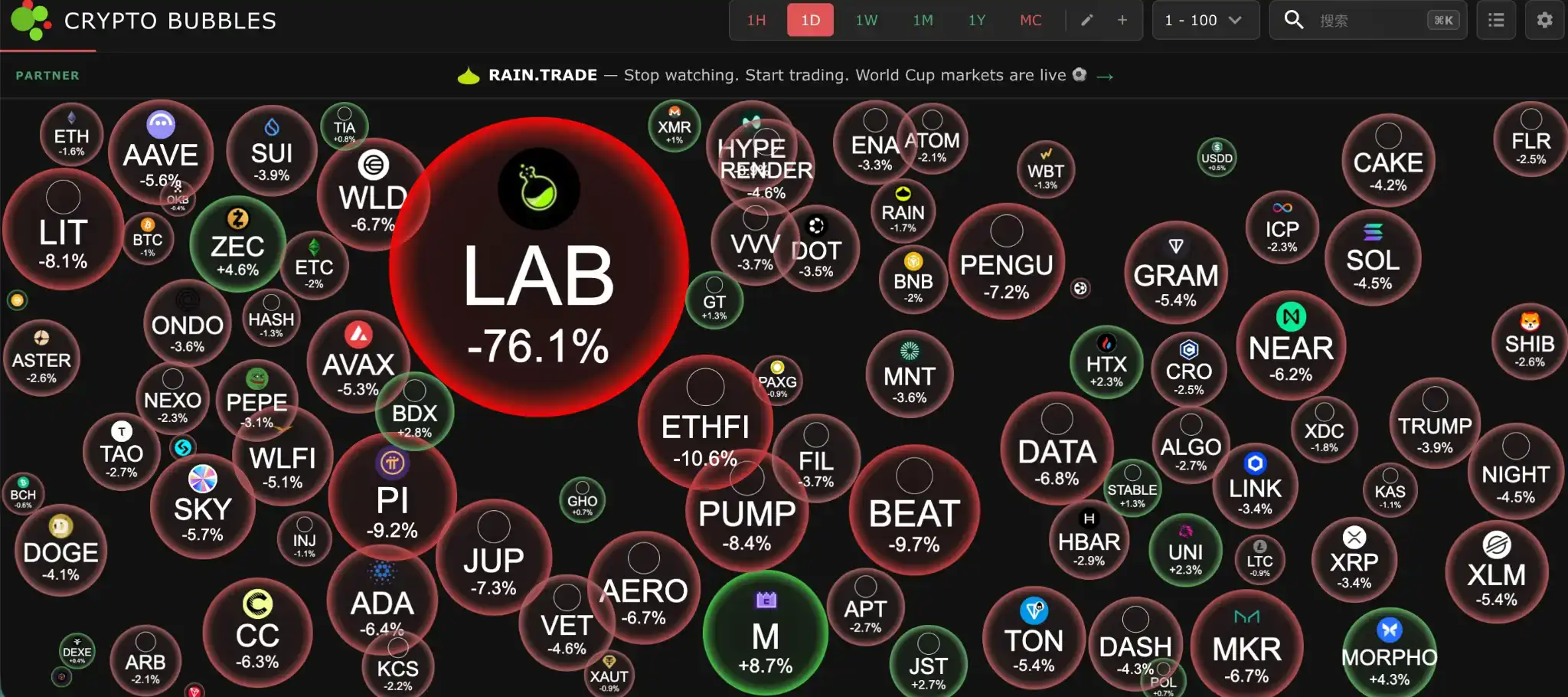

Today's Biggest Gainers among Top 100 Cryptos by Market Cap: M up 8.7%, ZEC up 4.6%, MORPH up 4.3%, BDX up 2.8%, JST up 2.7%.

Nikkei Technically Pressured, Falls for 3 Consecutive Days

Following a sharp overnight decline in the Nasdaq, the Tokyo Stock Exchange came under pressure today. The Nikkei 225 index experienced intense volatility throughout the day, ultimately closing down 2.11%, marking its third consecutive day of decline. Tech stocks led the losses, dragged down by U.S. chip stocks and in resonance with the South Korean market.

Worsening Middle East tensions have pushed up energy costs. Japan's reliance on crude oil from the Strait of Hormuz is as high as 93.5%, sparking fears of imported inflation that directly impacts corporate profits. High-valuation tech stocks suffered heavy blows: semiconductor giant Tokyo Electron fell 3.7%, capacitor maker Taiyo Yuden, a key supplier for AI servers, plummeted 8.5%, and Advantest dropped 4.7%, indicating market doubts about the sustainability of the semiconductor boom cycle.

Japan's macro-financial environment has entered a danger zone. The yield on 10-year government bonds rose to 2.86%, a 30-year high, while the 30-year bond yield exceeded 3.98%. A Daiwa Securities strategist pointed out that investor confidence in the AI sector has not recovered, and a Goldman Sachs economist warned Japan could fall into a vicious cycle of debt and high-interest payments. The market is highly focused on the potential for "fiscal dominance" by the Bank of Japan under fiscal pressure. The next 48 hours require close attention to U.S. wholesale inventory data and the Fed meeting minutes for guidance on global liquidity.

Chip Stock Volatility Drags Market, South Korean Stocks Fall into Technical Bear Market

South Korean stocks were among the most volatile markets in Asia. Affected by adjustments in the global AI industry chain, foreign capital profit-taking, and concentrated deleveraging, it closed down 5.35%. The index has now plunged more than 20% from its late-June all-time high, technically confirming entry into a technical bear market. The Ministry of Finance urgently stated it will closely monitor risks with the central bank and regulators, naming chip stock concentration as the main cause of market instability.

The previously profitable chip giants became the main source of market bleeding. Samsung Electronics shares plunged 6.25%, and SK Hynix fell 5.68%. Over-concentration in the semiconductor sector amplified volatility, with leveraged ETFs acting as volatility amplifiers. A South Korean economist publicly criticized that KOSPI has gradually become a "casino," and leveraged ETFs linked to single stocks are a policy failure, not only amplifying market fluctuations but also eroding corporate value and investor wealth.

IBK Investment & Securities researcher Byun Jun-ho noted that semiconductor stock prices are undergoing violent corrections following the inflection point of slowing earnings growth, and a peak in investment sentiment is an undeniable fact. A Fidelity International portfolio manager cautioned that the AI semiconductor boom entirely depends on annual capital expenditures of around $1 trillion by a few tech giants. Once this scale is proven unsustainable, the downside could be unimaginable.

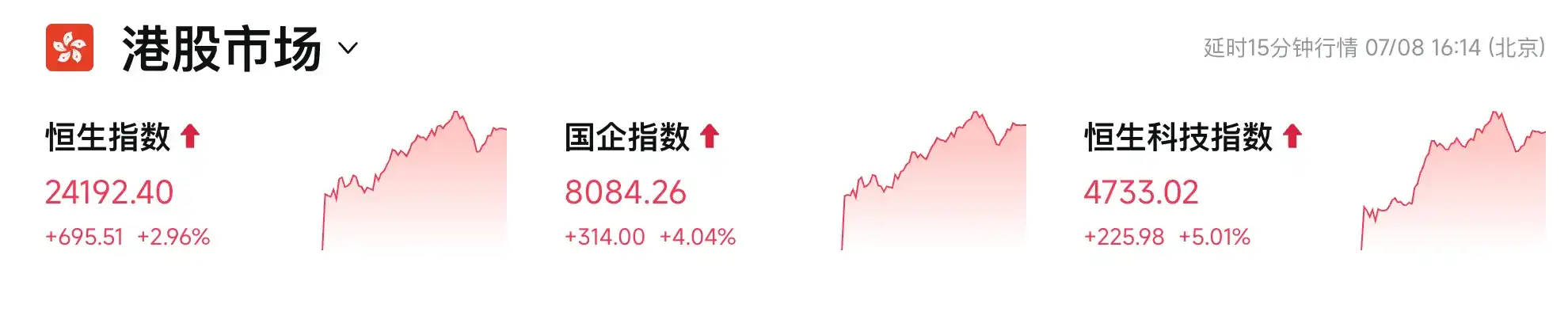

A-shares Consolidate and Pull Back, Hong Kong Tech Leads Strongly

A-shares showed a consolidating and declining trend on Wednesday, with the Shanghai Composite Index down 0.49%, the Shenzhen Component Index down 1.87%, and the ChiNext Index down 1.7%.

More stocks fell than rose. Computing power, AI server, and cloud computing sectors bucked the trend and surged, with stocks like Inspur Information, Sangfor Technologies, Wangsu Science & Technology, and Yunsail Zhilian hitting the daily limit-up. Sectors like lithium batteries, lab-grown diamonds, and humanoid robots saw noticeable adjustments.

The semiconductor self-reliance theme saw a full-scale counterattack. CanSemi hit the limit-up, while Huahong Grace surged over 10% to a record high, driven by international investment banks raising target prices.

Hong Kong stocks, however, opened higher and rallied strongly. The Hang Seng Index rose about 700 points, reclaiming the 24,000 level, with the Hang Seng Tech Index surging over 5% and tech and internet stocks soaring across the board.

-

Alibaba surged over 12%, with its market cap returning to HK$2 trillion, leading the market. Reports suggest Taobao Flash Sales' losses are narrowing faster than expected, and Agent product integration is progressing.

-

Xiaomi Group's stock skyrocketed over 10%, returning above HK$25. The company officially announced the launch of a new car brand "SkyNomad," with its first model set for release in the second half of the year.

-

At the sensitive moment of the first batch of cornerstone lock-up shares being lifted for Zhipu AI, instead of the usual sell-off, nearly 70% of national-level strategic capital and local government guidance funds pledged long-term holdings with strong backing. J.P. Morgan ruthlessly raised its target price to HK$2,000,刺激其股价盘中逆势暴涨18% (stimulating its stock price to surge 18% against the trend intraday).

-

SMIC, Lenovo, Kuaishou, and other chip and tech stocks rose broadly.

Southbound capital recorded a net purchase of over HK$11 billion, indicating funds flowing from South Korea and Japan to Hong Kong stocks' "import substitution" and low-valuation AI assets. Institutional views suggest a resonance between Hong Kong stocks' valuation attractiveness and fund rebalancing, with short-term catalysts including Fed minutes and Chinese macro data.

In the next day or two, focus on China's June CPI/PPI data. The central bank and market participants expect policy implementation in the third quarter to improve liquidity, making tech and consumption recovery worth tracking closely. Overall, the market is seeking a new balance amid global volatility, with Hong Kong's resilience likely to persist.