Original|Odaily Planet Daily (@OdailyChina)

Author|Wenser(@wenser 2010)

Over the past decade, Bitcoin mining companies were once the most stable foundation of PoW networks and the cost anchor of the BTC "Tier 0 market." But now, these industry cornerstones are collectively pivoting, either actively or passively, towards AI.

On the surface, the direct incentive for mining companies to transform is the continuous increase in mining difficulty and the compression of profit margins by a sluggish market; but the deeper driving force is the extreme pursuit of the AI narrative by capital markets—and mining companies happen to possess the most easily convertible real-world assets: electricity, land, cooling systems, data centers, and ready-made data infrastructure, which can be exchanged for AI computing power contracts worth tens of billions of dollars.

Amid the clamor of multi-model competition, mining companies standing at the intersection of energy, electricity, computing power, and crypto assets are undergoing an unprecedented yet almost inevitable industry migration.

Some are steady and watchful, some are forced to turn and go all-in, but one thing is certain: the wind has risen—this is a structural shift blowing from the crypto market towards the AI world.

A Hard Battle That Must Be Fought, and a Cake Too Tempting to Refuse

Entering 2026, for mining companies, the real pressure has never come solely from price fluctuations, but from structural squeeze: difficulty continues to rise, unit revenue continues to fall, and operating costs continue to increase.

In the Winter: Selling Coins to Survive and Bankruptcy Liquidation

On February 20, Bitcoin mining difficulty once increased by 15% to 144.4T, the largest increase since 2021. During the same period, the network hash rate recovered from 826 EH/s to 1 ZH/s, but the hashprice fell to a multi-year low of only about $23.9/PH/s. With the profit compression brought by the 2024 halving continuing, mining companies were forced into a cash flow defense mode.

The most symbolic event came from Bitdeer. On February 20, it disclosed that its own BTC holdings had dropped to 0, with production and sales exactly equal that week. Although founder Jihan Wu later explained that "being 0 now does not mean being 0 in the future," the market still saw it as a microcosm of the pressure on mining companies.

The困境 is not limited to one company. In early February, NFN8 Group filed for Chapter 11 bankruptcy protection in Texas, USA, planning to sell all its assets. Documents showed that a core mine fire, the burden of leases from sale-leaseback models, and the cliff-like drop in hashprice after the halving directly crushed its cash flow. Despite owning multiple mining facilities, NFN8's own assets of 5000 mining rigs were valued at less than $50,000, while liabilities reached the million-dollar range.

As the environment continued to deteriorate, mining companies' reaction was unusually consistent—marching towards AI.

Second Spring: Astonishing Profits Behind AI/HPC Mega Orders

For AI giants, computing power data centers are always scarce: traditional construction cycles take 3-5 years, with high costs for land, electricity, and cooling. Mining companies already have power contracts, infrastructure, and operational experience, making them the most realistic承接方 in the AI expansion cycle.

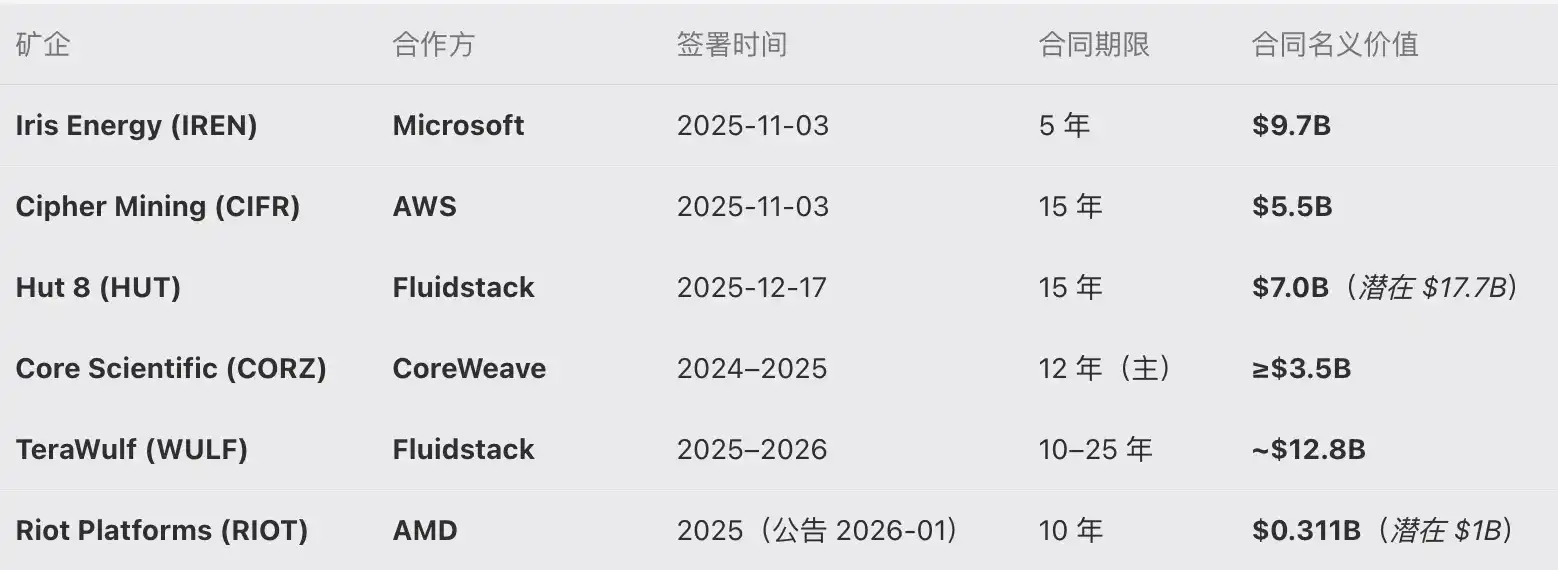

Since last year, mining companies have seen a集中爆发 of orders. According to public data statistics, as of the time of writing, 6 mining companies including IREN, CIFR, HUT have accumulated AI/HPC orders worth approximately $38.5 billion. Among them, TeraWulf's $12.8 billion order contract with Fluidstack and IREN's 5-year $9.7 billion contract with Microsoft are惊人数据, and have also become important supports for their stock prices. From financial reports, the proportion of AI/HPC revenue for many mining companies has increased from less than 15% to 40%-60%.

If mining is a cyclical business, AI is like a long-term cash flow pipeline.

Earnings Consensus: AI Becomes the Keyword

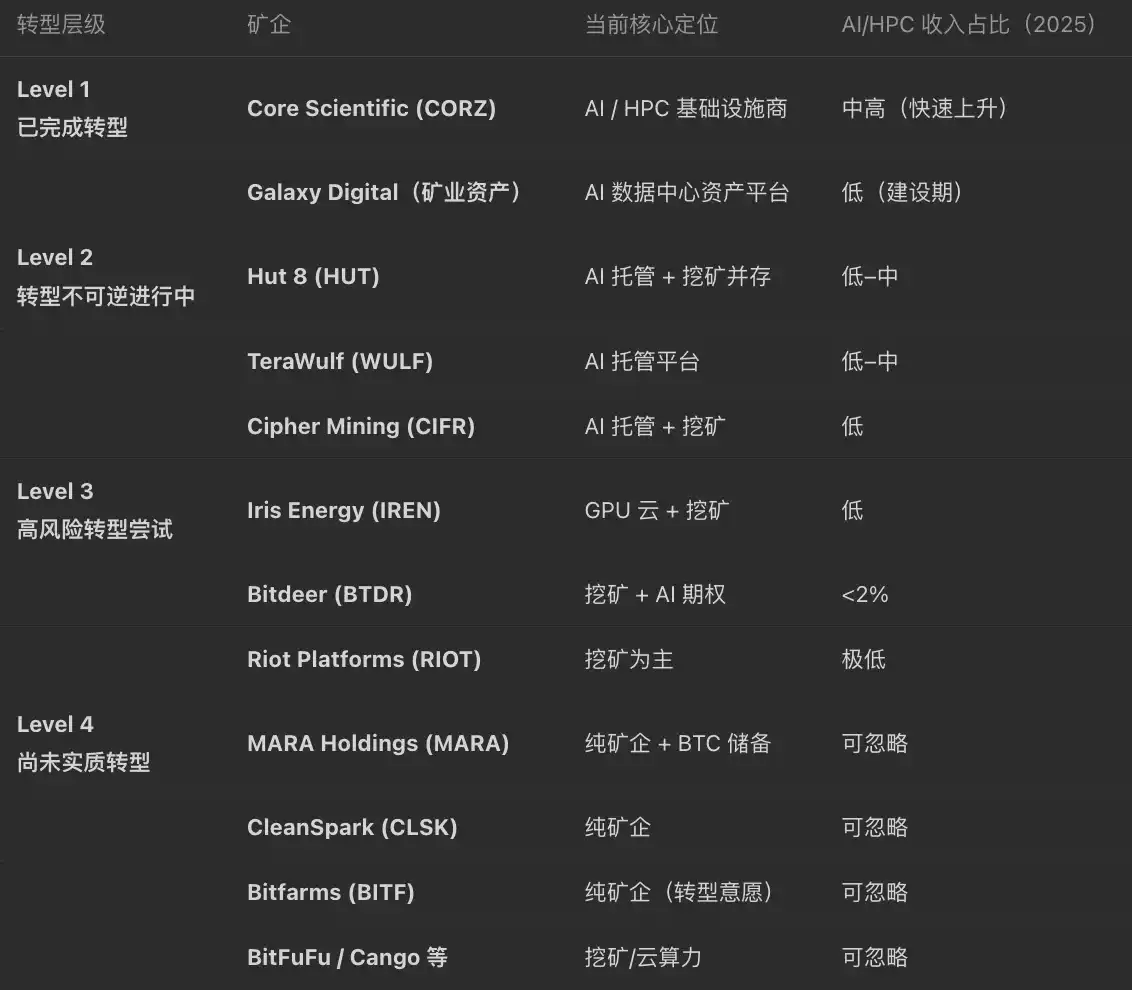

The Q1 2026 earnings season almost gave a unanimous signal: mining companies are systematically transforming.

"HPC Contract Giant" WULF: Holds Over $12.8 Billion in Contracts

Mining company TeraWulf's full-year 2025 revenue reached $168.5 million, a year-on-year increase of 20.3%, of which $16.9 million came from the newly launched high-performance computing (HPC) leasing business.

TeraWulf currently holds over $12.8 billion in HPC contracts, with 522MW of capacity already signed, and has obtained $6.5 billion in financing to support data center expansion.

"AI Mining Giant in the Making" IREN: Holds Microsoft's $9.7 Billion Order

Thanks to previous huge orders and rapid transformation, IREN has隐隐 become a new generation of "AI mining giant in the making".

According to the financial report of mining company Iris Energy (IREN), as of January 31, 2026, it held $2.8 billion in cash and cash equivalents. So far this fiscal year, it has obtained over $9.2 billion in funds through customer prepayments, convertible bonds, GPU leasing, and GPU financing. Subsequent plans include adding 140,000 GPUs, expecting to achieve $3.4 billion in annual recurring revenue by the end of 2026.

"Trump's" HUT: Holds $7 Billion in Orders

Mining company Hut8's 2025 fiscal year generated $9.6 million in revenue from hosting services, holding approximately $1.4 billion in cash and Bitcoin reserves.

In addition, Hut8's spun-off mining subsidiary American Bitcoin (ABTC) achieved full-year 2025 revenue of $185.2 million, deployed approximately 25 EH/s of computing power and owns about 78,000 ASIC miners. Furthermore, its BTC reserves have exceeded 6,000 coins.

The company is also a major crypto mining company supported by the Trump family, thus receiving high market attention.

"Brand Transformation Completed" CIFR: Holds $5.5 Billion in Orders

Mining company Cipher Digital disclosed in its 2025 fiscal year performance report that it officially changed its name from "Cipher Mining" to "Cipher Digital" to complete its brand transformation.

Last November, CIFR reached a leasing agreement with Amazon Web Services worth up to $5.5 billion; additionally, it exchanged 5.4% equity for Google's agreement to provide a guarantee for the $1.4 billion contract signed with Fluidstack.

"Selling Coins to Buy Land and Build Data Centers" RIOT: Reaches Leasing Cooperation with AMD

Mining company Riot Platforms announced its full-year 2025 performance, with annual revenue reaching $647.4 million, a significant increase from $376.7 million in 2024; its Bitcoin holdings exceed 18,000 coins.

In January of this year, RIOT sold 1080 Bitcoins and used the proceeds (approximately $96 million) to purchase the Rockdale plot to develop a data center project. Additionally, the company signed a data center leasing and service agreement with AMD, which will deploy 25 megawatts of critical IT load capacity at the Rockdale campus. The aggressive investment firm Starboard Value stated that Riot's potential valuation from transitioning towards AI and HPC could be as high as $21 billion.

"BTC Stalwart" MARA: Partners with Capital Institutions to Layout AI Data Centers

MARA's financial report data shows that affected by the average Bitcoin mining price dropping about 14%, MARA's Q4 2025 revenue was $202.3 million, a year-on-year decrease of about 6%. At the end of February, MARA announced a cooperation with investment institution Starwood Capital Group to build large-scale data centers for artificial intelligence and cloud computing customers on the basis of existing mines in the United States. After the news was announced, its stock price rose about 17% in after-hours trading.

It is worth mentioning that unlike other mining companies firmly transitioning to the AI field, MARA's management emphasized that although short-term price trends are uncertain, its long-term confidence in the Bitcoin asset class has not changed, Bitcoin will still be the long-term strategic core.

"Data Center Revenue Soars" CORZ: Holds CoreWeave's Over $10 Billion Order

Core Scientific (CORZ) announced its Q4 2025 financial report. Total revenue for Q4 2025 was $79.8 million, down from $94.9 million in the same period last year. Among them, Bitcoin mining revenue dropped to $42.2 million; data center hosting service revenue大幅增长 to $31.3 million, higher than $8.5 million in 2024. Q4 gross profit rose to $20.8 million, higher than $4.8 million in the same period in 2024.

Core Scientific CEO Adam Sullivan said that the company's existing construction projects are more than half completed and are expanding the hosting platform to a 1.5 gigawatt leasable capacity pipeline. Last October, AI company CoreWeave planned to acquire CoreScientific for about $9 billion, but ultimately failed due to lack of shareholder approval; in January this year, CoreScientific sold 1900 BTC (approximately $175 million) for business transformation.

The company estimates that AI business will drive revenue compound growth of 60.9% from 2026 to 2028, reaching $1.5 billion by 2028.

Other Mining Company Representatives: Bitfarms Renames, BitDigital Switches to ETH Camp

In February, Bitfarms (BITF) announced that it would move its headquarters from Canada to the United States and plans to change its name to Keel Infrastructure (pending shareholder, exchange, and court approval), accelerating its transformation into infrastructure. Previously, the company had converted $300 million in debt financing into project financing in October last year for the construction of a data center in Pennsylvania, and sold the Paso mine for $30 million in January this year, officially exiting the Latin American market.

On the other hand, BitDigital's turn was more thorough. As early as last July when the DAT (Odaily Note: Digital Asset Treasury company)热潮兴起, it率先 announced switching from BTC to ETH treasury listed companies; in January this year, it further clarified that it would completely stop Bitcoin mining and instead increase its focus on Ethereum infrastructure, staking, and HPC/AI strategy, marking the official completion of the阵营切换 for this mining company that has been deeply involved in mining for five years. Currently, its AI subsidiary WhiteFiber has completed an IPO, and BitDigital holds approximately 27 million shares, worth over $457 million at the current market value.

In addition to the above two, Galaxy, Bitdeer, Cleanspark, Cango Cango, etc. are still in the stage of promoting AI transformation, and the proportion of revenue contribution remains to be increased. Among them, Cango Cango completed a $10.5 million equity financing in February this year and received an additional $65 million investment commitment, which may accelerate the layout of AI/HPC data center business.

The following is a brief comparison based on public information for reference.

Capital Attitude: Choosing Winners, Not Narratives

The market does not fully accept the "AI transformation," but is quickly differentiating.

In early February, JPMorgan pointed out in a report that Bitcoin mining companies performed strongly at the beginning of the year, mainly driven by the phased缓解 of network competition and the升温 of the HPC narrative. At that time, the total market value of the 14 US-listed mining companies and data center operators it tracked rose to about $60 billion at the end of January, a month-on-month increase of 23%, far exceeding the S&P 500's同期约 1% gain.

But soon, with the密集发布 of a new round of AI models and the impact of OpenClaw on the valuation system of software stocks, market sentiment quickly turned. Capital began to worry about the structural disruption brought by AI, and the stock prices of mining companies related to AI infrastructure随之回调, with CIFR, IREN, and Hut8's intraday declines once exceeding 10%.

On February 10, Morgan Stanley released a research report, giving CIFR and WULF an overweight rating, while downgrading MARA to underweight.

By the end of February, with order fulfillment and stock price recovery, the market wind reversed again. Some analysts believe that against the background of high short-selling ratios by hedge funds, coupled with mining companies locking in long-term low-cost power contracts, their strategic value is no longer limited to traditional mining, but is closer to that of AI infrastructure suppliers.

With order fulfillment and stock price recovery, the market logic has gradually become clear: capital only bets on structural winners.

Therefore, the future of mining companies largely depends on three things:

Execution: Whether the migration of computing power form can be completed quickly;

Resource Endowment: Whether electricity and land have scale advantages;

Narrative Ability: Whether it can be embedded in the upstream supply chain of AI.

In fact, the company's transformation decision is not important; what is more important is capital screening.

The tide has come. Mining companies only have two choices: either migrate with the trend or become history.