After hitting an all-time high of $291 back in January 2025, Solana has begun what has been a year of steady declines. While there have been some relief bounces along the way, the main direction has been downward. At the time of writing, the price of Solana is now sitting more than 71% below its all-time high levels. Other major metrics have also seen significant declines during this time, with Open Interest and Weight Funding Rate falling to two-year lows.

Solana Open Interest And Weighted Funding Rate Reflect The Bear Trend

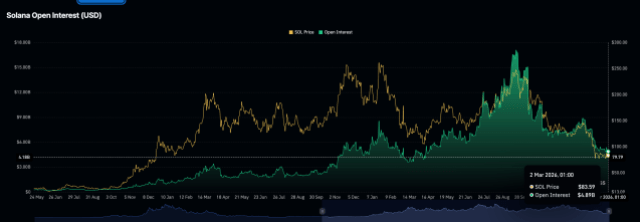

According to data from the Coinglass website, the Solana open interest had actually peaked long after its price hit its peak, which is usually not the case. The open interest topped out at $17.1 billion, nine months after the price hit its all-time high. However, in the five months following the open interest hitting a new high, things have changed drastically.

The website shows that Solana’s open interest has now crashed below $5 billion, sitting at $4.89 billion at the time of writing. Interestingly, the open interest has followed closely with the price decline, and the crash below $100 for the first time since January 2024 has triggered a cascade.

Since open interest measures the open contracts on an asset, it is often a signal of how much attention a coin is getting. With the open interest sitting so low, it suggests that investors are not taking as many bets on Solana as they used to. This is normal in bear markets, when investors are still fearful and wait to see the market improve before jumping back in again.

In the same vein, the weighted funding rate has taken a nosedive. Similar to the open interest, the funding rate had hit a new all-time high back in 2025 before moving downward again, and has now hit its lowest level in more than one year.

The funding rate is essentially what traders pay to hold perpetual positions, with long traders paying short traders when the rates are positive and short traders paying long traders when the rates are negative. Simply put, the funding rate can encourage traders to open positions in different directions in favor of not paying fees.

Currently, the Solana weighted funding rate is fluctuating between positive and negative. However, it has been mostly negative with the decline in price. This means that currently, short traders are paying to keep their positions open.