Blockchain activity is rising across major networks, but the latest data highlights a widening gap in how that activity is defined.

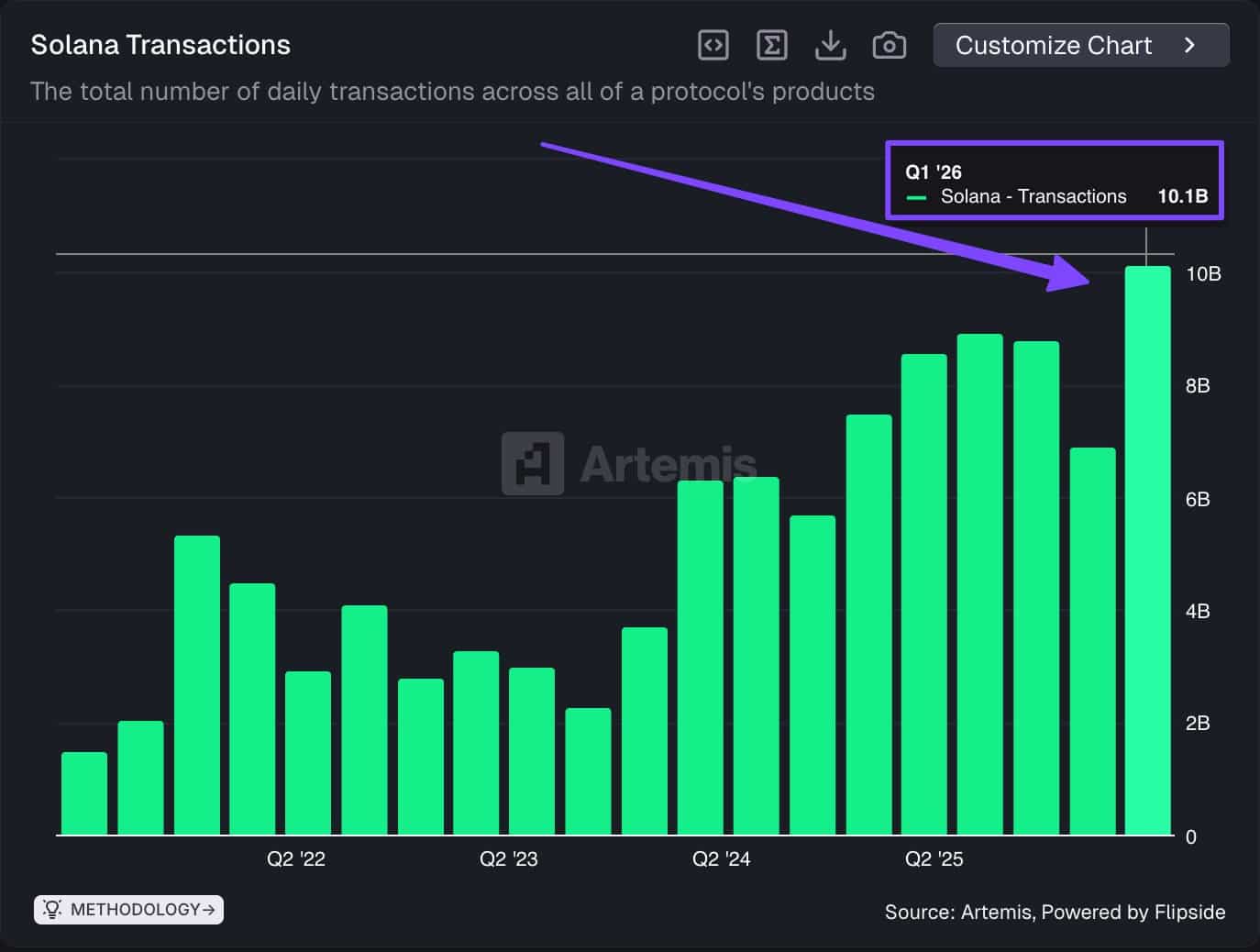

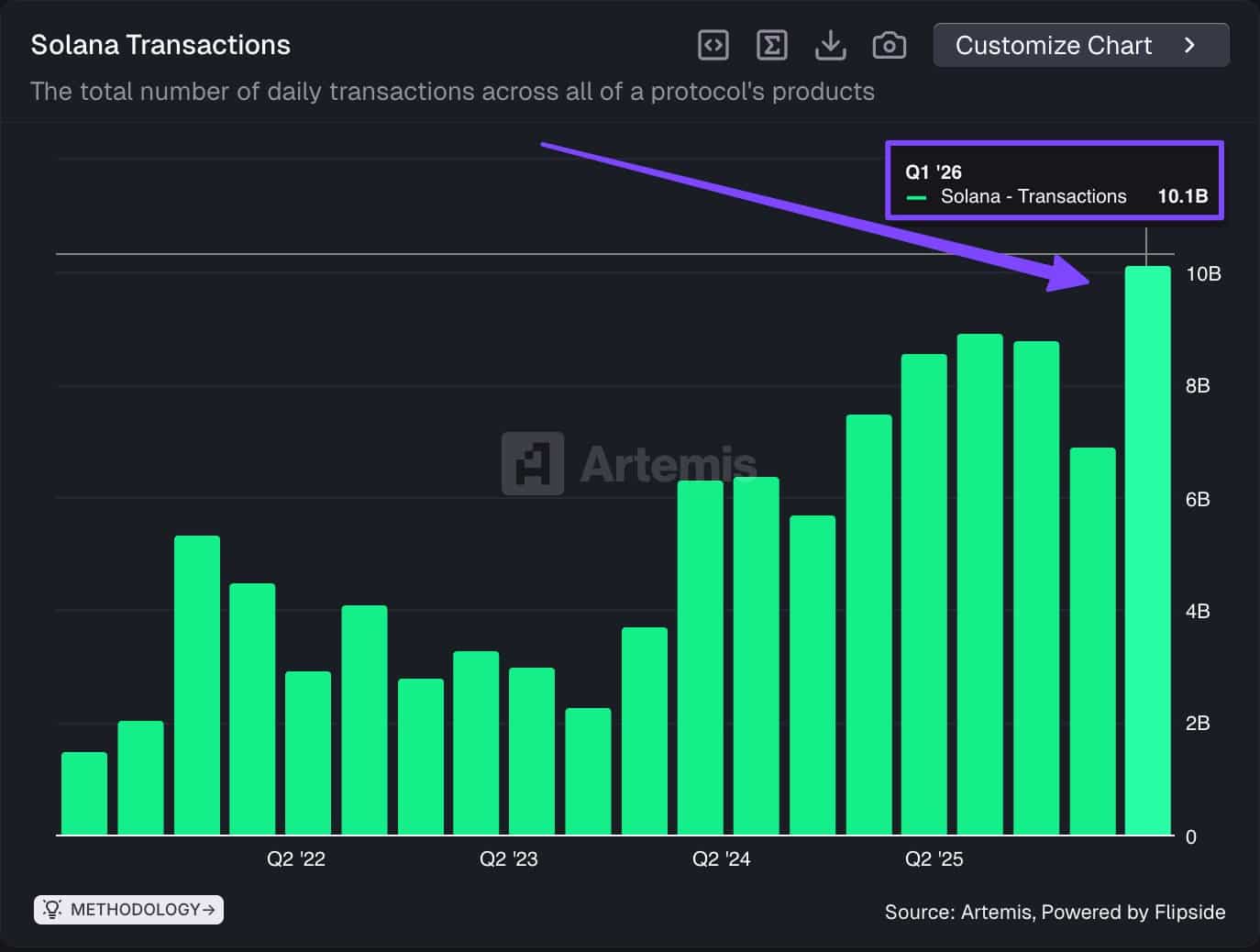

New figures from Artemis show Solana processed 10.1 billion transactions in Q1 2026, marking the first time it has crossed the 10B threshold in a single quarter.

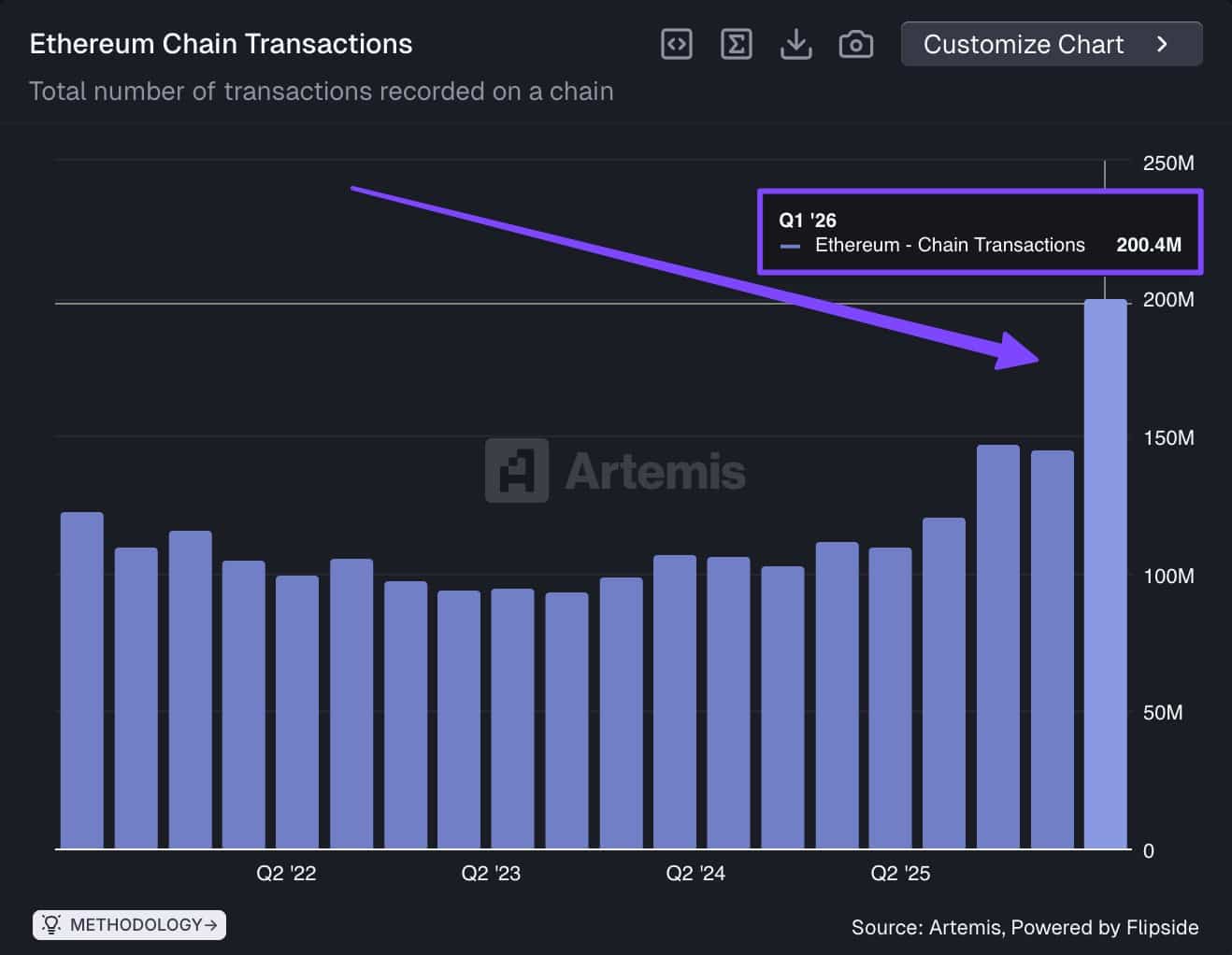

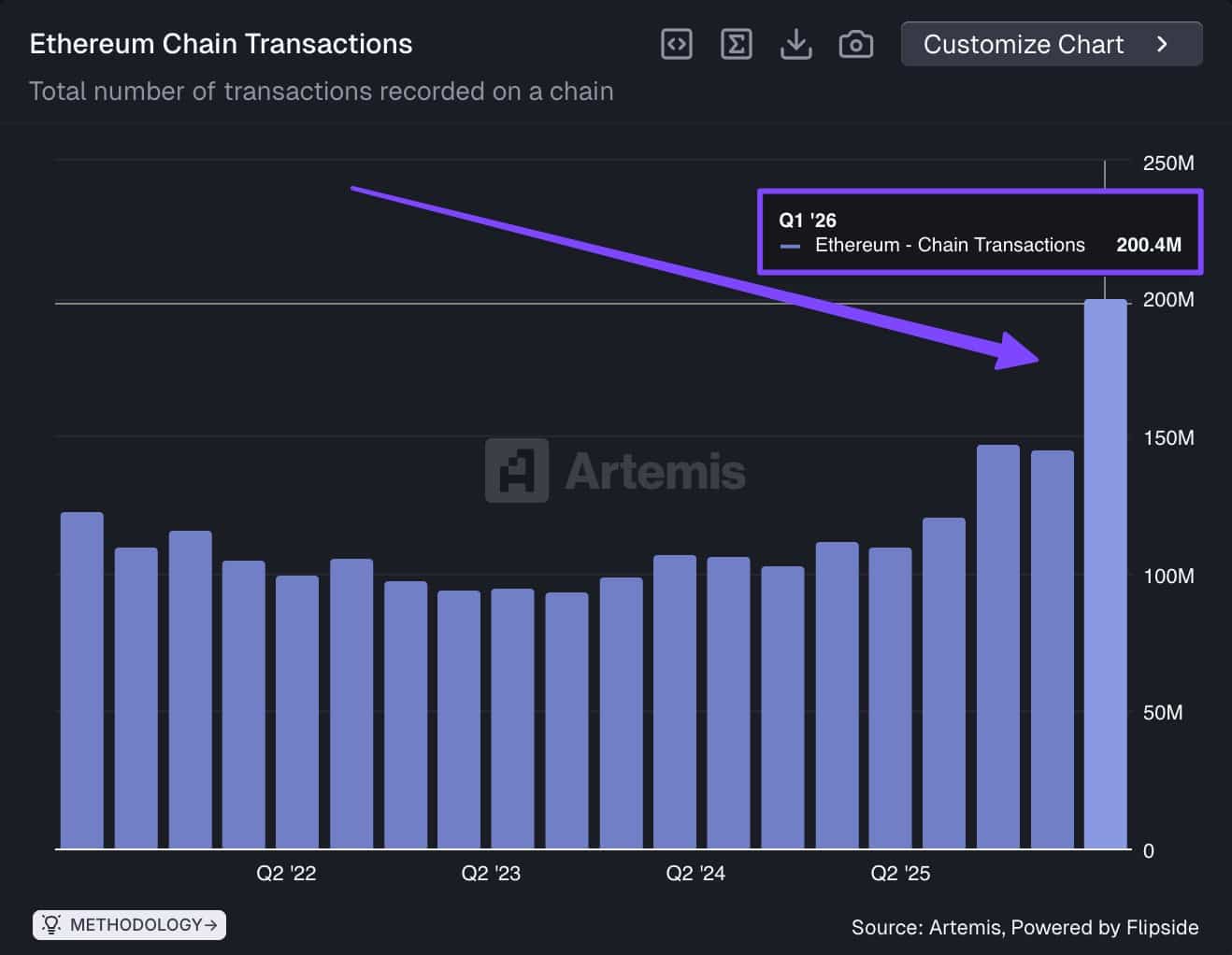

Over the same period, Ethereum recorded just over 200 million transactions, also a record high.

At face value, the disparity is stark. But the numbers point less to competition and more to diverging blockchain roles.

Solana’s throughput model accelerates

Solana’s transaction growth has been driven by its core design: high throughput and low fees.

The network has positioned itself as a platform for high-frequency activity, including trading, gaming, and automated transactions. This has enabled it to process billions of transactions per quarter, with activity accelerating through 2025 and into early 2026.

The scale reflects a system optimized for speed and volume, where transaction costs remain low enough to support frequent interactions.

Ethereum’s value layer expands steadily

Ethereum’s growth trajectory looks different.

While transaction counts remain significantly lower, the network continues to anchor high-value activity, including decentralized finance, institutional flows, and Layer 2 settlement.

Rather than maximizing raw throughput, Ethereum’s ecosystem has evolved toward a model where activity is distributed across scaling layers, with the base chain acting as a secure settlement layer.

The result is fewer transactions, but typically higher value per interaction.

Two definitions of blockchain activity

The contrast between the two networks underscores a broader shift in how blockchain usage is measured.

Solana’s metrics highlight quantity — the ability to process massive volumes of transactions efficiently.

Ethereum’s metrics reflect value density — where fewer transactions can represent significant economic activity.

As a result, raw transaction count alone no longer provides a complete picture of network dominance.

A multi-chain reality takes shape

The data suggests that blockchain ecosystems are increasingly specializing rather than competing directly.

Solana is emerging as a high-throughput execution environment, while Ethereum continues to function as a foundational settlement layer for a broader ecosystem of applications.

Both models are expanding simultaneously, suggesting a market structure where different networks optimize for different use cases.

Final Summary

- Solana’s 10.1B quarterly transactions highlight its strength in high-throughput, low-cost activity at scale.

- Ethereum’s 200M transactions reflect its role as a high-value settlement layer, emphasizing quality over quantity.