On the 8th of April, Morgan Stanley became the first Wall Street bank to launch its own Bitcoin-tracking exchange-traded fund under the ticker MSBT.

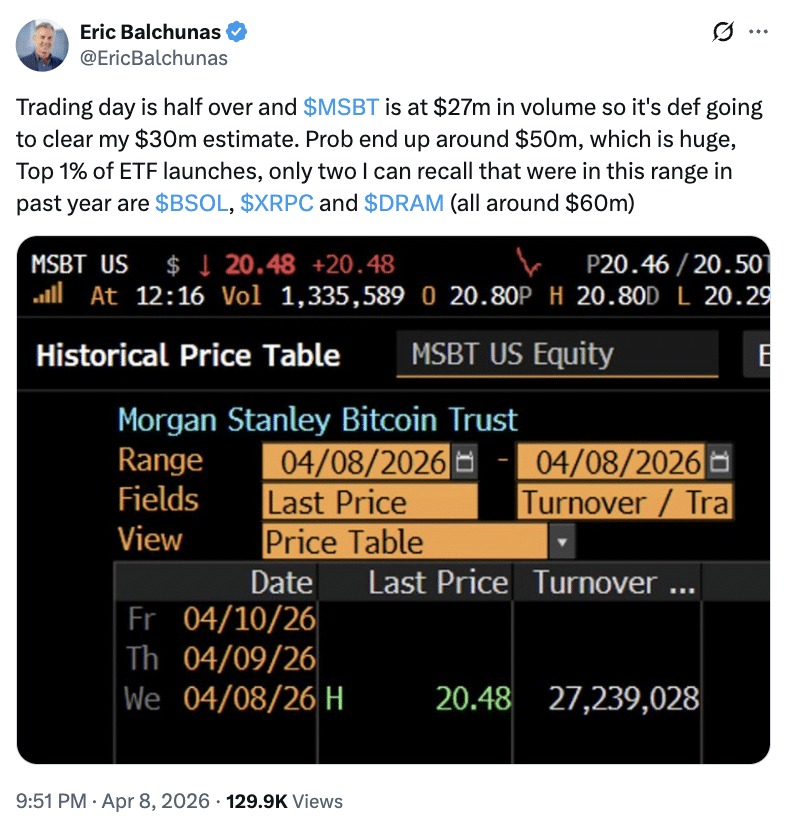

Debuting on the NYSE Arca, MSBT recorded $30.6 million in inflows on its first day, as reported by Farside Investors ETF monitor.

Interestingly, Senior Bloomberg Analyst Eric Balchunas had already predicted this inflow when he took to X and noted,

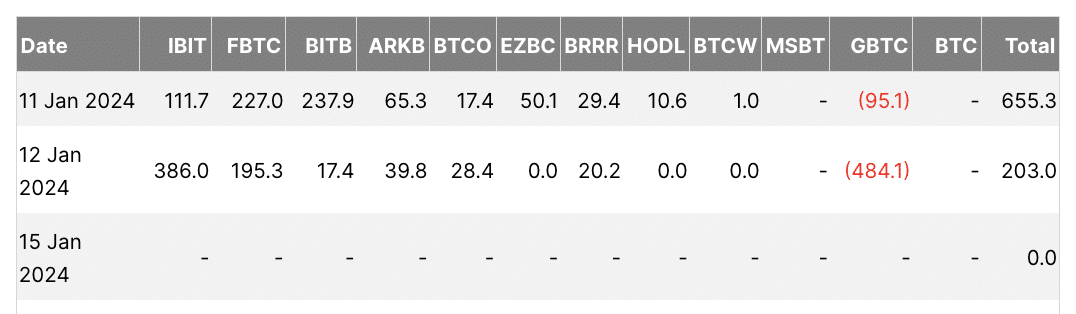

Morgan Stanley’s MSBT vs other Spot BTC ETFs debut

However, if looked back, in comparison to other Bitcoin [BTC] ETFs, the performance was low.

This is because on the 11th January 2024, the launch date of multiple Spot Bitcoin ETFs, Bitwise’s BITB saw inflows worth $237.9, followed by Fidelity’s FBTC, which recorded inflows worth $227.0 million.

Additionally, BlackRock’s IBIT saw inflows worth $111.7 million. In fact, only Invesco’s BTCO, Valkyrie’s BRRR, Wisdom Tree’s BTCW, and VanEck’s HOLD were the ones that recorded inflows less than MSBT.

Does MSBT have an edge in this competitive market?

Yet despite this, and being late to the launch list, the fees and scale are giving MSBT a secret advantage over others.

Accounting for an expense ratio of 14 basis points in comparison to Grayscale’s BTC’s 1 basis point and BlackRock’s IBIT’s 11 basis points, MSBT is the cheapest fund.

Expressing on the matter, Allyson Wallace, global head of ETFs at Morgan Stanley Investment Management, in a recent Bloomberg interview said,

The demand, especially from the high-net-worth investors, has been quite high. Viewed at the firm level, this is an asset class that is not going away.

Overall, this shift in sentiment shows how traditional institutional leaders are finally understanding the value of crypto.

Remarking on the same, Strategy’s new CEO, Phhong Lee, recently hit the nail on the head when he said,

In the last month, Morgan Stanley, Charles Schwab, and Citadel — among the world’s largest wealth managers, broker-dealers, and hedge funds — have announced plans to build Bitcoin capabilities. Probably nothing.

Volatile market dynamics

This comes at a time when the overall crypto market surged after the announcement of an immediate ceasefire in the ongoing U.S- Iran tension. In turn, this resulted in the crypto market surging over 4% on the 8th of April.

However, at press time, the crypto market was back in the hands of sellers and was trading at $2.42 trillion. Yet despite the drop, Bitcoin was still above the $70,00 mark, changing hands at $71,501.17 at the time of reporting.

Final Summary

- Morgan Stanley’s Bitcoin ETF debut was not that strong, but fees and scales are giving it an additional advantage over other Spot BTC ETFs.

- Launching at a time when the crypto market was volatile shows banks’ long-term conviction in Bitcoin.