Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web3_golem)

Last week, a new Meme launch platform on the Hyperliquid ecosystem called alt.fun attracted significant attention from Meme players. Within just one week of launch, its leading token ALT reached a peak market cap of $8.8 million. Its price has since retraced, with the market cap currently hovering around $6.7 million.

The novelty of alt.fun can be understood as a combination of Pump.fun and Hyperliquid, allowing users on this platform to experience the dual thrill of playing with Memes and opening leveraged contracts simultaneously.

Introduction to the alt.fun Platform Mechanism

Specifically, each Meme token launched on alt.fun has a corresponding contract position on Hyperliquid as its underlying asset.

Similar to Pump.fun, any user can launch a Meme coin on HyperEVM with one click via the alt.fun platform. The token price is still influenced by a bonding curve. The total supply of a created Meme coin is 1 billion tokens. When 75% of the tokens are sold, the token successfully "graduates" and is migrated to the HyperSwap V2 liquidity pool.

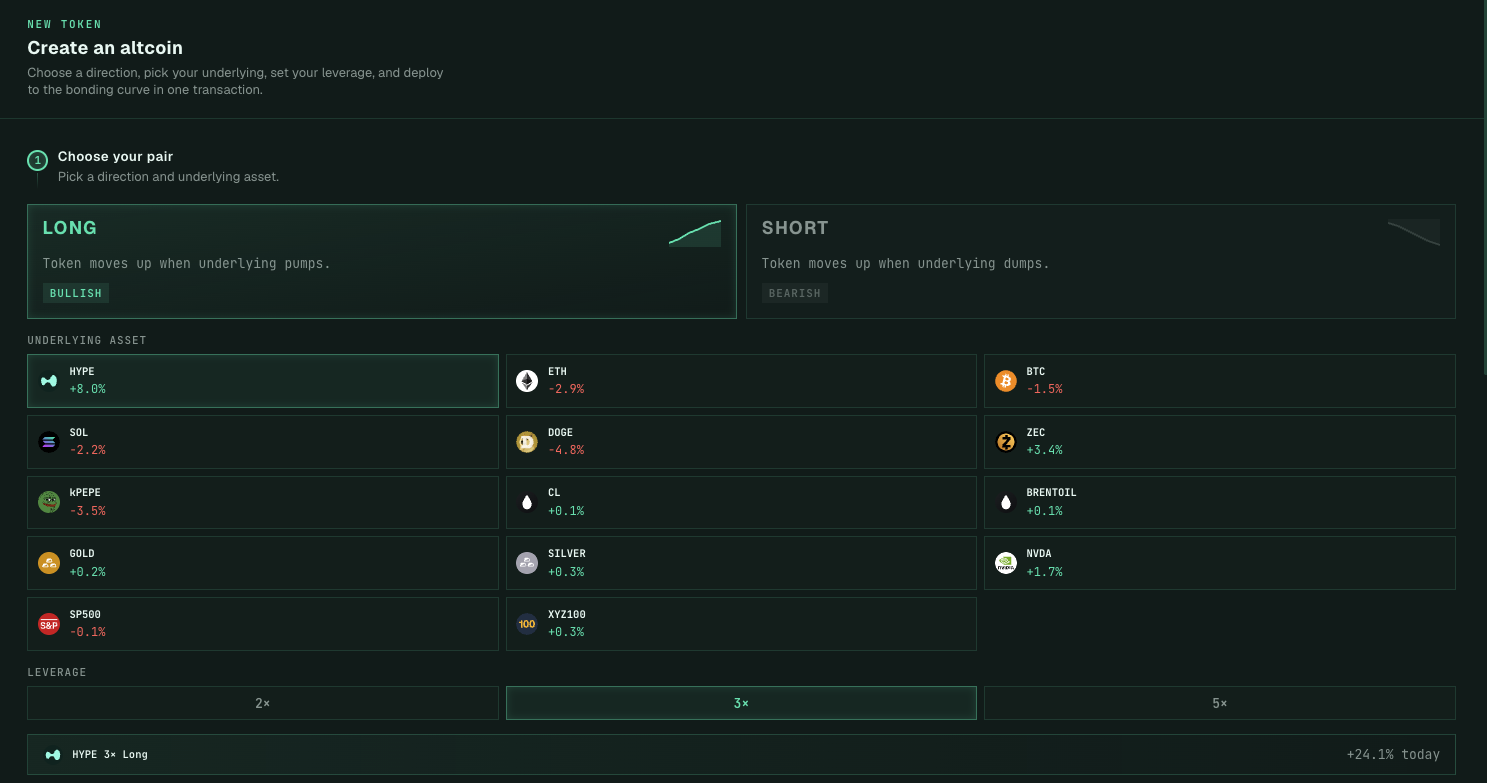

The difference from Pump.fun is that when creating a token on alt.fun, the user also needs to select an underlying asset and specify a leverage level (2x/3x/5x) for a short/long position. At the exact moment of token creation, the platform mints a corresponding amount of Leveraged Tokens (LT) on BounceTech(Odaily note: a permissionless leveraged token platform on Hyperliquid) and sends them to the user. These leveraged tokens represent perpetual contract positions on Hyperliquid. For example, if a user chooses to create a token based on a 3x long HYPE position, what they receive is essentially a leveraged token tracking the returns of a 3x long HYPE position.

As shown in the figure below, currently on alt.fun, users can choose from 14 underlying assets when creating a token. Similarly, when a player buys a Meme coin on this platform, the platform also mints the corresponding leveraged tokens on BounceTech. If a player sells, this process is reversed—the leveraged tokens are redeemed, and the user receives the corresponding USDC.

This model of packaging leveraged tokens as underlying assets and then selling them is similar to the securitization of specific risk exposures like futures and options in traditional finance, such as 3x short Nasdaq ETF, 5x short crude oil products, etc. In this process, the alt.fun platform acts as a role similar to an asset management company, managing the long-term positions behind the leveraged tokens for users.

The core price of such financial products follows the net asset value. However, because the token price on the alt.fun platform is also simultaneously influenced by the Meme coin bonding curve mechanism, the graduation model and price drivers for tokens on this platform are not singular.

Dual Graduation Modes and Price Driving Factors

This also means that token prices on the alt.fun platform are influenced by two factors: first, by market sentiment from buying and selling; second, by the performance of the underlying asset. So now you might understand the meaning of alt.fun's slogan, "Your token pumps even when nobody's buying."

For example, if a user creates a token based on a 3x long HYPE position with an initial investment of $20 (the platform's minimum buy-in size), and subsequently HYPE rises by 10%, then even if no one else buys the token, the user's holding value increases by 30% to $26.

Based on this dual price driver, the graduation model for tokens on the alt.fun platform is also not limited to one method. Specifically, the graduation condition for its tokens is reaching a market cap of $9,000. This essentially calculates the value of the leveraged token. Besides achieving graduation through token purchases, if the token's own value driven by the underlying asset's rise reaches a $9,000 market cap, it can also graduate smoothly. Therefore, whether a token reaches the graduation threshold is often a combined result of both price mechanisms.

Of course, ideally, the underlying asset's rise drives the leveraged token's increase, which, combined with the emotional catalyst from the Meme market, might cause the token's price to spiral upward rapidly. However, once the underlying asset falls, the leveraged token's value continues to shrink, potentially causing market panic and a sell-off, leading to the token's price crashing instantly.

Therefore, although alt.fun's mechanism can effectively leverage amplification effects, this only works in one-directional market trends and requires users to accurately catch the trend. If encountering volatile market conditions for the underlying asset, users must also bear the decay loss from leverage. This is because when the underlying asset price fluctuates, the platform needs to perform "rebalancing" to manage positions to avoid liquidation. This means that even if the underlying asset falls and then recovers to its original price, the leveraged token will suffer losses and gradually depreciate due to forced position reductions during the dip.

Furthermore, in cases of sudden price spikes or flash crashes, the platform might fail to react in time, potentially leading the leveraged token's value to zero.

Meme or not Meme

The alt.fun platform currently has a total of 41 graduated tokens. Only two have a market cap exceeding one million: ALT (based on 5x long HYPE) and STONKS (based on 5x long S&P 500). The total number of users is around just over 1,000. Although alt.fun is still in its early stages, we can already identify its current development bottlenecks.

First, the platform has too few underlying assets. With the current 14 underlying assets, there can be at most 84 different combinations of leveraged tokens. alt.fun has already seen leveraged tokens with the same leverage level (short/long) on the same underlying asset. For instance, the current top token ALT is based on 5x long HYPE, while another token, ATH, with a certain market cap, is also based on 5x long HYPE. Apart from the token name and creation time, there is no difference between them. In that case, why wouldn't an investor buy the lower-market-cap ATH?

Although alt.fun may support more underlying assets in the future, its core pain point is its inability to foster Meme coin community consensus.

The essential reason investors choose to buy leveraged tokens on the alt.fun platform instead of opening leveraged positions directly on Hyperliquid is to obtain greater price leverage and, because the platform manages position rebalancing on the backend, individual users can act as "hands-off managers," not worrying about individual liquidation risks.

But this is also the issue. Investors buying an alt.fun token are essentially doing so based on future price expectations for its underlying asset, not based on narrative, market games, attention—these "meaningless things" that ironically are the core value supporting Memes. A Meme's ability to rise or gain market recognition often isn't due to any actual value backing or financial design behind it; what's more important is its community propagation attribute.

As a Meme player, it's difficult for me to develop a love for a leveraged token similar to the passion for a particular Meme community's culture. If someone truly has faith in the underlying asset of a leveraged token, they might as well issue their own leveraged token rather than buying an existing one and bearing unnecessary premiums.

Therefore, the mechanism of the alt.fun platform appears novel, but in my view, it's merely a mechanical innovation. If alt.fun focuses on developing towards a DeFi platform in the future, there might be an opportunity. However, if it insists on forcing its way into the Meme launch platform track, it is destined to be a flash in the pan.