Ghana has legalized cryptocurrency trading by establishing a regulatory framework targeting the industry.

Ghana’s parliament has passed the Virtual Asset Service Providers Bill into law, Bank of Ghana (BoG) Governor Johnson Asiama said, according to a report on Sunday by the state-owned Daily Graphic news agency.

“Virtual asset trading is now legal, and no one will be arrested for engaging in cryptocurrency, but we now have a framework to manage the risks involved,” Asiama said on Friday at the BoG’s annual Nine Lessons, Carols and Thanksgiving Service.

The timing aligns with earlier central bank communications, as Asiama had previously indicated Ghana was targeting the introduction of crypto regulation by the end of 2025.

Ghana’s central bank gains supervisory powers

Under the legislation, the Bank of Ghana becomes the primary regulator for cryptocurrency activity, with powers to license and supervise crypto asset service providers (CASPs).

The law positions Ghana to better protect consumers from fraud, money laundering and systemic risks, while removing uncertainty over the legal status of cryptocurrency, Asiama said, adding:

“What this means is that now we have the framework to manage it and to manage the risks that can involve that kind of activity [...] These are not just legal milestones; they are enablers of better policies, stronger supervision and more effective regulation.”

The governor also mentioned that the crypto law is intended to support innovation and expand Ghana’s financial inclusion, particularly among young people and tech-driven entrepreneurs.

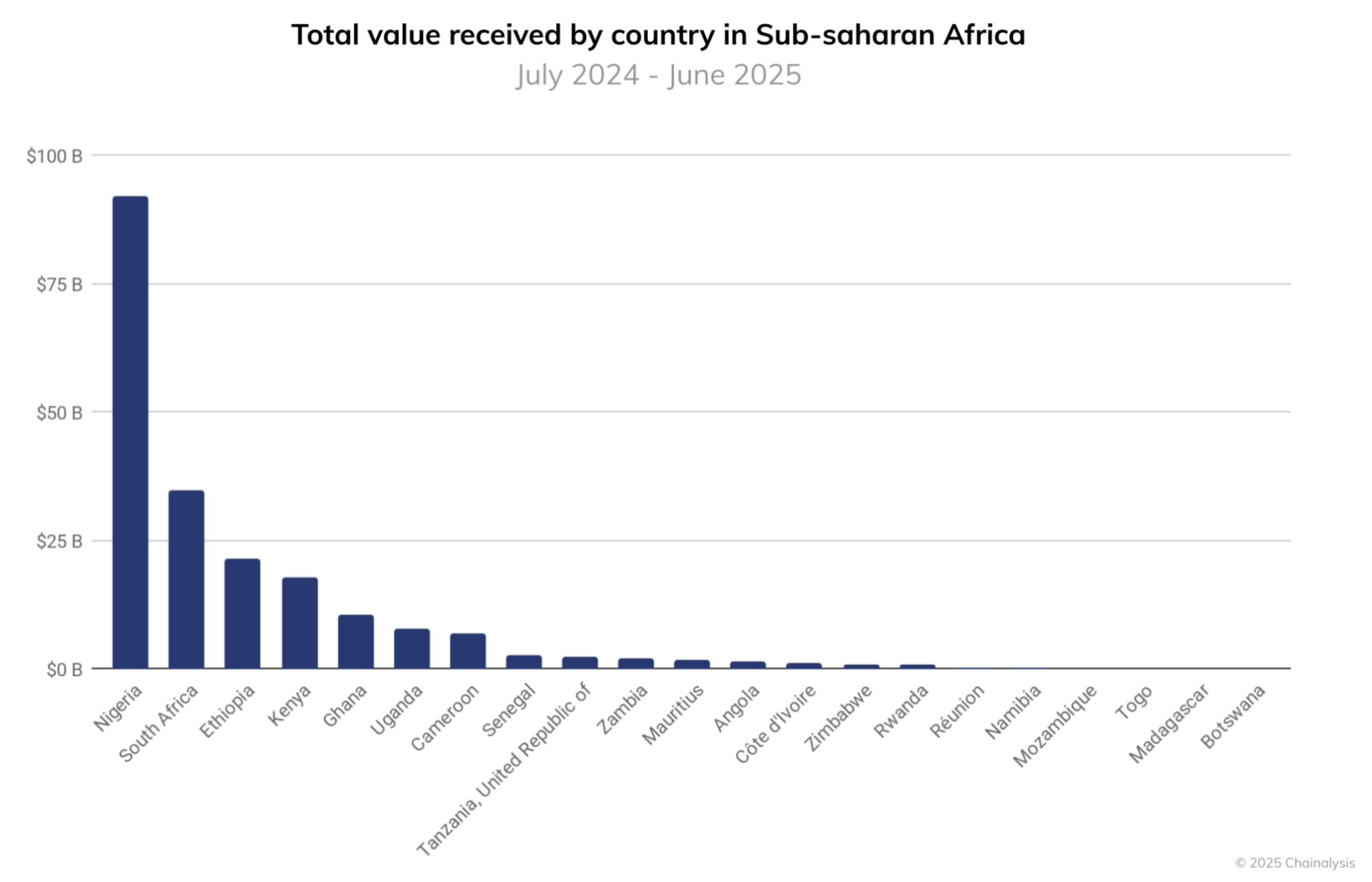

Ghana ranks among Sub-Saharan Africa’s top five crypto economies

Ghana’s move to regulate cryptocurrency activity comes as the country emerges as a significant player in crypto adoption across the region.

According to Chainalysis’ 2025 Geography of Cryptocurrency Report, Ghana ranked among the top five Sub-Saharan African countries by total crypto value received between July 2024 and June 2025.

In the meantime, Nigeria continued to dominate the region, receiving at least $92 billion in crypto value over the period, or nearly three times the amount recorded by South Africa, the report showed.

Related: CAR’s crypto push fueled ‘state capture’ by elites, criminal networks: Report

The Sub-Saharan region received over $205 billion in on-chain value, up about 52% from the previous year. This growth makes it the third-fastest growing region in the world, just behind Asia-Pacific and Latin America, according to Chainalysis.