Galaxy’s yield-focused product, GalaxyOne, will now support Solana [SOL] staking, marking the first time a crypto-yield feature has been activated for individual users on the platform.

On the 30th of March, the firm said it would channel back full staking rewards, commission-free, for the entire year.

The new feature allows clients to earn up to an estimated 6.50% in variable rewards on crypto through staking, with no platform commission through December 31, 2026, allowing users to retain more network-generated rewards.

Initially, GalaxyOne used to offer a high yield for cash deposits and stock lending options. The SOL staking yield debut will kickstart its expansion into crypto staking rewards, which individual investors can enjoy alongside their traditional interest-generating assets.

Zac Prince, head of GalaxyOne, noted,

Staking launches today with SOL, with ETH coming soon, and our clients can now buy, transfer, trade, earn rewards, and manage their crypto alongside the rest of their financial portfolio, all in one platform.

For the unfamiliar, staking allows one to delegate their tokens to secure a blockchain (Proof of Stake, PoS) via a validator and earn rewards in return.

In fact, Galaxy is one of the top 10 Solana validators (6.55 million SOL staked) and has been sharing the rewards with institutional investors for the past few years. As such, the update only ropes in individual investors for the first time.

Demand for SOL staking in Q1 2026

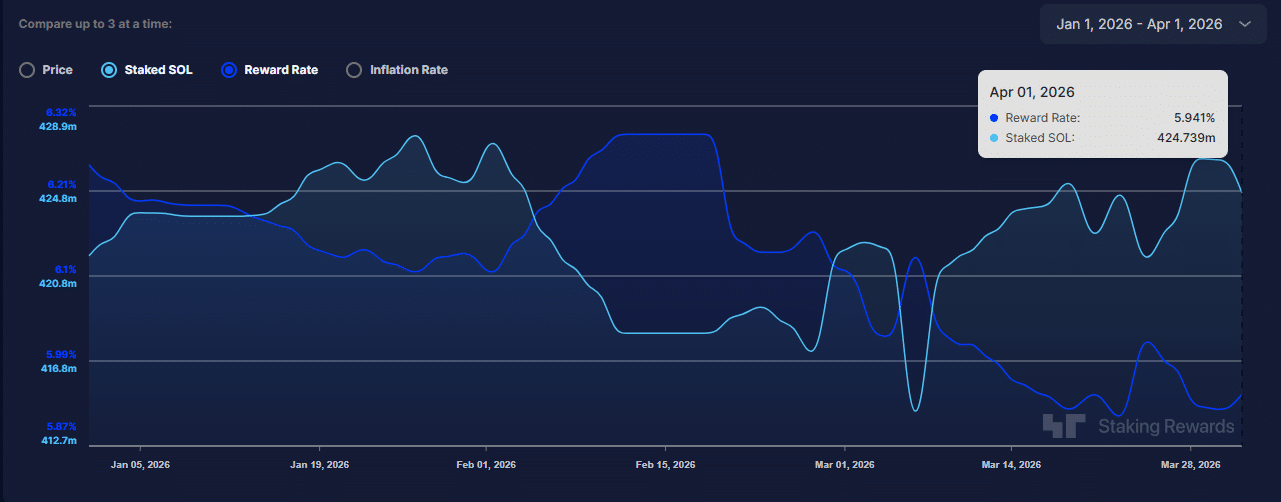

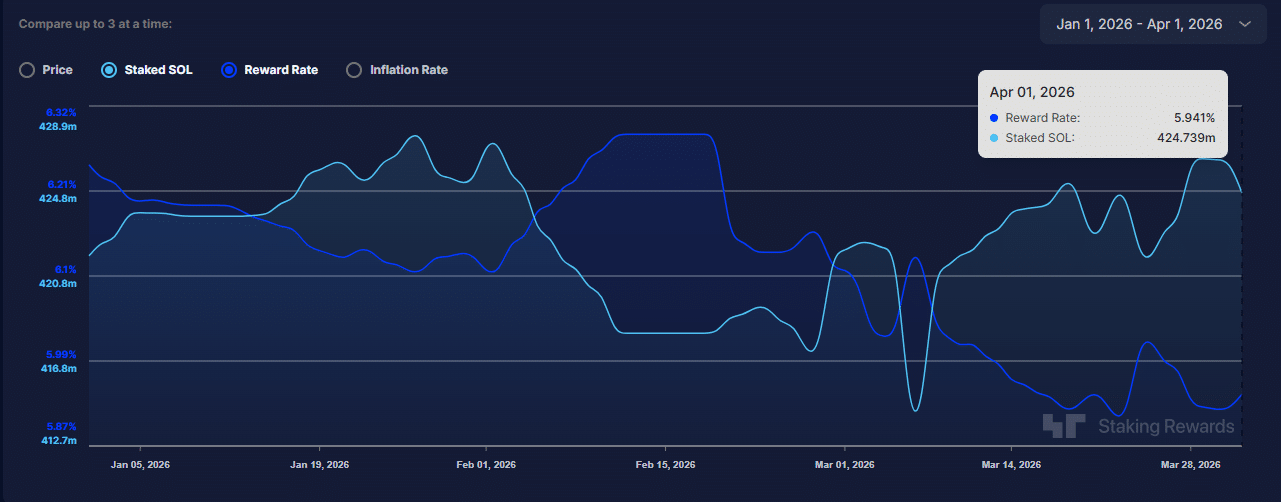

That said, rising demand for SOL staking can be deemed bullish for the altcoin. It exerts buying pressure, especially if players acquire SOL directly from the spot markets for staking purposes. However, there have been fluctuations in Q1 2026.

According to Staking Rewards data, staked SOL increased to a quarterly high of 427.53 million SOL in late January. However, demand dipped about 3% to a low of 414 million SOL in early March before rebounding.

In March, the renewed staking demand recovered to January levels, 68% of the total SOL supply.

Over the same period, SOL’s price bounced back about 20% from $80 to nearly $100. It remains to be seen whether the GalaxyOne update will trigger meaningful staking demand and boost SOL’s price.

Final Summary

- SOL staking demand recovered back to Q1 highs above 420 million SOL after a brief 3% dip.

- The Q1 staking demand partly fueled SOL’s 20% surge in March and could benefit more if GalaxyOne’s move drives renewed staking appetite.