Ethena’s [ENA] price now appears to be aligning with its weakening financial performance. Over the past 24 hours, the asset has recorded a double-digit decline, dropping to $0.089 at press time.

While the numbers reflect mounting pressure, a broader evaluation of market conditions is necessary to determine whether this decline marks the start of a deeper correction or a temporary adjustment.

Ethena’s momentum weakens across key metrics

On-chain data shows that ENA has underperformed across multiple fronts since the start of Q1 2026, particularly when compared to its performance in the previous two quarters.

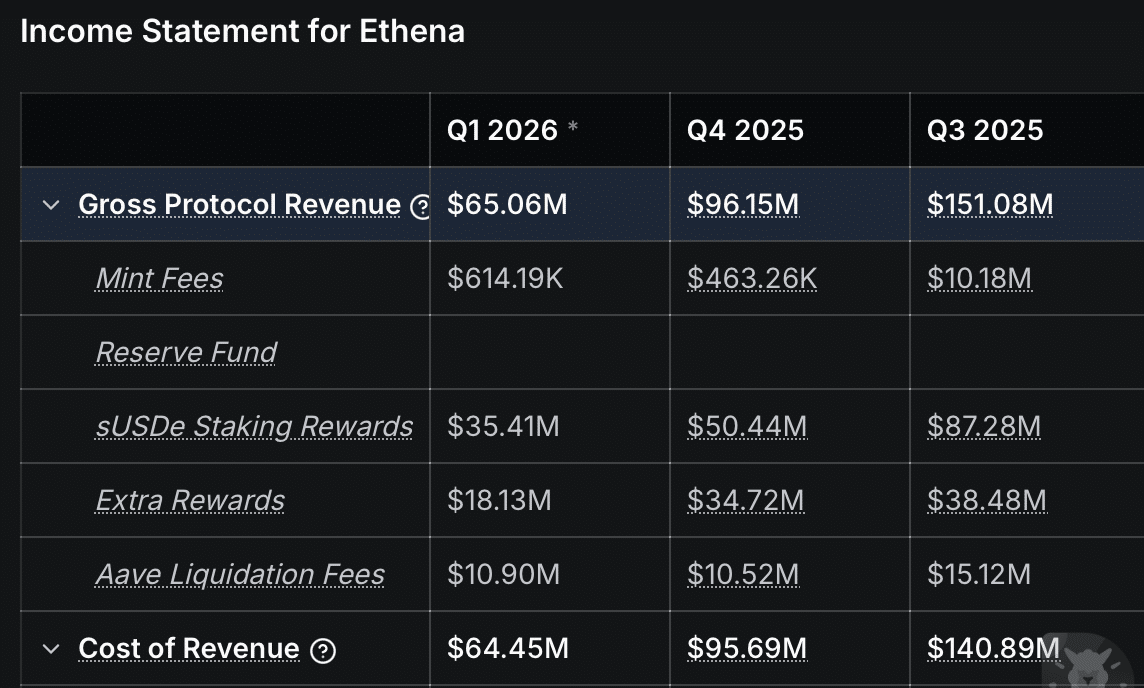

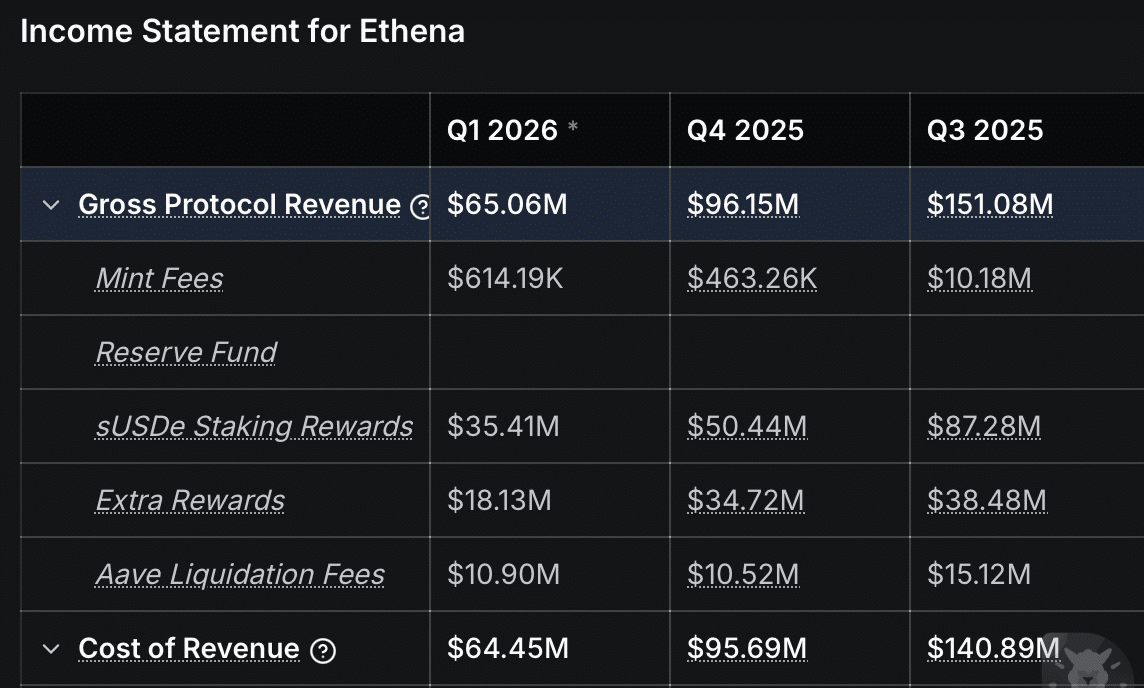

A key area of concern is revenue efficiency. Gross Protocol Revenue fell to $65.06 million, down from $96.15 million in Q4 2025, representing a 32% decline. The drop becomes even more pronounced when compared to Q3 2025.

This contraction points to weaker minting activity and reduced staking rewards, both of which suggest declining on-chain participation.

In a market that has remained relatively stable compared to the October–December 2025 cycle, this underperformance raises concerns about weakening user demand rather than external pressure.

Liquidity conditions reinforce this trend. Total Value Locked (TVL), a core indicator of protocol health and user commitment, has continued to decline steadily.

Since the start of March 2026, TVL has fallen by approximately $130 million, bringing it to around $6.66 billion at the time of writing. Within the last 24 hours alone, roughly $16 million has been unstaked, signaling sustained capital exit from the protocol.

Can profit alone sustain user interest?

Despite the broader slowdown, Ethena has recorded a slight improvement in gross profitability.

In Q1 2026, the protocol has generated $614,190 in gross profit, compared to $463,200 in Q4 2025. While this reflects a marginal increase, it does little to offset the sharp decline from earlier performance levels.

For context, Q3 2025 saw $10.18 million in gross profit, roughly 16.5 times higher than current figures. This gap highlights a structural decline in earning potential, even as short-term profitability shows minor improvement.

The implication is clear, as modest profit growth alone may not be sufficient to retain users, especially in a competitive DeFi environment where capital quickly rotates toward higher-yield opportunities.

User activity data supports this view. According to Artemis, Daily Active Users have dropped to around 1,200, the lowest level recorded since December.

Spot demand offers a counter-signal

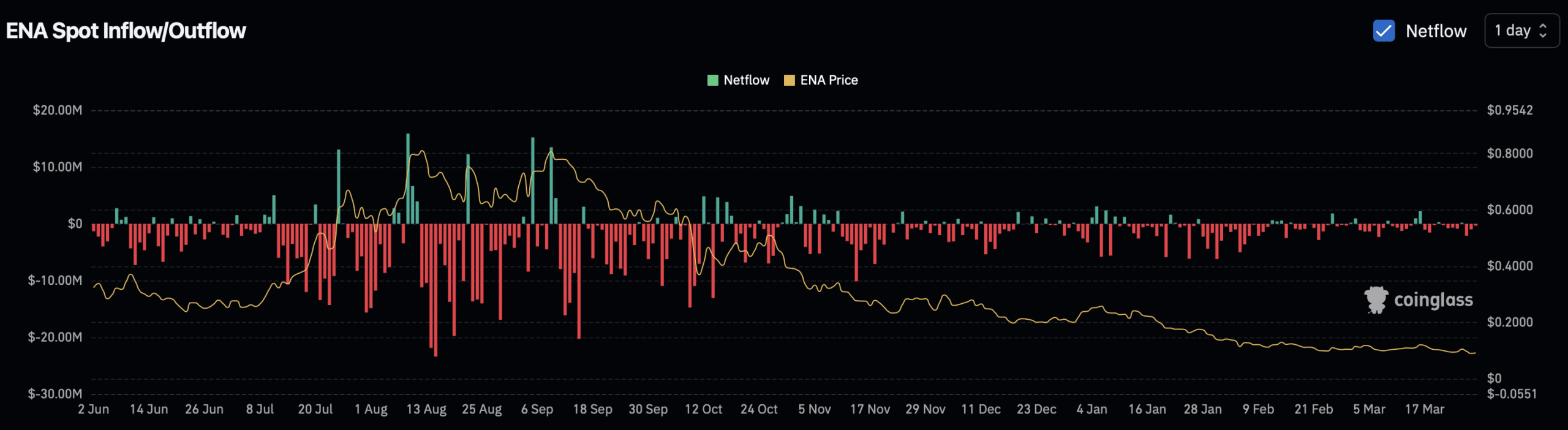

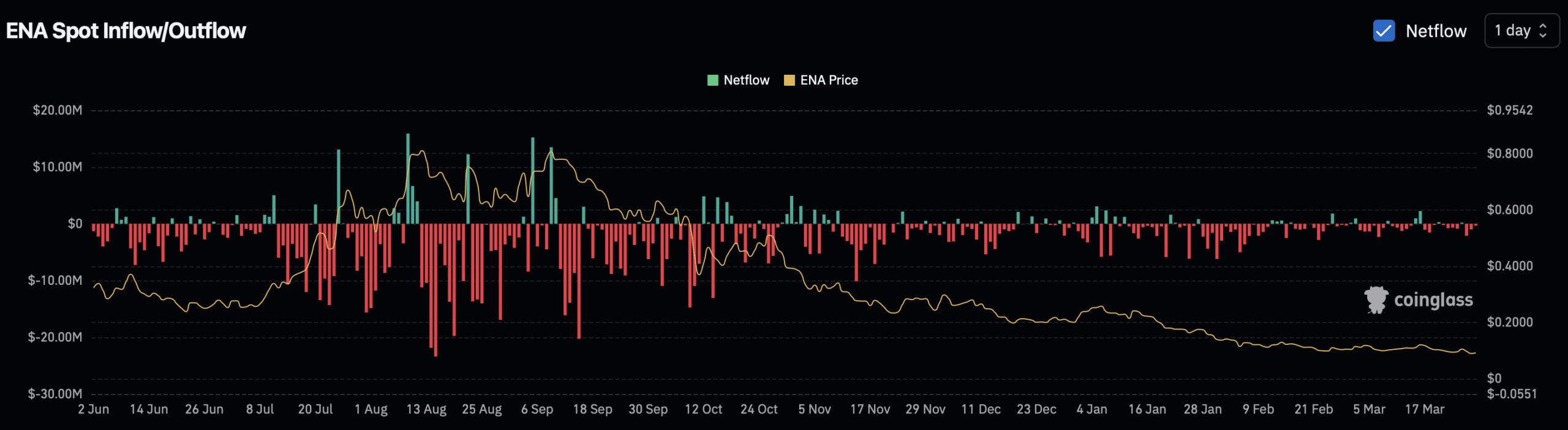

Despite weakening fundamentals and declining liquidity, spot market activity presents a more resilient picture. Exchange netflow data indicates that buying pressure has increased recently. Over the past 24 hours, net inflows into spot positions reached approximately $303,000.

More notably, this is not an isolated event. Over the past three days, cumulative purchases have climbed to around $3.41 million, suggesting consistent accumulation.

Such a sustained demand indicates that investors continue to absorb sell-side pressure, even as capital exits the protocol layer.

If this accumulation trend holds, it could limit further downside and support price stabilization. However, without a recovery in core fundamentals, particularly user activity and revenue generation, any upside may remain constrained within a narrow range.

Final Summary

- Ethena’s protocol performance deteriorated in Q1 2026, even as broader market conditions remained relatively stable.

- Spot investors continue to accumulate, despite rising liquidity outflows and declining TVL.