TL;DR

The recent market inclusion of Anthropic in the same trading chart is not an isolated event but a set of signals: a nearly one-trillion-dollar post-money valuation, confidential S-1 filing, rapidly growing revenue run-rate, and rumors surrounding Claude 5.

For investors, the meaning of these signals is straightforward. AI frontier labs are no longer proving themselves solely with papers, model rankings, and product reputation. They are starting to explain how much they are worth in a language the public market can understand. Model capabilities, enterprise adoption, revenue quality, compute costs, and risk disclosure are all being placed into a single pricing framework.

There is currently no official announcement, product page, or model card from Anthropic confirming Claude Fable 5. Statements about it sharing an underlying architecture with Mythos, adding safety guardrails, and improving long-context and complex task capabilities should still be considered rumors or market expectations. What's truly worth discussing is not what Fable 5 has already proven, but why an unconfirmed new model is being incorporated into Anthropic's IPO narrative ahead of time.

Anthropic Enters IPO Preparation Phase

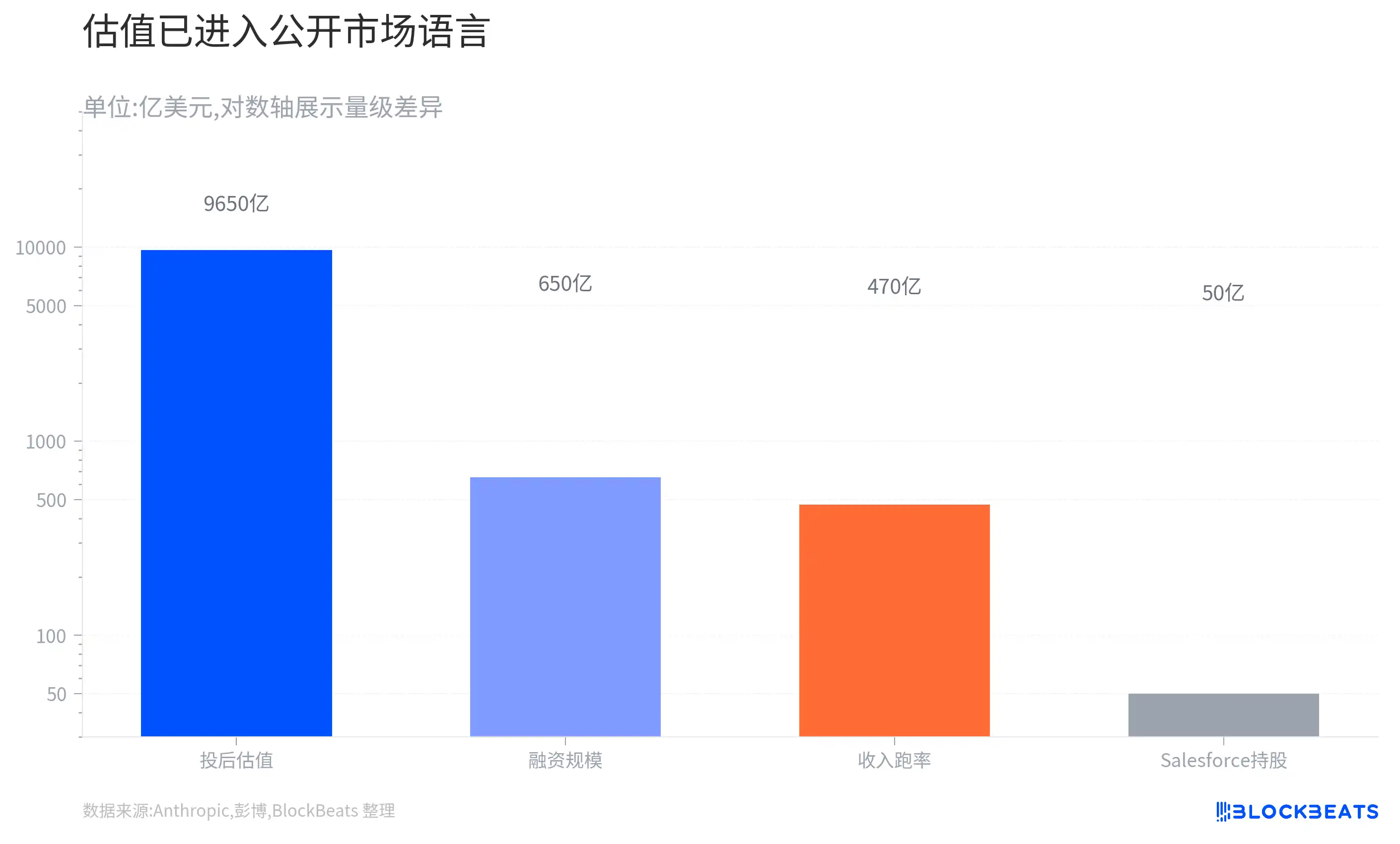

Anthropic's timeline is dense enough. On May 28, the company announced the completion of a $650 billion Series H financing, with a post-money valuation reaching $9.65 trillion, and stated that its run-rate revenue had exceeded $470 billion earlier that month. On June 1, Anthropic further confirmed it had confidentially filed a draft Form S-1 with the SEC for a planned IPO. The number of shares to be offered and the price range have not been determined, and the listing remains subject to SEC review, market conditions, and other factors.

This changes Anthropic's position in the market. It is no longer just the "safe model company" alongside OpenAI but an ultra-large AI platform candidate preparing for the public market. The private market can pay for future imagination, and the public market will also pay for the future, but it demands that companies break down that imagination into more verifiable metrics.

These metrics include whether revenue sources are stable, customers are concentrated, compute costs are controllable, model leadership is sustainable, and regulatory risks are disclosable and manageable. For frontier model companies, this transition is harder than for traditional software companies.

When traditional SaaS companies go public, investors typically look at ARR, net retention rate, gross margin, sales efficiency, and customer structure. Frontier model companies also need to answer these questions but additionally face training and inference costs, model iteration speed, safety incidents, cloud provider dependency, and chip cycles. The stronger the model, the greater the revenue potential, but also the heavier the cost and regulatory variables.

This is also what makes Anthropic special at this moment. Its high valuation cannot be supported solely by "Claude is smarter." It needs a more complete story: sustained progress in model capabilities, enterprise customers willing to pay, a sufficiently large revenue run-rate, a safety positioning that unlocks high-value scenarios, and an available capital market window. The amplification of the Claude 5 rumors is precisely because it appears to be the next piece of the puzzle in this story.

Fable 5 Rumors Being Traded in Advance

If Anthropic were simply releasing a new model in a routine manner, the market likely wouldn't be this excited. The amplification of the Claude 5 rumors is precisely because it coincides with a critical IPO juncture. Financing, valuation, S-1 filing, layered with heavyweight model leaks perfectly form a narrative the capital market loves to hear: the company proves with concrete action just before its IPO that it remains firmly at the forefront of capability iteration.

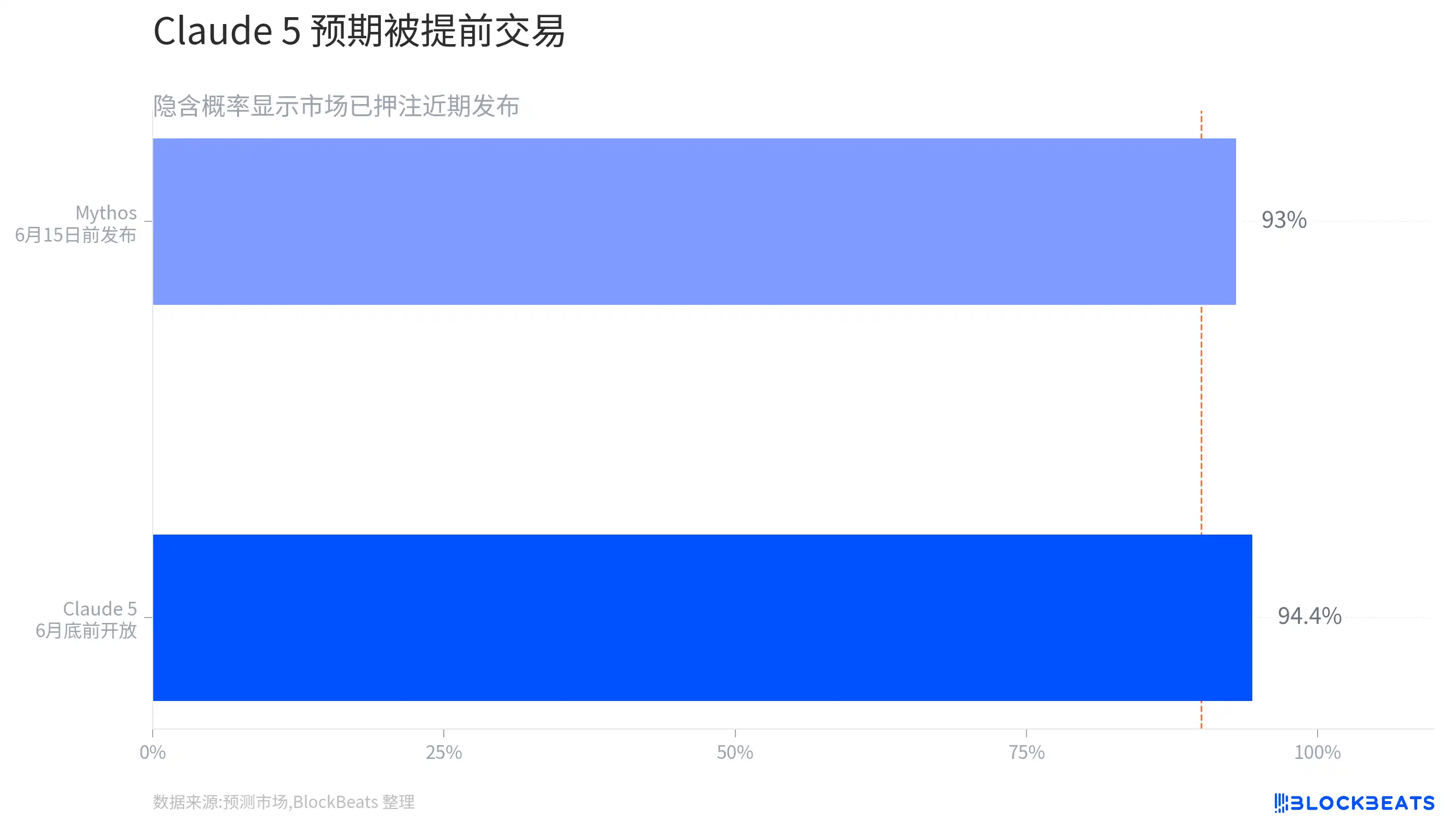

Prediction markets have already opened betting on "whether Claude 5 will be publicly available by June 30, 2026." The current market price reflects the traders' implied probability. While public information cannot yet fully confirm the specific timeline previously circulated, it's clear: the prediction market is already pricing a near-term release of Claude 5, and the price is not low.

This expectation carries inherent information. The market directly translates "product cadence" into "valuation narrative": if Anthropic can indeed consistently roll out stronger models, its nearly trillion-dollar post-money valuation with a high revenue run-rate will be interpreted as a natural outcome of rapid platform capability expansion; conversely, if the model cadence noticeably slows, then the near-trillion valuation would have to rely more heavily on the quality and certainty of existing revenue to sustain itself.

This trading method is not unfamiliar. Consumer internet companies emphasize user growth and retention before IPO, cloud companies highlight large customers and net expansion rates, chip companies talk about orders and capacity. AI model companies don't yet have a fully mature public market template, so model releases themselves become a visible signal. It is both a product update and a capability showcase, impacting developers and enterprise clients while also shaping investor imagination about the next phase of revenue growth.

But the impact of a model release on valuation is not linear. A stronger model can bring higher API call volumes, larger enterprise contracts, and stronger customer stickiness, but also potentially higher inference costs, more complex safety reviews, and heavier infrastructure investment. The public market ultimately won't just ask "Is it the strongest?" but also "How much compute is consumed per dollar earned?" "Can gross margins improve?" "Will safety boundaries limit commercialization speed?"

Mythos Provides Imagination, But Also Brings Disclosure Pressure

The more differentiated part of Anthropic's current narrative is not "another chatbot model," but the controlled frontier capabilities represented by Mythos and Project Glasswing.

According to official Anthropic disclosures, Claude Mythos Preview is a general, unreleased frontier model that will not be made broadly available. Project Glasswing is oriented towards defensive security work, where collaborative partners gain controlled access for use in critical software security, zero-day vulnerability discovery and remediation, among other scenarios. Anthropic also disclosed that the project has already discovered a significant number of zero-day vulnerabilities and committed to up to $1 billion in usage credits and $4 million in open-source security donations.

This provides Anthropic with a valuation story different from that of a regular consumer chatbot. It can position itself as a foundational model supplier entering complex tasks, high-value enterprise workflows, and safety-critical scenarios. For the public market, this is easier to map to large customer budgets than "users like to chat," and it's also easier to explain why enterprises are willing to pay a premium for more reliable, safer models.

If there is indeed a technical link between a future Fable 5 and Mythos, with the former offering stricter guardrails to a broader user base, it would create a narrative path in theory: the most frontier capabilities are first validated in a controlled environment, then partially productized in a safer form. This path aligns with Anthropic's long-emphasized safety positioning and fits the demand of enterprise clients for controlled AI.

But the same dynamic pushes Anthropic towards greater regulatory pressure. Cybersecurity capabilities have a dual-use (civilian-military) nature. Models that can find and fix vulnerabilities could also be misused in attack chains. Mythos's controlled release already indicates such capabilities cannot simply be fully released. If future, more general models are interpreted by the market as "trickled-down Mythos capabilities," the company must more clearly explain safety guardrails, access restrictions, misuse monitoring, and liability boundaries.

These contents will enter the S-1 risk disclosures. Public market investors won't only care about how powerful the model is, but also whether that power brings additional regulatory costs, national security reviews, reputational risks, and potential liabilities. For an AI company with a post-money valuation nearing one trillion dollars, a major safety incident could be more than just a product mishap; it could be a systemic variable affecting the listing timeline and valuation multiples.

What's Next is the S-1, Not New Rumors

For Anthropic, what is most likely overestimated by the market right now is not model capability, but the relationship between model capability and valuation.

Discussions about Fable 5, Claude 5, and even Mythos can indeed boost market sentiment. A stronger model means higher customer attention, stronger developer interest, and means Anthropic can continue to maintain its presence in the frontier model competition. But these factors are essentially growth expectations. They can explain why the market is willing to trade the future in advance, but they are insufficient alone to prove that the nearly trillion-dollar valuation has been validated by reality.

Once truly in the public market, investor concerns will quickly become specific. How much of that over $470 billion revenue run-rate can ultimately convert into sustainable, auditable revenue? Is enterprise customer growth coming from long-term deployments or pilot phases? What proportion of revenue comes from top customers? What roles do strategic partners and cloud channels like Amazon and Alphabet play? More importantly, while model inference volumes grow rapidly, can training and inference costs be continuously reduced to support margin improvement?

These metrics ultimately determine not just the growth rate, but how the market defines Anthropic.

If the company can persistently lower unit costs, increase customer stickiness, and build a broader software ecosystem around its models, then investors are more willing to view it as the next-generation AI software platform. If revenue growth is consistently accompanied by massive compute investment and expanding capital expenditures, then the market is more likely to categorize it as a high-growth, high-consumption AI infrastructure company. Both narratives can support high valuations, but they correspond to different valuation multiples and risk tolerances.

OpenAI's presence will make this comparison more apparent, but the two don't necessarily constitute a simple zero-sum competition. OpenAI possesses stronger consumer touchpoints and ecosystem influence, while Anthropic has built a more distinct enterprise, safety, and governance narrative. What the future public market will truly compare might not be who releases a certain model first, but who can more stably convert model capabilities into revenue growth and explain the future to investors with lower uncertainty.