Author: insights4vc

Compiled by: Deep Tide TechFlow

Deep Tide's Take: Robinhood has launched its own Layer 2 chain and "tokenized stocks," seemingly bringing stocks on-chain. However, what users actually get are packaged debt instruments—they hold neither voting rights nor true equity ownership. How far this packaging game can go depends on whether users, developers, and regulators can accept this contradiction of a "simple interface, complex underlying structure."

Robinhood's move is easily misinterpreted if one only looks at the surface. On the surface, the story is appealing: a major retail broker launches a public, Ethereum-compatible, Arbitrum-based Layer 2; it supports wallets, ETH gas fees, bridges, tokenized market exposure, and DeFi integration; it aims to make financial products cheaper, more portable, and more global. This is all largely true.

The real strategic questions lie beneath. Robinhood is building a permissionless financial chain, but the assets that make this chain strategically interesting are not truly permissionless financial objects. They are packaged claims on rights, still bound by law. The chain itself may be freely deployable. Tokens may be transferable between supporting wallets. But the economically meaningful instruments still rely on issuers, prospectuses, custodians, networks of authorized participants, sanctions and KYC controls, jurisdictional exclusions, oracle designs, and legal recourse that looks nothing like direct share ownership.

This is the broker-chain paradox. Robinhood's opportunity lies in hiding this complexity well enough that the products feel simple, global, and useful. Robinhood's risk is that users, developers, and regulators refuse to ignore the underlying complexity. If users think "tokenized stocks" are "stocks," the gap between language and legal reality becomes a product liability issue. If regulators believe the packaging is clear and fairly disclosed, the structure may expand. If they believe the packaging encourages misunderstanding, expansion may stall precisely where the story gets interesting.

Viewed this way, Robinhood Chain is neither a pure crypto experiment nor a simple extension of broker applications. It's an attempt to create a new layer in between: a consumer-facing financial stack whose interface feels intuitive, but whose underlying mechanisms are deeply structured, tightly controlled, and jurisdiction-specific. This is commercially rational. But also inherently fragile. If Robinhood cannot sustain the illusion of simplicity without overstating what users actually own, no part of the strategy will work.

Robinhood's Current Position and Super App Ambitions

Robinhood's launch of Robinhood Chain is not a defensive move. The company is acting from a position of unusual operational strength—for a broker that just a few years ago was viewed by many investors as a cyclical retail trading platform.

Robinhood (NASDAQ: HOOD) plans to release its Q2 2026 earnings after market close on Wednesday, July 29, 2026.

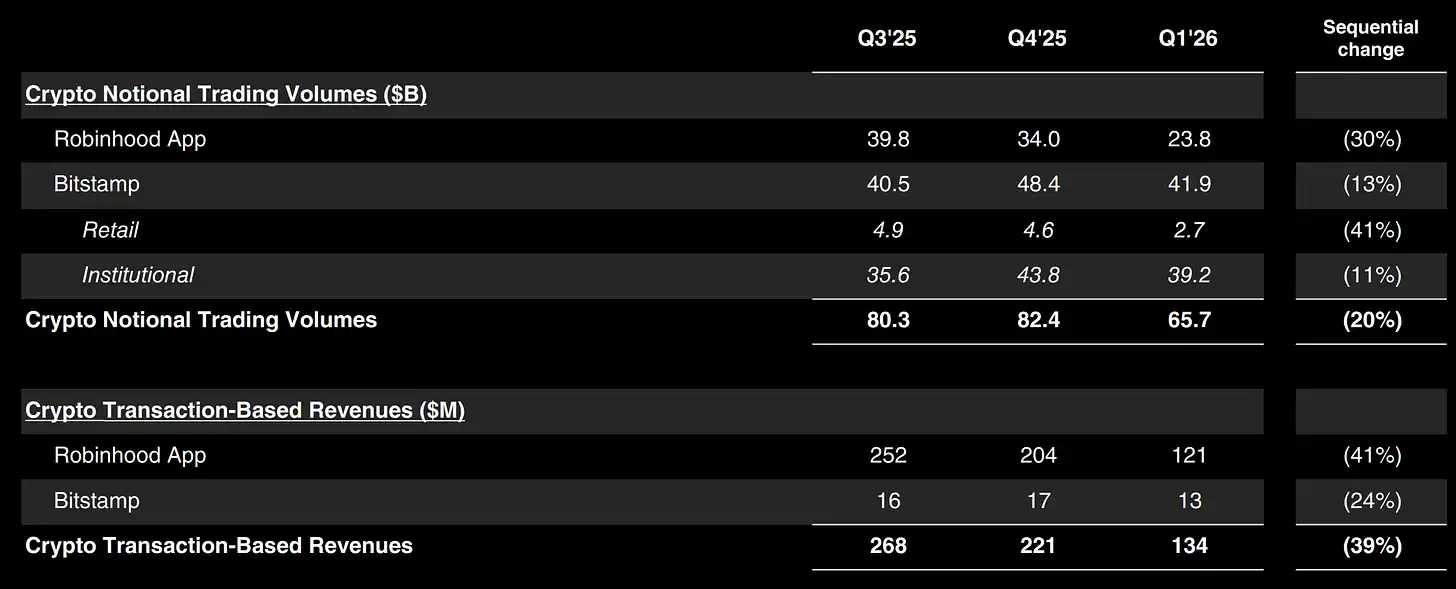

The revenue structure matters because it shows where the business actually monetizes today. In Q1 2026, options generated $260M in transaction revenue, stocks $82M, event contracts $104M, other transaction revenue $43M, and cryptocurrencies $134M. The standout growth line was event contracts, rising from $3M year-over-year to $104M, while crypto revenue fell from $252M to $134M. Therefore, the launch of Robinhood Chain coincides with a time when the company's earnings are still primarily driven by active retail trading, high-margin products, and balance sheet monetization, not by any existing on-chain business line.

This distinction is important for strategy and valuation. Robinhood Chain is not saving the business. It's trying to create a new interface on top of a business that is already functioning. This makes the move more credible because the company has room to experiment. It also makes the move easier to overhype because the existing earnings engine is still rooted in established broker economics.

The rest of the balance sheet and user engagement point in the same direction. Robinhood disclosed a $17B margin book, $16.7B in cash and deposits, $27.4B in retirement assets under custody, and $66B in crypto notional trading volume in Q1 2026, of which $42B came from Bitstamp and $24B from the Robinhood app. This last number is particularly relevant. Bitstamp already makes Robinhood's crypto footprint look more like infrastructure than an isolated retail trading feature.

From Broker App to Financial Super App

The strategic logic of Robinhood now appears more coherent than when the company first began adding disparate products around its core brokerage. In Q1 2026 and subsequent public materials, the company no longer just describes product expansion. It outlines a more complete operating model: brokerage, options, futures, event contracts, banking, Gold, retirement, crypto, wallet, private market access, AI tools, global licenses, tokenized assets, and DeFi-linked yields. Management's talk of building a "global financial ecosystem" is not just corporate speak. It's an attempt to explain how the layers fit together.

The broader stack now includes several parts that would seem incoherent in isolation. Robinhood Banking and higher cash engagement matter because they deepen deposit and balance relationships. Robinhood Gold matters because it increases subscription attach rates and supports premium packaging models. Retirement matters because it lengthens asset lifecycles and dampens pure trading cyclicality. Futures and event contracts matter because they increase engagement and monetization intensity. Crypto matters because it provides 24/7 markets, self-custody rails, and global funding flexibility. Bitstamp matters because it expands institutional and international reach. The wallet matters because it gives Robinhood a credible non-custodial interface. Robinhood Chain matters because it provides a programmable settlement layer where, in principle, all this financial activity can begin to converge.

The company's international direction reinforces the same point. Robinhood's expansion into Canada via WonderFi, its disclosed progress on Singapore regulation, and its description of UK crypto plans. The importance of these steps is not just new territory, but that they create a testing ground for products that don't fully fit within the US retail broker rulebook. Tokenized wrappers and wallet-native products are easier to introduce at the edges of the group than by turning the regulated core of the US app crypto-native overnight.

The strategic sentence is simple: Robinhood Chain matters because it may allow Robinhood to extend its consumer distribution advantage into programmable finance without having to turn its core US brokerage crypto-native overnight. That's why the chain should be read as infrastructure strategy, not launch hype.

What Exactly Is Robinhood Chain

Robinhood Chain's documentation describes it as an Arbitrum Layer 2 chain built on Ethereum, using Ethereum blobs for data availability and ETH as the native gas token. Robinhood Wallet natively supports it, and other EVM wallets can add it manually. Assets can be transferred on-chain using the canonical Arbitrum bridge or partner routing. Public materials also emphasize that the chain is open and permissionless, EVM-compatible, and designed for tokenized real-world assets.

Robinhood's July 2026 launch materials say the chain is built using the Arbitrum platform to "institutional standards" and name Uniswap as the day-one AMM, with Pleiades as a proprietary AMM/proprietary trading venue. Robinhood's technical documentation adds that Stock Tokens are standard ERC-20s, each with a Chainlink price feed, and corporate actions are reflected via on-chain multipliers rather than rebalancing balance changes.

However, public documentation is not equally complete on all infrastructure questions. We found clear docs on connectivity, gas, bridges, token formats, and oracle design, but fewer clear public explanations on sequencer decentralization, governance pathways, fault proof states, or the exact current production roles of each named infrastructure partner. This doesn't mean the system is weak; it means some institutional-grade diligence questions still require more disclosure than the public docs currently provide.

The main takeaway is straightforward. Robinhood Chain is real, but still early. It has infrastructure, partners, and live products attached to it. What it doesn't yet have is proof of sustained liquidity, broad developer adoption, seamless regulatory portability, or material revenue contribution. This distinction matters. A public mainnet and a few live products are enough to take the strategy seriously. They are not enough to prove it.

Stock Tokens and the Legal Reality of On-Chain Stocks

The most important sentence in this article is also the simplest: Robinhood's Stock Tokens should not be described as on-chain stocks. They are tokenized economic exposures to securities through legal wrappers.

Robinhood's on-chain Stock Tokens are described in public materials and prospectus filings as tokenized debt securities issued by Robinhood Assets Jersey Limited. They provide economic exposure to reference shares or ETFs, but users do not obtain direct legal ownership of the underlying securities, beneficial ownership of those shares, or ordinary shareholder rights like voting. The product documentation is clear on this point, and the prospectus framework is clearer than most marketing shorthand around "stock tokens" implies.

The early "Classic Stock Tokens" from Robinhood Europe were legally different again. Those products are described as derivative contracts between users and Robinhood Europe, UAB. They are not transferable to external wallets and can only be opened or closed via the Robinhood Europe platform. The legal boundaries there are even less ambiguous: customers are dealing with derivative exposures, not tokenized claims of holder rights.

The newer on-chain product is more aggressive on distribution but more conservative on legal architecture. That's precisely why it might work. Tokens can behave like crypto assets at the interface layer: on-chain transfer, held in compatible wallets, referenced in DeFi, and priced by oracles. But the underlying claim remains conservative: a Jersey-issued, prospectus-governed, collateralized, limited-recourse debt security referencing underlying shares. Robinhood isn't dismantling securities law. It's packaging around it.

The structure also relies on designated service providers and legal control points. The documents reviewed for the underlying research identify Robinhood Assets Jersey Limited as issuer and tokenizer, Bitstamp Global Ltd. as an authorized offeror in the reviewed terms, and Alpaca Securities LLC as custodian and broker for the reference series. These roles matter because tokenized exposure, aspiring to be globally portable, remains in practice knotted together by highly traditional financial plumbing.

Even the asset-backing story is more complex than the phrase suggests. Robinhood's materials state each token is 1:1 backed by underlying shares. The prospectus framework describes segregated accounts per series but also permits securities lending. During the life of a securities loan transaction, the issuer's economic exposure runs through collateral and contractual rights, not through untouched shares sitting statically in custody. This difference could matter in stress conditions. It introduces borrower, collateral, operational, and recovery-value risks that are alien to the simple intuition a retail user might derive from the product name.

Corporate actions and dividends are similarly indirect. Robinhood's materials explain dividends are handled through a multiplier mechanism adjusting token reference economics, not through direct shareholder distributions to users. The prospectus also flags withholding tax and Section 871(m) considerations for dividend equivalents. Again, this doesn't make the product defective. It makes the product structured. Users should buy this structure with their eyes open.

Transferability is real but not absolute. Robinhood says on-chain Stock Tokens can be held and transferred on supported blockchains and compatible wallets. At the same time, documentation allows for pausing, freezing, and restrictions under certain conditions, and purchase or redemption remains subject to KYC, AML, sanctions compliance, and jurisdictional exclusions. This is closer to a programmable, wrapped, conditional product than an unrestricted bearer instrument.

The business conclusion is straightforward. The product is aggressive on distribution but conservative on legal architecture. This combination is not a flaw. It's likely the only viable route to market. But it also means Stock Tokens should be evaluated as a legal and market structure experiment making economic exposure portable, not as an on-chain replacement for actual stock ownership.

Digital Assets as Infrastructure, Not Just Trading Revenue

Robinhood's digital assets strategy is now too broad to fit back into the old "crypto trading revenue" box. Crypto as a revenue line still matters, but its role as infrastructure is becoming more important. This shift is precisely where the deeper significance of Robinhood Chain lies.

Crypto trading revenue still matters, but it no longer tells the whole story. In Q1 2026, Robinhood generated $134M in crypto transaction revenue, a significant decline year-over-year, despite reaching $66B in crypto notional trading volume. Of that $66B notional volume, $42B came from Bitstamp and $24B from the Robinhood app. In other words, Robinhood's digital assets footprint has already outgrown its consumer crypto label.

Bitstamp is central here. Robinhood completed its ~$200M cash acquisition of Bitstamp in June 2025, explicitly positioning the deal as gaining global exchange capabilities, institutional clients, white-label infrastructure, staking, institutional lending, and broader license coverage. In subsequent filings, Robinhood has already described Bitstamp as extending the institutional side of the business into services like on-exchange lending, OTC settlement, post-trade settlement, and institutional perps. A company doesn't talk this way if it still views crypto as an adjunct to its retail business.

Robinhood Earn makes the same point from the consumer side. Public materials describe a simple flow: users buy USDG on Robinhood Crypto, move it into a self-custody wallet, and then lend via Morpho. Robinhood carefully discloses that the wallet is non-custodial and withdrawal times depend on pool liquidity. The Morpho side describes Robinhood Earn as a progressive rollout to eligible US users. This is more than adding yield to cash balances; it's educating the Robinhood userbase that DeFi can live behind an interface without requiring crypto-native behavior from the customer.

The stablecoin angle matters because it could prove more durable than any single speculative trading cycle. If Robinhood can turn stablecoin balances into an invisible funding rail, it gains a portable, programmable financing layer for wallet-native activity, international flows, and future collateral use cases. In that model, stablecoins are not the product itself but the settlement medium underlying products. That's a strategically more important role.

Robinhood Wallet is the user-side bridge to this tech stack. Supporting materials show the wallet already spans multiple major blockchains and now includes Robinhood Chain itself. This matters because wallet strategy is where broker distribution and crypto infrastructure meet. Brokers can custody, wallets can compose. Robinhood increasingly wants to have both within the same customer relationship.

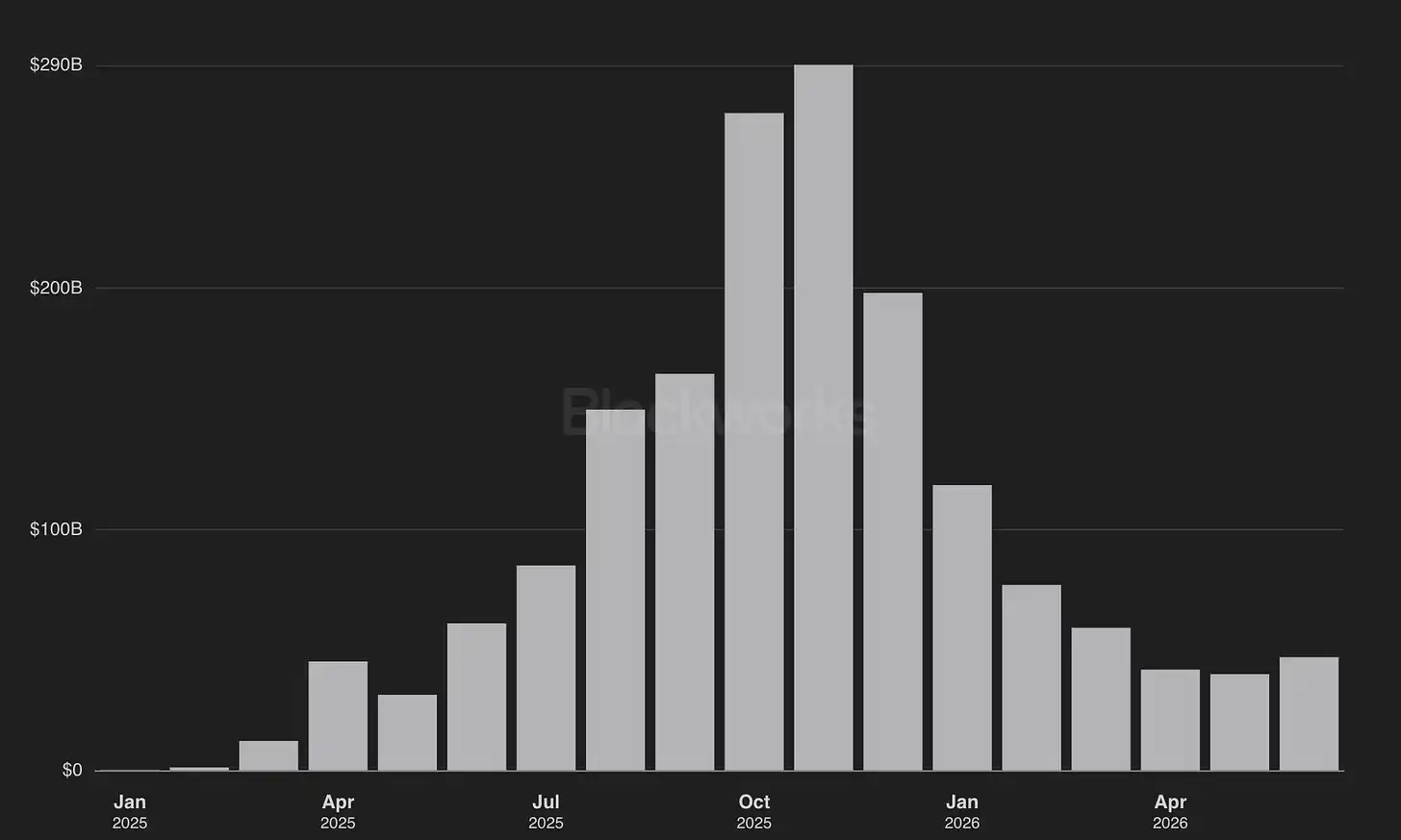

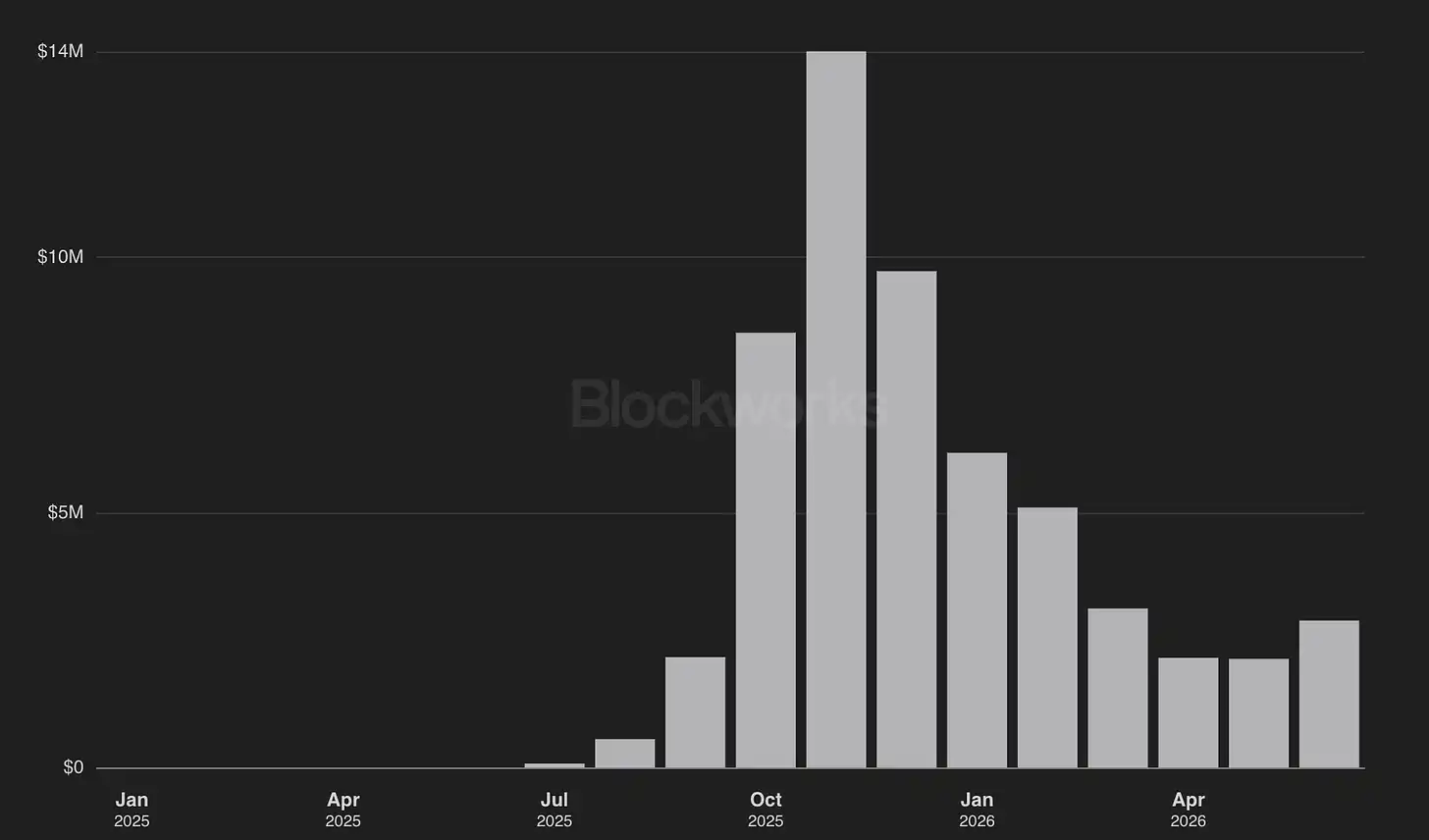

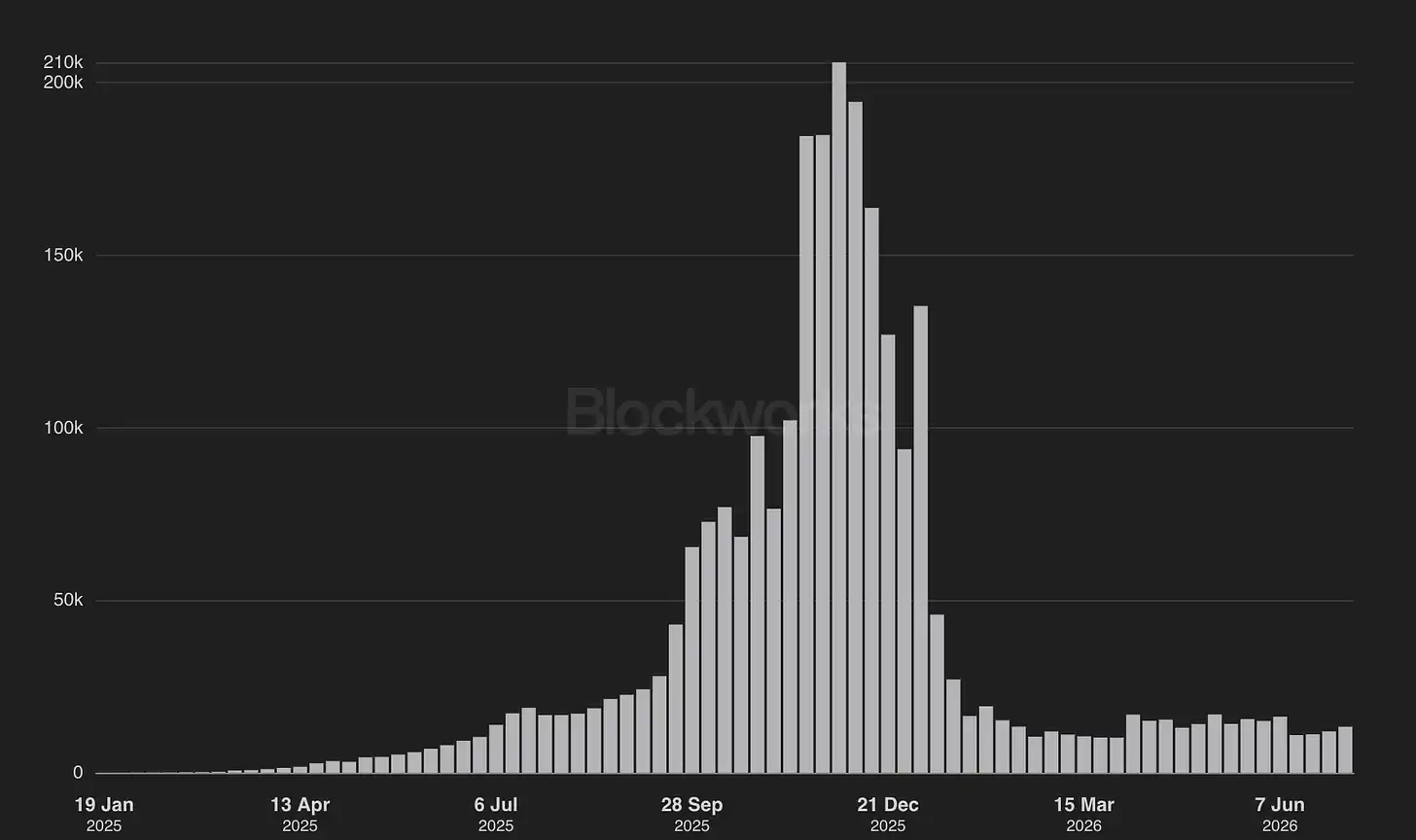

Why Lighter Matters

Lighter is one of the clearest examples of Robinhood's infrastructure positioning. Lighter gives Robinhood access to advanced on-chain trading design without having to build a crypto-native perpetual exchange from scratch. Public materials describe Lighter as a custom zero-knowledge rollup with order matching and clearing proofs, price-time priority execution, and an emergency exit design if certain operations aren't processed on time. Robinhood Wallet materials describe perpetual contracts within the wallet, including liquidation mechanics and funding rate dynamics, with the underlying decentralized protocol responsible for handling liquidations.

Perpetual contracts notional volume (Source: Blockworks)

Revenue (Source: Blockworks)

Traders (Source: Blockworks)

This is useful strategically in several ways. It expands the wallet's engagement surface. It lets Robinhood test high-frequency, high-engagement trading demand in a self-custody environment. It shortens time to market. It exposes Robinhood to the economic model and user behavior of global 24/7 trading without shifting the entire burden onto the regulated US broker architecture.

But Lighter also heightens the brand challenge. Perpetual contracts bring leverage, liquidation, incentive-sensitive liquidity, and retail loss risk closer to the Robinhood ecosystem. Lighter's own documentation explicitly states that RWA markets trade around the clock and use margin mechanisms. This may be commercially attractive, but it's also the kind of product layer that can bring political, regulatory, and reputational friction for a mass-market broker.

So the correct conclusion is narrower than markets might hope. Lighter is not proof that Robinhood can own a perpetuals economy like Hyperliquid, but rather proof that Robinhood can plug crypto-native trading infrastructure into its consumer wallet funnel. This makes strategic sense, but is not the same as owning the trading venue.

Risk Disclaimer:

insights4.vc and its newsletter provide research and information for educational purposes only and should not be considered professional advice of any kind. We do not advocate any investment actions, including buying, selling, or holding digital assets.

The content reflects the authors' opinions only and does not constitute financial advice. Please conduct your own due diligence before engaging with digital assets or related technologies, as they are high-risk and their value can fluctuate significantly.