Strategy CEO Phong Le is calling for a rethink of how banks are required to capital-charge bitcoin exposure under Basel-style rules, arguing that current risk-weighting treatment materially shapes whether regulated institutions can engage with digital assets at all.

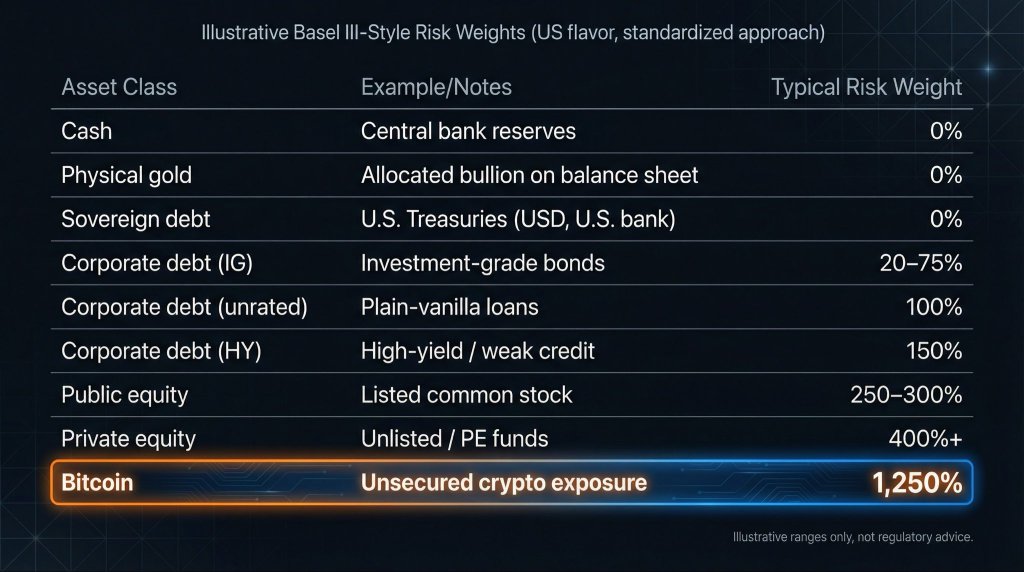

The catalyst was a chart shared on X that labels bitcoin “unsecured crypto exposure” with a “typical risk weight” of 1,250% under an “Illustrative Basel III-Style” standardized approach, alongside 0% weights for cash, physical gold, and US Treasuries.

A Capital Penalty For Bank Bitcoin Exposure

Le framed the issue as structural rather than political, pointing to the way global capital rules flow into national bank regulation. “The Basel Accords set global bank capital standards and risk-weighting rules for assets. These frameworks materially shape how banks engage with digital assets, including bitcoin,” he wrote. “They are developed by the Basel Committee of central banks and regulators across 28 jurisdictions — the US is just one.”

He tied that directly to Washington’s stated ambitions for crypto leadership. “If the US wants to be the Crypto Capital of the World, our implementation of Basel capital treatment deserves careful review,” Le said.

Jeff Walton, who posted the image Le quoted, summarized the contrast in blunt numbers: “Basel III Risk weights for assets: Gold: 0% Public equity: 300% Bitcoin: 1,250%,” adding that if the US wants to be a “crypto capitol,” “the banking regulations need to change,” because “Risk is mispriced.”

The chart itself presents a ladder of “typical” risk weights across asset classes. Cash and central bank reserves sit at 0%, physical gold at 0%, and sovereign debt such as US Treasuries (USD, U.S. bank) also at 0%. Investment-grade corporate debt is shown in a 20–75% range, unrated corporate debt at 100%, high-yield at 150%, public equity at 250–300%, and private equity at 400%+. Bitcoin is set apart at 1,250%.

Conner Brown, Head of Strategy at the Bitcoin Policy Institute, argued that the practical effect is to make bank intermediation of bitcoin prohibitively expensive. “It’s hard to overstate how bad of a policy error this is,” he wrote. “Banks are required to set aside capital based on how risky regulators think an asset is. The higher the ‘risk weight,’ the more expensive it is for a bank to hold.”

Brown described the 1,250% figure as translating into a one-for-one capital requirement relative to exposure. In his words, bitcoin’s treatment “means banks must hold $1 in capital for every $1 of Bitcoin exposure,” while gold is treated “the same as cash” with “essentially no capital cost.”

He also pushed back on the premise that bitcoin should be penalized relative to legacy assets, pointing to operational traits he sees as favorable for risk management and market functioning, including continuous trading, fast auditability of holdings, fixed supply, rapid global settlement, and transparent pricing. The result, he argued, is that regulators have effectively discouraged banks from offering custody and related services that corporates and individuals might prefer inside the regulated perimeter.

Brown said the knock-on effects extend beyond bank balance sheets to competitiveness. He argued the framework diverts activity toward “non-bank entities and offshore jurisdictions,” which he characterized as carrying higher risks, and warned that failing to adjust the approach could leave US institutions at a disadvantage globally.

At press time, Bitcoin traded at $67,857.