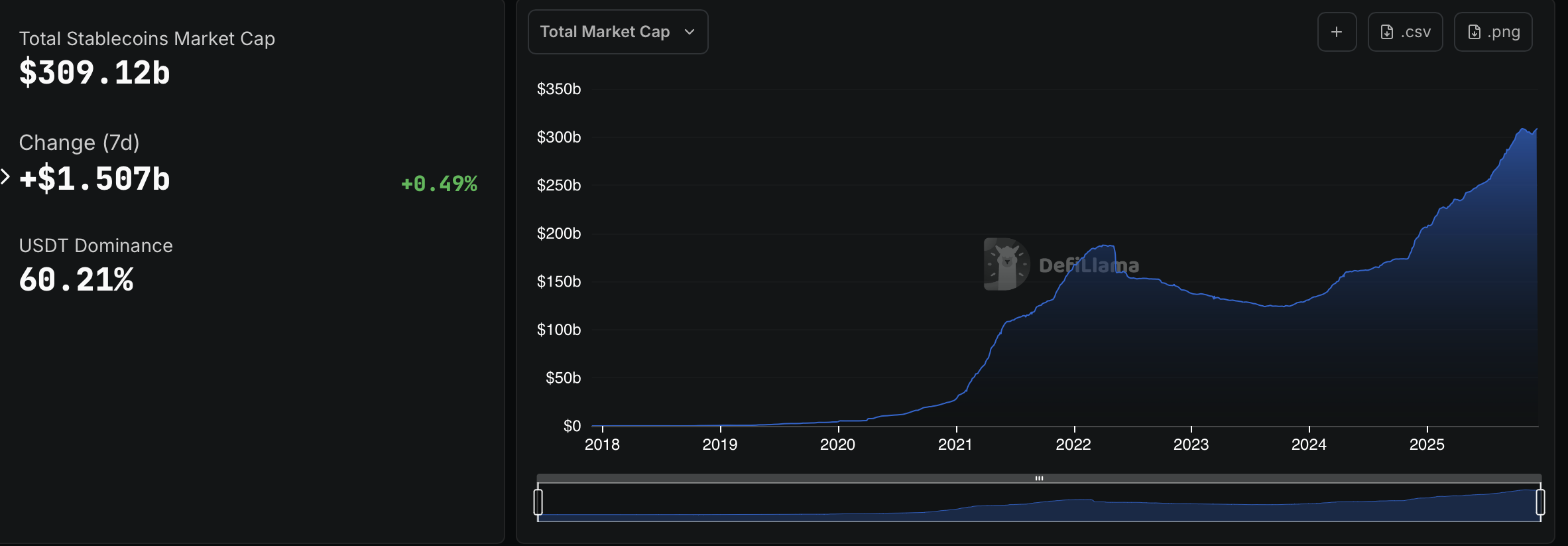

Mexico’s central bank warned in a new financial stability report that “stablecoins pose significant potential risks to financial stability,” citing their rapid growth, links to traditional finance and global regulatory gaps that could fuel arbitrage and magnify market stress.

Stablecoins’ heavy reliance on short-term US Treasurys, market concentration with two issuers controlling 86% of the supply and past depegging episodes with stablecoins underscore how vulnerable the sector remains to stress, according to the Banxico report.

Without coordinated international safeguards, mass redemptions or issuer failures could spill into broader funding markets, the central bank warned.

Banxico also highlighted diverging regulatory approaches as a growing source of risk, noting that frameworks like the EU’s MiCA and the US GENIUS Act impose different reserve, redemption and depositor-protection requirements, creating regulatory gaps that could incentivize arbitrage across jurisdictions.

Banxico acknowledged that stablecoins can improve settlement efficiency, reduce transfer costs and support remittances and liquidity in decentralized finance. However, it plans to keep a cautious distance between the traditional financial system and virtual assets, citing their potential to cause stress in broader markets.

Crypto adoption in Mexico is relatively low. According to Chainalysis’ Global Crypto Adoption Index, the country fell to 23rd place in 2025 from 14th place in 2024 in the adoption ranking.

The central bank’s warning reflects Mexico’s broader cautious stance on crypto. Despite the rise of exchanges like Bitso, the country has not introduced significant new digital-asset legislation and still relies on its 2018 Fintech Law as the primary regulatory framework.

Related: As inflation bites, Latin America banks on stablecoins instead of bankers

Brazil and Argentina lead Latin America in crypto adoption

While Mexico’s central bank maintains a cautious stance on digital assets, other Latin American countries have embraced adoption.

Chainalysis’ 2025 Geography of Crypto Report shows that Latin America generated nearly $1.5 trillion in crypto transaction volume from July 2022 to June 2025, with monthly activity increasing to almost $88 billion by December 2024 from $20.8 billion in mid-2022. Several months in late 2024 and early 2025 consistently exceeded $60 billion.

According to the report, Brazil led Latin America by a wide margin, receiving $318.8 billion in crypto value from July 2022 to June 2025, nearly one-third of all activity in the region, while Argentina ranked second with $93.9 billion in transaction volume.

The central banks of the two leading countries are also taking a more proactive stance in regulating digital assets.

In November, Brazil’s central bank finalized rules that place crypto companies under banking-style supervision, including treating stablecoin transactions and certain self-custody wallet transfers as foreign exchange operations.

In Argentina, a country that has suffered from soaring inflation, the central bank is reportedly weighing whether to allow traditional financial institutions to trade cryptocurrencies in a potential reversal of its 2022 ban, according to a report from La Nación on Friday.

Magazine: Meet the onchain crypto detectives fighting crime better than the cops