Global stock markets recovered after a brief decline, with renewed buying interest in AI-related stocks boosting market risk appetite; at the same time, Iran's announcement of a pause in talks with the United States has reignited tensions in the Middle East, with geopolitical risks continuing to increase their disturbance on markets.

The MSCI World Index rose slightly by 0.1%, staying near its record high, after having fallen as much as 0.2% earlier in the session. Asian stocks rebounded from a drop of up to 1%, climbing 0.3% overall, with South Korea's Kospi—often seen as a bellwether for AI investment—closing up 0.1%, erasing all its losses. Nasdaq 100 index futures narrowed their decline to 0.3%, while Marvell soared over 14% in night trading. European equity futures extended their gains to 0.6%, indicating a return of tech stock buying and a clear improvement in market risk appetite.

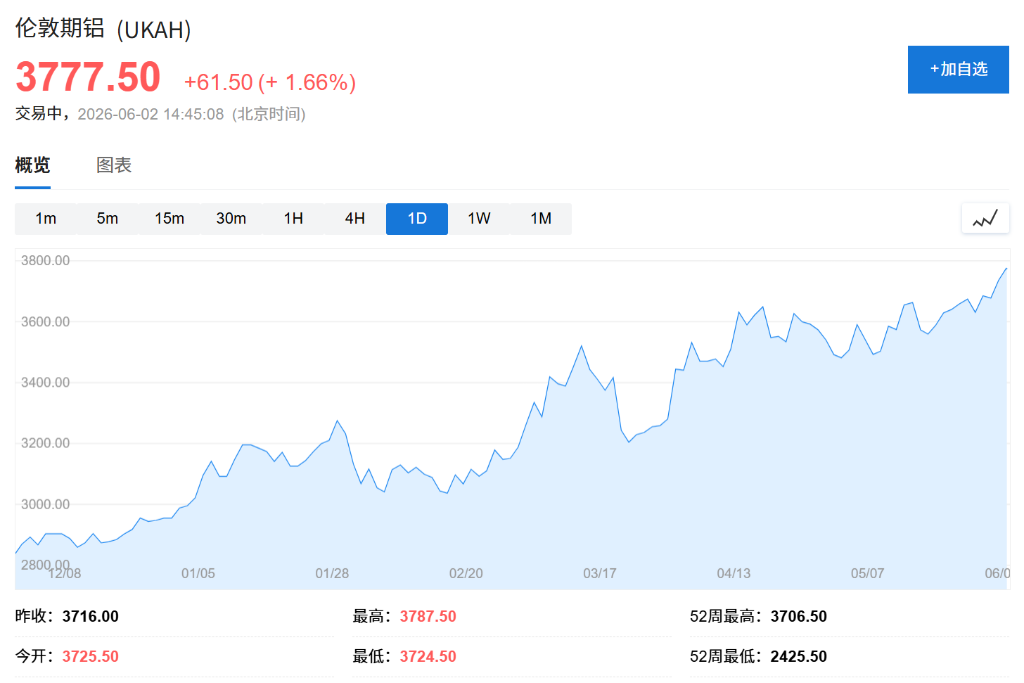

In the commodities market, Brent crude oil hovered near $94 per barrel, and the gold price rose about 1% to $4,523 per ounce. Aluminum prices extended gains for a fourth consecutive day, with London Metal Exchange aluminum briefly hitting $3,775 per ton in early trading, its highest level since 2022. Copper prices rose 0.5% to $13,899.50 per ton. Iran's announcement that it was suspending talks, citing Israeli military actions in Lebanon, further heightened market concerns about potential supply disruptions through the Strait of Hormuz.

Hebe Chen, an analyst at Vantage Global Prime, said: "The AI trade isn't over, but after such a stretched rally, it has become hypersensitive to any headline that could potentially reignite the oil-inflation-rates feedback loop—a loop the market took three months to escape."

- The Nikkei 225 index closed down 0.3% at 66,734.24 points, and the Topix index closed down 0.4% at 3,924.24 points. South Korea's Kospi closed up 0.1%, erasing all its losses.

- Nasdaq 100 index futures narrowed their decline to 0.3%, while Marvell soared over 14% in night trading. European equity futures extended their gains to 0.6%.

- Japan's 10-year government bond yield fell after a well-received bond auction, and US Treasury prices also strengthened slightly.

- The yen held near 159.70 against the US dollar.

- Gold rose about 1% to $4,523 per ounce.

- Brent crude oil hovered near $94 per barrel.

- Aluminum extended gains for a fourth day, with LME aluminum briefly hitting $3,775 per ton, its highest since 2022.

- Copper rose 0.5% to $13,899.50 per ton.

- Bitcoin fell 1.4% to $70,386.76.

Sustained strong demand for AI-related stocks has been the core engine driving global equity markets to record highs this year, helping to offset market volatility stemming from Middle East tensions. The S&P 500 recorded its eighth consecutive session of gains on Monday, its longest winning streak since May 2025. The Philadelphia Semiconductor Index (SOX) has surged about 70% over the past two months and is on track for its strongest quarterly performance ever; the chip sector, by a wide margin, has been the best-performing sector in the S&P 500 this year.

However, some investors are beginning to be wary of stretched valuations. Vikas Pershad, a portfolio manager at M&G Investments, said in a Bloomberg Television interview: "The magnitude of the move that we've witnessed has exceeded our expectations. The direction is not surprising, but given where we are, we've cut back on our exposure to memory chips."

Bloomberg strategist Garfield Reynolds also flagged risks: Momentum has dominated equity markets over the past year, meaning any sharp, swift pullback in major indices could trigger a sustained downturn; and if substantive negative macro factors emerge, the AI-driven rally faces cooling pressure.

Aluminum prices have risen about 25% year-to-date, with Middle East hostilities a key driver. The region is a major hub for global aluminum smelting, with several smelters forced to close or reduce output due to the conflict. Iran's latest announcement to pause talks further unsettled the market about regional supply prospects. At the same time, investors are optimistic about the demand outlook for industrial metals, continuing to pour into copper and aluminum markets.

The tightness in the physical market is clearly visible in the futures structure: On Monday, the premium of the LME aluminum cash contract over the three-month contract reached $111.75 per ton, its highest since 2007, indicating a rapidly widening near-term supply deficit and extremely urgent demand for immediate delivery.

Brent crude oil edged lower near $94 per barrel on Tuesday, having risen on Monday after a phone call between President Trump and Israeli Prime Minister Netanyahu about the Lebanon conflict yielded contradictory accounts. The opposing narratives from the two sides are the latest example of mixed signals regarding ceasefire negotiations. Trump has repeatedly stated that talks are progressing and nearing an agreement, while Iran last week dismissed reports of an imminent interim deal and on Monday said it would coordinate actions with its proxies.

Jason Pride and Michael Reynolds of Glenmede said: "Expectations for a US-Iran deal remain in flux. Recent conflict events and the contradictory statements from both sides indicate that key details remain unresolved."

In other news, the White House announced it would lower tariffs on agricultural machinery such as combine harvesters to reduce production costs for American farmers and manufacturers.

In currency markets, the yen held near 159.70 against the US dollar. Japan's Finance Minister Satsuki Katayama said authorities are ready to take foreign exchange intervention measures if necessary, following the finance ministry's release of monthly intervention data last Friday. Japan's 10-year government bond yield fell after a well-received bond auction, with investors drawn in by the high yields despite lingering Middle East uncertainties. US Treasury prices also strengthened slightly. Among major Asian markets, the Nikkei 225 closed down 0.3% at 66,734.24 points, and the Topix closed down 0.4% at 3,924.24 points.

A busy week of US economic data releases will be another key focus for markets, culminating in Friday's May non-farm payrolls report, from which investors hope to glean clues about the health of the US economy and the policy path of new Federal Reserve Chair Kevin Warsh. Chris Turner, head of FX strategy at ING Bank, wrote in a note on Monday that markets are gradually forming the view that US economic growth is re-accelerating as AI investment spreads deeper into the broader economy, and he expects this week's data to further support the market narrative that "the Fed can comfortably maintain its full employment objective while focusing policy efforts on inflation upside risks."