On March 26, military AI company Shield AI announced the completion of a $20 billion financing round, with its valuation soaring from $53 billion a year ago to $127 billion, a 140% increase. The lead investors were not Silicon Valley venture capitalists but global PE giant Advent International and J.P. Morgan's Security & Resilience Investment division, which jointly contributed $15 billion in equity financing. According to Bloomberg, Blackstone Group injected an additional $500 million in preferred stock and committed to a $250 million delayed draw term loan facility.

The $20 billion financing itself is not the key point; what matters is who is writing this check. This is a snapshot of the ongoing shift in the capital structure of defense technology.

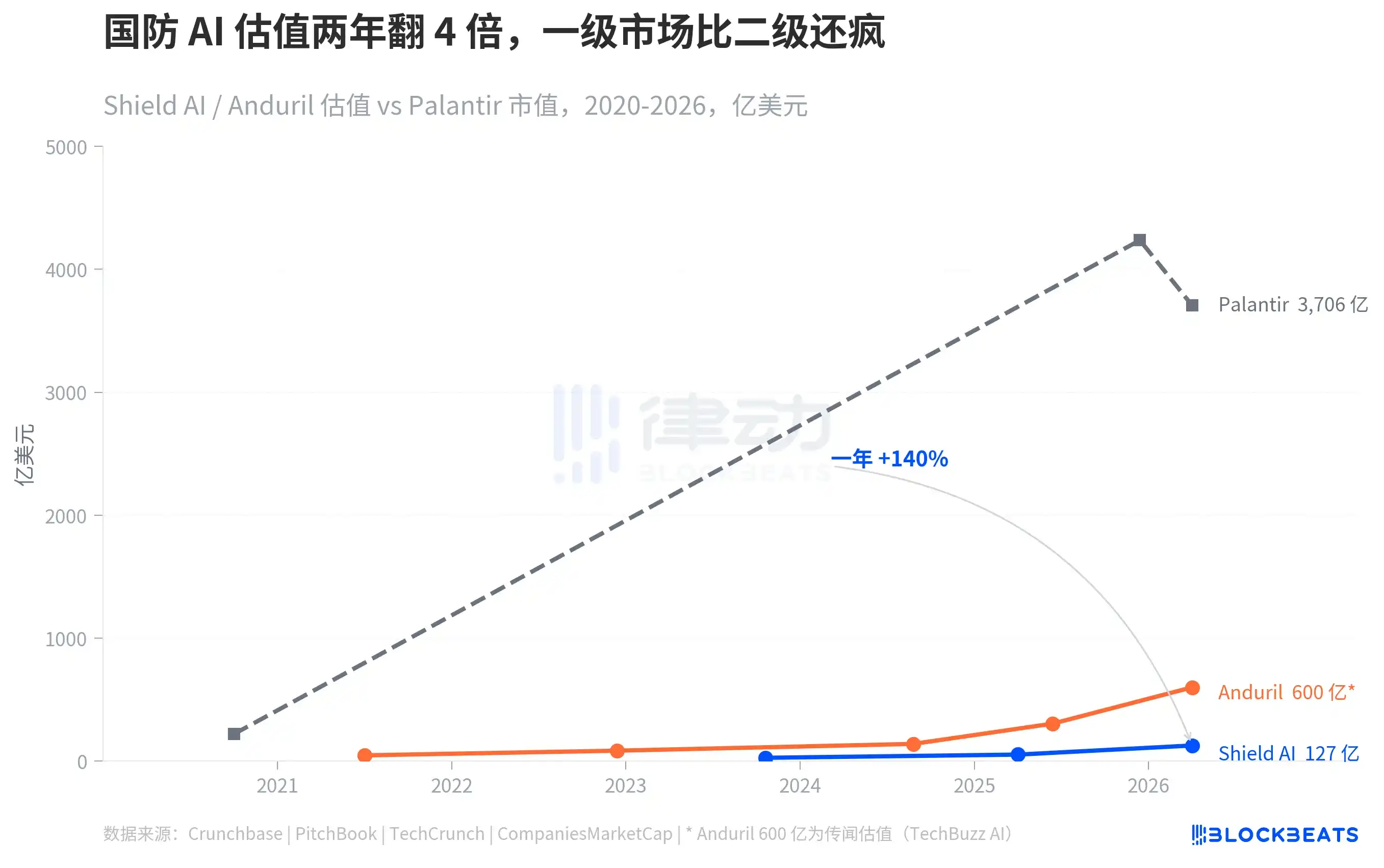

Placing Shield AI and its competitor Anduril on the same timeline reveals a clear trend. In October 2023, Shield AI's Series F valuation was $2.7 billion. Anduril's Series E in late 2022 was valued at approximately $8.5 billion. By March 2026, Shield AI's valuation rose to $12.7 billion, while Anduril, according to TechBuzz AI, is seeking a new funding round at a $60 billion valuation. Both companies have achieved more than a fourfold increase in valuation in just over two years.

The slope of this curve steepened significantly in 2025. According to Sacra estimates, Anduril's revenue reached $2.1 billion in 2025, a 110% year-on-year increase, with a 2026 revenue forecast of $4.3 billion. Although Shield AI has not disclosed its revenue, Tracxn data shows its cumulative financing has exceeded $3 billion. The valuation growth far outpaces revenue growth, indicating that the pricing of defense AI companies has shifted to a "platform expectation" model—valuations are based not on current revenue but on their anticipated position in future military procurement systems.

As a reference, Palantir, the only publicly listed company in the AI defense sector, had a market capitalization of approximately $22 billion at its IPO in September 2020. According to its Q4 earnings report, Palantir's Q4 2025 revenue reached $1.41 billion, a 70% year-on-year increase, with full-year FY2026 revenue guidance of $7.18 billion to $7.20 billion. By the end of 2025, its market capitalization ballooned to over $420 billion. The primary and secondary markets are telling the same story, but the valuation curve in the primary market is even steeper than Palantir's post-IPO trajectory.

Valuation surges are not solely driven by capital expectations. Shield AI has tangible product lines: the MQ-35 V-BAT vertical takeoff and landing reconnaissance drone, already in service, and the next-generation autonomous fighter X-BAT, announced in October 2025. According to DroneXL, the X-BAT costs approximately $27 million per unit, less than a quarter of the price of an F-35, with a range of 2,300 miles. It requires no runway and can take off from a trailer, with mass production planned for 2029.

In February 2026, Shield AI's core AI engine, Hivemind, was selected by the U.S. Air Force to provide mission autonomy for Anduril's Fury drone (designated YFQ-44A) in the Collaborative Combat Aircraft (CCA) program. According to The Defense Post, flight demonstrations are expected in the coming months. In the same funding round, Shield AI also acquired flight simulation software company Aechelon Technology. Aechelon's simulation technology was previously used to train U.S. military pilots. Post-acquisition, Shield AI now controls three key components: training data generation, autonomous flight algorithms, and hardware platforms.

However, what truly steepened the valuation curve is the structural change in funding sources. Shield AI's earlier funding rounds were led by venture capitalists and strategic investors like Andreessen Horowitz and L3Harris. This round's lead investors were replaced by PE giants Advent International and J.P. Morgan, with Blackstone providing preferred stock and debt financing. This is not an isolated case.

According to Bisnow, the U.S. Army has awarded contracts for the construction of two military base data centers to Carlyle and KKR-affiliated CyrusOne, with each project valued at $2 billion and lease terms of up to 50 years. According to S&P Global data, in the first two and a half months of 2025 alone, global PE/VC deal volume in the aerospace and defense sector reached $4.27 billion, with 83% flowing into North America. PE giants are no longer making mere financial investments in the military sector; they are beginning to treat defense infrastructure as a long-term asset class.

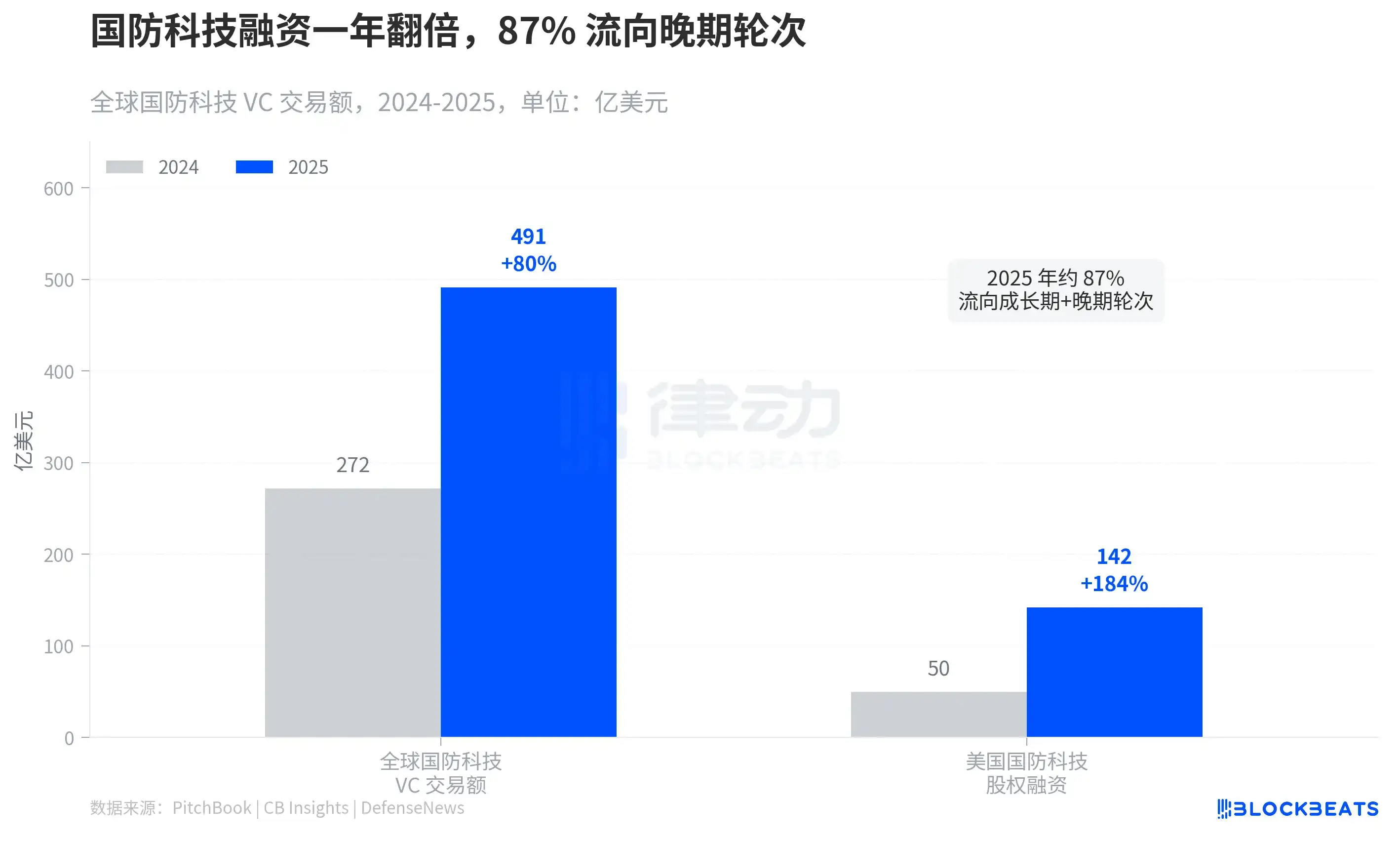

According to PitchBook data, global defense tech VC deal volume reached $49.1 billion in 2025, nearly doubling from $27.2 billion in 2024. According to DefenseNews, domestic defense tech equity financing in the U.S. surged from $5 billion in 2024 to $14.2 billion, an increase of almost threefold. Approximately 87% of this capital flowed into growth and late-stage rounds. Funds are no longer directed at experimental prototypes but toward companies ready for mass production and delivery. According to J.P. Morgan estimates, global defense tech has absorbed approximately $130 billion in venture capital since 2021.

Behind this influx of capital lies a clear buyer signal.

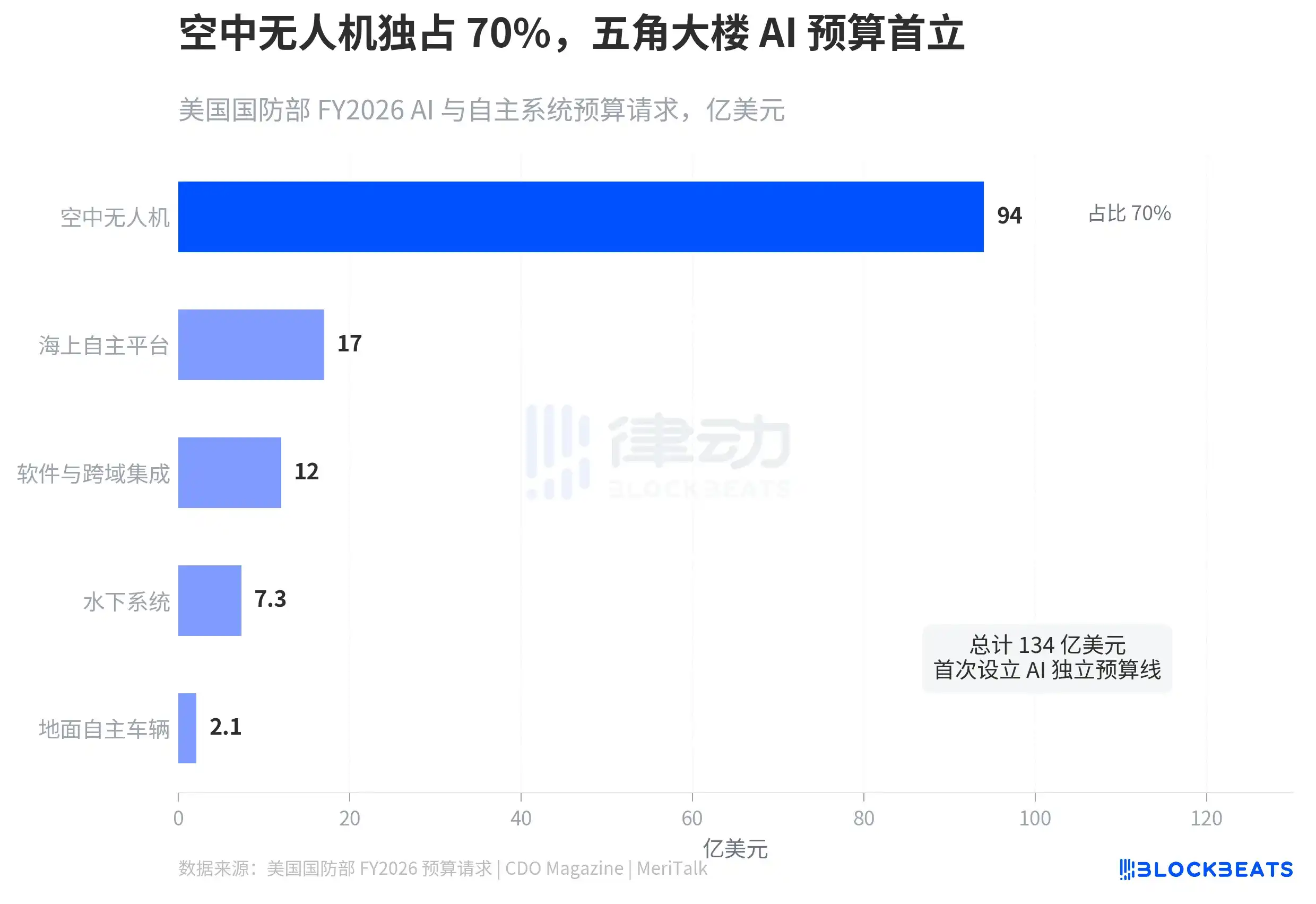

According to the U.S. Department of Defense's FY2026 budget request, the Pentagon has, for the first time, established an independent budget line for AI and autonomous systems, totaling $13.4 billion. Of this, aerial drones account for $9.4 billion, over 70%. Maritime autonomous platforms receive $1.7 billion, software and cross-domain integration $1.2 billion, and underwater systems $730 million. This is a dedicated AI allocation within the FY2026 total budget of $1.01 trillion. Previously, the U.S. military never categorized AI and autonomous systems as independent budget items.

In an AI strategy memorandum released in January 2026, Defense Secretary Pete Hegseth explicitly stated that the U.S. military would become an "AI-first combat force" and listed seven FY2026 priority projects, including autonomous drone swarms and AI-driven kill chain execution systems.

The $9.4 billion budget for aerial drones corresponds precisely to the core product lines of Shield AI and Anduril. The Pentagon is not "exploring" military applications of AI; it is procuring them. The U.S. Air Force's CCA program plans to make its first mass production decisions in FY2026.

When the Pentagon paves the way for AI drone orders with a $13.4 billion budget, and when PE firms treat military bases as infrastructure with 50-year leases, the capital logic of defense technology has shifted from venture capital-style bets on sectors to infrastructure-level asset allocation.