Written by: Ryan Yoon

Compiled by: Luffy, Foresight News

For a long time, discussions in the crypto industry have remained confined to the stablecoin issuance stage. The operational data of leading issuers like Tether and Circle, as well as regulatory policies from various countries, have been seen as the sole barometers for the industry, but this is merely the starting point of the stablecoin industry chain.

The complete stablecoin industry chain covers the entire commercial flow of funds after token issuance and is divided into five segments: issuance, fiat on/off-ramps, on-chain transfers, payments, and yield generation.

Analyzing from the perspective of the entire industry chain, it's easy to see that the stablecoin issuance market is monopolized by a few giants, but downstream segments have numerous participants, harboring vast incremental market opportunities.

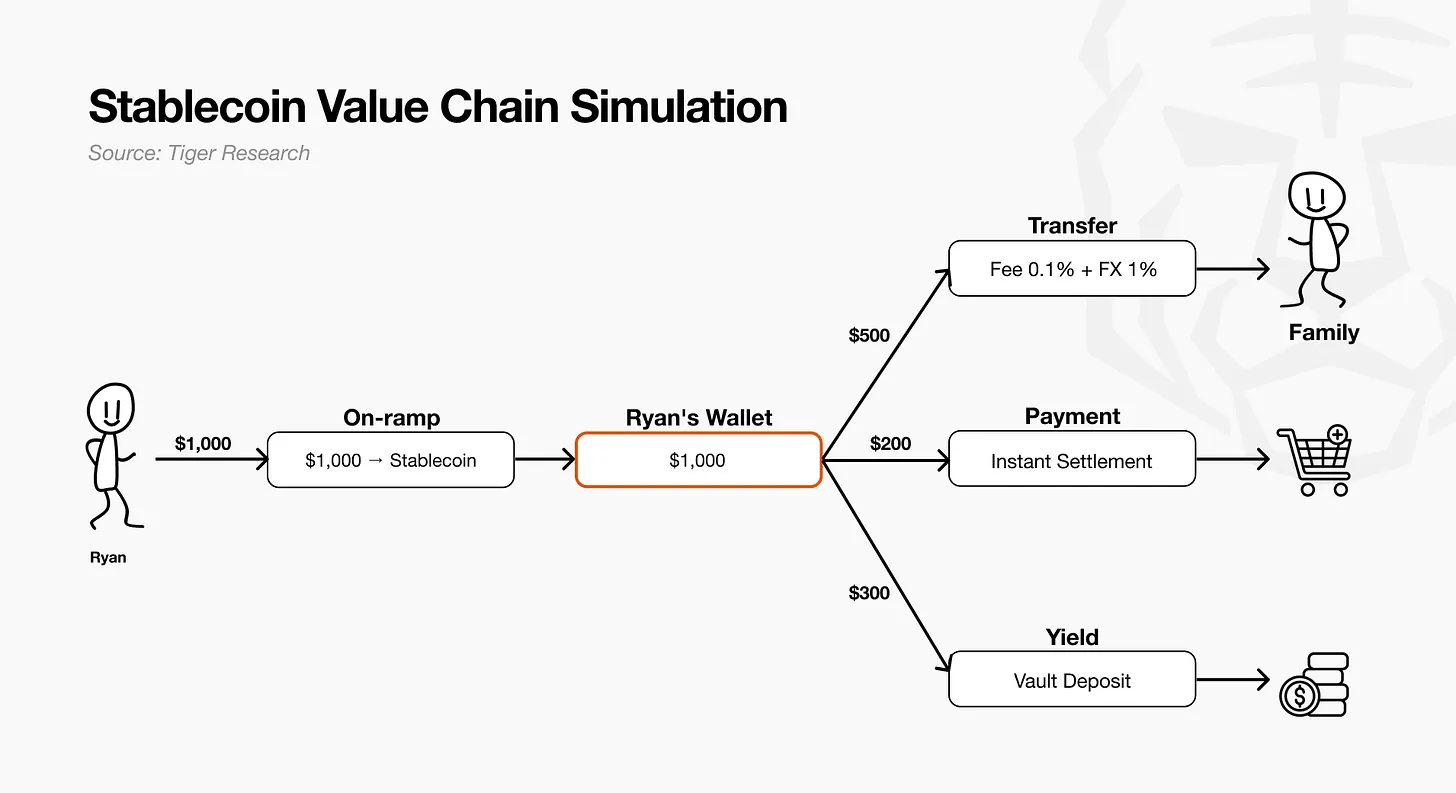

From Issuance to Yield: Tracking $1000

Let's take an account with $1000 as an example to outline these five industry chain segments, providing an intuitive understanding of the business logic at each stage.

- Issuance: Leading issuers mint stablecoins backed by assets like US Treasuries, providing ample liquidity to the market.

- On/Off-Ramps: Users exchange $1000 in fiat for stablecoins through on/off-ramp service providers, who complete the conversion and transfer the tokens to the user's wallet. Funds officially leave the traditional fiat system, becoming on-chain liquidity.

- On-chain Transfer: The user sends $500 in stablecoins to family in Mexico for living expenses. The transfer system achieves second-level settlement, and the recipient exchanges it for local currency for daily spending.

- Merchant Payment: The remaining $200 is used for offline consumption, with the payment layer completing real-time settlement.

- Asset Appreciation: The final $300 of idle funds in the wallet is deposited into a yield vault, continuously generating returns as a financial asset.

This $1000 completes the entire process from fiat exchange to stablecoin, cross-border payment, offline consumption, and asset appreciation. Each link the funds pass through corresponds to a commercialized scenario within the stablecoin industry chain.

Issuance Segment

Stablecoin issuance exhibits strong economies of scale. Industry barriers are built on brand trust and liquidity. Tether and Circle, as first-mover giants, have formed an oligopoly. New entrants must break away from the single model of earning reserve interest and build differentiated competitiveness.

Industry Landscape

Stablecoin issuance involves minting and burning tokens backed by reserves like US Treasuries, pegging their value to fiat currency. The total market size is approximately $3000 billion, with USD stablecoins accounting for 99.99%. Tether and Circle collectively hold an 83% market share, with economies of scale continuously strengthening: the more ample the liquidity, the higher the transaction convenience and market trust.

As the industry matures, the originally integrated business of issuers has begun to split. While issuers appear as single entities, four major internal functions are already handled by different institutions: compliance licensing, reserve asset custody, token minting/burning, and channel distribution. Issuers outsource most of the actual operational work. For example: Circle delegates significant distribution business to Coinbase; Tether entrusts reserve custody work to Cantor Fitzgerald.

Business Models

- Reserve Interest Model: Core revenue comes from investment returns on reserve assets, where leading issuers Tether and Circle hold significant advantages.

- Payment Fee Model: Revenue stems from token payment and settlement fees. Profitability depends on transaction activity, not issuance market cap.

- Issuance-as-a-Service (IaaS): Does not directly issue stablecoins but provides infrastructure and compliance licensing externally, earning spreads. Growth relies on network effects rather than pure scale expansion (Paxos, Bridge).

- Regional Exclusive Stablecoins: Early layout in regulatory gray areas and non-USD stablecoin tracks to lock in localized liquidity (e.g., KRWQ Yen stablecoin, JPYC Korean Won stablecoin).

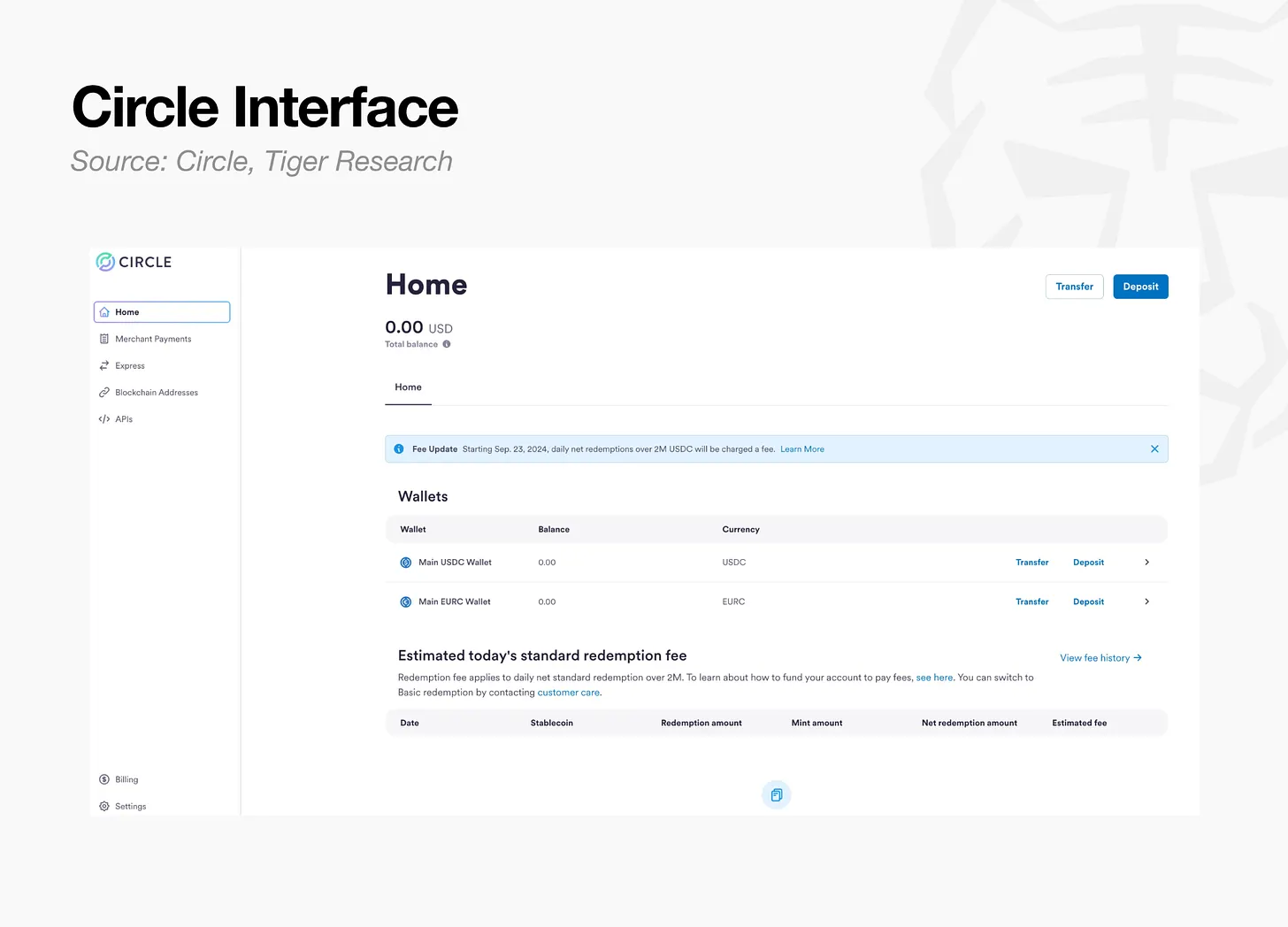

Case Study: Circle

Institutional clients deposit US dollars with Circle, which mints USDC at a 1:1 ratio. Circle's core revenue comes from interest on deposited reserves; therefore, it does not charge separate fees for minting. The business core is maximizing the scale of non-interest-bearing deposited funds. Client deposits are held in the Circle Reserve Fund, a US SEC-registered money market fund managed by BlackRock, paired with cash-like assets, primarily invested in short-term US Treasuries.

Circle distributes reserve interest through channel-sharing agreements. In August 2023, it signed a cooperation agreement with Coinbase with the following interest-sharing rules:

- USDC held on the Coinbase platform: 100% of corresponding reserve interest goes to Coinbase.

- USDC held on Circle's own platform: 100% of corresponding reserve interest goes to Circle.

- USDC circulating outside these two platforms (third-party exchanges, individual/institutional wallets, DeFi protocols): Reserve interest is split 5:5 between the two parties.

This mechanism is a carefully designed channel incentive strategy, ceding part of the issuance revenue to core distribution partners in exchange for maximizing the circulation scale of USDC across the entire ecosystem.

Industry Insights

Stablecoin issuance is a scale-driven track where first-mover advantage and liquidity volume are decisive. The barrier to direct entry for new players is extremely high. New entrants should not focus on issuance but seize opportunities from the industry's professional fragmentation, building irreplaceable middleware capabilities in single segments like compliance licensing, asset custody, settlement infrastructure, or distribution channels.

The future core of industry competition is no longer "who issues the larger stablecoin," but who can capture value across the entire flow and usage chain of stablecoins, occupying key ecosystem positions.

On/Off-Ramp Channels

On/off-ramp service providers earn revenue from transaction fees and exchange spreads. User actual fees vary by payment channel: bank transfer 2%-4%, bank card 4%-7%. According to Banxa data, the service provider's actual net fee rate is about 3%. Exchange services are highly homogeneous, leading to intense competition, giving rise to aggregator platforms that automatically match the lowest-cost exchange channels.

Industry Landscape

This segment includes two types of entities: on/off-ramp service providers for fiat-to-crypto exchange, and wallets/custodians for asset storage. They are deeply intertwined, with the former handling fiat-to-on-chain asset conversion and the latter responsible for asset custody. Revenue relies on transaction volume-driven fees and spreads. However, the exchange function lacks differentiation; service provider products are highly similar, and industry net fee rates are gradually converging to around 3%.

Business Models

- C2C Direct On/Off-Ramps: Provide exchange services directly to end-users, earning fees and spreads. Highly homogeneous. Competitiveness depends on global compliance license coverage, payment channel richness, brand reputation, and conversion efficiency (MoonPay, Ramp Network, Banxa).

- B2B White-Label Model: Embeds on/off-ramp infrastructure into wallets/apps, sharing ~1% transaction fee with partners. No need to build a C2C-facing brand. Deep integration with major partners creates a moat through high switching costs (Transak).

- Aggregators: Connect to multiple on/off-ramp service providers, automatically matching the optimal exchange path, earning intermediary service fees. Value increases with the number of connected providers but is highly dependent on the partner network, presenting limitations (MELD).

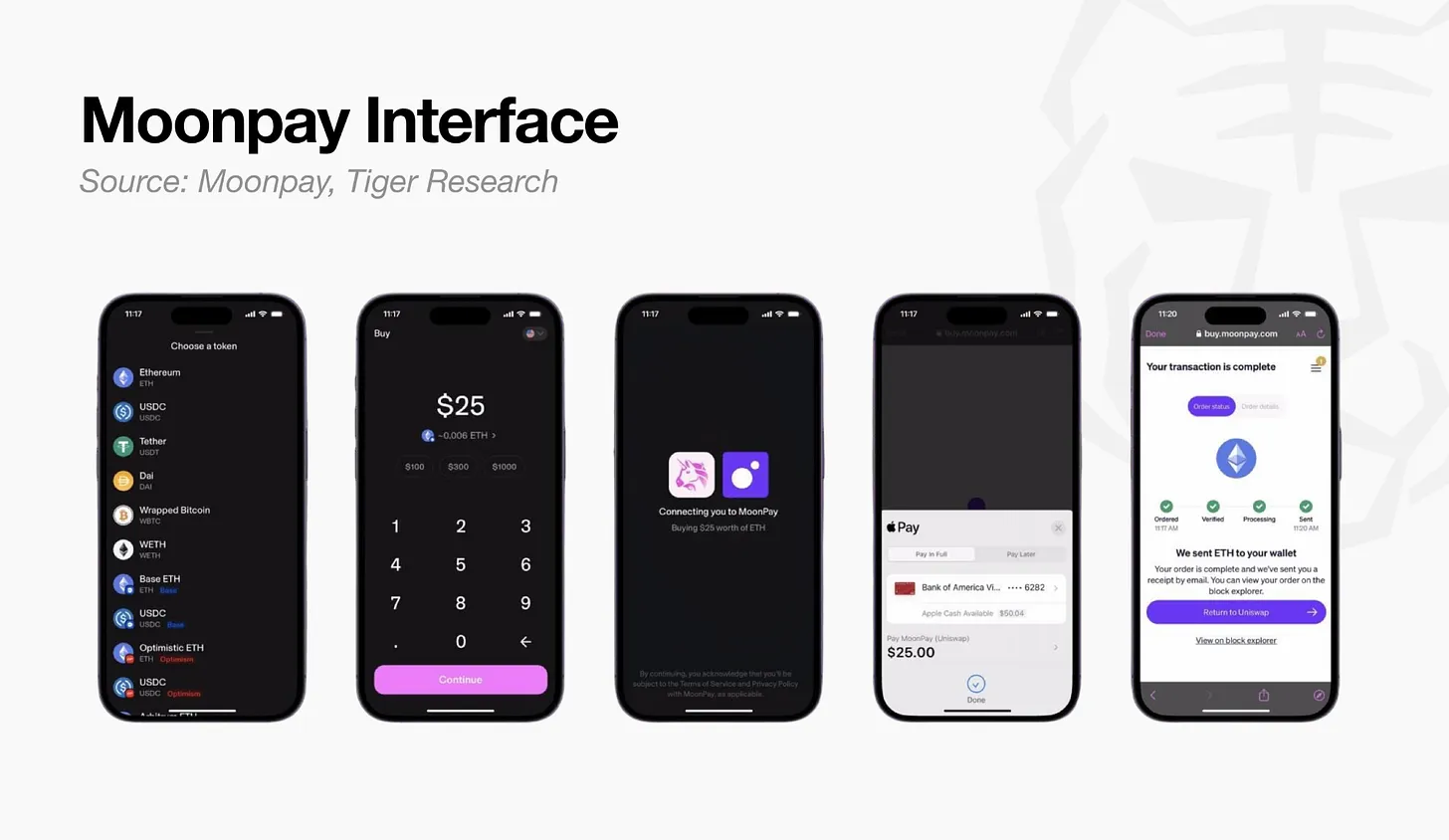

Case Study: MoonPay

MoonPay is a non-custodial on/off-ramp platform where users' crypto purchases are directly transferred to their own wallets. Core revenue comes from transaction fees and exchange spreads: bank transfer fee 1%, bank card up to 4.5%, minimum fixed fee of $3.99 for small transactions. Official fees are divided into three tiers, clearly reflecting MoonPay's revenue allocation and channel-sharing logic.

Revenue comes from two main sources: its own traffic and embedded transactions in third-party apps. Its core strategy is to embed exchange services into over 500 wallets and applications, allowing partners to set their own fees, efficiently expanding a large-scale distribution network while sharing revenue with channels.

Industry Insights

The profit margin for standardized on/off-ramp fee business continues to face pressure, with price wars constantly compressing gross margins. For long-term sustainable operation, one-time fee revenue must be transformed into stable, recurring cash flow. Therefore, C2C on/off-ramp service providers are extending downstream into issuance and settlement infrastructure. MoonPay's acquisition of Iron and launch of customized stablecoin issuance services align with this direction, though the effectiveness of this recurring revenue model remains to be proven.

The "embedded" strategy has led to two outcomes: some service providers develop independently, building proprietary moats (Transak, Turnkey); others are acquired by large payment/custody companies, e.g., Privy by Stripe, Dynamic by Fireblocks. It's still unclear which path will become mainstream, but on/off-ramps and wallets are indispensable key hubs for the entire industry.

On-chain Transfer Segment

This segment handles stablecoin transfers between entities, including personal transfers, cross-border corporate salary payments, etc. The appeal lies in the directly quantifiable cost advantage of stablecoins for cross-border transfers. Traditional cross-border transfers average over 6% in fees, while stablecoins can significantly reduce costs.

Industry Landscape

Both ends of the fund exchange (USD to stablecoin, stablecoin to local fiat) incur fees and FX spreads, but the cost of on-chain token transfer is nearly zero. Industry revenue focus is not on the transfer action itself, but on the exchange at both ends and compliance licensing for cross-border transfers. Obtaining a US state Money Transmitter License (MTL) takes 12-24 months, making the "compliance-as-infrastructure" licensing rental model a popular profit channel.

Business Models

- Cross-border B2B Infrastructure: Builds enterprise cross-border payment settlement systems, charging 5–10 basis points transfer fee + FX spread (varying from tens of basis points to ~1% depending on remittance channel and scale). Some go further by issuing their own stablecoins to earn reserve interest, e.g., Bridge's open issuance model (Bridge, BVNK, Conduit).

- Payroll Distribution Platforms: Specialize in global employee salary payments, directly connecting companies and employees. Revenue has two layers: SaaS monthly subscription fee (fixed per employee or ~25 bps withdrawal fee); plus earning interest on idle funds from pending salaries, similar to Rise Earn (Rise, Toku).

- Personal Cross-border Transfers: Target C2C personal cross-border remittances, leveraging stablecoins to reduce backend costs, setting uniformly low fees to create a price gap vs. traditional providers (Félix Pago).

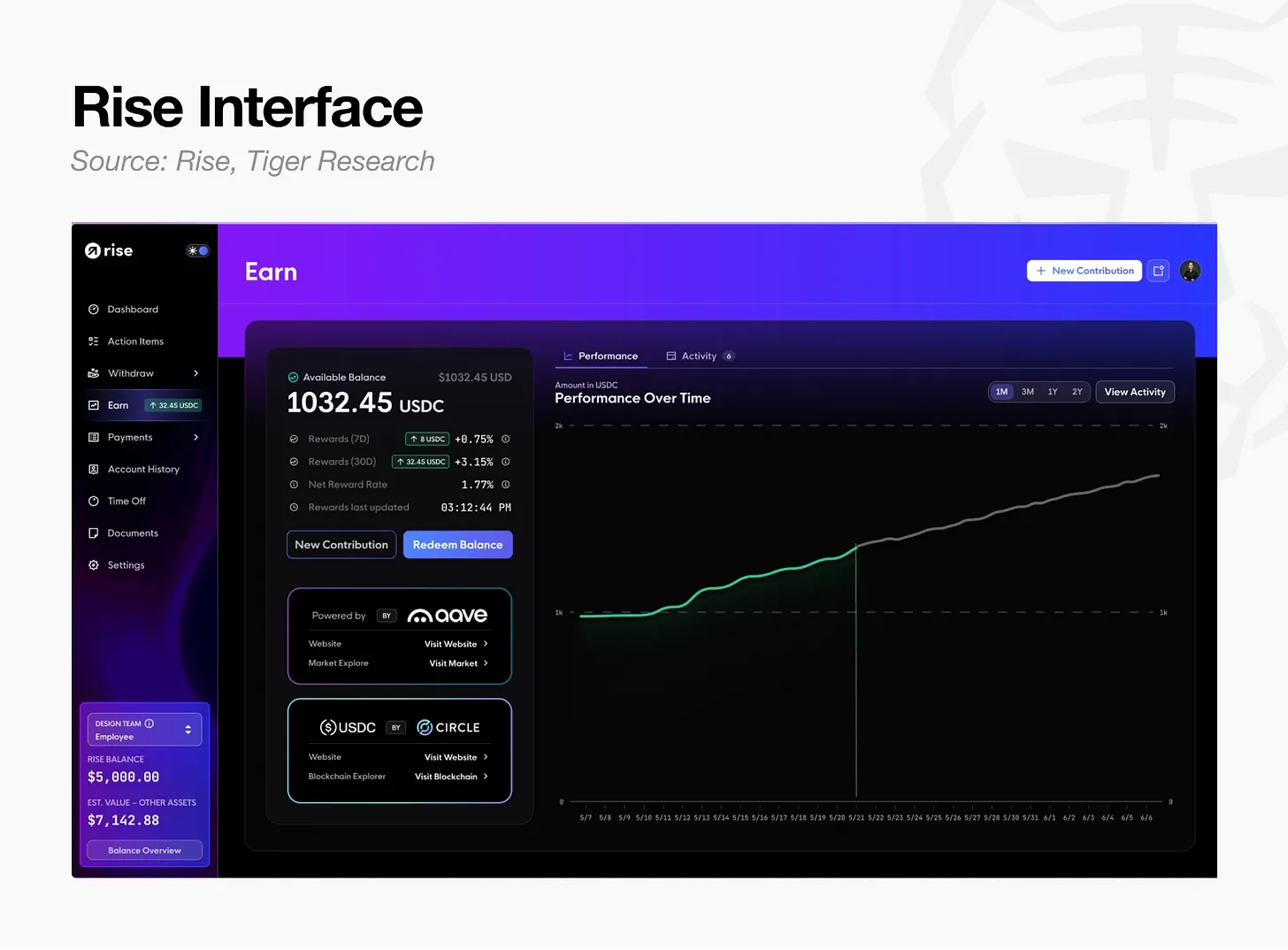

Case Study: Rise

Rise is a stablecoin payroll platform. Companies can pay salaries in USD or USDC. Employees can choose from over 90 fiat/stablecoin withdrawal channels monthly. The platform has processed $15B cumulatively, with over half of withdrawals choosing stablecoins. The platform's core收费 is not token transfer, but managing the entire employment lifecycle: automated KYC/AML, compliant employment contracts per country, tax document generation, charging ongoing subscription fees.

Rise's revenue is three-tiered, synchronized with payroll fund flow:

- Subscription & Transaction Fees: Companies choose one: fixed $50 per employee monthly subscription, OR 3% of salary total + $2.5 per transfer fee. Salaries are paid monthly, ensuring stable recurring revenue.

- Compliant Employment Entity Service: Platform acts as the legal employer, bearing employment risks, charging $399 per person monthly. Premium comes from underwriting compliance risk, not transfer功能.

- Idle Fund Appreciation: Pre-deposited salaries from companies and USDC held by employees before withdrawal are all deposited into Arbitrum's on-chain Aave lending pool. No custody fees for deposit/withdrawal, taking a 1% share of generated interest upon withdrawal, officially launched March 2026.

Monthly salary payments naturally create pools of idle funds (pending payout, unwithdrawn). Rise's three-tier收费 logic progresses layer by layer: from employment relationship subscription, to compliance risk underwriting, to idle fund appreciation, avoiding unprofitable pure transfer收费.

Industry Insights

The ultimate winner in cross-border transfers will not be the service provider with the lowest transfer cost, but the comprehensive platform that integrates exchange at both ends, compliance licensing (Mural Pay, Yellow Card), captures user employment relationships (Rise), and adds yield generation (Rise Earn). Mastercard's up-to-$1.8B acquisition of cross-border payment provider BVNK indicates ongoing consolidation in transfer and payment settlement infrastructure.

Payment Segment

Payments are a core scenario in the industry chain, using stablecoins for goods/services settlement. Merchant acquiring and bank card business are main drivers, but industry commercialization maturity lags market expectations. The velocity of on-chain stablecoin retail circulation is only one-twentieth of traditional M1 money supply: user funds are deposited once and spent intermittently, lacking the closed-loop cash flow of salary deposits + daily spending.

Industry Landscape

Bank card interchange fees are a core payment revenue stream, growing with transaction volume. However, retail transaction frequency is relatively low, making single-card profitability thin, with revenue split among card networks, issuers, and payment gateways. The truly high-margin环节 is not the front-end C2C card brand, but the back-end issuing and settlement infrastructure. Most消费卡 service providers lack their own issuing licenses, heavily relying on underlying infrastructure, limiting revenue to exchange spreads.

Business Models

- Payment Infrastructure Providers: Build merchant acquiring and settlement systems. Besides payment fees, they can issue their own stablecoins to earn reserve interest. Stripe's Bridge open issuance, replicating Circle's reserve-sharing model, is one of the most profitable activities in this segment (Stripe, BVNK).

- Bank Card Issuing Infrastructure: Provides back-end for branded card issuance to wallets, exchanges, neobanks. As a Visa/Mastercard principal member, shares interchange fees, earns program management fees and FX spreads. Core differentiation: using USDC for real-time on-chain settlement reduces collateral requirements by up to 60% vs. traditional models, significantly improving capital efficiency (Rain, Reap).

- C2C Bank Cards & Neobanks: Provide bank cards and accounts to users. Revenue from interchange fee sharing, FX spreads, membership subscriptions, yield on deposited funds. Lack own issuing licenses, limiting access to reserve interest; mostly rely on infrastructure providers like Rain, Reap (Cypher, KAST).

- Card Networks: Handle transaction authorization and settlement. Interchange fees belong to issuers; networks earn per-transaction network service fees growing with volume. Major networks embed stablecoin settlement into their infrastructure, deepening ties with partner banks (Visa, Mastercard).

Case Study: Rain

Rain is a B2B back-end infrastructure provider, enabling wallets, exchanges, neobanks to launch their own branded消费卡. Partners只需 integrate via API; Rain, as a Visa/Mastercard principal member, handles licensing, compliance, and full issuing operations.

The complete process for a user spending offline with a Rain-powered card:

- Real-time Authorization: Like traditional cards, goes through Visa/Mastercard network;商户 and consumer are unaware of stablecoin底层.

- Real-time Balance Deduction & Accounting: User's on-chain assets are converted and deducted in real-time; Rain manages accounting across all programs.

- Daily Network Settlement: Rain settles entirely in USDC with card networks,不受 bank settlement cutoff times, operating 365 days/year, no weekend/holiday delays.

- Liquidity Utilization: In credit models, user repayment lags settlement, creating funding gaps. Rain tokenizes credit card receivables, using them as collateral for on-chain borrowing to prefund settlement, cumulatively循环借贷 over $175M, reducing collateral needs by 60% vs. traditional issuers.

In short, consumers experience seamless刷卡; Rain handles all back-end authorization, settlement, and funding operations.

Industry Insights

The core profit point in payments is not the直观的刷卡手续费, but the reserve interest enabled by issuing licenses and the improved capital efficiency from T+0 real-time settlement. Most消费卡 brands are merely front-end customer acquisition channels,全部 relying on underlying infrastructure providers.

Leading card networks directly acquire cross-border payment infrastructure like BVNK. Visa, Mastercard, Stripe, Google jointly launching the stablecoin alliance Open USD aims to vertically integrate their own settlement systems, safeguarding独家 reserve interest收益.

Asset Appreciation Segment

Appreciation is the final segment of the industry chain and has the most complex business models. Reserve interest that issuers cannot distribute to users eventually flows back to holders here. On-chain lending has evolved into a complete on-chain asset management industry.

Industry Landscape

Early on-chain lending pooled funds into单一 liquidity pools, where单一 asset default risk could spread system-wide. Modular, isolated architectures are now prevalent, segregating collateral and terms across different markets, decoupling underlying fixed lending protocols from yield vaults operated by risk managers.

This layering has spawned an independent on-chain asset management track: Risk managers, analogous to traditional asset managers, charge vault management fees (up to 5% APR) and performance fees (up to 50% of profits). The top four players control ~65% of vault TVL, forming an oligopoly.

Building on this appreciation infrastructure, a variety of end-user financial products flourish: tokenized US Treasuries, private credit等 RWA products, yield-bearing synthetic dollars, restaking.

Business Models

- Lending Protocols: Earn spread between deposit and borrow rates, or generate protocol revenue via own stablecoin issuance, e.g., Aave's GHO. Morpho's model removes protocol fees, directing all收益 downstream to risk managers and token ecosystems in exchange for network scale growth (Aave, Morpho).

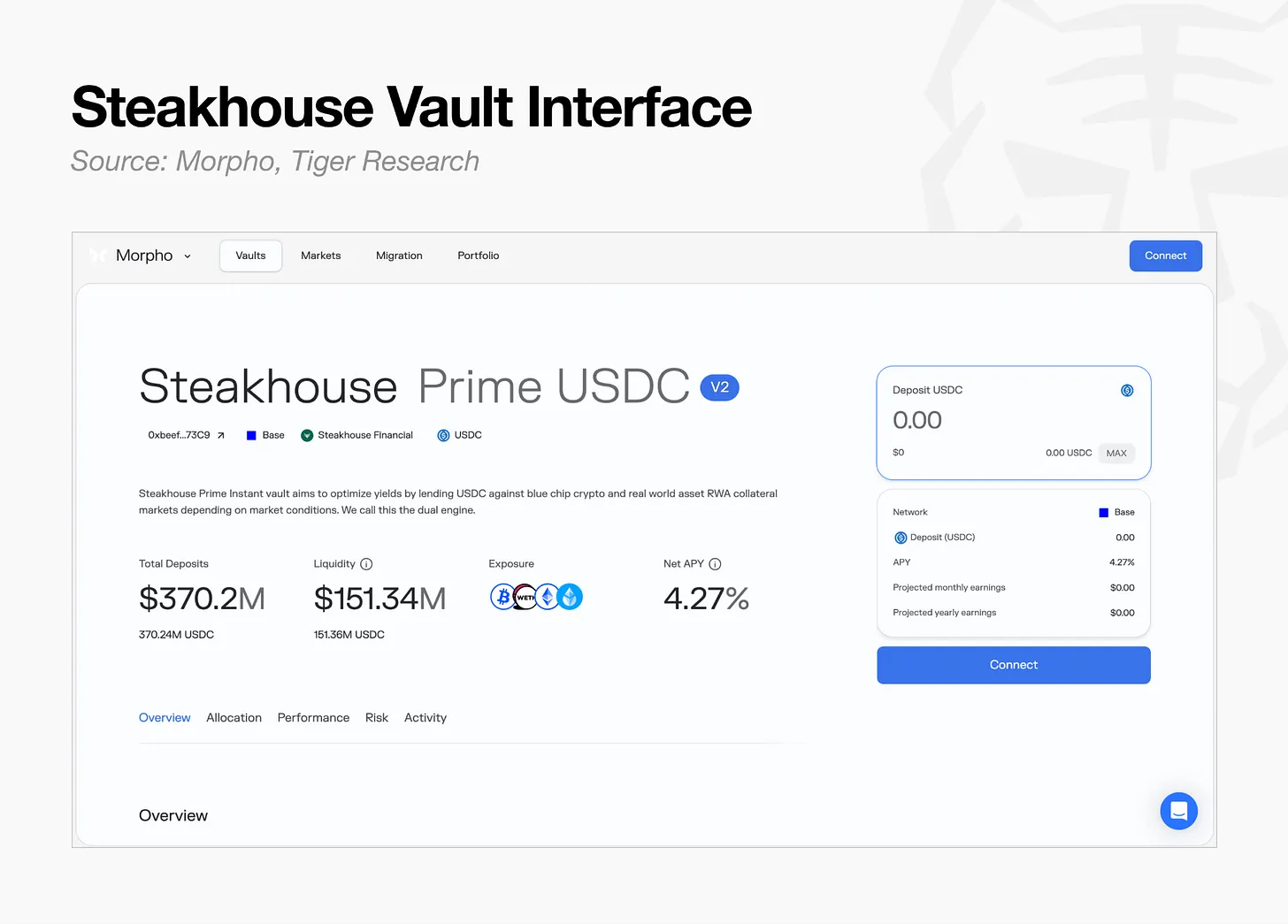

- Risk Managers: Build asset allocation and risk models on top of lending protocols, charging vault management fees. Example: Steakhouse, a team of <20, manages $1.7B AUM, taking ~5% of generated interest, with运营成本 far lower than traditional financial institutions (Steakhouse, Gauntlet).

- RWA Yield Vaults: Issue/distribute tokenized US Treasuries/money market funds, charging 0.15%-0.5% annual management fee. BlackRock's BUIDL as underlying, Ondo Finance packages for DeFi access, Plume Nest distributes via RWA-specific blockchain (BUIDL, Ondo, Nest).

- Yield-bearing Synthetic Dollars: Generate收益 through delta-neutral basis trading, floating net interest spreads, distributing interest to token holders.分为 crypto derivatives收益 and Treasury-backed routes (Ethena, Sky).

- Restaking: Unlocks liquidity from already staked assets to earn额外收益. Some providers achieve full vertical integration, charging DeFi vault management fees while connecting to消费卡 for payments (Ether.fi).

Case Study: Steakhouse

Steakhouse Financial is an on-chain risk manager, i.e., an on-chain asset manager. It does not build its own lending protocols but conducts investment advisory业务 on existing infrastructure like Morpho: selecting collateral assets, setting LTV risk parameters, allocating funds across markets.

Revenue model mirrors traditional asset management, taking management and performance fees from investment收益. Lending protocols handle underlying operations, accounting, settlement, custody. Managers scale based on risk management expertise alone, without bearing infrastructure costs.

Industry Insights

Current on-chain managers oversee ~$7B AUM, compared to the global traditional asset management industry's $147T, indicating massive growth potential.

However, high收益前提 is underlying system stability. Recent stablecoin depegs and restaking sector cascading risks暴露 tail risks not mitigated by smart contract audits alone.

Market funds are shifting from high-yield synthetic dollars towards lower-yield but more stable Treasury-backed products. Institutional investors' core demand is not超 high APY, but predictable, controlled-risk收益.

Future Direction of the Stablecoin Industry Chain

The key to winning in stablecoins is not单纯 scaling issuance, but precisely targeting specific user groups. However, building a native crypto-financial system from scratch is long-cycle and成本极高.

The most viable strategy is grafting stablecoin advantages—24/7 settlement, low-cost transfers, programmable yield—onto成熟 traditional financial payment infrastructure. Major recent M&A like Stripe acquiring Bridge and Mastercard's deep partnership with BVNK全部 confirm the trend of融合 traditional financial infrastructure with stablecoin tech.

Two long-term trends持续放大 sector opportunities:

- Regional Fiat Stablecoin Adoption: When governments/institutions launch local currency stablecoins, they prefer reusing mature issuance infrastructure and local banking channels over building整套 systems from zero.

- Compliant Financial Integration: Licensed institutions like JPMorgan, Visa, BlackRock优先选择成熟商用 infrastructure over in-house tech development.

These trends push industry opportunities持续向 traditional financial entry必经 segments扩张: bank card issuing/settlement, asset custody, asset appreciation.

The conclusion is that issuers need to跳出同质化内卷 of the issuance track. Stablecoins are not standalone financial products but efficiency-upgrading tools for traditional payment infrastructure. The ultimate winners will be firms controlling various infrastructure layers on top of traditional finance.

随着 industry structural transformation, value重心 is shifting in two directions. 1) Downstream to the settlement layer: Falling interest rates削弱 issuance端 interest收益; rising stablecoin usage drives up underlying settlement infrastructure value. 2) Inward towards合规 systems: Stablecoins won't replace existing finance but will rapidly integrate into compliant regulatory frameworks; local stablecoins填补 USD stablecoin network gaps, naturally completing生态融合. This trend is irreversible.