Daily market key data review and trend analysis, produced by PANews.

Macro Markets

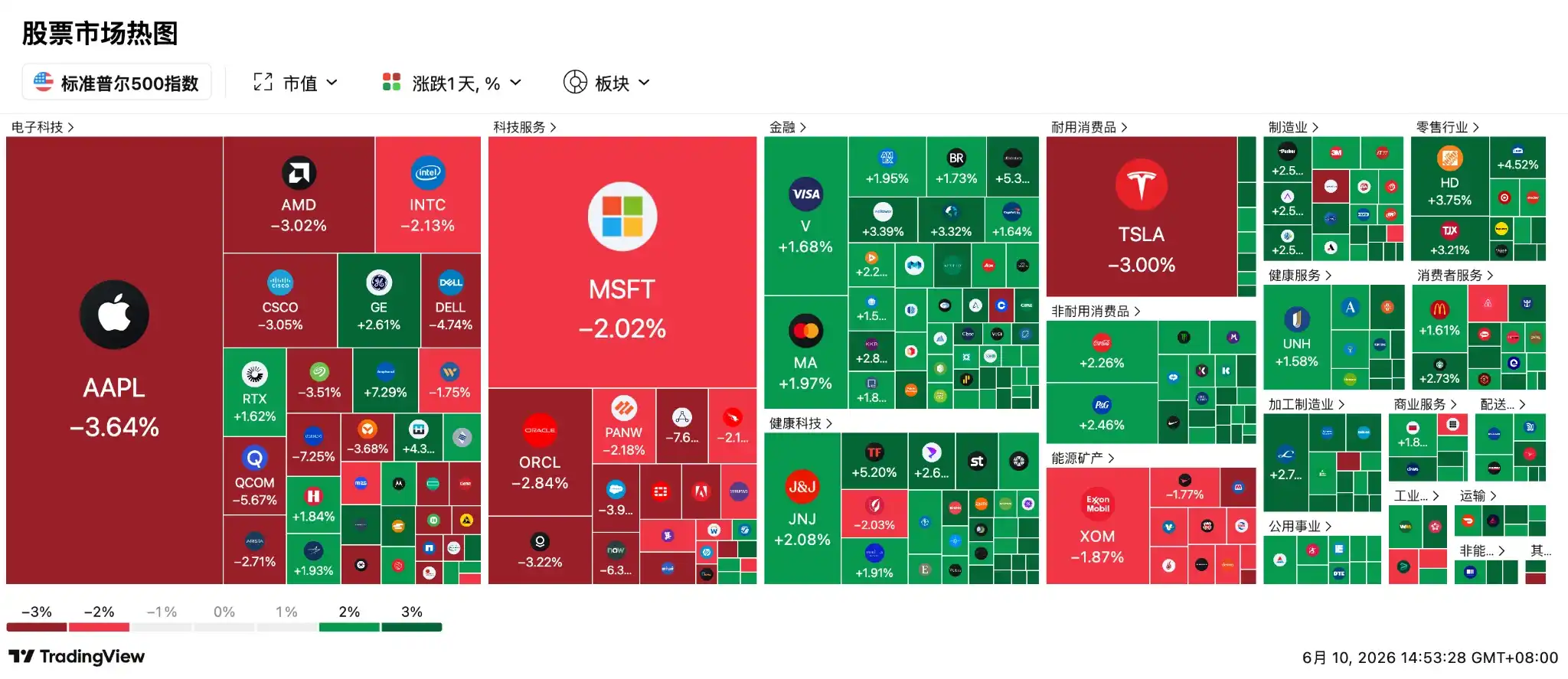

Tech stock selling caused sharp intraday volatility in US stocks on Tuesday, with the Nasdaq index at one point falling over 4%, closing down 0.97% below last Friday's low. The S&P 500 fell 0.26% to 7386.65 points, while the Dow Jones Industrial Average edged up 0.17% to 50872.11 points, supported by defensive sectors like consumer goods.

Geopolitical tensions escalated again. In response to the downing of a US military helicopter, US forces completed strikes on 20 targets within Iran. Iran subsequently retaliated against US bases in Jordan and Bahrain. Affected by this, the crude oil market saw intense volatility, with WTI crude oil briefly falling below $87, eventually closing sharply down over 3% near $88.50.

Gold prices were also impacted, with spot gold falling to the $4200 mark, hitting a nearly three-month low and already below the 200-day moving average. Analysts at Standard Chartered pointed out that as inflation rises and real yields climb, ETF funds are accelerating their outflow. The current ETP holdings structure is relatively fragile, potentially amplifying downward price pressure, with the next key technical support located near $4100. Notably, Citigroup analysts stated in a Monday report that if the Strait of Hormuz remains closed until late summer, gold prices could fall to $3500. Despite this, Ed Yardeni, founder of Yardeni Research, remains bullish, believing $4000 is a solid floor and sees potential up to $10,000.

US May inflation data will be released tonight at 8:30 PM. Wall Street institutions generally predict that, driven by surging energy prices, the May headline CPI year-on-year may rise to 4.2%~4.3%, hitting a nearly three-year high. However, the month-on-month core CPI is expected to be only 0.17%~0.22%, significantly below market consensus, with cooling in components like housing and auto insurance potentially being key to the slowdown in core inflation. The market is currently closely watching this data to gauge the policy stance of the new Federal Reserve Chairman, Kevin Warsh, at next week's interest rate meeting.

US Stock Dynamics

US stocks performed poorly after the AI frenzy subsided, with tech stocks experiencing heavy selling. The Philadelphia Semiconductor Index at one point plunged as much as 8.6%; ARM and Marvell Technology fell over 10% during the day; Micron Technology and Intel also fell up to 7% and 5% respectively. Apple, failing to deliver super-expected surprises at the WWDC conference, led the decline with its stock plummeting 3.64%. Super Micro Computer (SMCI) announced up to $7 billion in equity financing to purchase AI server components, with severe concerns about equity dilution causing its stock to crash over 10% in a single day, closing down 7.62%.

The optical communications sector experienced a "massacre" triggered by a research report. The prominent AI research firm SemiAnalysis released a report stating that NVIDIA's 800VDC power architecture and CPO (Co-Packaged Optics) large-scale production will be delayed until 2028. This expectation hammered the supply chain directly: Applied Optoelectronics (AAOI) plummeted 17% in a single day, Lumentum fell 8%, and chip giant COHERENT crashed 11.44%. Although NVIDIA Vice President Gilad Shainer strongly refuted this at the Computex exhibition, calling CPO "the most exciting technology today" and stating it would ramp up in the second half of the year, it failed to stop the spread of panic. The market began betting on NPO and traditional pluggable modules as transitional substitutes.

Meanwhile, Oracle is scheduled to release its earnings report after the US market close on Wednesday. The market generally expects revenue to reach $19.1 billion. TD Cowen and UBS have raised their price targets to $300 and $285 respectively, believing there is still room for acceleration in the cloud infrastructure business. Jefferies analyst Brent Thill stated that strong demand in the cloud infrastructure business will be a key factor driving the stock price. The options market indicates traders expect the company's stock price could swing up to 11% in a single week after the earnings release.

Cryptocurrency

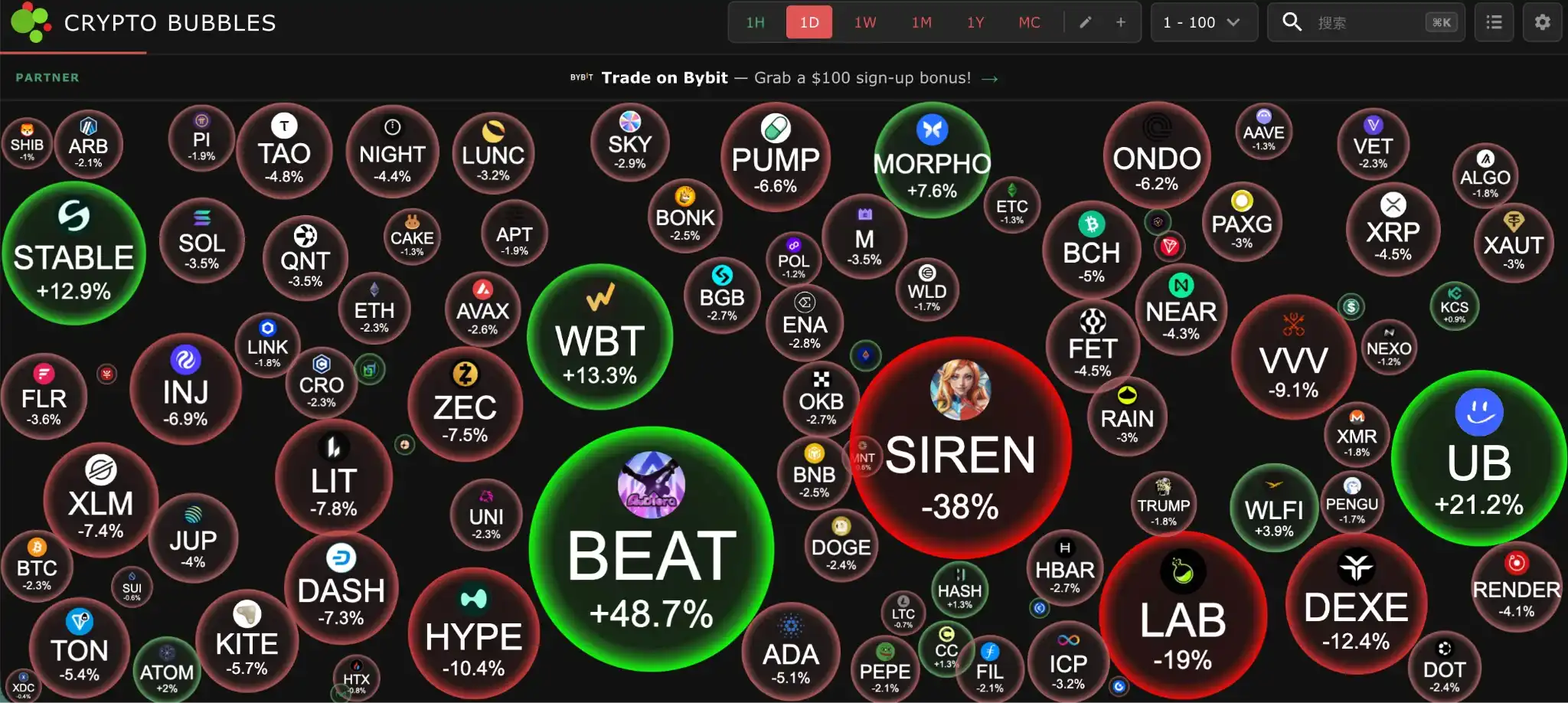

Bitcoin continues to face pressure. Bitcoin ETFs saw a net outflow of $77.43 million yesterday, with total assets falling back to $775.8 billion, completely erasing the incremental funds since Trump's election victory.

The market remains cautious about the upcoming US CPI data. Analysts point out that if inflation remains high, it could further dampen the rationale for Bitcoin as a hedge tool. Bitwise research shows Bitcoin often reacts ahead of traditional markets, so its current trend may indicate a broader risk adjustment. Glassnode's MVRV model warns that once $60,000 is decisively lost, the deep value zone of $50,000 will become the next ruthless magnetic attraction point.

Ethereum is also weak. Options market data shows that ETH's open interest has fallen 25% since the May high, indicating weakening investor confidence in future price movements. Although institutions like Bitmine bought 75,000 ETH worth $122 million against the trend, analyst Ash Crypto warned that if it falls below $1500, Ethereum could head straight to $1000.

On-chain black swan events have intensified panic. Sahara AI saw its token halved by nearly 60% in a single day due to a rumor about a CCIP cross-chain bridge supplementing liquidity being misinterpreted as a sell-off. The Humanity project suffered a devastating blow, with hackers invading employee computers and wildly minting 1 billion H tokens. Currently, both H and SAHARA token prices have somewhat rebounded.

Today's Outlook:

-

Informed sources: SpaceX will determine the issuance price as early as June 11, with the stock listing on June 12.

-

Upbit 24-hour trading volume ranking: SAHARA, WLD, XRP, BTC, ETH.

-

Magic Eden (ME) will unlock approximately 172 million tokens worth about $10.4 million on June 11.

-

HOME (HOME) will unlock approximately 750 million tokens worth about $40.2 million.

Top gainers among the top 100 cryptocurrencies by market cap today: BEAT up 48.7%, UB up 21.2%, WBT up 13.3%, STABLE up 12.9%, MORPHO up 7.6%.

Asia-Pacific Market

Asia-Pacific stock markets failed to stay immune. Under the dual pressure of Middle East conflict and the rout of US tech stocks, they experienced a major plunge.

The South Korean KOSPI index faced extremely severe selling, plummeting 6.46% and triggering circuit breakers at one point. The Japanese Nikkei 225 index also plunged over 1600 points, down 2.49%. Arjun Jayaraman, portfolio manager at Causeway Capital, pointed out that the proliferation of retail funds with high leverage and new ETFs in Japanese and Korean markets is amplifying this panic-driven volatility manifold.

Semiconductor giants became the epicenter of the selling wave in the Asia-Pacific market. Despite *The Korea Economic Daily* reporting the positive news that Samsung Electronics plans to build an advanced packaging plant in Gwangju, it seemed pale in the face of macro panic. Samsung Electronics stock plunged over 7%, and SK Hynix fell more than 8%. The Japanese chip contingent also retreated, with Advantest and Kioxia both falling nearly 4%. Not only that, even SoftBank Group saw its stock crash over 9% in a single day due to its attempt to use OpenAI shares as collateral for a $6 billion loan being blocked.

Amid the wailing, the A-share market walked its own independent logic due to strong data and World Cup expectations. China's May export data shone brightly, with a year-on-year surge of 19.4% in US dollar terms. Among them, integrated circuits skyrocketed 111%, and computer equipment surged 66%. Xing Zhaopeng, strategist at ANZ, remarked that the global AI hardware frenzy is substantively reshaping China's trade landscape. On the consumer side, with less than 48 hours until the US-Canada-Mexico World Cup opening, expectations for the "midnight viewing" late-night snack economy sparked by the time difference ignited the beer sector. Hui Quan Beer hit the daily limit up, while Zhujiang Beer and Yanjing Beer rose over 5%, becoming a rare bright spot in the gloomy market.