Author: neira, Tokenized Financial Product Architect, Tempo

Compiled by: Jiahuan, ChainCatcher

Most people believe that stablecoins are replicating the function of Eurodollars and further expanding the offshore US dollar system.

But this is not the case. Stablecoins primarily replace only certain functions within the existing system, especially the US dollar balances required for daily operations and settlement; in some aspects that the Federal Reserve cares most about, they may even suppress the multiplier effect of credit expansion.

The truly important question is: What happens when financial intermediaries, using stablecoins as a base, create a new layer of US dollar claims on top of them?

This article explains how this new collateralized financing channel operates, what conditions it needs to meet to achieve scale, and why its behavior under stress has a fundamentally different structure from the traditional Eurodollar system.

Abstract

Stablecoins introduce a tokenized private US dollar claim. Even if the issuer, reserve assets, and primary settlement bank are all within the US legal boundary, or rely on banking and securities settlement infrastructure connected to the US, such claims may still become economically "offshore" in terms of circulation and collateralized use.

Enforceable collateral control opens a secured credit channel, but does not thereby create a monetary claim. The true monetary event occurs only when another balance sheet funds, rolls over, or accepts at near-par value a liability issued against this controlled token.

Haircuts price the distance between "effective control over the token" and "reliable conversion into bank dollars." The source of elasticity is different: it comes from the balance sheet issuing the liability against the token, and from the willingness of third-party balance sheets to treat this liability as a near-par asset even under stress.

The decisive variables include: who has effective control over the token, what legal and operational path it takes to convert into bank dollars, how high the actual cost is, how long the duration is, and whether the resulting claim can still be financed at close to par if these paths are blocked.

Collateral dollars are not the stablecoin itself. It is a second-layer liability that another balance sheet is willing to issue, fund, and maintain at near-par value against a controlled token balance.

1. The Eurodollar System is a Hierarchy of Claims

In the strict sense, a Eurodollar is a US dollar-denominated bank liability booked outside the direct jurisdiction of the Federal Reserve: it is a private promise to deliver dollars, issued by a banking institution whose legal domicile, regulatory treatment, and liquidity access differ from those of a US domestic bank.

The broader offshore US dollar system also includes dollar claims issued by dealers and market intermediaries, based on collateral and derivatives. The unit of account is always the dollar, but the balance sheet issuing the claim is outside the direct jurisdiction of a central bank.

This market constitutes a system of private US dollar balance sheets. An offshore institution can create a dollar claim simply by booking a matching liability and asset simultaneously. Final settlement may still go through US payment systems, but "creation" and "settlement" are institutionally separate.

This separation allows non-US institutions to finance positions, hedge exposures, and settle in dollars without constant reliance on domestic central bank money. But it also creates dependencies: on rollover ability, interbank credit, dealer intermediation, and conversion to higher-tier claims when settlement pressures intensify.

Claims are ranked by: the strength of the par-value promise, the quality of the backing assets, tenor, market liquidity, and the directness of access to higher-tier money. Under normal conditions, market-making and rollovers compress this hierarchy. Under stress, this compression reverses: counterparty lines tighten, tenors shorten, haircuts widen, and the hierarchy reasserts itself through various operational constraints.

Elasticity comes from those balance sheets willing to expand their US dollar liabilities before final settlement imposes a hard constraint.

In the unsecured channel, offshore banks issue deposits, CDs, or interbank liabilities and invest the funds in dollar assets. In the secured channel, dealers issue a dollar claim against collateral, with the haircut determining how much funding the collateral can support.

In the derivatives channel, FX swaps and forwards create dollar funding not through an immediately visible deposit, but through commitments across time. The forward leg allows banks and non-banks to convert balance sheet capacity at the currency level into dollar funding capacity. A transferable stablecoin balance is merely a spot claim, with no forward funding market behind it, and thus cannot replicate the above functions at all.

In the Eurodollar context, "offshore" primarily refers to the legal and balance sheet location of the liability's issuer. Stablecoins acquire their "offshore" character differently, through economic usage: even if the issuer and its reserves remain within the US, or rely on US-connected banking and securities settlement infrastructure, their circulation, custody, staking, and leverage chains may still operate outside the US legal boundary.

Therefore, the real comparison is between two chains: the stablecoin collateral chain versus the offshore dollar funding chain. Directly opposing "token" and "Eurodollar deposit" is a mismatched comparison.

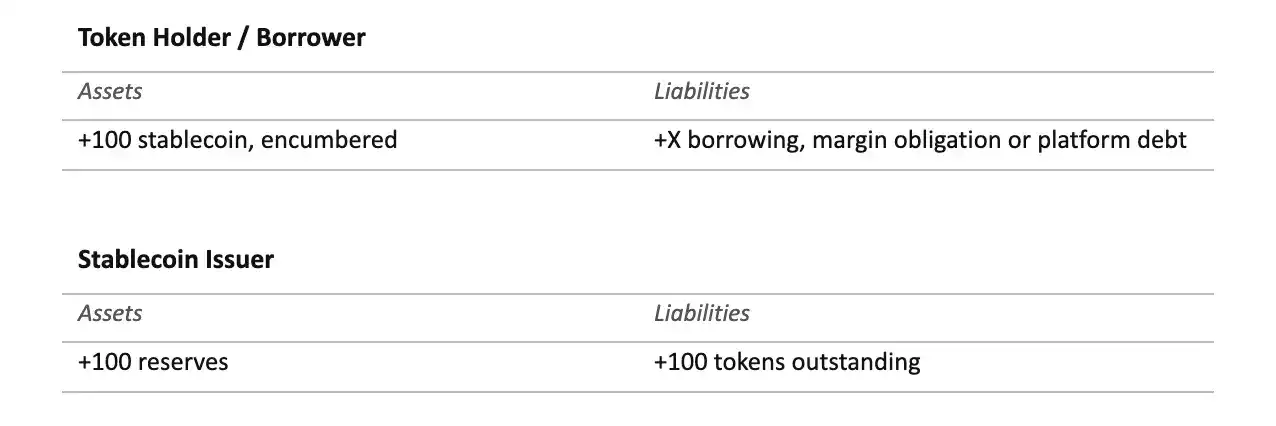

A Eurodollar deposit, from its birth, lands on a bank balance sheet capable of credit expansion: it is elastic from the very first entry. A stablecoin is born on the balance sheet of an issuer promising reserve backing, so its birth brings only "substitution"; elasticity appears later, elsewhere.

Only when another intermediary issues a fundable liability against it, and more balance sheets accept that liability at near-par value, does a stablecoin relate to elasticity.

2. Stablecoins Disrupt Specific Layers Within the Offshore Dollar System

Stablecoins change the composition of claims within certain specific layers of the offshore dollar system. The system itself remains in place.

The most obvious substitution occurs in this scenario: the holder wants a transferable dollar balance, not access to a full dollar balance sheet. Exchanges, brokers, payment companies, and some corporate treasury departments can hold stablecoins as settlement inventory. In this use, tokens take over part of the function previously performed by offshore operating deposits.

The balance sheet change here is direct. The user replaces a claim on an offshore bank with a claim on a stablecoin issuer. The bank loses that liability; the issuer gains a token liability matched by its reserve portfolio.

The composition of those reserves determines where the displaced funding demand ultimately reappears. If the reserves remain as bank deposits, the banking system recaptures part of the funds. If reserves move into Treasury bills or repos, pressure shifts to the sovereign collateral market and dealer intermediation. This substitution merely redirects "dependence on banks," it does not eliminate it.

This substitution is strongest in the operating balance layer: exchange inventory, broker settlement balances, payment floats, corporate working capital. It weakens at the wholesale bank funding layer, because this layer involves term deposits, CDs, and interbank placements that create maturity structures.

In FX swaps, it is almost non-existent: forward commitments and cross-currency balance sheet capacity together create dollar funding, where spot tokens have no role. In the dealer layer, stablecoins can become an eligible asset, but they are still subject to the truly critical constraints: capital, settlement capacity, counterparty lines, collateral inventory. It cannot replace any of these constraints.

A stablecoin accepted as collateral can support a further dollar claim. But until another balance sheet is willing to fund, roll over, or hold that claim at near-par value, it remains merely secured credit.

3. A Dollar Balance Does Not Create Dollar Balance Sheet Capacity

The offshore dollar system serves two distinct needs.

One is the need for "dollar balances": a claim that can be stored and transferred for payment. Stablecoins fit this need well in scenarios where transfer friction is the main constraint.

The other is the need for "dollar balance sheet capacity": the ability to obtain funding, margin, hedging, or maturity transformation. This capacity resides in banks, dealers, and funds. It consumes capital, liquidity, and counterparty lines, and can be withdrawn when conditions tighten.

There is a third need, overarching the first two: the need for a type of claim that other balance sheets are willing to treat as a near-par asset without re-examining the underlying collateral every time. Users need a dollar balance. Leveraged funds need funding capacity. Cash pools or second-layer funders need a claim that can be held at near-par value. The collateral channel only truly matters when it touches this third need.

Three tests separate these layers.

Transferability. The holder can transfer this dollar claim. Stablecoins easily pass this test.

Funding Capacity. Intermediaries are willing to lend, provide margin, or extend credit against this claim. Stablecoins pass this test only under eligibility, control, and haircut constraints.

Monetary Acceptance. Can the claim created by that intermediary itself be funded or held at near-par value? Only at this stage do stablecoins become systemically significant.

Corporate-level substitution also follows the same gradient: strongest for settlement inventory, weakest for relationship banking. A token balance can replace the portion of operating deposits used to transfer value. But it cannot replace any of the things behind most corporate cash positions: overdraft facilities, FX credit lines, correspondent banks, intraday liquidity providers, sanctions compliance interfaces, credit relationships.

Tokens transfer claims. Balance sheets provide elasticity.

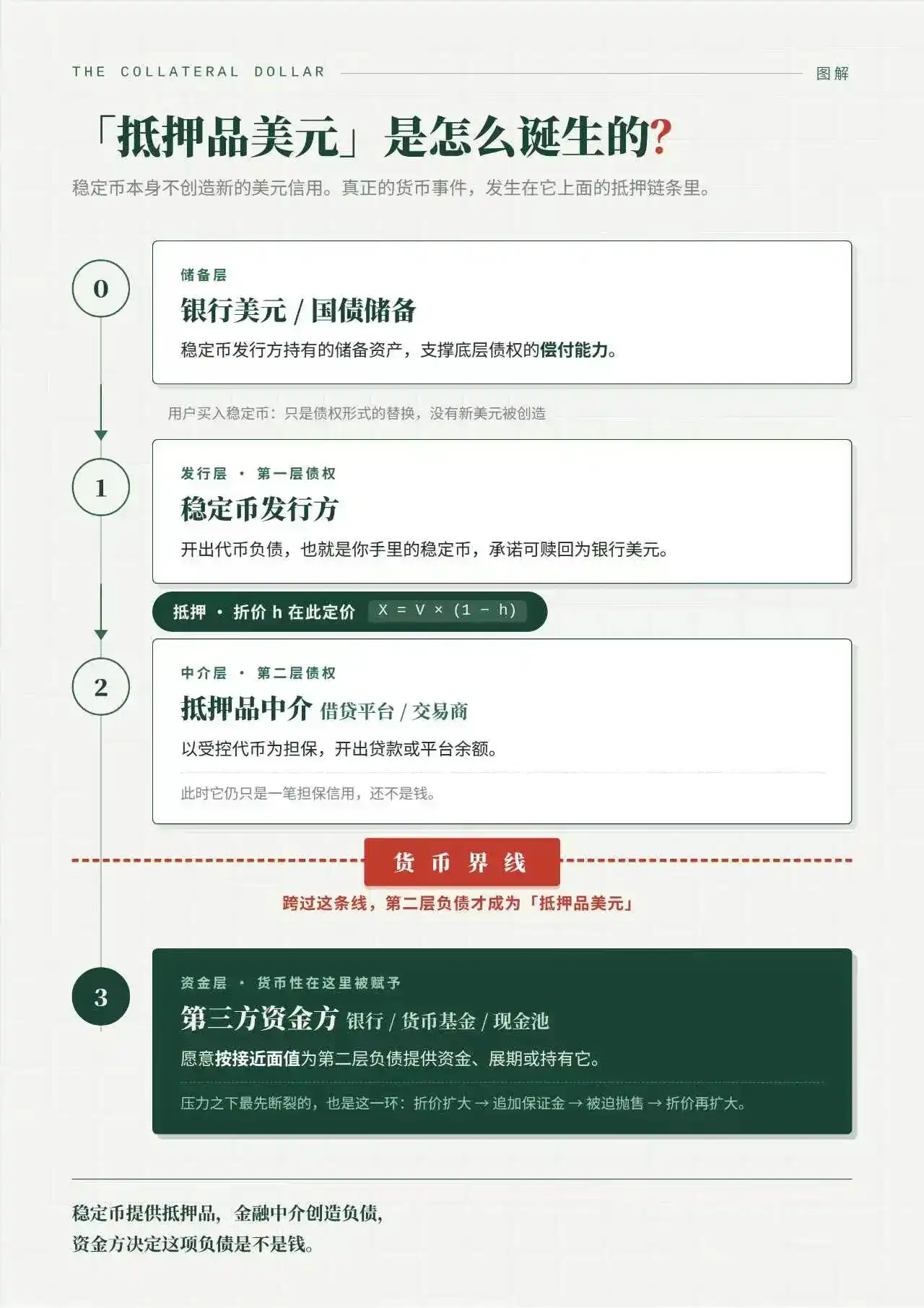

4. From Deposit Elasticity to Haircut Elasticity

In the traditional offshore channel, elasticity originates from a bank liability.

(Offshore Bank)

The depositor holds a near-money claim; the bank obtains deployable funds. Elasticity is born on the liability side of an expandable balance sheet.

Stablecoin issuance creates a narrower structure.

(Stablecoin Issuer)

The holder receives a transferable claim; the issuer holds reserves. As long as the issuer stays "narrow," no second private dollar claim is created: only the form and location of the first claim change.

The secured channel begins the moment tokens are used for funding. The haircut determines how much funding the controlled token can support:

X = V_token × (1 − h)

where X is the second-layer funding capacity, V_token is the market value of the controlled token, and h is the haircut rate. Here, the accounting must distinguish four balance sheets.

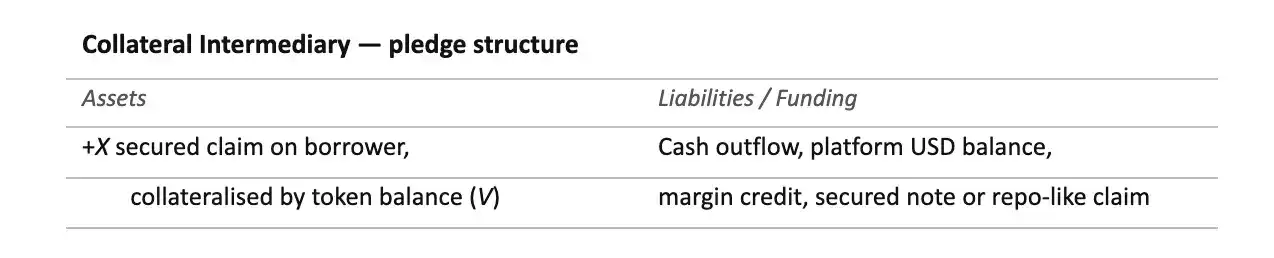

The collateral intermediary's situation depends on the legal form of control. Pledge and title transfer are not the same balance sheet.

(Collateral Intermediary: Pledge Structure)

In a pledge structure, the borrower remains the owner of the tokens. The intermediary does not own the full token balance; it holds a secured claim of amount X and has control or enforcement rights over collateral valued at V. Its balance sheet exposure is X; legal protection covers V. The surplus collateral V − X economically still belongs to the borrower, unless default and liquidation mechanisms dictate otherwise.

(Collateral Intermediary: Title Transfer Structure)

In a title transfer structure, the intermediary holds the tokens themselves. Assuming token value is 100 and the loan is 90, the intermediary controls the full token balance of 100, while the borrower retains the economic surplus through the right to "receive equivalent collateral or residual value upon repayment."

The intermediary's total legal control is V; its net economic exposure is X. The difference V − X is not freely usable equity. It is the borrower's residual protection, embedded in the obligation to "return equivalent collateral or settle the surplus upon liquidation."

If the loan is funded using existing cash, the intermediary may not have expanded its liability; it merely exchanged cash for a secured exposure or title transfer exposure. If the loan is funded by issuing platform balances, notes, repo-like claims, or other short-term liabilities, then the intermediary has expanded its balance sheet.

Therefore, the monetary question does not stop at whether title is transferred. It depends on how the loan itself is funded, and whether the resulting liability is accepted at near-par value.

This distinction matters because the stress mechanisms differ. In a pledge, the lender's enforcement relies on perfected rights, priority, and liquidation rights over collateral still associated with the borrower. In title transfer, the intermediary may have stronger control, rehypothecation ability, or liquidation rights, but also bears a clearer obligation to return equivalent collateral or value once the secured exposure is settled.

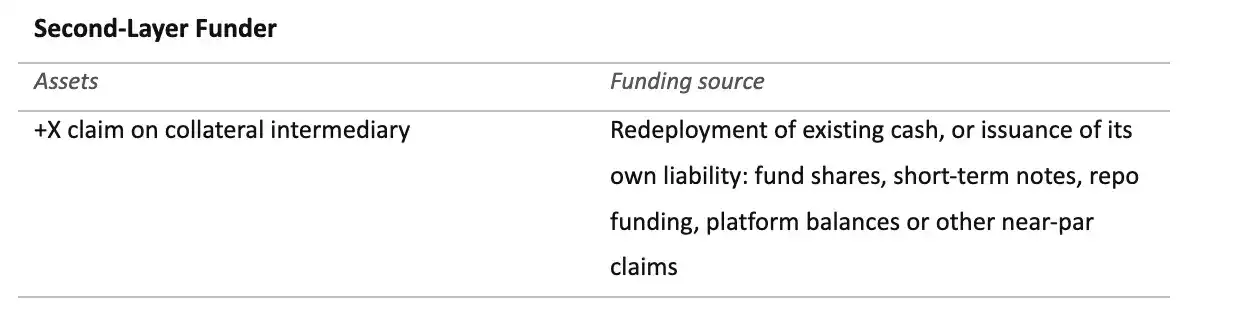

(Second-Layer Funder)

Monetary elasticity is strongest in the second scenario: the funder finances this claim by issuing its own near-par liability. In the first scenario, the system merely reallocates existing cash to a claim backed by tokens; the stock of private dollar liabilities does not necessarily expand.

Issuance by itself creates nothing but tokens. Secured credit advances value against tokens. Only when the lender's claim becomes an asset that another balance sheet funds at near-par value is the monetary line crossed. The step from secured lending to money creation happens here, never earlier.

Haircuts price the distance between "effective control over the token" and "reliable conversion into bank dollars," converting collateral value into funding capacity. And elasticity itself comes from the liability issued against the token and the willingness of another balance sheet to fund that liability at near-par value.

5. The Institutional Conditions for the Collateral Channel

Four conditions determine whether a second-layer claim can be funded at near-par value.

Legal Control. Having enforceable priority over the borrower, the borrower's creditors, custodians, platforms, and any intervening bankruptcy estates. The questions for the issuer are different: redemption eligibility, transferability, freeze rights, account status, blacklist risk, and the legal status of the token holder's claim. The lender must know if the arrangement is a pledge, title transfer, custody control, smart contract lock-up, or a hybrid platform claim. Each creates different rights upon default.

Operational Control. Liquidation paths and redemption paths must be distinguished. Liquidation depends on secondary market depth, dealer balance sheets, and access to trading venues. Redemption depends on issuer rules, whitelists, settlement banks, banking hours, and redemption timing. A haircut that treats these two exit paths as equivalent is not rigorous.

Haircut Rigor. Haircuts must cover: issuer risk, reserve composition, settlement bank access, redemption eligibility, custody structure, legal enforceability, venue depth, on-chain finality, operational suspension rights, wrong-way risk with the borrower, market maker concentration, and the time required to convert tokens into bank dollars.

Funding Persistence. Third parties are willing to fund the lender's claim without having to re-analyze the tokens, borrower, and full liquidation path from scratch each time. Whether the original lender is comfortable with the collateral is never the criterion. As long as every funder must individually analyze each secured loan, the result is bilateral secured credit, not a near-par claim.

Near-par funding is bound to tenor. A claim that can be lent overnight is not the same as one that can withstand multi-day redemption delays, periodic fund withdrawals, or investor runs. Moneyness is not just a price issue; it's also a timing issue.

The real test is: after the borrower, issuer, custodian, trading venue, and settlement bank have each become independent risk sources, whether the liability issued against the token is still a near-par asset. Whether the token can be staked is the easiest part.

6. Stress Transmission in the Collateral Channel

Stress in the offshore dollar system manifests as movement up the hierarchy. Weaker counterparties lose funding. Repo lenders widen haircuts. Dealers begin rationing balance sheet capacity. Claims previously treated as near-cash now require explicit liquidity support.

In a collateral channel built on stablecoins, the higher-layer claim fails first. The underlying token is the issuer's promise to "redeem for bank dollars." The second-layer claim is the intermediary's promise to "provide near-par liquidity backed by that token." The former may still be solvent, but the latter has already lost its near-money status.

Under normal conditions, tokens trade at par, haircuts are low, intermediaries extend credit as usual, and second-layer claims are treated as near-cash. No one simultaneously tests the full liquidation and redemption paths. The vulnerability lies precisely in the layer above the issuer.

The first break is often an adjustment in collateral terms, long before any run on the token occurs. A lender raises the haircut; the borrower receives a margin call. A borrower unable to provide cash or additional collateral forces the intermediary to liquidate, redeem, or fund the position internally. The second-layer claim immediately becomes highly balance-sheet-intensive.

The arithmetic here is unforgiving. A token balance funded at a 2% haircut can support credit of 98:

100 × (1 − 0.02) = 98

With a 15% haircut and a secondary market price of 99 cents, the loanable value drops to 84.15:

99 × (1 − 0.15) = 84.15

The missing 13.85 must come from somewhere:

98 − 84.15 = 13.85

Either a margin call, a forced sale, an internal funding move, or a broken second-layer claim.

This static formula measures the first loss of funding capacity. The real stress mechanism is dynamic. V_token and h are not independent variables. A higher haircut lowers loanable value and triggers margin calls that may force token sales. Forced selling depresses the token's secondary market price. Lower prices in turn "justify" further haircut increases, creating new funding gaps.

X_t = V_t (1 − h_t)

For small changes:

ΔA ≈ (1 − h_t) ΔV − V_t Δh

Under stress, these two move together. Δh rises because lenders demand more protection; ΔV falls because the margin call process itself creates selling pressure. Thus, the haircut is not just a measure of risk; it can become a transmission mechanism for risk.

The liquidation path converts a funding problem into a market depth problem. The redemption path converts it into a banking channel problem. Internal funding leaves it as an intermediary capital problem, which is where it becomes expensive. Passing the claim to another funder only works if the claim still trades near par.

The exit of a dealer or platform withdraws an institution that had been "warehousing" the time gap between liquidation and redemption, converting collateral into near-par funding. This is different from declining liquidity. Once such warehousing stops, the hierarchy immediately reasserts itself.

Unlike the mature offshore dollar system, the stablecoin collateral chain has no established "dealer of last resort" mechanism or central bank swap line architecture for liabilities written on tokens. The underlying token may have reserves. The second-layer claim has only its own funding market.

Reserve quality supports the solvency of the underlying claim, but it offers no guarantee of "par liquidity" once redemption channels, settlement banks, or secondary market depth fail. The issuer having sufficient reserves can coexist with the collapse of the credit system built on top of it.

7. Conclusion

The Eurodollar analogy holds only to a certain extent. A stablecoin is a tokenized private US dollar claim; even if the issuer and reserves remain within the US legal boundary or rely on US-connected banking and securities settlement infrastructure, its usage may still become economically offshore.

Reserve quality supports the solvency of the underlying claim. The leverage, margin, platform credit, and secured liabilities built on it must answer to a different set of tests.

Collateral eligibility does not reach monetary acceptance: until the lender's claim becomes a near-par asset in others' eyes, a loan backed by tokens remains merely a loan.

The deposit channel of the Eurodollar system begins with a bank liability and expands through deposit creation, interbank funding, and forward dollar markets. The collateral channel for stablecoins begins with a controlled tokenized asset and expands only when an intermediary issues a liability against that token and another balance sheet treats that liability as near-money.

The issuer holds the underlying promise, the collateral intermediary makes the second promise, and the funders decide whether this second promise possesses near-money attributes. Haircuts price the distance between "token control" and "bank dollar conversion." And under stress, it is precisely this distance that widens first.

Only when the claim built on stablecoins survives the leap from "token liquidity" to "bank dollar liquidity" do collateral dollars truly exist.