Author: Zhou, ChainCatcher

This year, Bitcoin pioneer Adam Back and the company he founded, Blockstream, have repeatedly found themselves at the center of discussions within the crypto community.

In February, documents related to Epstein released by the U.S. Department of Justice disclosed that Jeffrey Epstein had invested in Blockstream in 2014 through a fund related to Joichi Ito.

In April, an investigative report published by The New York Times listed Adam Back as one of the strongest candidates for being Bitcoin's inventor, Satoshi Nakamoto.

Simultaneously, the Bitcoin treasury company BSTR, which he is involved in promoting, is preparing to go public via a SPAC merger.

However, new controversies soon emerged. Earlier this month, the investigative account NatInfoSec published a lengthy article alleging that Blockstream may be raising billions of dollars from investors under the guise of mining revenue, but the actual mining facilities and supporting hash rate are questionable, and the structure resembles a Ponzi scheme.

The article used strong language. Although some inferences still require independent verification, the several points of doubt it raised have prompted the market to re-examine Blockstream.

Image source:RootData

Chain of Allegations: Hash Rate, Revenue, and Disclosure Doubts

1. Doubts About Hash Rate and Payment Capacity

This is the most solid part of the financial logic in the allegations. NatInfoSec points out that to meet the obligations of the currently issued BMNs (Blockstream Mining Notes), Blockstream would need to operate over 20 EH/s of hash rate. If contract buffer clauses are included, the required hash rate could be as high as 35 to 45 EH/s. However, Blockstream's own dashboard shows its current actual hash rate is only 15 EH/s.

A mining facility of that scale should appear in public records such as ERCOT grid connection filings in Texas, power purchase agreements with Hydro-Québec, customs import data for ASIC equipment, hash rate attribution on mining pools, and coinbase signatures on-chain. NatInfoSec claims it could not find evidence matching the scale of Blockstream's notes in the aforementioned public channels.

In NatInfoSec's view, if mining output cannot cover payment obligations, it is necessary to question where the BTC ultimately received by investors comes from. The article specifically mentions the 'Substitute Performance BTC' mechanism in the BMN2 terms, stating that this clause allows Blockstream to fulfill its delivery obligations with BTC from any source during the 48-month contract period, without prior notice, without disclosing the source, and with no upper limit on quantity.

The article also claims that BMN1 once made up for payment shortfalls by purchasing BTC on the open market. This shifts the core question of BMNs from "is the mining revenue sufficient" to "is the source of payments verifiable."

2. High Returns and High-Risk Debt

The article mentions that Blockstream has issued related notes of different tiers through platforms like STOKR, with yields gradually increasing from about 9.775% to 18%, with the latest tier approaching 20%.However, some maturity arrangements are reportedly not direct principal repayments but are rolled over into new notes with higher yields. However, these claims still need further verification against the original issuance documents.

It is well known that Bitcoin mining is a highly cyclical industry, with real-time fluctuations in miner prices, network hash rate, difficulty adjustments, electricity prices, and BTC prices, making it difficult for mining companies to promise static fixed returns externally. Fixed annualized returns around 20%, in this industry context, require the issuer to provide a clear source explanation.

3. Chris Cook's Past Conviction and Disclosure Issues

The most impactful part of the allegations concerns the background of Christopher William Cook.

NatInfoSec states that Cook was once an important person in charge of Blockstream's mining business and currently serves as the CEO of Exacore. The article points out that Exacore is a related operating entity spun off from Blockstream's mining business. After reviewing U.S. federal court records, NatInfoSec claims to have found that Cook was sentenced in 2008 by the U.S. District Court for the Southern District of Florida to 41 months in federal prison for mail fraud (case number 06-80187) and ordered to pay approximately $1.85 million in restitution.

The core method of the case was commercial credit fraud: registering multiple shell companies, forging financial statements and bank information to defraud goods worth over $1.8 million from more than 30 retailers, then reselling them for cash.

The article notes that this conviction record does not appear in any BMN issuance documents. Furthermore, Blockstream's marketing materials on the STOKR platform allegedly claimed Cook "formerly worked at NASA," but his actual connection to NASA was reportedly only a student tour project he participated in at age 18.

Additionally, NatInfoSec further listed clues about Cook's recent purchases of mansions, airplanes, yachts, investments in Trump Media stock, and several supplier lawsuits, alleging funding flow and governance risks behind the BMNs.

4. BSTR/SPAC Controversy and Linkage

NatInfoSec also attempts to extend the BMN controversy to Bitcoin Standard Treasury Company (referred to as BSTR). The company, related to Adam Back, is reportedly preparing to go public via a SPAC merger. NatInfoSec questions why Cook's conviction record and the BMNs' massive potential liabilities do not appear in SEC registration filings and raises concerns about BSTR's governance structure, including Adam Back signing agreements representing both sides of the transaction and custodian Komainu having equity ties with Blockstream.

However, this is the part of the allegations most easily rebutted. The legal relationships, guarantee structures, and liability boundaries between BMNs, Blockstream, Exacore, and BSTR are currently not clear. If the related notes have no group guarantee and are not included in the BSTR listing entity, directly equating BMN risk with BSTR risk may involve excessive extrapolation.

BitMEX Cools the Waters, Community Demands Verifiability

On June 21, BitMEX Research published a commentary article addressing NatInfoSec's allegations point by point. BitMEX acknowledged that Cook's criminal past is likely true and that NatInfoSec probably identified the same person. Regarding the nearly 20% yield, BitMEX also expressed concern, stating it requires further explanation from the issuer.

However, for the other allegations, BitMEX considered the evidence insufficient or misleading. Regarding the non-disclosure of Cook's past in BSTR SEC filings, BitMEX's judgment was that Cook is not a director of BSTR, and the mining business is not expected to be included in the listing entity, so there is no mandatory disclosure obligation. Regarding whether BMN liabilities should be counted in BSTR, BitMEX believes there are no group guarantee clauses in the BMN documents, making them legally independent structures. Regarding the allegation of insufficient L-BTC collateral, BitMEX considered that the original article cited data from a code error on the liquid.network website, which has been fixed and now displays normally.

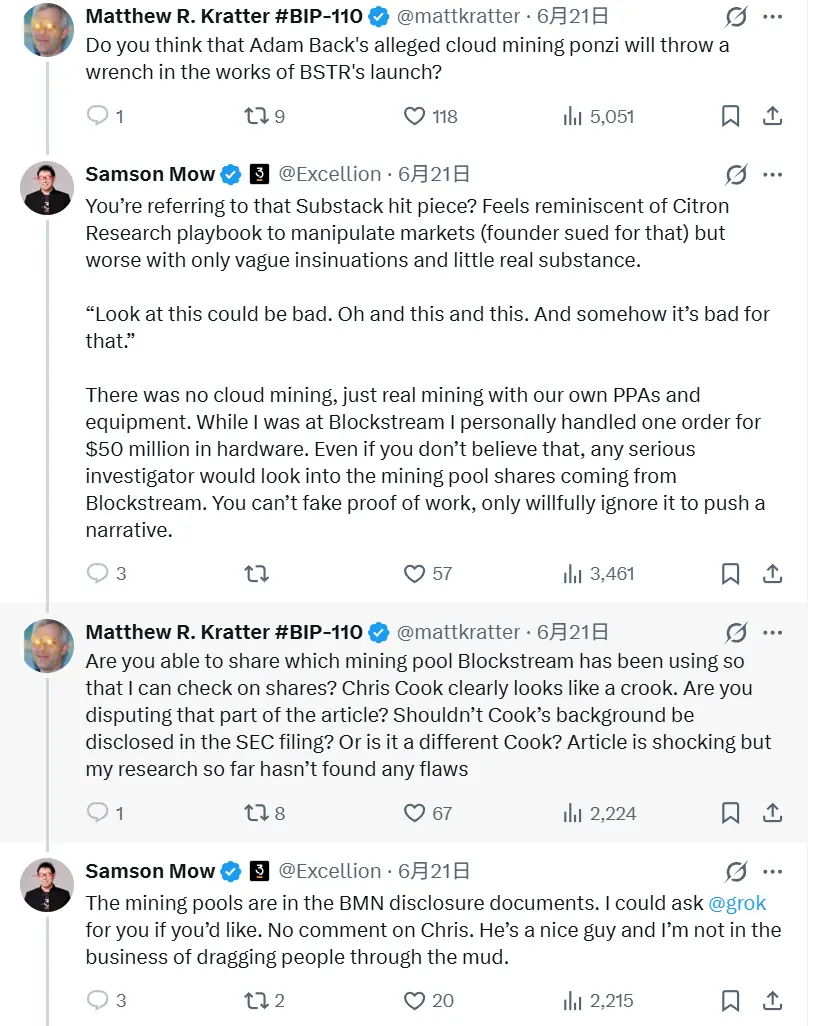

Furthermore, the debate continues at the community level. Former Blockstream CSO, now Jan3 CEO, Samson Mow, defended the BSTR narrative on X. He argued that the market should not focus only on short-term controversies but see that more Bitcoin treasury companies are about to enter the market. Mow stated that BSTR is about to enter the market with $1.5 billion in funds and will become an important competitor in the BTC asset accumulation race.

But critics quickly brought the question back to the BMNs themselves. Prominent Bitcoin commentator Matthew R. Kratter responded by directly questioning whether Adam Back's so-called "cloud mining Ponzi" allegations would affect BSTR's launch. He then further questioned which mining pool Blockstream actually uses, whether the public can verify pool shares accordingly, and demanded a response on whether Cook's background should have been disclosed in SEC filings.

The debate escalated further around hash rate verifiability. Mow responded that the term "cloud mining" is not accurate; Blockstream is engaged in real mining using its own PPAs and equipment. He also mentioned that during his tenure at Blockstream, he personally handled a $50 million hardware order and stated that serious investigators should look at the mining pool shares from Blockstream, not ignore PoW evidence.

However, skeptics did not accept this explanation. Developer Chris Guida countered, asking where the public can openly verify hash rate from Blockstream. He argued that merely knowing which mining pools are mentioned in BMN documents does not prove that the valid shares in those pools actually come from Blockstream, unless Blockstream or the pools publicly label the source of that hash rate.

This debate compresses the core issue of BMNs to one point: Whether Blockstream is engaged in real mining is not the only problem; the real problem is whether investors and external observers can independently verify this hash rate, revenue, and source of payments.

BMNs Still Await Answers: Real Assets and Liability Boundaries

Despite the evident polarization of community views on this incident, it has not resolved the questions surrounding the BMNs themselves. Regarding this mining note product, the market still lacks several key pieces of information.

First, what exactly are the actual issuance scale, outstanding obligations, and liability boundaries of the BMNs? Authorized issuance scale, actual issuance scale, outstanding scale, maturity structure, and related guarantees are not the same thing. The market needs to know where the risk of this mining note actually resides and whether it could spill over to Blockstream or other related companies.

Second, does the mining facility's hash rate suffice to support payment expectations? If the publicly visible mining facility locations, power contracts, miner scale, pool revenue, and historical output do not match the issuance scale and payment arrangements, the natural question becomes whether the revenue truly comes from mining or from other funding sources.

Third, where exactly does the nearly 20% fixed return come from? High returns themselves do not equal fraud, but in a highly cyclical industry, they necessitate higher transparency.

Fourth, are the BTC or L-BTC payments to investors verifiable? If BMN payments involve L-BTC on the Liquid network, then on-chain transparency, peg-out risks, and proof-of-reserves will all become real concerns for investors.

Fifth, what are Cook's actual authority and beneficial relationship within the BMNs and Exacore? If he holds a core position in fund usage, mining assets, or note design, the importance of disclosure increases.

These questions currently do not directly prove fraudulent activity by Blockstream. Objectively speaking, as a mining note product for investors, its premium and relatively high yield carry relatively obvious risks. This means BMNs still have considerable room for further explanation regarding their actual scale, fund usage, source of returns, and governance disclosure.

As of publication, Blockstream has not yet issued a systematic official response to the related controversies.