Zk rollups 是加密领域最有前途的创新之一,但很容易与最近出现的新解决方案混淆。

因此,本文将对一些最著名的 Zk rollup 协议进行可视化介绍。

首先,零知识(ZK)rollup 是一种第 2 层扩展解决方案,它通过在链下处理交易并将它们在链上捆绑在一起来增加以太坊的吞吐量。

本文将不会对技术细节进行介绍。

总的来讲,ZK Rollup 的好处包括非常低的 gas 费和不牺牲区块链的安全性。

本文将介绍 8 个不同主题的 ZK rollup 协议。

1. zkSync

zkSync 是一个 Zk-rollup,它也是 EVM 兼容的。

尽管仍在研发进行中,但该团队已经启动了主网。你已经可以用真钱试试。

此外,他们已经筹集了 4.58 亿美元资金。而且还没有自己的 token。

根据 @l2 beat 和 @ETH_Daily 之前分享的数据:

・Zksync 的 TVL 有 5300 万美元;

・根据 @Orbiter_Finance 数据,它是交易数量排名第三位的 L2;

・到目前为止,至少有 300 个项目加入了该生态系统。

在下面你可以看到它不断增长的生态。

2. StarkNet

StarkNet 可能是 zkSync 最大的竞争对手。这是另一个 Zk Rollup 解决方案。

StarkNet 已经启动了主网。但是你也可以在测试网上试用 StarkNet。

他们同样还没有 token。

在这里,我链接了一个可能的 StarkNet 代币空投指南。

同样,正如 @l2 beat 所述以及之前由 Ethereum Daily 分享的那样:

・StarkNet 的 TVL 为 460 万美元;

・超过 200 个项目加入了生态系统;

・团队迄今共筹集了 2.73 亿美元资金。

下图展示了其不断发展的生态的可视化图表。

3. zkLend

zkLend 并不是一种 Zk Rollup。事实上,它是直接建立在 StarkNet 上的 L2 货币市场协议。

现在它在测试网上可用。您可以尝试使用您的 Argent 或 Braavos 钱包借出和借用测试代币。

而且它还没有代币。

4. zk.money

这是一项建立在名为 Aztec Network 的以隐私为中心的 Zk-rollup 之上的 DeFi 服务。

你已经可以向 zk.money 桥接真实资金并使用 Aave、Yearn 和 Lido 等 dapp。

zk.money 上的操作都是私人的。

5. Aztec Network

这是一个面向隐私的 Zk-rollup,里面有很多已经可以使用的产品。

它的主要目标是为协议提供透明度,但为用户提供隐私。

Aztec 刚刚筹集了 1 亿美元,该链和 zk.money 都没有代币。

6. Polygon ZK

Polygon 也在构建 ZK 解决方案。他们正在使用完全可用的源代码和与 EVM 等效的代码来创建它。

到目前为止,您可以在测试网中进行尝试。

7. ZKSpace

ZkSpace 是一个 Zk-rollup 平台,由三部分组成:

・ZkSwap,L2 AMM Dex;

・ZkSquare,一种支付服务;

・ZkSea,NFT 市场和铸造中心。

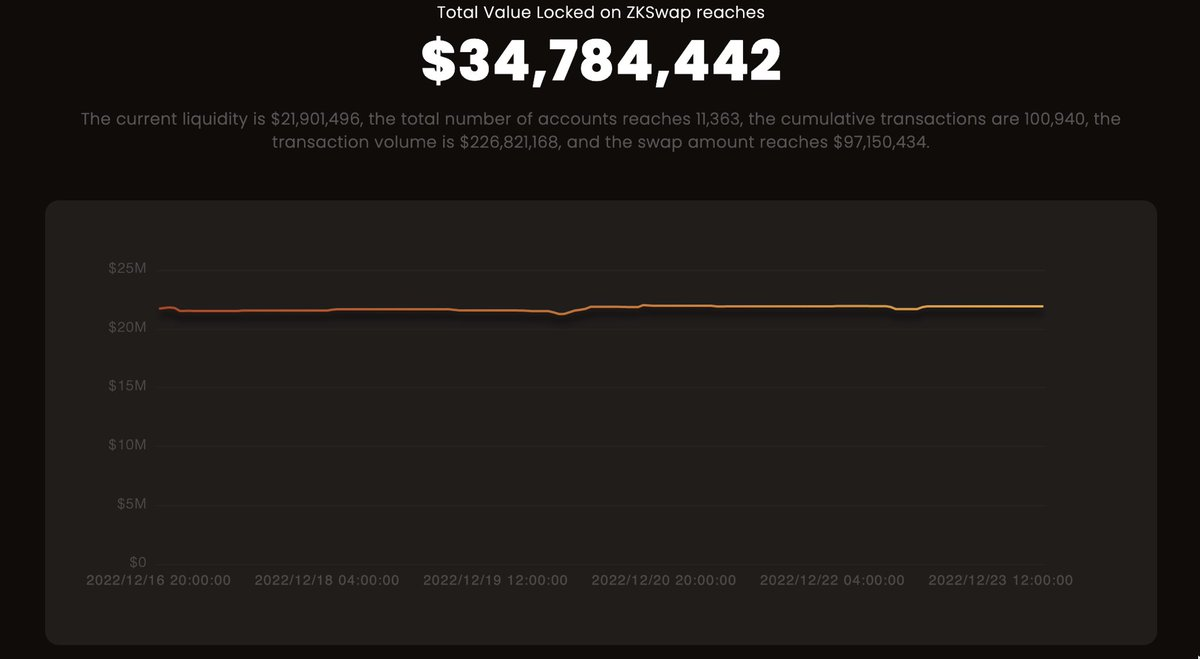

下面是他们基于生态系统真实资金的 TVL。

8. Scroll

Scroll 是一个 zkEVM Layer2。

他们的目标是拥有一个可扩展的网络,以实现对现有以太坊协议的本地兼容性。

你可以试试他们的测试网。

他们在 4 月份筹集了 3000 万美元,目前还没有代币。

尽管这些是传闻最多的,但我们不应忘记其他公司也在构建 Zk-rollup 解决方案。

例如,路印(loopring)已经有可用的 L2。

免责声明:我想重申一下,我没有深入研究这些 Layer2 背后的技术。

ZkSNARK 和 ZkSTARK

这两种是可以用来计算和验证交易的不同机制。基本上是可以构建 Zk-rollup 的两种不同类型的基础。

总而言之,本文旨在介绍当前的 Zk-rollup 应用格局。

也许您会发现这对于寻找新协议、了解它们的基本差异或试用它们(在可能的空投之前)很有用。

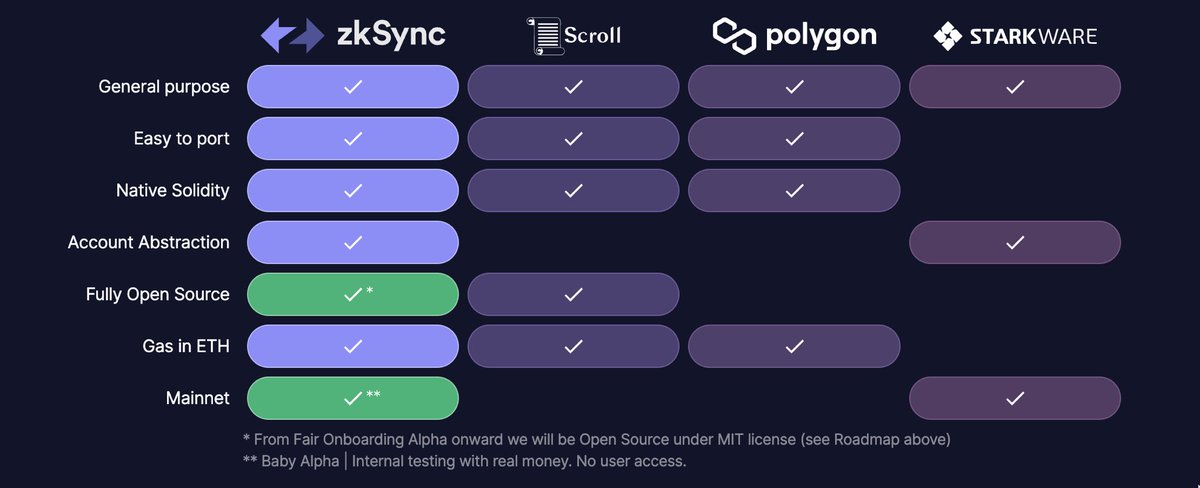

下图展示了各大 zk rollup 应用的简要比较。