今年4、5月的时候,web3在微信指数中的趋势数据,一度超过了区块链。从2021年12月份开始,web3这个词突然出圈,进入传统互联网,然后开始蔓延火爆。

从最近互联网圈的融资情况和创业动态看,似乎传统VC们都在号召“ALL in Web3”。那么Web3到底是什么?未来会如何发展?白话区块链带你一起来拨开迷雾,给Web3祛魅。

Web3是什么?

这段时间我们看到互联网创业圈子,似乎人人都在说Web3,但是,关于Web3到底是什么,答案五花八门,其实到现在还没有一个共识度很高的定义,和「元宇宙」一样。

Web3到底是什么呢?

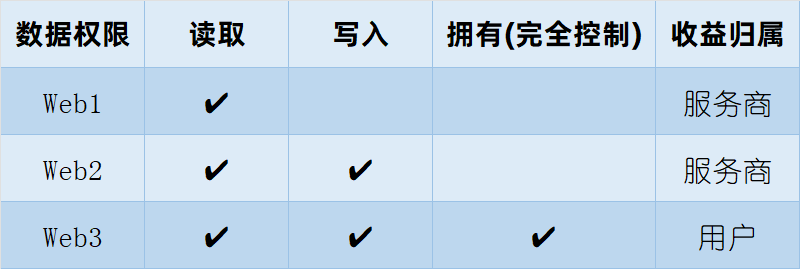

要说清楚web3,我们还是要先看一下Web1和Web2。

这张图片之前在网络上流传很广,总结得也比较清楚。

Web1是可读的互联网,在Web1中,我们可以从网络上获取新闻资讯,但是几乎只能单方面地获取信息,无法参与互动。

到了Web2,有了留言评论、点赞、私信聊天、发布主题等等这些一些功能,所以,Web2不仅仅是可读的,而且还可写,可参与互动。

那Web3呢,我们不仅仅可读、可写,还可拥有。

可拥有具体是指什么呢?其实是落到了「控制权」上面:我们对账号、对在平台上互动产生的数据信息、对资产等有了控制权,我们能说了算。

Web3的「控制权」到底是什么?

那么Web3的控制权到底是什么?我们来列举几个简单的场景。

1)对账号的控制权

在Web2时代,我们要使用平台的服务必须注册账号,或者使用微信、QQ等统一账户去登录。当你的行为规范不符合平台标准的时候,你的账号可能随时被限制被封禁。

所以,在web2时代,你其实是没有账号的控制权的。

但是,在web3时代,你可以用一个账号登录所有的平台,而且,这个账户背后是由一系列密码学算法、博弈论等技术手段保障的,让你对自己的账户拥有控制权,不会随意被平台限制或封禁。

也就是说,在Web3,你的账号是你自己说了算的,不会受到中心化的平台的控制。

2)对数据的控制权

在Web2中,为了获取平台的服务,我们在使用平台之前不得不签署数据隐私相关的条款,否则就无法使用相关服务。

在使用服务的过程中,会产生一系列数据,比如,在某宝上我们有对商品的喜好数据、有购买能力数据、有购买频率数据等,这些数据可能都会被某宝大数据平台制作成用户标签,作为精准的用户标签卖给相关的店铺,这也是我们感觉平台给我们推荐的全是喜欢的商家和产品的原因,因为,我们的购买习惯数据告诉了他们一切。

但是,当我们被当做一个个精准标签卖给店家的时候,我们是无法从中获得任何收益的。我们为这些平台积累了大量数据,这些数据成为平台的核心资产,但我们作为数据的供应方和拥有者,却无法分的任何一杯羹。

但是,在Web3时代,我们产生的数据都属于我们自己。我们可以选择把这些数据开放给平台或者给其他需要的商家,而且,开放出去的同时,我们可以获得相应的收益。当然,我们也可以选择不开放,对于卖或者不卖,我们自己能说了算。

而且,在密码学算法等的保障下,我们的数据信息是抗审查的,也就是说,在没有经过我们的同意下,任何一方都无法强制性地查看我们的信息。你可以相信,在Web3中,你和朋友的聊天记录是完全保密的。

所以,这种控制权,是不泄露数据隐私情况下的控制权。

3)对资产的控制权

关于对资产的控制权,其实不需要多说了。在Web2中,我们的资产保管在银行、支付宝、微信等大平台机构中,除了实体资产之外,我们的钱只是这些账户里面的数据,会不会某一天你账户里面的所有资产全部被冻结或归零呢?这个是完全有可能的。

但是,在Web3,你拥有你资产的控制权,你钱包里面的资产虽然也是一串数字,但是,只要你的私钥在,你的资产就还在,基本上谁都没法强制没收你的资产。

Web3和区块链有什么关系?

所以,看过这些Web3可能的场景之后,关于Web3,我们似乎可以这样说:

Web3是要尽可能地打破对中心化平台或机构的信任,打破他们的垄断,拿回个体对数据、信息、资产等的控制权。

这样看来,似乎Web3的内核又回到了去中心化。

而提到去中心化,我们第一个想到的自然是区块链。所以,也许我们可以说,区块链技术是实现Web3的技术手段。

目前出现的公有链项目,似乎都能归到Web3的范畴,只是因为不同项目去中心化程度的差异,导致这些项目达到Web3的程度差异而已。