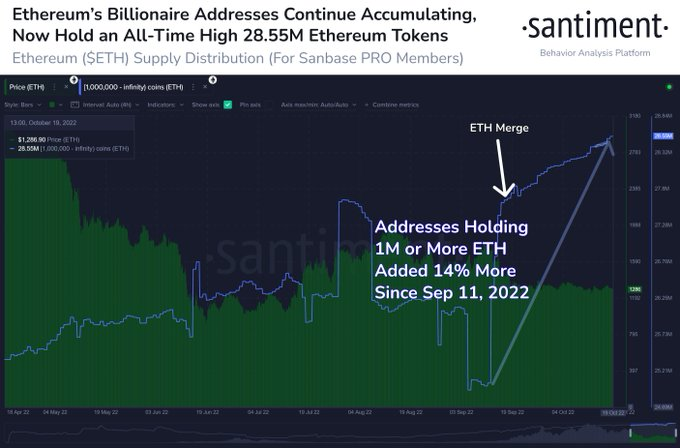

Ethereum (ETH) whale investors have continued to accumulate the second-largest cryptocurrency by market cap. Data from Santiment shows that since Sept. 11, Ethereum whale addresses that hold one million or more ETH have collectively added 3.5 million more coins.

The addition marks an increase of 14% to the ETH holdings of the billionaire whales during the period since the Merge. It also pushes the cumulative holdings of 132 or so wallets that fall in this cohort to an all-time high balance of 28.55 million ETH — worth approximately $36 billion at the time of writing.

In contrast, ETH sharks and whales — the cohort of investors below billionaire whales that hold between 100 and 1 million ETH tokens — have been selling off their ETH holdings according to previous Santiment data. Notably, the redistribution trend started shortly after the Ethereum blockchain's migration to using a proof-of-stake consensus mechanism according to previous

ETH market continues to be dominated by bearish sentiments

Despite the telling whale activity and new blockchain dynamics introduced by the Merge, the price of ETH has continued to trade largely in the red. ETH is down about 6.21% in the last month, according to data from CoinMarketCap. On the day, the token is changing hands at around $1,270, down 1.9%, at the time of writing.

However, analysts looking on the bright side have noted that the price of ETH would receive a boost when whales currently redistributing return to active accumulation. Similarly, they have opined that bullish signals persist in the network's performance in fee generation which is at a one-month-high.