Ethereum [ETH] bulls might already be facing their biggest test of Q3.

On the macro front, risk-off sentiment returned quickly after the U.S.-Iran ceasefire collapsed, triggering a sharp market-wide sell-off and highlighting how sensitive risk assets remain to geopolitical developments. A recent Ethereum trader position highlighted this volatility.

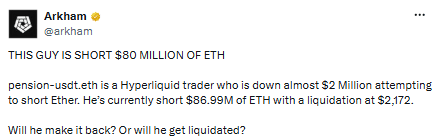

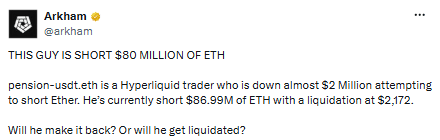

According to Arkham Intelligence, an Ethereum trader opened an $86.99 million ETH short position, with liquidation set at $2,172. Notably, the position emerged after headlines surrounding the ceasefire collapse and the U.S. cutting off a trade deal with Spain, adding further pressure to market sentiment.

This suggests the position was likely a calculated bet on further downside rather than a random short.

Adding to the market uncertainty, Arkham Intelligence also flagged a wallet movement linked to Ethereum founder Vitalik Buterin, who transferred $1.6 million worth of ETH to a new wallet. The move sparked speculation that another sell-off could be coming, especially after recent ETH transfers from Vitalik.

With the market already shifting back into risk-off mode, the combination of possible sell-side pressure and a large $80 million ETH short position has created a more cautious setup for bulls. The key question now is whether this short position is an early signal of a deeper ETH breakdown or if bulls can defend key support levels and trigger a short squeeze.

Ethereum faces a critical support test as bearish pressure rises

Ethereum sits at the crossroads of bearish market conditions and a strong technical setup.

While risk-off sentiment, rising short interest, and selling pressure support the bearish case, Ethereum is retesting the key $1,580 support level. This zone has acted as a major demand area over the past three years, triggering strong recoveries, including a +149% rally in October 2023 and a +203% in April 2025.

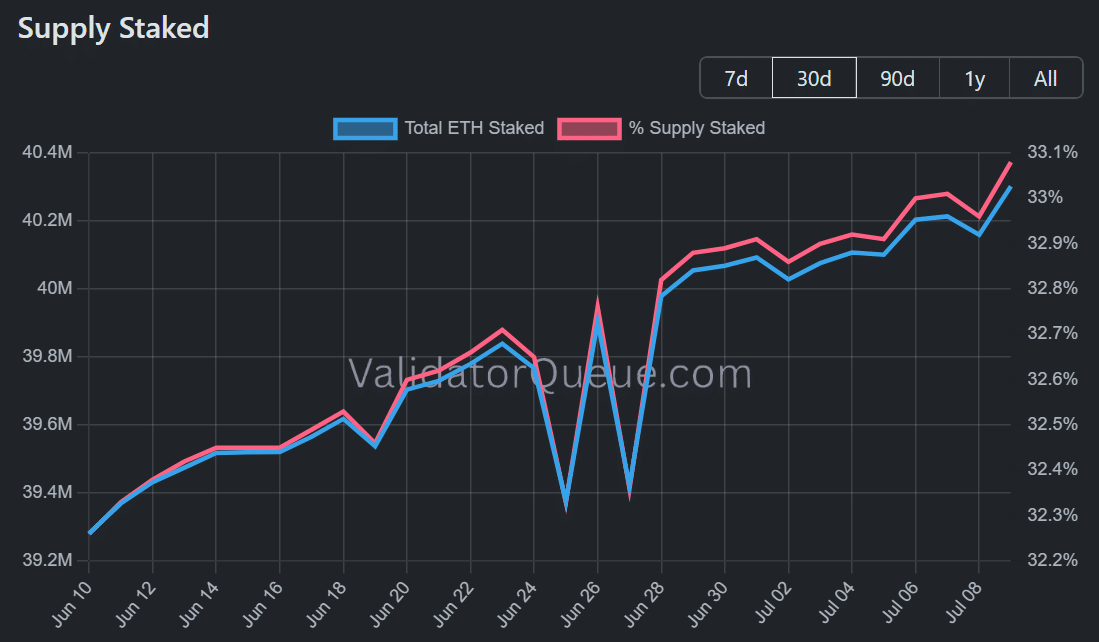

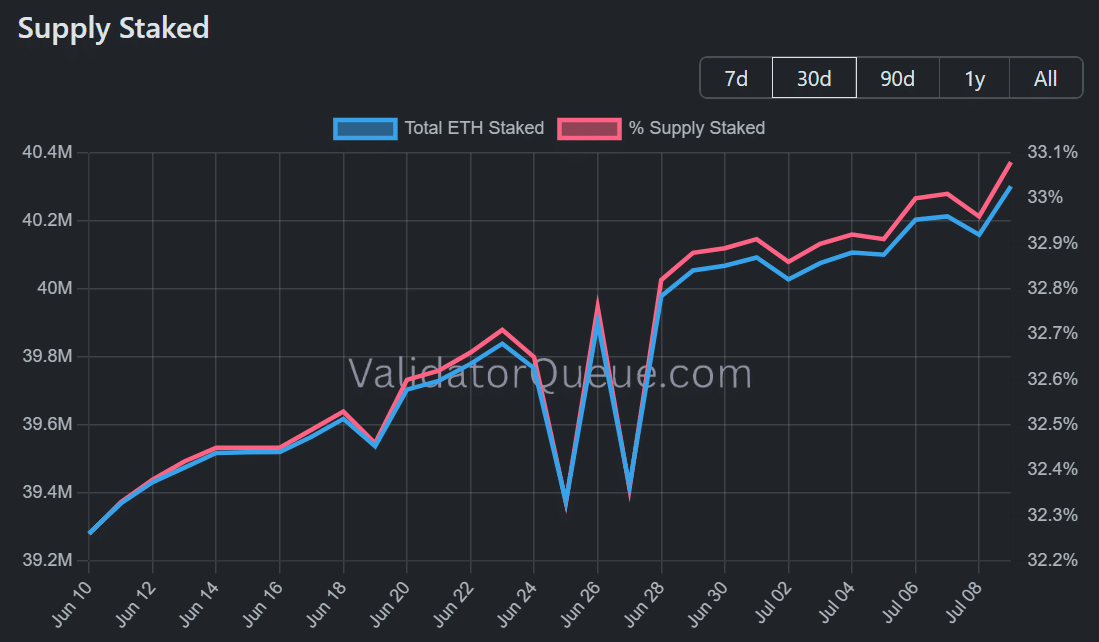

For bulls, defending $1,580 is therefore critical to keeping the bullish structure intact. Adding to the support narrative, Tom Lee-linked Bitmine continues to accumulate ETH. According to Lookonchain, Bitmine purchased another 40,000 ETH worth around $71.6 million. At the same time, staked ETH supply has reached a new all-time high of over 40 million ETH, representing around 33% of total supply.

With this accumulation, ETH’s move above $1,750 looks more than just a short-term bounce.

Instead, bulls appear to be stepping in despite the broader risk-off environment, rising short interest, and market concerns around Vitalik’s recent ETH transfer.

If this momentum continues, the $80 million short position could come under pressure, with liquidation risk building around $2.7k. In this setup, Ethereum’s technical structure could be setting up a bear trap.

Final Summary