GPT-5.6 Sol预览版发布小半个月了,首批用户内测报告终于新鲜出炉!

英伟达首席工程师用最直白最不绕弯子的话告诉你:

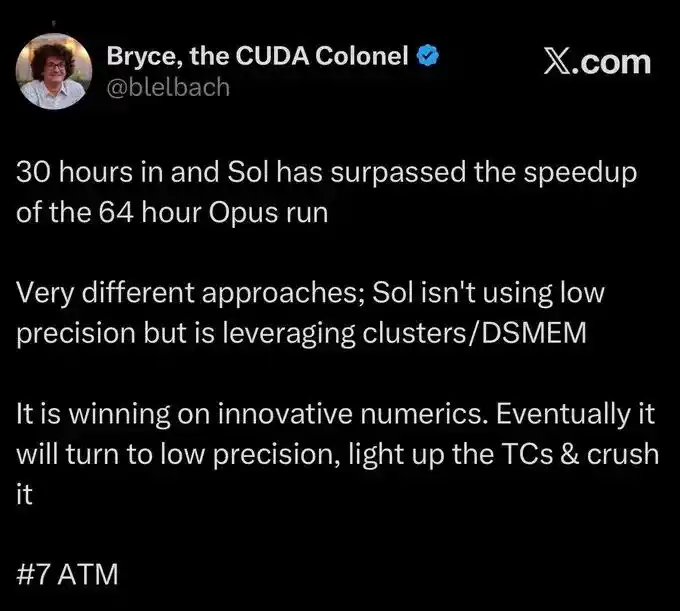

Sol很猛!30小时,就跑赢了Opus 64小时才达到的CUDA加速效果。

后续版本优化后,或将彻底碾压Opus......

网友们也没闲着,直接给整活上了,各种对(la)比(cai)层出不穷:

同样是造飞船,且看GPT-5.6这边的舱内走廊,色彩搭配和光线选择就很有科技感,明暗层次拉得开;反观5.5这边,色调偏暖偏灰,画面整体扁平了不少,怎么看都更像公司更衣室。

更甭说飞船外的宇宙场景,GPT-5.5活像马赛克聚会。(doge)

这一局GPT-5.6完胜!

要说为啥最近GPT-5.6再度热度爆表,一是老对家Fable 5复出,二就是模型终!于!动!了!

等了这么多天,终于有消息传出,模型将在最近两天正式上线。

届时不再是少数「合作伙伴」可用,这一次全体都有!

(等等党赢了~)

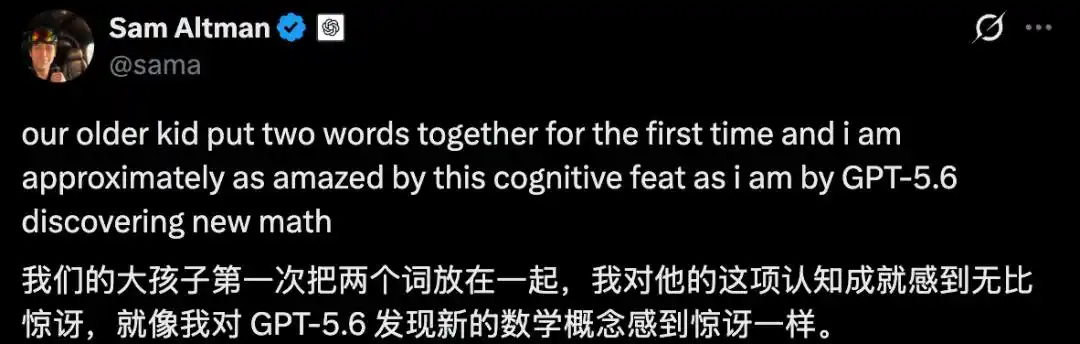

奥特曼也亲自下场凡尔赛,把气氛烘到最高潮:

我家好大儿生平第一次会说两个字的词,那种震撼程度,跟GPT-5.6发现全新数学理论时一毛一样。

没毛病!都是亲生的(doge)

首批内测结果出炉

翻了一圈内测用户的发帖,几个共识还挺一致。

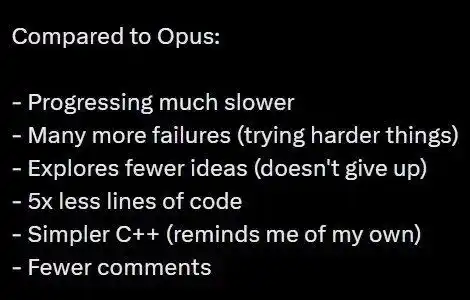

头一个,就是前面那位英伟达工程师提及的:代码更简洁,总体代码量更少。

同样一个需求,别的模型可能写一堆,Sol则明显克制得多,能三行解决绝不写五行,代码行数仅为Opus的1/5。尤其是C++,写法和真人手搓很像,注释也更少。

对于要长期维护的项目来说,优势在Sol。

当然,编码上也不是全无槽点,比如迭代推进速度较慢,失败次数也较多,因为Sol总是会去尝试难度更高的任务。

相比Opus,它试错探索的思路也更少,一旦认准方向就死磕到底。

简单来说,就是模型放弃了大量无脑试错,转为长线深耕,不追求表面输出结果好看,核心就盯着底层性能优化。

这也很符合OpenAI给Sol的定位——

面向高难度推理、复杂代码等长链路任务,尤其适合需要规划、迭代、调用工具、协调步骤的复杂工作流。

同一个提示词,丢给Sol和GPT-5.5 Pro,对比效果也很直观:

无论是交互式SVG、3D模型还是生成游戏,Sol的指令遵循和空间推理能力都更胜一筹,在一致性上也更好。

其中前端设计这块,Sol也交出了更干净整洁的答卷。

相比GPT-5.5,Sol页面布局和层次留白都拿捏得相当到位,画面也更精致。视觉这一关,Sol稳稳高分通过。

狙击Fable 5成功?

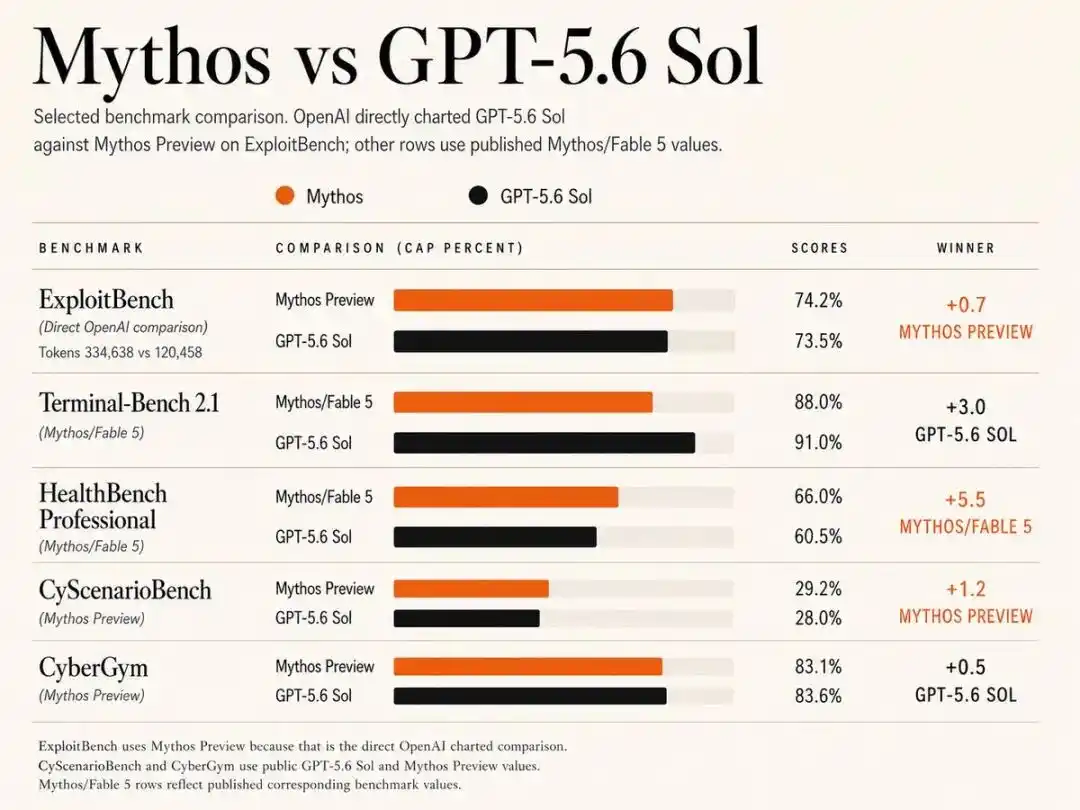

不过要说网友们最关心的问题——对比Fable 5如何?

效果可能还是略逊一筹。

在部分基准测试上,Sol和Fable 5得分持平甚至反超,但在整体模型体验和代码质量上和Fable 5还存在一定差距。

比如网友Gipp就做了一项3D FPS游戏对比。

当GPT 5.6还在努力适配游戏世界、光照和玩法时,Fable 5已经能把一个提示词转换为一款可玩的成品游戏。

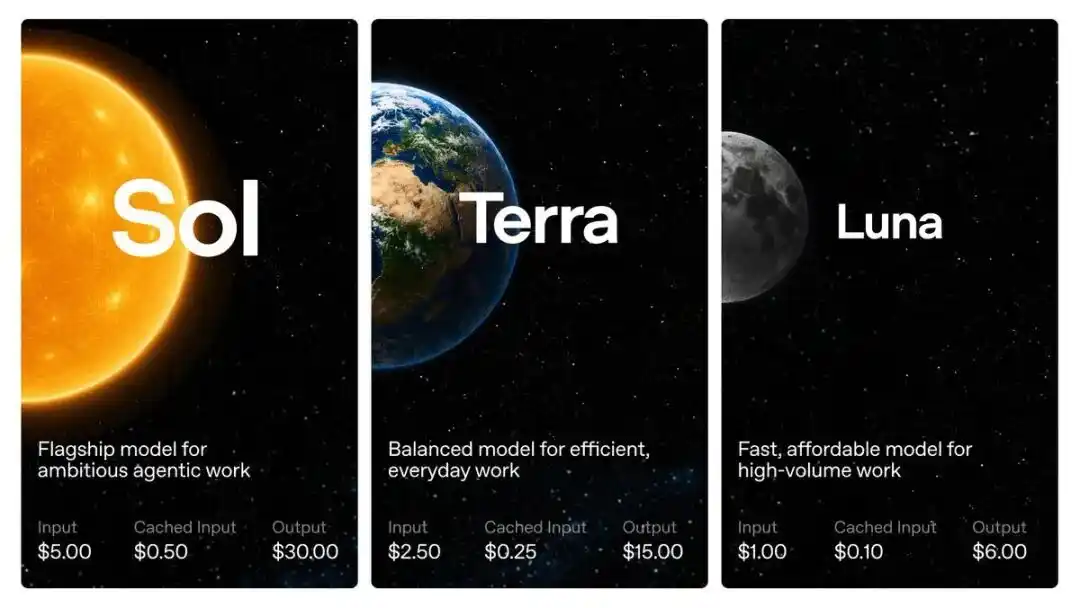

不过Fable 5的成本要高得多,每百万输入Token 10美元,输出Token 50美元,Sol的投入成本只有每百万Token 5美元,输出成本30美元。

Sol几乎便宜了一半!

所以在模型能力相近的情况下,Sol和Fable 5到底鹿死谁手还真不好说。

更要命的是安全限制,自从Fable 5被制裁后,这次二进宫出来,网友明显感觉Fable 5压根不干活了。

正常写代码、debug,稍不留神就会被系统判成高风险,任务直接降维给Opus 4.8处理,就连「raspberry里有几个r」这种问题都被拦截了。

网友们反手给Fable 5一个差评......

GPT-5.6这边,情况稍好一些。官方已经明确表示,已经添加了更强大的安全系统,也会根据不同模型能力配置不同的保护策略,限制也会比Fable 5要小一些。

总之,燥候GPT-5.6全量上线吧,到时候咱们再实测见分晓~

参考链接:

[1]https://x.com/mark_k/status/2073467892889272609?s=20

[2]https://x.com/kimmonismus/status/2073799386535006210

[3]https://x.com/gippp69/status/2073697790723596469

本文来自微信公众号“量子位”,作者:鹭羽